Quick Navigation

Report Overview

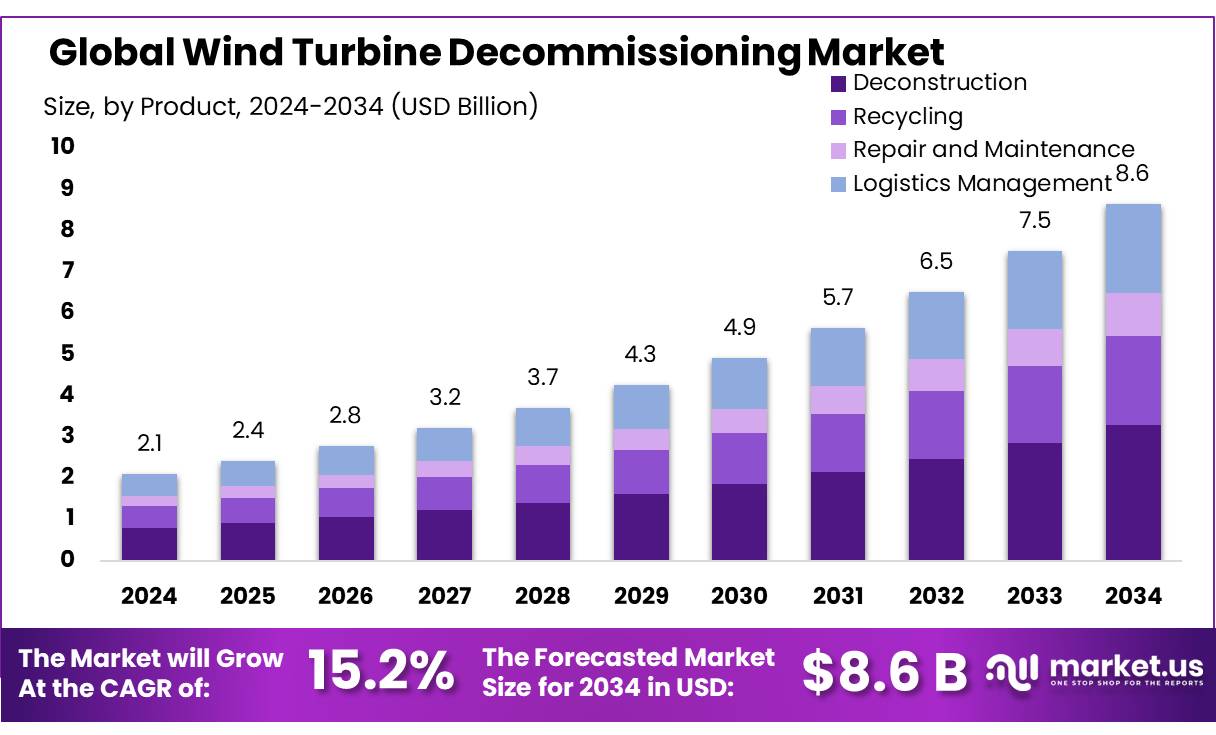

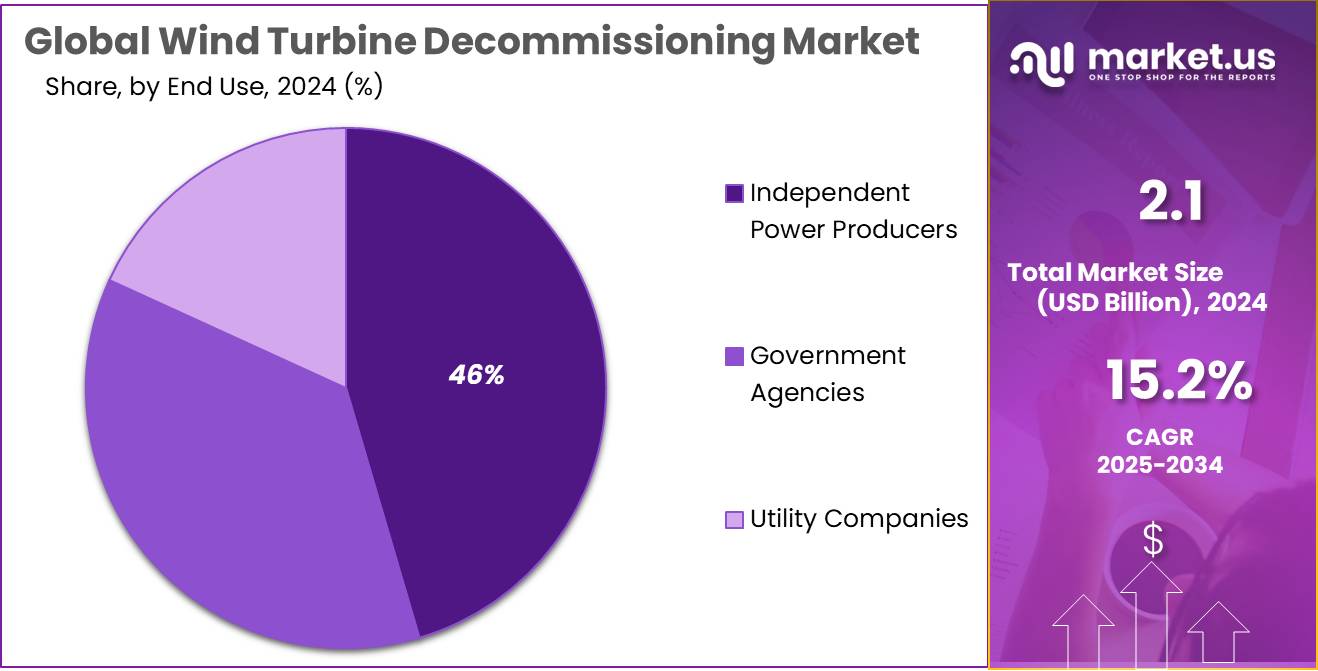

The Global Wind Turbine Decommissioning Market size is expected to be worth around USD 8.6 Bn by 2034, from USD 2.1 Bn in 2024, growing at a CAGR of 15.2% during the forecast period from 2025 to 2034.

The wind turbine decommissioning market involves the dismantling, recycling, and disposal of turbines at the end of their operational life. As global wind energy continues to grow, many turbines are reaching the end of their 20-25 year lifecycle, creating increasing demand for decommissioning services. This trend highlights the need for efficient and sustainable waste management for key turbine components like blades, towers, and nacelles.

According to the Global Wind Energy Council (GWEC), the global wind energy capacity exceeded 850 GW in 2023. However, a substantial portion of this capacity is now approaching the end of its operational life, contributing to the emerging demand for decommissioning services. The financial burden associated with decommissioning is significant—Xcel Energy has estimated the cost to decommission each wind turbine at approximately US$ 532,000, which could potentially pose a challenge to market growth.

As older turbines are replaced with newer, more efficient models, the need for specialized decommissioning becomes even more pronounced. In Europe alone, it is projected that over 25,000 turbines will require decommissioning by 2030, presenting a substantial opportunity for service providers in the market.

Key Takeaways

- The Global Wind Turbine Decommissioning Market is expected to grow from USD 2.1 billion in 2024 to USD 8.6 billion by 2034, at a CAGR of 15.2%.

- Deconstruction services held a 38.5% market share in 2024 due to the need to dismantle key turbine components.

- Horizontal Axis Wind Turbines accounted for a 56.2% market share in decommissioning activities in 2024.

- Blades represent a dominant component in decommissioning, holding a 39.3% market share in 2024, due to their recycling challenges.

- The onshore segment captured a 58.5% market share in 2024, driven by the prevalence of onshore wind farms.

- Independent Power Producers held a 46.5% market share in decommissioning services in 2024.

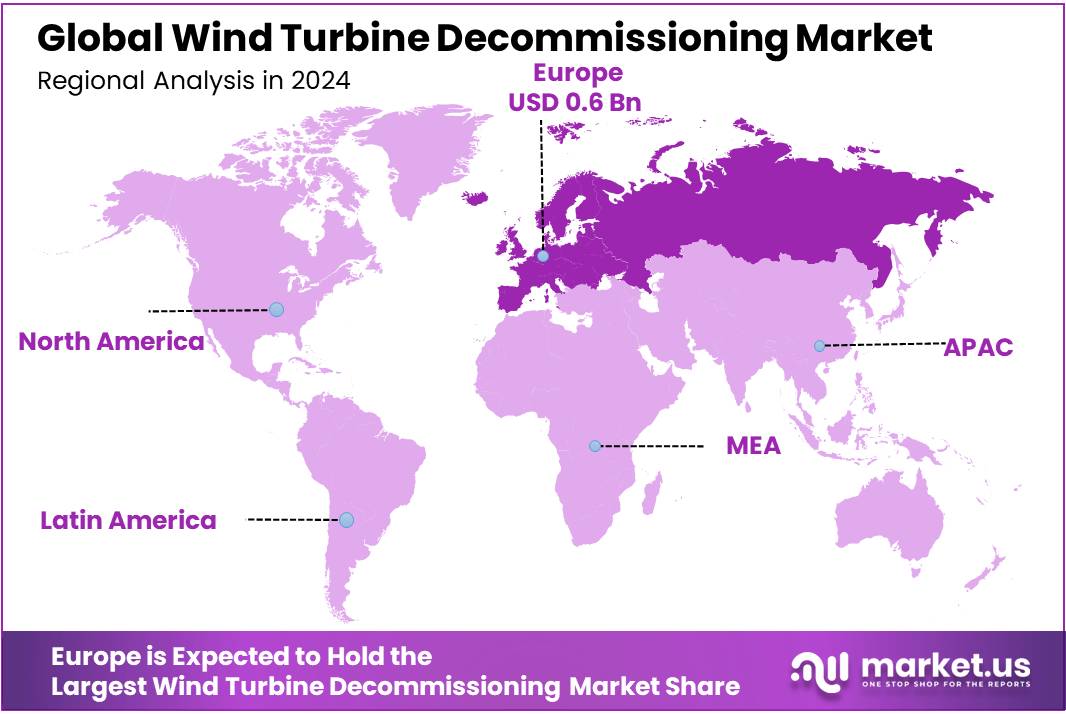

- Europe is expected to lead the market with a 32.5% share by 2023, driven by regulatory frameworks and a large number of aging turbines.

Analysts’ Viewpoint

Wind turbine decommissioning is becoming a critical focus in the renewable energy sector as turbines approach the end of their 20-25 year lifespan. The demand for decommissioning is growing alongside the increasing number of aging turbines worldwide. Industry analysts project the market for decommissioning to reach $7.5 billion by 2030, driven by these aging assets.

This market offers significant investment opportunities, particularly in areas like turbine recycling, repowering (replacing old turbines with newer, more efficient ones), and the development of disposal infrastructure. However, challenges such as high upfront costs and the technical complexity of removing offshore turbines could deter some investors.

Advancements in turbine recycling and blade reuse technologies will be key in mitigating the costs and risks of decommissioning. Currently, fewer than 10% of turbine blades are recycled effectively, but innovations in materials and recycling processes could lower these costs and make decommissioning more cost-efficient in the future.

The regulatory environment, however, remains fragmented, with different countries having varying standards for turbine disposal and end-of-life management. This lack of consistency can complicate cross-border operations, making it essential for governments to implement clear and unified regulations to guide these efforts.

By Service Type

In 2024, Deconstruction held a dominant market position, capturing more than a 38.5% share of the wind turbine decommissioning market. This leading position is primarily driven by the increasing number of wind turbines reaching the end of their operational lifespans, which necessitates the dismantling and removal of turbine components such as the tower, nacelle, and rotor blades. Deconstruction is a critical service within the decommissioning process, as it involves the physical disassembly of the turbine and the safe disposal of various materials, including metals, composites, and electrical components.

The growing focus on sustainability and environmental regulations surrounding the disposal of turbine materials further reinforces the demand for deconstruction services. As the wind energy sector continues to mature, a significant volume of turbines built in the early 2000s are nearing the end of their operational life, which is expected to drive increased demand for deconstruction services through the mid-2020s.

By Wind Turbine Type

In 2024, Horizontal Axis Wind Turbines (HAWT) held a dominant market position, capturing more than a 56.2% share of the wind turbine decommissioning market by turbine type. This dominance is attributed to the fact that HAWTs represent the most widely used technology in the global wind energy sector. With their established presence across both onshore and offshore installations, the decommissioning of HAWTs has become a key focus for wind turbine operators and service providers alike.

The majority of wind farms in operation today feature horizontal axis turbines due to their efficiency and scalability, particularly in terms of energy production. As these turbines approach the end of their operational life, decommissioning becomes an essential service to ensure the safe removal of turbine components and to minimize environmental impact. The decommissioning process for HAWTs typically involves dismantling large structures, including the tower, nacelle, rotor blades, and electrical systems, requiring specialized expertise in handling complex machinery and hazardous materials.

By Component

In 2024, Blades held a dominant market position, capturing more than a 39.3% share of the wind turbine decommissioning market by component. This significant share is primarily driven by the large physical size of the turbine blades and the complexity involved in their removal and disposal. As wind turbines reach the end of their operational lives, decommissioning efforts are often centered around the proper handling of blades, which are typically made from composite materials like fiberglass and carbon fiber. These materials pose challenges for recycling and disposal, making blade decommissioning a crucial segment of the overall wind turbine decommissioning process.

Blades are among the largest and most challenging components to dismantle, requiring specialized equipment and expertise. Given their size and weight, transporting and disposing of blades in an environmentally responsible manner has become a key focus for the industry. The demand for effective blade recycling technologies, such as mechanical grinding or thermal treatment, is expected to increase as stricter environmental regulations are introduced to address the growing volume of wind turbine waste.

By Location

In 2024, the onshore segment held a dominant market position, capturing more than 58.5% of the total market share. This dominance can be attributed to the substantial number of onshore wind farms in operation globally, which are reaching the end of their operational life cycle. Onshore wind turbines are more prevalent compared to offshore turbines, particularly in regions like North America, Europe, and Asia-Pacific, where wind energy infrastructure has been developed extensively in land-based locations.

Consequently, the need for decommissioning services in onshore locations is growing rapidly, driven by the need to dismantle, recycle, and dispose of aging turbines. This is particularly evident in Europe, where large numbers of onshore turbines are set to be decommissioned by 2030, contributing to an increased demand for specialized decommissioning services in the coming years.

By End User

In 2024, Independent Power Producers (IPPs) held a dominant market position in the wind turbine decommissioning market, capturing more than a 46.5% share. IPPs are major stakeholders in the wind energy sector, responsible for a significant portion of installed wind capacity globally. As these producers near the end of their wind turbine asset lifecycle, decommissioning services become essential to ensure compliance with environmental regulations and to mitigate potential risks associated with aging infrastructure.

The demand for decommissioning services among IPPs is driven by the large number of wind turbines reaching the end of their operational lifespan. This growing number of turbines creates an increasing need for efficient and cost-effective dismantling, recycling, and disposal solutions. Additionally, the environmental impact and the adoption of sustainability practices have prompted IPPs to adopt more comprehensive strategies for decommissioning, ensuring that materials are properly recycled and disposed.

Key Market Segments

By Service Type

- Deconstruction

- Recycling

- Repair and Maintenance

- Logistics Management

By Wind Turbine Type

- Horizontal Axis Wind Turbine

- Vertical Axis Wind Turbine

- Offshore Wind Turbine

- Onshore Wind Turbine

By Component

- Blades

- Nacelle

- Tower

- Foundation

By Location

- Onshore

- Offshore

By End User

- Independent Power Producers

- Government Agencies

- Utility Companies

Drivers

Government Initiatives Driving Wind Turbine Decommissioning

One of the major driving factors behind the growing trend of wind turbine decommissioning is the increasing focus on sustainability and responsible resource management. As wind turbines near the end of their operational life, typically around 20-30 years, governments and environmental organizations are placing more emphasis on ensuring their safe and eco-friendly disposal or repurposing. This is in line with global efforts to reduce waste, prevent land degradation, and promote circular economy practices.

For example, in Europe, where wind energy is a significant part of the energy mix, the European Commission has established clear guidelines on the decommissioning process. These guidelines focus on minimizing environmental impact by ensuring turbines are dismantled, recycled, or repurposed effectively. A report by the European Wind Energy Association (EWEA) estimated that by 2050, over 40,000 turbines in Europe will reach the end of their service life, highlighting the urgent need for proper decommissioning strategies.

Additionally, governments across the world are incentivizing the recycling of wind turbine blades, which are often made from composite materials that are not easily biodegradable. In the U.S., the Department of Energy (DOE) has funded research into new methods of recycling these blades. These initiatives are part of a larger push to ensure that the renewable energy sector remains environmentally responsible at every stage of its lifecycle, from installation to decommissioning.

As the wind energy sector continues to grow, the importance of sustainable decommissioning practices will only increase, making it a critical area for future investment, research, and policy-making. These efforts are essential to reducing the industry’s environmental footprint and ensuring that wind energy remains a truly sustainable source of power.

Restraints

High Costs of Wind Turbine Decommissioning

One of the significant challenges to wind turbine decommissioning is the high cost associated with dismantling and disposing of aging turbines. As turbines near the end of their operational life, their decommissioning process can be both complex and expensive. A typical decommissioning project involves removing large, heavy components, such as the rotor blades, towers, and nacelles, which requires specialized equipment and labor. Additionally, safely transporting and recycling these materials adds another layer of expense.

For instance, the cost of decommissioning a single wind turbine can range between $100,000 to $300,000, depending on its size, location, and the complexity of the dismantling process. In the U.S., the wind energy sector has grown rapidly, with over 60,000 turbines currently in operation. According to the National Renewable Energy Laboratory (NREL), as turbines age and need replacement or removal, the overall cost for decommissioning could become a financial burden on wind farm operators, especially as more turbines reach the end of their service life in the coming decades.

One major restraint is the lack of a clear financial mechanism for covering decommissioning costs. While many wind farm operators are required to set aside funds for decommissioning, these funds often fall short due to fluctuating turbine prices and the unpredictable nature of waste disposal costs. Governments and industries have yet to implement robust, universal financial frameworks that adequately address these growing costs.

To counteract this, some governments are starting to offer incentives and grants for developing more cost-effective recycling solutions, particularly for turbine blades. For example, the European Union has provided funding for research into sustainable disposal methods to ease the financial burden of decommissioning while also advancing the circular economy in the wind energy sector. However, more needs to be done to ensure a financially sustainable future for turbine decommissioning.

Opportunity

Renewable Energy Transition in Wind Turbine Decommissioning

As the global demand for renewable energy continues to rise, the need for efficient wind turbine decommissioning has emerged as a significant growth opportunity. With thousands of turbines reaching the end of their operational lifespan over the next few decades, industries must focus on how to responsibly dismantle these structures while recovering valuable materials and ensuring minimal environmental impact.

In 2020, the global wind turbine market saw over 90 GW of new installations, and the International Renewable Energy Agency (IRENA) predicts that wind power capacity could reach 2,000 GW by 2050. However, this rapid growth also leads to a corresponding increase in decommissioning efforts, presenting a massive opportunity in the recycling and repurposing of turbine components, particularly the blades, which are notoriously difficult to recycle. The decommissioning industry is expected to grow alongside this wind energy boom, with some estimates suggesting that decommissioning costs could rise to $5 billion annually by 2050.

Government initiatives, particularly in Europe, are already working to address this challenge. The European Union has pledged to boost the circular economy, encouraging the recycling of wind turbine components through its “Green Deal” and specific regulations targeting the end-of-life management of renewable energy assets. For instance, the EU’s directive on waste management emphasizes recycling and repurposing materials, providing funding to support innovations in turbine blade recycling technologies.

Trends

Growing Focus on Sustainable Wind Turbine Decommissioning

The decommissioning of wind turbines is gaining attention as the global wind energy industry faces the challenge of managing aging turbines. As wind farms mature, especially those built in the early 2000s, a significant number of turbines are reaching the end of their operational life. This shift has made turbine decommissioning a critical part of the wind energy lifecycle.

One of the key trends in this sector is the increased emphasis on sustainability during decommissioning processes. Traditionally, turbines are dismantled and parts like steel, copper, and other metals are recycled. However, as more turbines reach decommissioning, the industry is focusing on finding innovative, eco-friendly ways to recycle or repurpose turbine blades. Blades, often made from composite materials like fiberglass, are notoriously difficult to recycle, which has raised environmental concerns.

A report by the National Renewable Energy Laboratory (NREL) suggests that by 2050, the U.S. could see over 14,000 wind turbines decommissioned annually, resulting in about 2 million tons of waste per year. This has prompted efforts to develop new technologies and processes for blade recycling. For example, in 2023, Siemens Gamesa announced a breakthrough in producing recyclable wind turbine blades that could set a new standard for sustainability in the industry.

Governments are also stepping in with initiatives to guide this shift. The European Union, for instance, has introduced policies under its Green Deal that encourage turbine manufacturers to create recyclable blades and ensure that wind farms follow circular economy principles. These efforts aim to reduce landfill waste and lower the environmental impact of turbine decommissioning, ultimately contributing to a more sustainable renewable energy future.

Regional Analysis

Europe is poised to dominate the global wind turbine decommissioning market, accounting for approximately 32.5% of the market share, with a valuation of USD 0.6 billion in 2023. The region’s strong commitment to renewable energy, coupled with a large number of aging wind turbines, positions it as a key player in the decommissioning sector. Over the past two decades, Europe has been a frontrunner in wind energy adoption, with countries like Germany, the UK, Spain, and Denmark having some of the largest installed wind capacities globally. As many of these turbines approach the end of their operational lives, decommissioning is becoming increasingly crucial.

The decommissioning trend in Europe is driven by regulatory frameworks and sustainability goals set by the European Union. The EU’s Green Deal, aimed at reducing carbon emissions, has led to investments in the circular economy, encouraging the recycling and repurposing of wind turbine components, especially blades, which have traditionally been challenging to recycle. Additionally, the European Commission has introduced policies to ensure that turbines are decommissioned in an environmentally responsible manner, with an emphasis on waste reduction and recycling.

Germany is expected to be one of the largest markets within Europe, with significant decommissioning activity projected for the coming years. This is due to the country’s aggressive wind energy policies and its substantial fleet of aging turbines. By 2030, it is estimated that over 10,000 turbines in Europe will reach the end of their life cycle annually, increasing the demand for decommissioning services. With Europe’s focus on sustainable energy and responsible waste management, the market for wind turbine decommissioning is expected to expand further in the region.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Aggreko Ltd is a global leader in providing temporary power generation and temperature control solutions. They are also involved in the wind turbine decommissioning market by providing the necessary power and equipment for the dismantling and recycling of turbine components. With expertise in energy supply, Aggreko ensures minimal downtime during the decommissioning process. Their role helps operators transition turbines efficiently, while minimizing operational disruptions and promoting sustainable disposal practices.

Apex Clean Energy is a prominent renewable energy developer, particularly focused on wind power. They specialize in wind energy projects and contribute to turbine decommissioning by offering innovative strategies for the sustainable dismantling of turbines. Their focus on environmental responsibility ensures that decommissioned components are recycled or disposed of in line with sustainability goals. Apex supports the wind industry with advanced technologies that enhance decommissioning efficiency, while aligning with regulatory and eco-friendly standards.

Belson Steel Center Scrap Inc. is a key player in metal recycling, including the recycling of materials from decommissioned wind turbines. They specialize in the collection and processing of ferrous and non-ferrous metals, turning waste into valuable resources. Their services are critical in the wind turbine decommissioning process as they offer environmentally responsible disposal and recycling options for metal parts. Belson’s contribution ensures the metal components of decommissioned turbines are processed sustainably and reused in various industries.

Top Key Players

- Aggreko Ltd

- Apex Clean Energy

- Belson Steel Center Scrap Inc.

- Cadeler A/S

- Deltares

- DEME NV

- Donjon Marine Co., Inc.

- EnBW Energie Baden-Württemberg AG

- Enel Green Power S.p.A.

- EOS Engineering & Service Co., Ltd.

- Intertek Group Plc

- JACK-UP BARGE

- Jansen Recycling Group

- M2 Subsea

- NIRAS A/S

- NIRAS Gruppen A/S

- Ocean Surveys, Inc.

- Oceaneering International, Inc.

- Principle Power, Inc.

- Ramboll Group A/S

- ReBlade

- SgurrEnergy

- Wind Decom

Recent Developments

Aggreko reported revenues in the range of $1 billion in 2024. Additionally, the company secured $66 million in funding in September 2024 to support its growing portfolio of energy solutions.

In December 2024, Apex Clean Energy secured financing for the 300 MW Prosperity Wind facility, marking its fifth project in Illinois and advancing the state’s clean energy objectives.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 2.1 Bn |

| Forecast Revenue (2034) | USD 8.6 Bn |

| CAGR (2025-2034) | 15.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Service Type (Deconstruction, Recycling, Repair and Maintenance, Logistics Management), By Wind Turbine Type (Horizontal Axis Wind Turbine, Vertical Axis Wind Turbine, Offshore Wind Turbine, Onshore Wind Turbine), By Component (Blades, Nacelle, Tower, Foundation), By Location (Onshore, Offshore), By End User (Independent Power Producers, Government Agencies, Utility Companies) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Aggreko Ltd, Apex Clean Energy, Belson Steel Center Scrap Inc., Cadeler A/S, Deltares, DEME NV, Donjon Marine Co., Inc., EnBW Energie Baden-Württemberg AG, Enel Green Power S.p.A., EOS Engineering & Service Co., Ltd., Intertek Group Plc, JACK-UP BARGE, Jansen Recycling Group, M2 Subsea, NIRAS A/S, NIRAS Gruppen A/S, Ocean Surveys, Inc., Oceaneering International, Inc., Principle Power, Inc., Ramboll Group A/S, ReBlade, SgurrEnergy, Wind Decom |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |