Quick Navigation

- Report Overview

- Key Takeaways

- By Project Type Analysis

- By Source Analysis

- By Equipment Analysis

- By Plant Size Analysis

- By Location Analysis

- By Technology Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

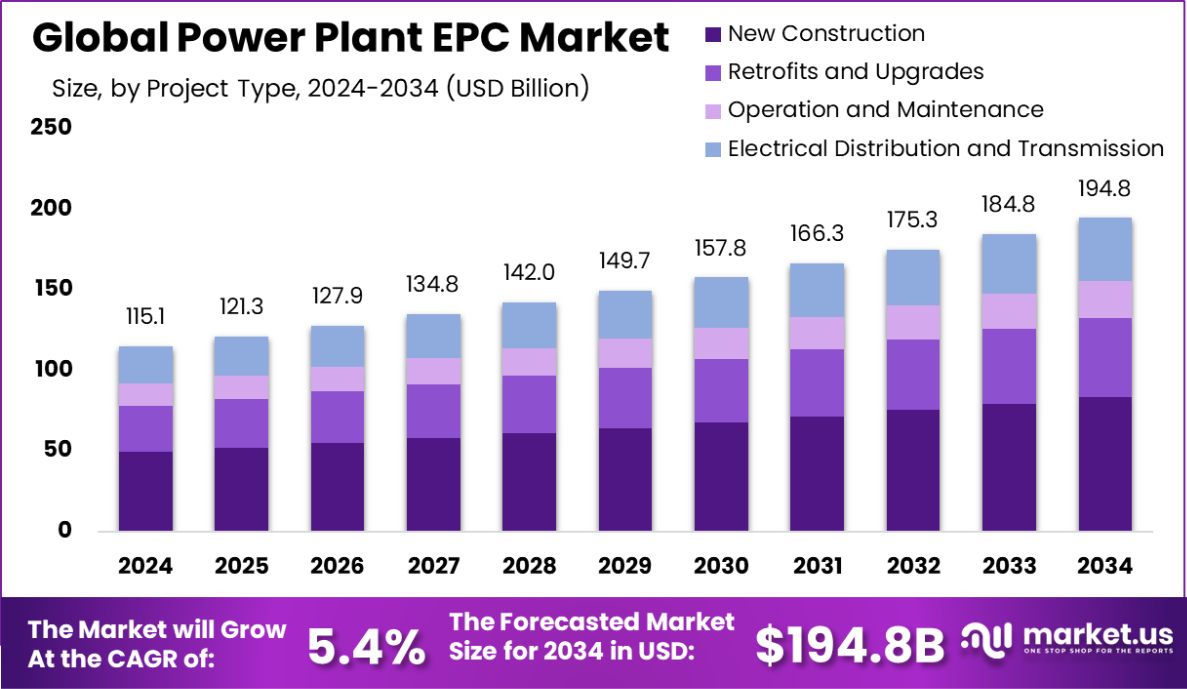

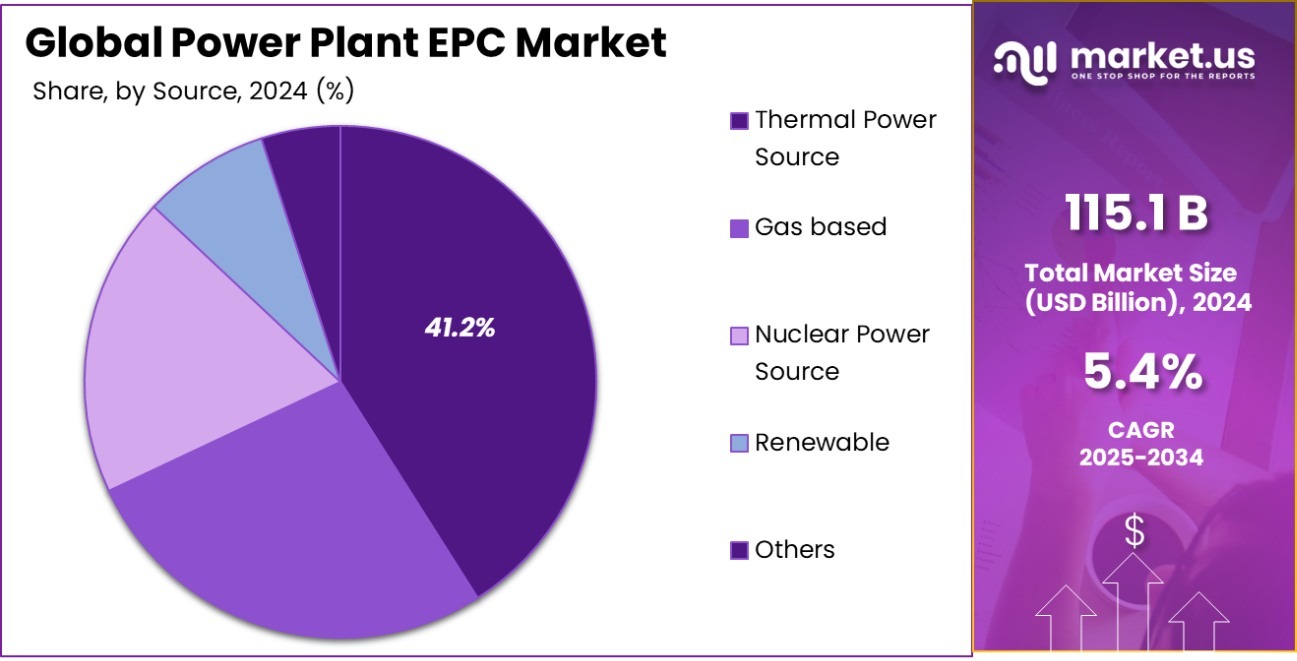

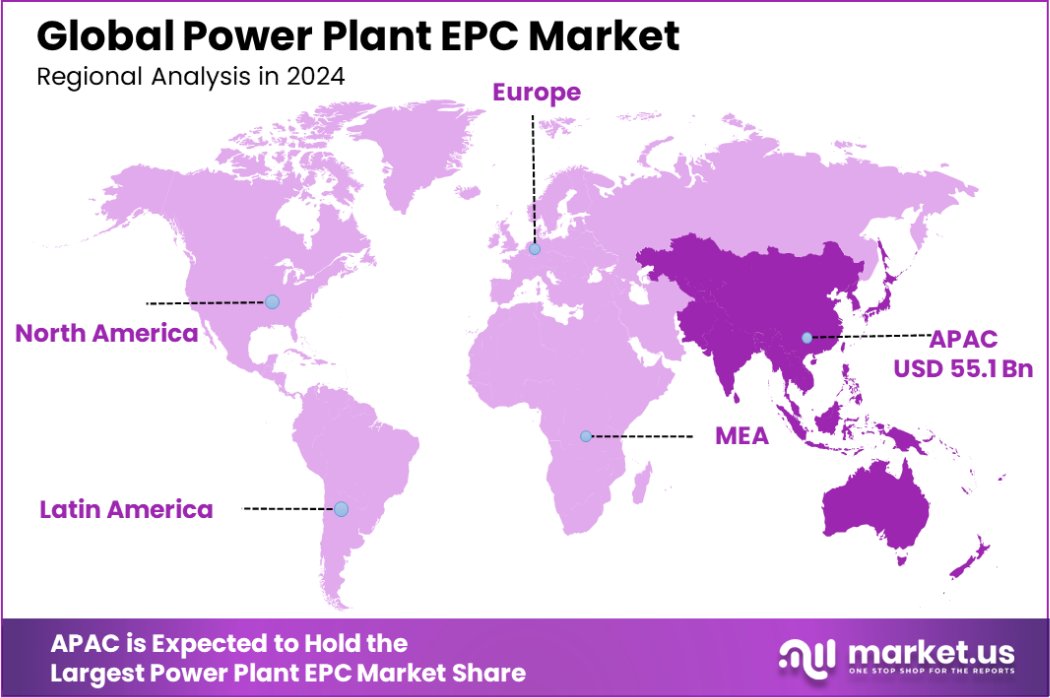

Global Power Plant EPC Market is expected to be worth around USD 194.8 Billion by 2034, up from USD 115.1 Billion in 2024, and grow at a CAGR of 5.4% from 2025 to 2034. Asia-Pacific leads the Power Plant EPC Market at 47.9%, USD 55.1 Bn.

Power Plant EPC (Engineering, Procurement, and Construction) refers to a form of contracting arrangement used in the energy industry. In this model, an EPC contractor is responsible for all the activities from design, procurement, and construction, to commissioning and handover of the project to the end-user or owner. The key advantage of this setup is that it provides a single point of responsibility which tends to reduce risks and overall costs associated with managing multiple contracts.

The Power Plant EPC market encompasses the comprehensive services offered by EPC contractors specific to power generation facilities. This market is driven by the demand for new power plants and the need for updating or expanding existing facilities. It includes a variety of power generation technologies like fossil fuels, nuclear, and renewables (solar, wind, hydroelectric).

One significant growth factor in the Power Plant EPC market is the global increase in energy demand fueled by economic growth and industrialization, particularly in developing countries. As these economies expand, the demand for reliable power sources drives investments in new power plants.

The demand within the Power Plant EPC market is also propelled by the need for more efficient and environmentally friendly power generation. Stricter environmental regulations worldwide are pushing power producers to adopt cleaner and more sustainable technologies, which often require new constructions or significant modifications to existing power plants.

There is substantial opportunity in the Power Plant EPC market for the integration of renewable energy sources. With a global push towards sustainability, there is a growing shift from traditional fossil-fuel-based power plants to renewable energy projects. This transition is supported by government incentives and public demand for greener energy solutions, opening new avenues for EPC contractors specializing in renewable energy projects.

GE Power, a leading gas turbine manufacturer, boasted a significant installed capacity of 593,233 MW as of March 31, 2022. Remarkably, combined-cycle gas turbine (CCGT) plants, according to asme.org, achieve up to 64% efficiency, with theoretical potential reaching 70%.

In 2025, Saudi Arabia plans to tender 6 GW of gas-fired CCGT projects with carbon capture and storage (CCS) readiness, as reported by Zawya. Additionally, the gas turbine world highlights that benchmark prices for the complete EPC scope of combined cycle plants vary from $1,579/KW for 34MW to $670/KW for 1,680MW outputs.

Key Takeaways

- Global Power Plant EPC Market is expected to be worth around USD 194.8 Billion by 2034, up from USD 115.1 Billion in 2024, and grow at a CAGR of 5.4% from 2025 to 2034.

- In the Power Plant EPC Market, new construction projects represent a substantial 43.3% share of the sector.

- Thermal power sources dominate, comprising 41.2% of the market, highlighting traditional energy’s enduring relevance.

- Gas turbines, crucial for efficient power generation, account for 35.7% of equipment utilized in this market.

- Large-scale power plants dominate the landscape, making up 38.5% of the Power Plant EPC Market.

- A significant majority, 78.2%, of EPC projects are executed in onshore locations, underscoring their popularity.

- In terms of technology, combined cycle systems lead with a 42.2% share, promoting efficiency in power generation.

- In 2024, Asia-Pacific dominated the Power Plant EPC Market, holding 47.9% and USD 55.1 billion.

By Project Type Analysis

New construction projects dominate 43.3% of the Power Plant EPC Market.

In 2024, New Construction held a dominant market position in the “By Project Type” segment of the Power Plant EPC Market, commanding a significant 43.3% share. This substantial portion underscores the ongoing investments in the development of new power generation facilities globally. The drive behind this trend largely stems from the increased energy demands of growing populations and expanding industrial sectors.

Moreover, the shift towards renewable energy sources to meet environmental targets has necessitated the construction of new infrastructure capable of harnessing wind, solar, and hydro energy. This focus on new construction is indicative of the market’s response to both economic stimuli and regulatory frameworks promoting sustainable development. As a result, EPC contractors with capabilities in cutting-edge technologies and project management are particularly well-positioned to capitalize on these opportunities.

By Source Analysis

Thermal power sources represent 41.2% of the Power Plant EPC Market.

In 2024, Thermal Power Source held a dominant market position in the “By Source” segment of the Power Plant EPC Market, with a 41.2% share. This leadership underscores the continuing reliance on thermal power generation despite the global shift towards renewable sources. Thermal power plants, which primarily use coal, gas, and oil to generate electricity, remain critical in regions where these resources are abundant and economically viable.

The high share indicates significant ongoing investments in these technologies, particularly in emerging economies where infrastructure and regulatory frameworks for renewables are still developing. Furthermore, advancements in thermal technology aimed at increasing efficiency and reducing emissions are likely to sustain its preference in the power generation mix.

EPC contractors within this segment continue to find substantial opportunities, especially in retrofitting and upgrading existing facilities to meet modern environmental standards.

By Equipment Analysis

Gas turbines equipment holds a 35.7% share in the Power Plant EPC Market.

In 2024, Gas Turbines held a dominant market position in the “By Equipment” segment of the Power Plant EPC Market, with a 35.7% share. This prominent position highlights the significant role gas turbines play in modern power generation. Known for their efficiency and shorter ramp-up times compared to traditional thermal power plants, gas turbines are increasingly favored for their ability to meet fluctuating energy demands quickly.

Their adoption is further driven by the global push for reduced carbon footprints, as gas turbines typically emit fewer pollutants than coal-fired plants. The substantial market share also reflects ongoing investments in natural gas infrastructure and technological advancements that enhance turbine efficiency and environmental compatibility.

EPC providers specializing in gas turbine technology are well-positioned to benefit from these trends, particularly in regions where natural gas is plentiful and relatively inexpensive.

By Plant Size Analysis

Large plant sizes account for 38.5% of the Power Plant EPC Market.

In 2024, the “Large” category held a dominant market position in the “By Plant Size” segment of the Power Plant EPC Market, with a 49.2% share. This significant share indicates a strong preference for large-scale power projects, reflecting the ongoing need for substantial, high-output facilities to meet the growing global demand for electricity. Large power plants, typically characterized by their extensive capacity to produce hundreds of megawatts, are essential in powering major cities and industrial sectors.

The dominance of large plants is also a testament to the economies of scale that can be achieved through bigger investments, which often lead to lower per-megawatt costs of electricity generation. This trend underscores the strategic focus of governments and private sectors on establishing robust infrastructure capable of securing energy supply and supporting economic growth on a large scale.

EPC contractors who excel in managing and executing large-scale projects continue to see expansive opportunities in this segment, driven by both developed and emerging economies.

By Location Analysis

Onshore locations lead with 78.2% in the Power Plant EPC Market.

In 2024, Onshore held a dominant market position in the “By Location” segment of the Power Plant EPC Market, with a 78.2% share. This overwhelming preference for onshore locations is driven by the logistical, regulatory, and economic advantages that these settings offer over their offshore counterparts. Onshore power plants are typically easier and less costly to construct and maintain, given the accessibility of sites and the availability of infrastructure such as roads and utilities.

Additionally, the regulatory hurdles for onshore project approvals tend to be less stringent than for offshore projects, speeding up the project lifecycle from planning to execution. The substantial share of onshore projects underscores the critical role they play in meeting the bulk of the global energy demand, particularly in regions where land availability is not a constraint.

EPC contractors specializing in onshore projects continue to benefit from the scale and scope of these developments, leveraging established networks and expertise to expand their market presence.

By Technology Analysis

Combined cycle technology comprises 42.2% of the Power Plant EPC Market.

In 2024, Combined Cycle held a dominant market position in the “By Technology” segment of the Power Plant EPC Market, with a 42.2% share. This prominence is largely attributed to the high efficiency and lower environmental impact of combined-cycle technology compared to conventional single-cycle processes.

In a combined cycle plant, the waste heat from the gas turbine is used to produce steam to generate additional power through a steam turbine, significantly enhancing the overall efficiency of power generation.

This technology aligns well with global initiatives aimed at reducing carbon emissions and improving energy efficiency. The substantial market share reflects the growing preference for technologies that can deliver higher output with reduced fuel consumption and emissions.

As the demand for sustainable and efficient energy solutions continues to rise, EPC contractors with expertise in combined cycle projects are likely to see increased opportunities, especially in markets that are actively transitioning towards cleaner energy sources.

Key Market Segments

By Project Type

- New Construction

- Retrofits and Upgrades

- Operation and Maintenance

- Electrical Distribution and Transmission

By Source

- Thermal Power Source

- Gas based

- Nuclear Power Source

- Renewable

- Others

By Equipment

- Gas Turbines

- Steam Turbines

- Generators

- Others

By Plant Size

- Small

- Medium

- Large

- Ultra-Large

By Location

- Onshore

- Offshore

By Technology

- Combined Cycle

- Coal-Fired

- Nuclear

- Gas Turbine

- Renewable Energy

Driving Factors

Increasing Global Energy Demand Fuels Market Growth

The primary driving factor for the Power Plant EPC Market is the escalating global demand for energy. As populations grow and economies expand, the need for a reliable and continuous power supply intensifies. This trend is particularly pronounced in developing regions where urbanization, industrialization, and improving living standards are rapidly increasing energy consumption.

To meet this burgeoning demand, governments and private companies are investing heavily in the construction of new power plants and the expansion of existing facilities. This dynamic has created a robust environment for EPC contractors, who are essential in designing, constructing, and commissioning power facilities efficiently. Their expertise in managing complex projects from inception to completion makes them pivotal in the global push to scale up power generation capacities.

Restraining Factors

High Initial Investment Hinders Power Plant Projects

One of the most significant restraining factors in the Power Plant EPC Market is the high initial capital requirement. Establishing a power plant, regardless of its type (thermal, hydro, nuclear, or renewable), involves substantial upfront investments. These costs cover a wide range of needs, including technological infrastructure, land acquisition, regulatory compliance, and labor.

For many regions, especially in economically developing countries, securing sufficient funding can be a major challenge. This barrier not only delays the commencement of new projects but can also deter investors from committing to power generation projects. The high initial outlay can slow down the expansion of energy infrastructure, impacting the overall growth of the EPC market as potential projects remain unrealized due to financial constraints.

Growth Opportunity

Renewable Energy Projects Offer Expansive Growth Opportunities

A significant growth opportunity within the Power Plant EPC Market lies in renewable energy projects. The global shift towards sustainability is prompting an increased focus on renewable sources such as solar, wind, hydro, and biomass. This transition is supported by governmental policies, environmental regulations, and public demand for cleaner energy options.

As countries aim to reduce their carbon footprints and meet international climate targets, the investment in renewable energy infrastructure is rapidly growing. For EPC contractors, this trend presents a lucrative chance to engage in numerous projects involving the design and construction of renewable energy facilities. These projects not only promise continued business but also offer contractors a chance to innovate and lead in the burgeoning green energy sector.

Latest Trends

Digitalization and Automation Enhance Power Plant Efficiency

A leading trend in the Power Plant EPC Market is the increasing incorporation of digital technologies and automation in power plant operations. This trend is revolutionizing the way power plants are constructed, monitored, and maintained. By integrating advanced digital tools like AI, IoT, and big data analytics, EPC contractors can enhance operational efficiency, improve safety, and reduce construction times.

These technologies enable real-time monitoring and predictive maintenance, which significantly lowers downtime and extends the lifespan of power facilities. Additionally, automation in various construction processes helps in reducing human error and optimizing resource allocation. This digital shift not only streamlines project execution but also supports the energy sector’s drive towards sustainability by ensuring cleaner and more efficient power generation.

Regional Analysis

In 2024, the Asia-Pacific Power Plant EPC Market captured 47.9% of the market, valued at USD 55.1 billion.

In 2024, Asia-Pacific dominated the Power Plant EPC Market, accounting for 47.9% market share and reaching a valuation of USD 55.1 billion. The region’s dominance is primarily driven by large-scale investments in power infrastructure, particularly in China, India, and Southeast Asia, where electricity demand continues to surge due to rapid urbanization and industrial expansion. Governments are heavily investing in renewable energy projects, coal-fired plants, and gas-based power stations, further strengthening the EPC market.

North America remains a key player, with significant EPC activities focused on renewable energy and grid modernization. The United States and Canada are witnessing an increasing number of solar, wind, and natural gas-based power plant projects, supported by favorable policies and private sector investments.

Europe continues to advance in clean energy EPC projects, with countries like Germany, France, and the UK driving developments in solar, wind, and hydrogen-based power plants. The region’s strong focus on sustainability and strict emission norms contribute to EPC market growth.

In Latin America and the Middle East & Africa, rising energy demands and government-led infrastructure initiatives are propelling power plant EPC investments. Brazil, Saudi Arabia, and the UAE are key markets experiencing increased construction of thermal and renewable power plants, ensuring steady regional growth.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, the global Power Plant EPC Market saw significant contributions from several key players, each bringing unique strengths and strategic focuses that shaped their market positions. AECOM and Bechtel continued to leverage their vast international experience and technological prowess to drive innovation in project execution. These companies have been pivotal in integrating digital tools, enhancing efficiency, and reducing environmental impacts across global projects.

Babcock & Wilcox and Doosan Heavy Industries and Construction remained leaders in thermal and combined cycle projects, capitalizing on the resurgence of interest in efficient, cleaner technologies in traditional power generation. Their expertise in advanced boiler technology and heavy industry equipment has positioned them well to handle the demands of modernizing existing facilities and constructing state-of-the-art new power plants.

Bharat Heavy Electricals Ltd. (BHEL) and China Energy Engineering Corporation (CEEC) dominated the market in their respective regions, underpinned by strong government relationships and extensive local market knowledge. BHEL continued to be a major player in India’s push towards expanding its power generation capacity, while CEEC played a critical role in China’s extensive energy infrastructure projects, focusing on everything from renewables to thermal power.

Black & Veatch and Burns & McDonnell benefited from their strong focus on sustainability and renewable projects, aligning with global trends towards green energy. Their projects often featured innovative use of technologies to improve project delivery and operational efficiency.

China National Electric Wire and Cable I/E Corp. and Datang International Power Generation Company Limited focused on expanding their international footprints. They pursued projects that bolstered their expertise in handling diverse energy sources, particularly in emerging markets where energy demand is rapidly growing. Their strategic movements included forming alliances and partnerships to leverage local market insights and enhance their service offerings globally.

Top Key Players in the Market

- AECOM

- Babcock Wilcox

- Bechtel

- Bharat Heavy Electricals Ltd.

- Black Veatch

- Burns McDonnell

- China Energy Engineering Corporation

- China National Electric Wire and Cable I/E Corp

- Datang International Power Generation Company Limited

- Doosan Heavy Industries and Construction

- Fluor

- GE Power

- Hitachi Power Systems

- Jacobs

- KBR

- Larsan and Toubro Ltd.

- Mitsubishi Heavy Industries

- Petrofac

- Saipem

- Samsung Engineering

- Sargent Lundy

- ShanDong Energy Group CO. Ltd.

- Siemens

- SK Engineering and Construction

- Sterlite Power Transmission Ltd.

- TATA Project

- Technip

- Thermax Global

- Toshiba

- Worley Parsons

Recent Developments

- In February 2025, Babcock & Wilcox Construction Co. secured $35 million in contracts for maintenance and service work at power plants and industrial facilities in North America.

- In September 2024, Bharat Heavy Electricals Ltd. (BHEL) received an EPC order worth INR 6,100 crore (approximately $730 million) from NTPC Ltd. for a 1×800 MW thermal power project in Chhattisgarh, India.

- In February 2024, Sterlite Power secured new orders worth INR 2,250 crores (approximately $270 million) for various power transmission products and services, including EPC contracts

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 115.1 Billion |

| Forecast Revenue (2034) | USD 194.8 Billion |

| CAGR (2025-2034) | 5.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Project Type (New Construction, Retrofits and Upgrades, Operation and Maintenance, Electrical Distribution and Transmission), By Source (Thermal Power Source, Gas based, Nuclear Power Source, Renewable, Others), By Equipment (Gas Turbines, Steam Turbines, Generators, Others), By Plant Size (Small, Medium, Large, Ultra-Large), By Location (Onshore, Offshore), By Technology (Combined Cycle, Coal-Fired, Nuclear, Gas Turbine, Renewable Energy) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | AECOM, Babcock Wilcox, Bechtel, Bharat Heavy Electricals Ltd., Black Veatch, Burns McDonnell, China Energy Engineering Corporation, China National Electric Wire and Cable I/E Corp, Datang International Power Generation Company Limited, Doosan Heavy Industries and Construction, Fluor, GE Power, Hitachi Power Systems, Jacobs, KBR, Larsan and Toubro Ltd., Mitsubishi Heavy Industries, Petrofac, Saipem, Samsung Engineering, Sargent Lundy, ShanDong Energy Group CO. Ltd., Siemens, SK Engineering and Construction, Sterlite Power Transmission Ltd., TATA Project, Technip, Thermax Global, Toshiba, Worley Parsons |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |