Quick Navigation

Report Overview

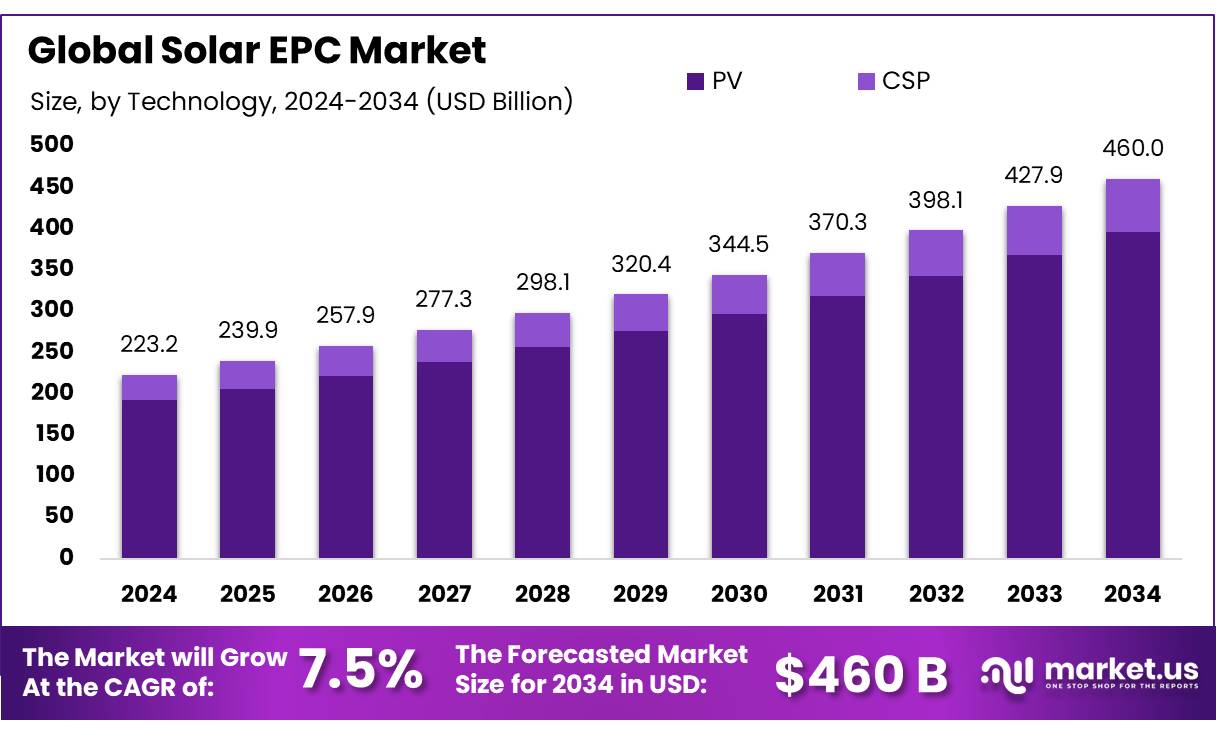

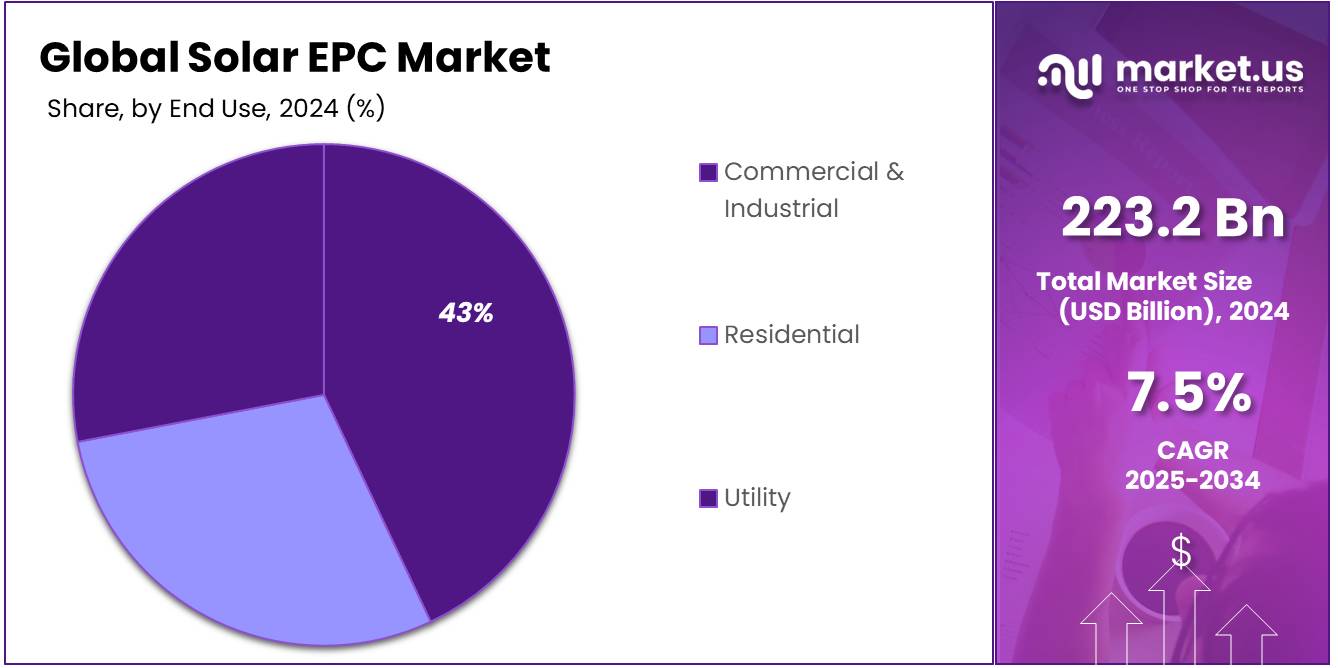

The Global Solar EPC Market size is expected to be worth around USD 460.0 Bn by 2034, from USD 223.2 Bn in 2024, growing at a CAGR of 7.5% during the forecast period from 2025 to 2034.

The Solar EPC (Engineering, Procurement, and Construction) market represents a pivotal segment in the global renewable energy industry, acting as a comprehensive service model that delivers end-to-end solutions for solar projects. EPC contractors are responsible for the detailed engineering design of the project, procurement of equipment, and construction installation. This turnkey solution not only ensures compliance with technical specifications but also adheres to budgetary constraints and timelines, which are critical for the project’s success.

The Solar EPC market has seen substantial growth, fueled by increasing global awareness and governmental support for sustainable energy sources. The market is characterized by its competitive landscape, where differentiation is primarily driven by cost efficiency, technological innovation, and the ability to deliver projects within stringent timelines. Major players in this sector include global corporations like First Solar, SunPower Corporation, and Canadian Solar, among others, which compete on both local and international levels.

Driving factors for the Solar EPC market include governmental policies favoring renewable energy, the declining cost of solar technologies, and the global push towards carbon neutrality. Financial incentives such as tax rebates, grants, and subsidies have made solar investments more attractive. Additionally, technological advancements in solar panel efficiency and battery storage solutions have expanded the potential applications of solar power, making it more feasible for both residential and commercial uses.

Solar EPC market is poised for continued growth, with significant opportunities emerging from developing regions like Asia-Pacific and Africa, where energy demand is surging, and solar power is becoming increasingly economically viable. The trend towards decentralized and off-grid energy solutions is also opening new avenues for market expansion. Future growth will likely be supported by innovations in photovoltaic technology, further cost reductions, and improved energy storage systems, which will enhance the overall value proposition of solar power.

The market faces challenges such as the volatility of raw material prices and the regulatory complexities across different regions. The need for land and grid integration also poses constraints, particularly in densely populated areas or regions with underdeveloped infrastructure.

Key Takeaways

- Solar EPC Market size is expected to be worth around USD 460.0 Bn by 2034, from USD 223.2 Bn in 2024, growing at a CAGR of 7.5%.

- Photovoltaic (PV) technology held a dominant market position in the solar EPC market, capturing more than an 86.2% share.

- Ground Mounted solar systems held a dominant market position within the solar EPC market, capturing more than a 57.4% share.

- 50 kW to 1 MW segment held a dominant market position in the solar EPC market, capturing more than a 38.3% share.

- Commercial & Industrial (C&I) applications held a dominant market position in the solar EPC market, capturing more than a 43.3% share.

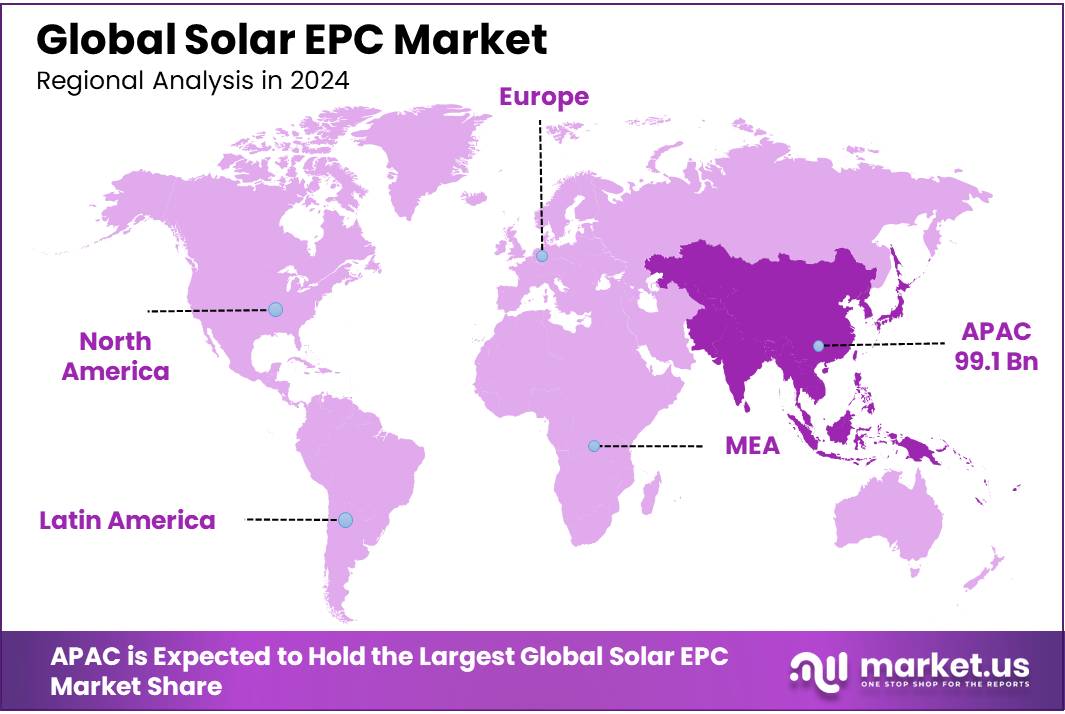

- Asia Pacific (APAC) region continues to dominate the global Solar EPC market, capturing a substantial 44.4% share, with a market value of approximately $99.1 billion.

By Technology

In 2024, Photovoltaic (PV) technology held a dominant market position in the solar EPC market, capturing more than an 86.2% share. This substantial market share can be attributed to the widespread adoption of PV technology due to its cost-effectiveness and scalability compared to other solar technologies. The PV sector has seen significant advancements in panel efficiency and reductions in the cost of materials, which have further solidified its leading status in the market. Businesses and residential consumers alike are increasingly opting for PV installations to benefit from lower electricity costs and to participate in a greener economy.

On the other hand, Concentrated Solar Power (CSP) technology, while smaller in market share, continues to play a critical role in specific market segments that require stable energy output, particularly in regions that receive consistent and intense sunlight. CSP technology is particularly valued for its ability to store solar energy for nighttime use or during cloudy intervals, providing a reliable power supply that can help stabilize the grid. While CSP installations are more capital-intensive and complex, ongoing research and technological improvements are expected to enhance their efficiency and cost-effectiveness in the coming years.

By Classification

In 2024, Ground Mounted solar systems held a dominant market position within the solar EPC market, capturing more than a 57.4% share. This segment benefits from its adaptability to various scales, from small community projects to vast utility-scale installations. The preference for ground-mounted installations is often attributed to their efficiency advantages; without the space constraints typical of rooftops, these systems can be designed to maximize sun exposure and enhance energy production.

Rooftop solar installations, while smaller in market share, continue to be popular in residential and commercial sectors due to their direct use of otherwise unutilized space and their ability to reduce transmission losses by generating power close to the point of consumption. They are particularly appealing in urban areas where land availability is limited.

Floating solar technology, the newest among the three classifications, is gaining traction in regions with limited land and abundant water bodies. These systems are installed on bodies of water, such as lakes and reservoirs, conserving land and water through reduced evaporation. While still a smaller part of the market, floating solar is expected to grow as water-land conflicts intensify and technology improves.

By Capacity

In 2024, the 50 kW to 1 MW segment held a dominant market position in the solar EPC market, capturing more than a 38.3% share. This segment typically caters to commercial and industrial clients who require substantial power output to meet their operational needs. The popularity of this capacity range can be attributed to its suitability for businesses looking to reduce utility bills and secure energy independence without the space requirements of larger installations.

Smaller capacity installations, such as those up to 1 kW and from 1 to 10 kW, are predominantly utilized in residential settings. These installations are ideal for homeowners seeking to lower their electricity costs and enhance their sustainability footprint. They are simple to install and maintain, making them accessible for a wide range of consumers.

The 10 to 50 kW capacity range serves a niche market, typically small businesses and community-based projects that require more power than typical residential setups but less than large commercial operations. This range is becoming increasingly popular as more small businesses look to solar power as a viable option to decrease operational expenses and contribute to environmental conservation.

By End Use

In 2024, Commercial & Industrial (C&I) applications held a dominant market position in the solar EPC market, capturing more than a 43.3% share. This sector has seen significant growth due to the rising cost of electricity and the increasing need for businesses to reduce their carbon footprints. Commercial and industrial customers are turning to solar power not only to lower their energy costs but also to ensure long-term energy reliability. Additionally, these businesses benefit from various financial incentives, such as tax credits and rebates, which make solar installations more attractive.

The residential sector, while smaller in comparison, continues to grow as homeowners look to cut down on energy costs and transition to more sustainable energy solutions. The affordability of smaller-scale solar systems and advancements in financing options, like solar leases and power purchase agreements, have helped make residential solar more accessible. By 2025, the residential segment is expected to see even more adoption as solar technology continues to improve, and more people become aware of its long-term benefits.

The utility-scale segment, while growing at a steady pace, remains a significant player in the solar EPC market. Utility companies are increasingly investing in large solar farms to meet government mandates on renewable energy production and reduce dependency on fossil fuels. These large-scale installations provide energy for entire communities, contributing to the overall sustainability goals of many regions. As more countries push for clean energy, the utility segment is expected to continue expanding, with larger and more efficient projects being deployed globally.

Key Market Segments

By Technology

- PV

- CSP

By Classification

- Rooftop

- Ground Mounted

- Floating Solar

By Capacity

- Up to 1 kW

- 1 to 10 kW

- 10 to 50 kW

- 50 kW to 1 MW

By End Use

- Residential

- Commercial & Industrial

- Utility

Drivers

Government Initiatives Driving Solar EPC Market Growth

One of the major driving factors for the growth of the Solar EPC market is the increasing support from government initiatives and policies aimed at promoting renewable energy. Governments worldwide are rolling out incentives, subsidies, and regulations to help transition to a greener, more sustainable energy mix. These efforts are providing strong backing for the adoption of solar energy, particularly in commercial and industrial sectors.

For instance, in the U.S., the Inflation Reduction Act (IRA), signed into law in 2022, includes significant tax credits and incentives for businesses to install solar power systems. It is estimated that these policies could result in the installation of more than 30 gigawatts of solar capacity annually by 2025. As per the Solar Energy Industries Association (SEIA), the act is expected to catalyze over $300 billion in investments over the next decade in clean energy technologies, with solar accounting for a significant share of that growth. This policy-driven push is helping many commercial and industrial sectors reduce their energy bills, while also contributing to sustainability goals.

Similarly, in Europe, the European Union’s Green Deal and various national programs are providing funding and incentives to encourage solar adoption. Germany, for example, introduced a 52 billion euro renewable energy expansion plan aimed at expanding solar power generation capacity. The German government also introduced legislation to make it easier for businesses to install solar systems by simplifying the permitting process.

These government-driven efforts are creating a fertile environment for the growth of the solar EPC market. With significant financial support, businesses are increasingly able to invest in renewable energy solutions, while governments continue to incentivize and regulate the shift toward clean energy. In turn, the entire solar energy supply chain, including EPC services, benefits from the heightened demand driven by these initiatives.

Restraints

High Initial Capital Costs as a Restraining Factor for Solar EPC Market Growth

One of the major challenges facing the Solar EPC market is the high initial capital cost associated with solar power installations. While solar energy offers long-term savings on energy bills, the upfront cost of purchasing and installing solar panels, inverters, and other equipment can be a significant barrier, especially for small businesses and homeowners. This high initial cost remains one of the key restraining factors for solar adoption, particularly in markets where financial incentives are limited or less accessible.

According to the International Renewable Energy Agency (IRENA), the global average cost of solar photovoltaic (PV) systems in 2020 was around $1,100 per installed kilowatt (kW). While prices have decreased over the years due to advancements in technology and economies of scale, they remain a considerable investment for many, particularly in developing regions.

For instance, in the U.S., the cost of installing a commercial solar system can range from $50,000 to $100,000 for a 50 kW system, depending on various factors like location, system size, and local installation costs. This price range is out of reach for many small businesses, despite the long-term savings and environmental benefits.

In addition to the high initial costs, solar EPC projects often face lengthy installation times and complex permitting processes, which further delay the realization of energy savings. While the U.S. and other countries have made strides in simplifying regulations, these barriers still exist and can deter potential customers, especially those in sectors with tighter budgets or time constraints.

To mitigate this challenge, governments are increasingly offering financial incentives, such as tax credits, subsidies, and low-interest loans, to help offset these costs. The U.S. government’s 30% investment tax credit (ITC), for example, has been a major driver in making solar more affordable for businesses and homeowners alike.

Opportunity

Growth Opportunities in the Solar EPC Market Through Corporate Sustainability Goals

A major growth opportunity for the Solar EPC market lies in the increasing number of corporations setting ambitious sustainability and renewable energy targets. As global awareness of climate change intensifies, more businesses are under pressure to reduce their carbon footprints and switch to greener energy sources. Solar power is often the go-to solution, especially for large companies aiming to meet their environmental, social, and governance (ESG) objectives.

For example, in the food industry, companies like Nestlé and Unilever have made significant commitments to renewable energy. Nestlé announced in 2020 that it would reach 100% renewable electricity for its global operations by 2025. Similarly, Unilever has committed to sourcing 100% renewable energy across its global operations, with solar power playing a key role in these plans. As major corporations in the food and beverage sector shift to renewable energy, the demand for solar EPC services is expected to rise.

The U.S. and European Union are also implementing policies that make it easier for companies to transition to solar. The U.S. government, for instance, provides tax credits such as the Investment Tax Credit (ITC), which covers up to 30% of the costs for commercial solar installations. This makes it financially more attractive for companies to make the switch, particularly in industries with large energy demands like food processing and manufacturing.

Moreover, many companies are choosing to implement solar power in their supply chains to not only meet regulatory requirements but also reduce operating costs in the long run. For example, Walmart has installed solar power systems on hundreds of its stores and distribution centers as part of its goal to become a more sustainable company.

Trends

Latest Trend in the Solar EPC Market: Increasing Adoption of Solar + Storage Solutions

A significant trend in the Solar EPC market is the growing adoption of solar power combined with energy storage systems (ESS), particularly in commercial and industrial sectors. As the technology improves and costs decrease, businesses are increasingly looking to solar + storage solutions to enhance energy independence, reduce reliance on the grid, and ensure consistent power supply during peak demand periods or outages.

For instance, companies like General Mills, a major player in the food industry, are leading the way in adopting solar and energy storage. In 2020, General Mills installed a solar + storage system at one of its manufacturing plants, with a 1.5 MW solar array paired with a 2 MW/4 MWh battery storage system. This allows the company to store excess solar energy generated during the day for use during high-demand hours or at night, significantly reducing its dependence on grid power. This move aligns with the company’s commitment to sustainability, as it aims to achieve net-zero emissions by 2050.

The combination of solar energy and storage is also supported by growing government incentives. In the U.S., the Investment Tax Credit (ITC) includes incentives not just for solar installations but also for storage systems, encouraging businesses to adopt integrated solutions. According to the U.S. Department of Energy, solar + storage installations have seen a surge in popularity, with the market for energy storage in the U.S. expected to grow by more than 15% annually through 2025.

In regions like Europe, where renewable energy targets are becoming stricter, solar + storage systems are being adopted at an increasing rate to meet these goals. For example, Germany’s commitment to renewables has driven investments in energy storage to ensure that solar power can be effectively used even when the sun isn’t shining.

Regional Analysis

In 2024, the Asia Pacific (APAC) region continues to dominate the global Solar EPC market, capturing a substantial 44.4% share, with a market value of approximately $99.1 billion. This dominance is driven by the rapid adoption of solar energy in key countries like China, India, and Japan, where favorable government policies, abundant sunlight, and ambitious renewable energy targets are propelling growth.

In North America, the Solar EPC market has experienced steady growth, driven largely by the United States, where the recent passage of the Inflation Reduction Act (IRA) is boosting investments in clean energy. The region holds a significant share of the market, with increasing corporate adoption of solar power solutions as companies pursue their sustainability goals.

Europe is another key player, focusing on renewable energy to meet its Green Deal targets. Countries like Germany, Spain, and France have been at the forefront of solar adoption, bolstered by strong government incentives and a clear policy framework aimed at reducing carbon emissions.

The Middle East & Africa (MEA) and Latin America, though smaller in comparison, are gradually emerging as growing markets for solar EPC services. The MEA region, with its high levels of solar radiation, sees increasing solar energy projects, particularly in countries like the UAE and Saudi Arabia. Latin America, particularly Brazil and Mexico, is making strides in solar energy adoption, spurred by both local and international investments.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Solar EPC market is highly competitive, with several key players leading the industry in innovation, project execution, and technological advancements. Companies such as SunPower Corporation, First Solar, Inc., and Canadian Solar Inc. are among the top contenders in the global market, offering comprehensive solar energy solutions ranging from project design to installation and maintenance. Bechtel Corporation and Abengoa are well-known for their involvement in large-scale utility projects, particularly in regions like the U.S. and Latin America.

Additionally, Wuhan LONGI Technology Co., Ltd., JA Solar Holdings Co., Ltd., and JinkoSolar have solidified their positions as some of the largest suppliers of solar modules, contributing significantly to the growing demand for solar power. Siemens Gamesa Renewable Energy, S.A. and Trina Solar Ltd. also play critical roles in advancing solar technologies and enhancing the efficiency of solar power generation. On the other hand, companies like Sterling and Wilson Renewable Energy Limited, L&T Construction, and Mahindra Susten are leading in the installation and construction of solar projects in emerging markets, including Asia and Africa.

The market is further diversified by regional players such as VIKRAM SOLAR LTD., Waaree Energies Ltd., and Risen Energy Co., Ltd., which are rapidly expanding their footprints in regions with strong renewable energy targets like India. As demand for solar solutions grows, these key players, alongside emerging innovators like BLUELEAF ENERGY and Talesun Solar Technologies Co., Ltd., are expected to drive significant market expansion and technological developments across various solar applications worldwide.

Top Key Players

- SunPower Corporation

- Wuhan LONGI Technology Co., Ltd.

- Abengoa

- Bechtel Corporation

- BELECTRIC

- Black & Veatch Holding Company

- BLUELEAF ENERGY

- Canadian Solar Inc.

- CHINT SOLAR (ZHEJIANG) CO., LTD.

- Eternia Solar

- First Solar, Inc.

- GCL System Integration Technology Co., Ltd.

- Hanwha Solutions Corporation

- JA Solar Holdings Co., Ltd.

- Jakson Group

- JinkoSolar

- JUWI

- L&T Construction

- Longi Green Energy Technology Co., Ltd.

- Mahindra Susten

- Powerway Renewable Energy Co., Ltd.

- Risen Energy Co., Ltd.

- Siemens Gamesa Renewable Energy, S.A.

- SOLA GROUP

- Sterling and Wilson Renewable Energy Limited

- SUNEL GROUP

- Sungrow Power Supply Co., Ltd.

- Talesun Solar Technologies Co., Ltd.

- Tata Power Solar Systems Ltd.

- Trina Solar Ltd.

- VIKRAM SOLAR LTD.

- Waaree Energies Ltd.

Recent Developments

In 2024, SunPower’s total installed solar capacity surpassed 18 GW, with 1.2 GW of new solar projects completed in the year. The company focuses heavily on energy-efficient solutions and integrated solar + storage systems.

In 2024 Wuhan LONGI Technology Co., Ltd., the company expanded its global footprint, delivering over 18 GW of solar modules, and reported $15.2 billion in revenue, driven by both domestic and international sales.

In 2024 Abengoa, the company’s solar-related revenues were approximately $1.8 billion, driven by both ongoing projects and new contracts, especially in regions like the U.S., Middle East, and North Africa. Known for its innovation in CSP technology, Abengoa continues to lead the way in designing and delivering projects that integrate solar energy with storage solutions to provide reliable, renewable power to the grid.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 223.2 Bn |

| Forecast Revenue (2034) | USD 460.0 Bn |

| CAGR (2025-2034) | 7.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (PV, CSP, By Classification, Rooftop, Ground Mounted, Floating Solar), By Capacity (Up to 1 kW, 1 to 10 kW, 10 to 50 kW, 50 kW to 1 MW), By End Use (Residential, Commercial And Industrial, Utility) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | SunPower Corporation, Wuhan LONGI Technology Co., Ltd., Abengoa, Bechtel Corporation, BELECTRIC, Black & Veatch Holding Company, BLUELEAF ENERGY, Canadian Solar Inc., CHINT SOLAR (ZHEJIANG) CO., LTD., Eternia Solar, First Solar, Inc., GCL System Integration Technology Co., Ltd., Hanwha Solutions Corporation, JA Solar Holdings Co., Ltd., Jakson Group, JinkoSolar, JUWI, L&T Construction, Longi Green Energy Technology Co., Ltd., Mahindra Susten, Powerway Renewable Energy Co., Ltd., Risen Energy Co., Ltd., Siemens Gamesa Renewable Energy, S.A., SOLA GROUP, Sterling and Wilson Renewable Energy Limited, SUNEL GROUP, Sungrow Power Supply Co., Ltd., Talesun Solar Technologies Co., Ltd., Tata Power Solar Systems Ltd., Trina Solar Ltd., VIKRAM SOLAR LTD., Waaree Energies Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |