Quick Navigation

Report Overview

The Global Marine Battery Market size is expected to be worth around USD 2812.2 Mn by 2033, from USD 701.2 Mn in 2023, growing at a CAGR of 14.9% during the forecast period from 2024 to 2033.

Marine batteries are special starter and deep-cycle batteries designed for use in boats and other recreational equipment used on water. They are used in place of traditional lead-acid automotive batteries and employ features that support specific requirements of your boat’s engine and running systems. Some marine batteries protect against brutal operating conditions that include vibration, high temperatures, and include maintenance-free plate designs that minimize battery corrosion and fluid loss.

Electrification trends in the maritime industry have led to investments in battery-powered vessels, including ferries, cargo ships, and luxury yachts. For instance, Norway leads the global adoption of electric ferries, with over 70 operational electric or hybrid vessels as of 2024. Similarly, the defense sector is incorporating marine batteries into submarines and unmanned underwater vehicles (UUVs) for silent operation and extended endurance, further fueling market growth.

Several factors are driving the expansion of the marine battery market. Stringent environmental regulations, such as the International Maritime Organization’s (IMO) target to reduce carbon emissions by 50% by 2050, are compelling shipbuilders and operators to explore cleaner propulsion technologies. Additionally, rising fuel costs have made electric and hybrid propulsion systems economically viable, offering lower operational expenses over the vessel’s lifecycle.

Government incentives and subsidies for sustainable energy adoption also play a crucial role. For example, the European Union has allocated over €1 billion under its Green Deal to support electric vessel development and related infrastructure. The growing demand for renewable energy integration on vessels, such as solar and wind energy systems, further complements the adoption of advanced marine batteries.

Technological advancements are shaping the marine battery landscape. The market has witnessed a transition from traditional lead-acid batteries to advanced lithium-ion (Li-ion) batteries, which offer higher energy density, longer life cycles, and faster charging capabilities. The rise of solid-state batteries, projected to achieve commercialization by 2030, is expected to revolutionize the market, offering enhanced safety and performance metrics.

Key Takeaways

- Marine Battery Market size is expected to be worth around USD 2812.2 Mn by 2033, from USD 701.2 Mn in 2023, growing at a CAGR of 14.9%.

- Lithium-ion batteries held a dominant market position in the marine battery sector, capturing more than a 44.1% share.

- 100-250 Ah capacity segment held a dominant position in the marine battery market, capturing more than a 48.1% share.

- Solid-state batteries held a dominant position in the marine battery market, capturing more than a 63.2% share.

- 150 – 745 KW held a dominant position, capturing more than a 39.1% share.

- 100 – 500 WH/Kg held a dominant position, capturing more than a 64.3% share.

- Commercial sector held a dominant position in the marine battery market, capturing more than a 52.1% share.

- Original Equipment Manufacturer (OEM) channel held a dominant position in the marine battery market, capturing more than a 67.1% share.

By Battery

In 2023, Lithium-ion batteries held a dominant market position in the marine battery sector, capturing more than a 44.1% share. This dominance is primarily due to their high energy density and efficiency, which make them particularly suitable for electric and hybrid marine vehicles. Lithium-ion batteries offer longer operational life and better weight management compared to traditional marine batteries, which is essential for performance and fuel efficiency in marine applications.

Fuel cells also play a significant role in the marine battery market, offering a clean alternative to conventional marine power systems. These batteries are favored for their environmental benefits, as they produce water as a byproduct and have a higher energy yield per weight than traditional batteries. The increasing focus on reducing emissions in maritime transport is driving the adoption of fuel cell technology in this sector.

Lead-acid batteries, while being one of the oldest types of rechargeable batteries, continue to be used in the marine industry due to their robustness and cost-effectiveness. They are commonly used in starting, lighting, and ignition applications where high burst currents are required. However, their heavy weight and lower energy efficiency limit their application in newer, energy-conscious designs.

Nickel-cadmium batteries, known for their excellent life span and ability to perform under harsh conditions, are another key player in the marine battery market. They are particularly valued in safety-critical marine applications due to their reliability and stable performance across a wide range of temperatures and charging conditions.

Sodium-based batteries are emerging in the market, offering high energy capacities and safety profiles suitable for large-scale marine applications. They are considered an innovative solution, particularly for long-haul marine voyages where battery durability and energy requirements are critical.

By Capacity

In 2023, the 100-250 Ah capacity segment held a dominant position in the marine battery market, capturing more than a 48.1% share. This mid-range capacity is particularly favored in the marine industry due to its versatility in balancing size, weight, and power output, making it suitable for a wide range of marine applications from leisure boats to commercial vessels. These batteries are capable of providing adequate power for typical marine operations while maintaining a compact form factor that does not overly burden the vessel’s weight and balance.

For smaller vessels and less demanding applications, the less than 100 Ah segment also plays a critical role. These batteries are typically used in light marine applications where space is limited and the power requirements are lower. Their smaller size and lower capacity are adequate for powering basic electronic devices and light propulsion systems.

Batteries with a capacity greater than 250 Ah are essential for larger, more energy-intensive applications. These high-capacity batteries are suited for commercial and industrial vessels that require significant power for long-duration voyages with extensive electronic equipment and propulsion needs. Their higher energy storage capacity ensures that these vessels can operate over longer distances without the need for frequent recharging.

By Design

In 2023, solid-state batteries held a dominant position in the marine battery market, capturing more than a 63.2% share. This type of battery is highly valued for its safety and high energy density, characteristics that are particularly important in the marine sector where space is at a premium and safety is paramount. Solid-state batteries do not contain liquid electrolytes, which reduces the risk of leakage and increases thermal stability, thereby decreasing the likelihood of fires and explosions.

Flow batteries, while less prevalent, play a crucial role in specific marine applications that require scalability and long-duration energy storage. These batteries are unique in that they store energy in external tanks rather than within the battery container itself, which allows for more flexible scaling of capacity by simply increasing the size of the tanks. This design is advantageous for large vessels that need sustained power for extended periods, as it can provide a continuous supply of energy without degrading the battery’s core components.

By Ship Power

In 2023, the marine battery market segment for ships requiring power outputs of 150 – 745 KW held a dominant position, capturing more than a 39.1% share. This range is particularly crucial for medium to large vessels that require substantial power for propulsion and onboard systems without resorting to traditional diesel engines. These include not only commercial and cargo ships but also larger passenger ferries and specialized service vessels. The demand in this segment underscores the ongoing shift in the maritime industry towards more energy-efficient and environmentally friendly solutions that can handle significant operational demands.

For vessels with less intensive power needs, the < 75 KW and 75 – 150 KW segments cater to smaller boats, including recreational and light commercial vessels. These batteries are typically used where maneuverability and short-distance travel are common, balancing power with energy efficiency for daily operations.

Interestingly, there seems to be a typographical error in the initial data points, mentioning both ’77 – 150 KW’ and ’75 – 150 KW’ categories. Assuming this refers to a single category, these batteries fit into small to medium-sized vessels, bridging the gap between personal leisure crafts and larger commercial boats that require moderate power for longer operational capabilities.

By Energy Density

In 2023, the marine battery market for batteries with an energy density of 100 – 500 WH/Kg held a dominant position, capturing more than a 64.3% share. This range is highly favored because it balances capacity and weight effectively, making it ideal for a variety of marine applications that require moderate to high power without the significant weight penalty of lower-density batteries. Batteries in this category are typically used in vessels that need a good balance of range, power, and weight, such as medium-sized commercial boats, luxury yachts, and some types of industrial marine equipment.

For batteries with less than 100 WH/Kg, the applications tend to be more limited to smaller or less power-intensive marine crafts. These batteries are often older technologies, such as some lead-acid types, which are heavier and less efficient but still used due to their lower cost and robustness in certain marine environments.

Conversely, batteries with an energy density greater than 500 WH/Kg represent the cutting-edge of marine battery technology, catering to high-performance applications. These batteries are suitable for high-speed boats, advanced naval craft, and specialized equipment requiring high power output with minimal weight impact. This segment, while smaller, is crucial for pushing the boundaries of what marine batteries can achieve in terms of efficiency and performance.

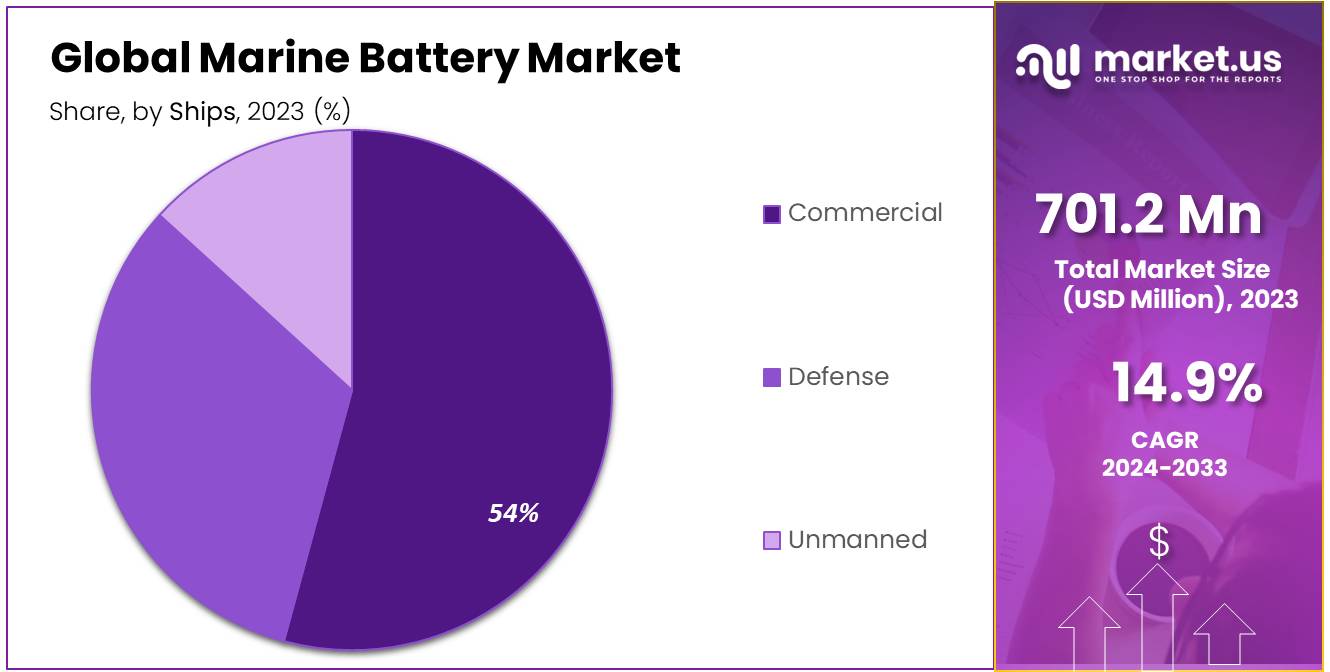

By Ships

In 2023, the commercial sector held a dominant position in the marine battery market, capturing more than a 52.1% share. This segment’s prominence is driven by the expanding use of batteries in commercial shipping, including cargo ships, tankers, and passenger ferries, as part of the industry’s push towards reducing greenhouse gas emissions and enhancing fuel efficiency. The adoption of battery-powered and hybrid systems in these vessels is instrumental in complying with international regulations aimed at curbing pollution and improving operational costs through reduced fuel consumption.

The defense sector also represents a significant portion of the marine battery market. Military ships, submarines, and other naval vessels increasingly rely on advanced battery technologies to improve stealth capabilities, reduce reliance on traditional diesel engines, and enhance endurance. Batteries in this segment need to meet stringent criteria for reliability and performance in critical and demanding environments, driving continuous innovation and technological upgrades.

The unmanned segment, which includes autonomous underwater vehicles (AUVs) and unmanned surface vehicles (USVs), is emerging as a vital area of growth. These vessels are predominantly used in scientific research, surveillance, and mapping applications where extended operational range and durability under harsh conditions are paramount. The integration of high-capacity, durable batteries is crucial to maximizing mission durations and expanding the capabilities of unmanned maritime vehicles.

By Sales Channel

In 2023, the Original Equipment Manufacturer (OEM) channel held a dominant position in the marine battery market, capturing more than a 67.1% share. This substantial market share reflects the strong preference for OEM supplied batteries in new maritime vessel constructions and factory replacements. OEM batteries are typically designed to meet specific operational requirements and rigorous safety standards, ensuring optimal compatibility and performance with the maritime technology they power. Manufacturers often collaborate directly with shipbuilders and marine engineers to integrate the latest battery technology into new ships, contributing to advancements in marine propulsion and energy systems.

The aftermarket segment, while smaller, serves a critical role in providing battery replacements and upgrades for existing vessels. This market is driven by the need for battery maintenance, performance enhancements, and replacements outside of standard OEM provisions. Aftermarket solutions offer flexibility for ship operators looking to upgrade their systems with newer technology or more cost-effective alternatives without being tied to the original manufacturer. The aftermarket also caters to older vessels that may require specific types of batteries no longer supplied by OEMs, ensuring that a wider range of ships can maintain operational efficiency and compliance with environmental regulations.

Key Market Segments

By Battery

- Lithium-ion

- Fuel Cell

- Lead Acid Battery

- Nickel Cadmium

- Sodium-based

By Capacity

- Less than 100 Ah

- 100-250 Ah

- Greater than 250 Ah

By Design

- Solid-state Battery

- Flow Battery

By Ship Power

- < 75 KW

- 75 – 150 KW

- 150 – 745 KW

- 77 – 150 KW

By Energy Density

- <100 WH/Kg

- 100 – 500 WH/Kg

- >500 WH/Kg

By Ships

- Commercial

- Defense

- Unmanned

By Sales Channel

- OEM

- After Market

Drivers

Increasing Adoption of Electric and Hybrid Technologies in Maritime Transport

A major driving factor for the growth of the marine battery market is the increasing adoption of electric and hybrid propulsion systems in ships. This trend is largely driven by the maritime industry’s need to meet stringent environmental regulations and reduce greenhouse gas emissions. The International Maritime Organization (IMO) has set ambitious targets to cut sulfur emissions and other pollutants, pushing the industry towards more sustainable and cleaner energy sources.

In 2023, the marine battery market witnessed substantial growth, driven by the rising demand for electric passenger ships, ferries, and commercial vessels that rely on advanced battery technologies to operate efficiently and sustainably. The shift towards electric and hybrid vessels is not only a response to regulatory pressures but also aligns with broader environmental sustainability goals within the sector.

This transition is supported by innovations in battery technology that enhance the energy density and efficiency of marine batteries, making them more capable of meeting the power and range requirements of modern ships. These technological advancements are crucial in overcoming previous limitations and making electric propulsion a viable option for a wider range of maritime applications.

Furthermore, the market’s expansion is facilitated by the increasing interest in maritime tourism and recreational boating, where there is a growing preference for quieter, cleaner, and more fuel-efficient vessels. This consumer-driven demand further accelerates the adoption of marine batteries in the commercial shipping sector.

The development and expansion of the marine battery market are underpinned by continuous improvements in battery technology, increased investment in research and development by major industry players, and supportive government policies aimed at promoting cleaner marine transportation solutions.

Restraints

High Initial Costs: A Major Barrier to Marine Battery Adoption

One of the principal restraining factors in the marine battery market is the high initial costs associated with these advanced technologies. Marine batteries, especially those like lithium-ion and solid-state batteries, are typically more expensive to produce than traditional fuel systems. This financial hurdle can deter smaller vessel operators and shipbuilders from transitioning to battery-powered solutions, despite the long-term cost savings and environmental benefits these technologies offer.

The significant upfront investment required for marine batteries is a considerable challenge, particularly for operators in developing regions or those with limited budgets. These costs not only encompass the batteries themselves but also the infrastructure needed for charging and maintenance, which can be substantial.

Moreover, the marine industry’s stringent safety and performance standards further elevate the initial costs, as marine batteries must be highly durable and reliable to withstand the harsh marine environment. While the long-term operational costs of using marine batteries—such as reduced fuel consumption and lower maintenance expenses—can offset the initial outlay, the initial financial barrier remains a significant impediment to wider adoption.

This situation underscores the need for continued technological advancements that can reduce costs, as well as potential financial incentives from governments to make the initial switch more feasible for more operators. These measures could help mitigate the impact of high initial costs and support the broader uptake of marine batteries in the industry.

Opportunity

Expanding Electrification in Maritime Transport

A significant growth opportunity within the marine battery market is the ongoing expansion of electrification in maritime transport. This shift is propelled by the need to meet stringent environmental regulations and the maritime industry’s push toward sustainability. Electrification in the marine sector not only helps reduce carbon emissions but also enhances the efficiency of marine operations.

The global marine battery market, valued at approximately USD 1.06 billion in 2023, is expected to experience robust growth, projecting to reach about USD 5.40 billion by 2032, growing at a compound annual growth rate (CAGR) of 19.10% from 2024 to 2032. This growth is driven by increasing investments in electric and hybrid propulsion technologies across commercial and recreational vessels. These advancements are crucial as they cater to both environmental mandates and the industry’s operational demands for more effective power solutions.

In regions like Europe, which is projected to hold the highest market share, the adoption of electric propulsion is particularly strong due to advanced marine infrastructure and regulatory support from governments encouraging the use of cleaner energy sources. North America is also seeing significant growth, driven by investments in maritime technology and increased adoption of electric propulsion by government agencies and private operators.

This ongoing transition to electrification presents substantial opportunities for marine battery providers, particularly those who continue to innovate and adapt their offerings to meet the increasingly sophisticated requirements of modern maritime operations.

Trends

Advancements in Battery Technology and Electrification

A major trend shaping the marine battery market is the rapid advancements in battery technology coupled with the increasing shift towards electrification in the maritime industry. This trend is driven by the need for more environmentally friendly and efficient maritime operations, alongside stringent environmental regulations pushing the industry towards cleaner energy sources.

Solid-state and lithium-ion batteries are at the forefront of this trend, offering higher energy densities, greater efficiency, and improved safety profiles over traditional marine batteries. Solid-state batteries, in particular, are gaining traction due to their increased safety and stability, making them ideal for use in marine environments where reliability is crucial. Meanwhile, lithium-ion batteries are favored for their long life spans and ability to efficiently handle high energy demands, making them suitable for a wide range of marine applications, from commercial ships to luxury yachts and naval vessels.

The adoption of these advanced battery technologies is facilitated by their potential to power hybrid and fully electric propulsion systems, which are becoming increasingly prevalent in the maritime sector. This shift not only helps reduce emissions but also lowers the operating costs associated with fuel consumption and engine maintenance.

Furthermore, the integration of renewable energy sources for battery charging is emerging as a key trend. The use of solar, wind, and other renewable energy forms to charge marine batteries enhances the sustainability and efficiency of maritime operations, aligning with global efforts to reduce the carbon footprint of the shipping industry.

This combination of technological advancements and a shift towards more sustainable practices is creating significant growth opportunities within the marine battery market, as stakeholders are keen to invest in solutions that meet both regulatory requirements and the growing environmental consciousness among consumers and businesses alike.

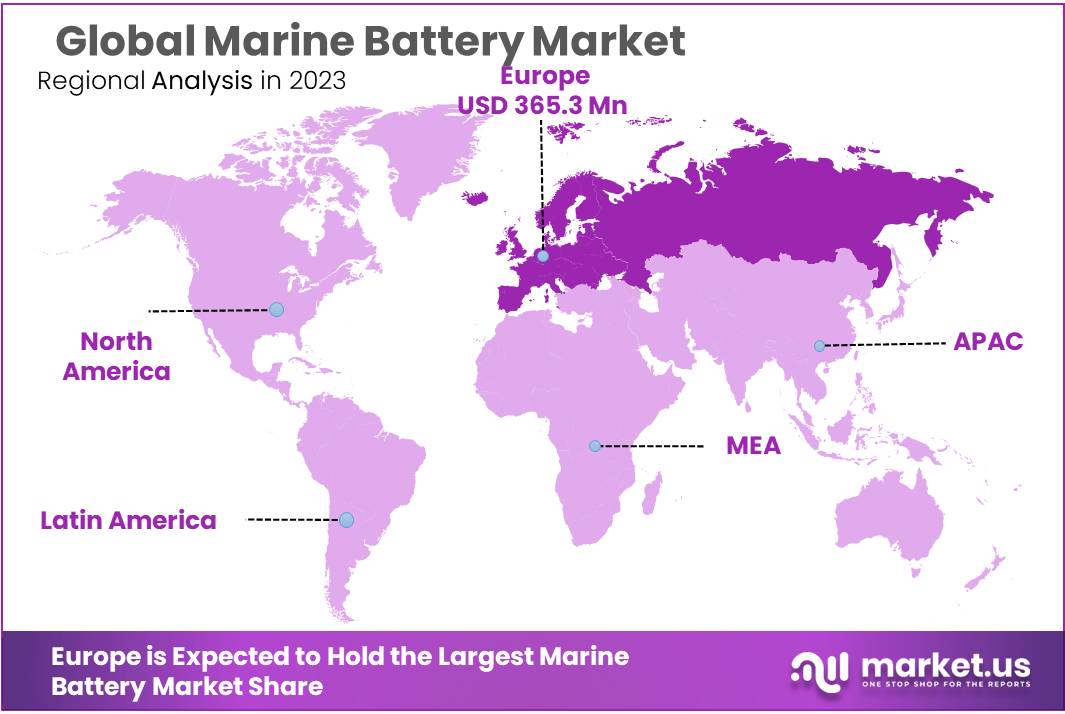

Regional Analysis

In 2023, Europe dominated the marine battery market, holding a 52.1% share, valued at approximately USD 365.3 million. This region leads due to its robust maritime industry, stringent environmental regulations, and aggressive adoption of electric propulsion systems across its vast commercial fleet. European market leadership is supported by extensive investments in maritime technology and a strong network of marine battery manufacturers and shipbuilders.

North America, while not the largest market, is experiencing substantial growth, driven by increasing government initiatives towards sustainability and the electrification of marine vessels. The region’s focus on reducing emissions from the maritime sector fuels the demand for advanced marine battery solutions, particularly in the United States and Canada, where there is also a rising trend in recreational boating that employs hybrid and electric systems.

Asia Pacific is witnessing moderate growth in the marine battery market. The growth is primarily driven by the expanding commercial shipping activities and maritime tourism in countries like China, Japan, and South Korea. The region is home to several leading battery manufacturers, which supports local market expansion and technological innovations in marine battery systems.

The Middle East & Africa and Latin America are seeing slower growth compared to other regions. However, these areas hold potential due to increasing commercial marine activities and a gradual shift towards adopting more sustainable marine operations. The development of maritime infrastructure and regulatory frameworks supporting marine battery usage will be crucial for the growth in these markets.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The marine battery market is characterized by a dynamic array of key players who are pivotal in shaping the industry’s landscape through technological innovations and expansive product offerings. Akasol AG, Corvus Energy, and EnerSys are standout contributors, known for their advanced battery solutions that cater to a wide range of marine applications, from commercial shipping to leisure crafts. These companies are at the forefront of developing high-density energy storage solutions that enhance the efficiency and sustainability of marine operations.

Companies like Leclanché SA and Wärtsilä Oyj Abp are also instrumental, focusing on the integration of hybrid and fully electric systems in maritime vessels, which aligns with global efforts to reduce maritime emissions. On the other hand, firms such as Exide Industries Ltd. and G.S. Yuasa Corporation provide robust and reliable batteries that support both conventional and innovative applications in the marine sector. These manufacturers are deeply involved in research and development to push the boundaries of battery technology, improving safety, longevity, and performance.

In addition, newer entrants like Echandia Marine AB and Shift Clean Energy are making significant strides by targeting niche markets within the marine industry, such as submarines and specialized naval vessels, with tailor-made battery systems. This strategic focus on specialized segments allows these companies to carve out distinct positions in the market, ensuring continued growth and innovation within the broader marine battery ecosystem.

Top Key Players

- Akasol AG

- Corvus Energy

- Echandia Marine AB

- EnerSys

- EST Floattech

- Exide Industries Ltd.

- Furukawa Battery Solutions Co. Ltd.

- G.S. Yuasa Corporation

- HBL Power Systems Ltd.

- Johnson Controls International

- Leclanché SA

- Lifeline Batteries

- Powertech Systems

- Saft Groupe S.A.

- Saft SA

- Sensata Technolgies Inc.

- Shift Clean Energy

- Siemens AG

- Systems Sunlight SA

- Toshiba Corporation

- Wärtsilä Oyj Abp

Recent Developments

In 2024, Akasol AG continues to lead innovations in the marine battery market by enhancing its battery systems to support the electrification of the maritime industry.

In 2024 Corvus Energy, the company has notably contributed to reducing over 10 million tons of CO2 emissions since its first battery system installation in 2013, highlighting its significant impact on environmental sustainability in shipping.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 701.2 Mn |

| Forecast Revenue (2033) | USD 2812.2 Mn |

| CAGR (2024-2033) | 14.9% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Battery (Lithium-ion, Fuel Cell, Lead Acid Battery, Nickel Cadmium, Sodium-based), By Capacity (Less than 100 Ah, 100-250 Ah, Greater than 250 Ah), By Design (Solid-state Battery, Flow Battery, By Ship Power (< 75 KW, 75 – 150 KW, 150 – 745 KW, 77 – 150 KW), By Energy Density (<100 WH/Kg, 100 – 500 WH/Kg, >500 WH/Kg), By Ships ( Commercial, Defense, Unmanned), By Sales Channel (OEM, After Market) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Akasol AG, Corvus Energy, Echandia Marine AB, EnerSys, EST Floattech, Exide Industries Ltd., Furukawa Battery Solutions Co. Ltd., G.S. Yuasa Corporation, HBL Power Systems Ltd., Johnson Controls International, Leclanché SA, Lifeline Batteries, Powertech Systems, Saft Groupe S.A., Saft SA, Sensata Technolgies Inc., Shift Clean Energy, Siemens AG, Systems Sunlight SA, Toshiba Corporation, Wärtsilä Oyj Abp |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |