Quick Navigation

- Report Scope

- Key Takeaways

- Analysts’ Viewpoint

- Key Statistics

- Regional Analysis

- By Type

- By Mounting Angle

- By Voltage

- By Application

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunities

- Challenging Factors

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Recent Developments

- Report Scope

Report Scope

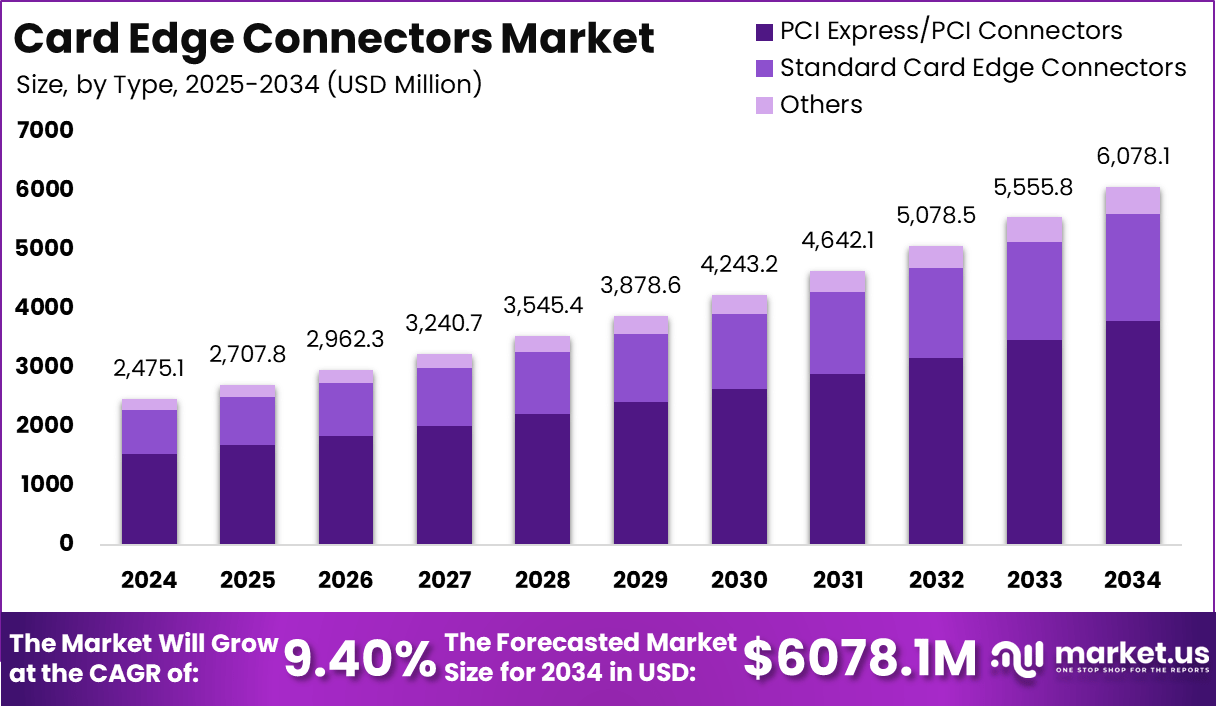

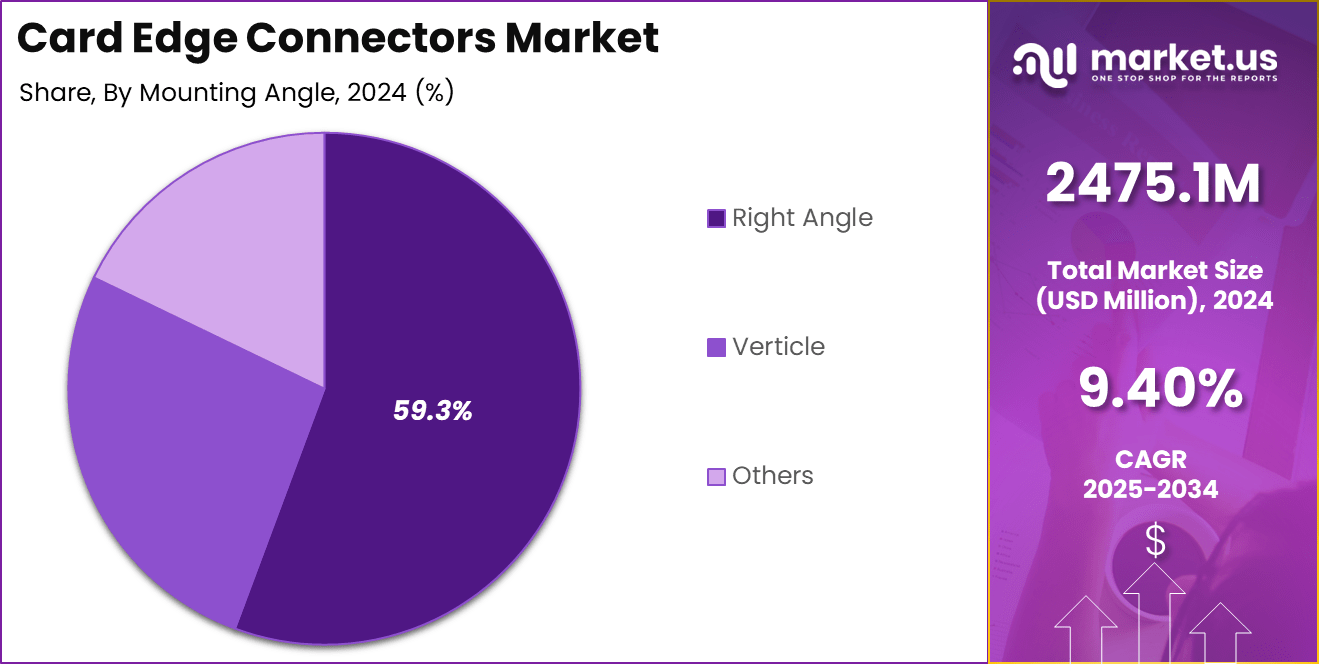

The Global Card Edge Connectors Market is expected to be worth around USD 6078.1 Million by 2034, up from USD 2475.1 Million in 2024. It is expected to grow at a CAGR of 9.40% from 2025 to 2034.

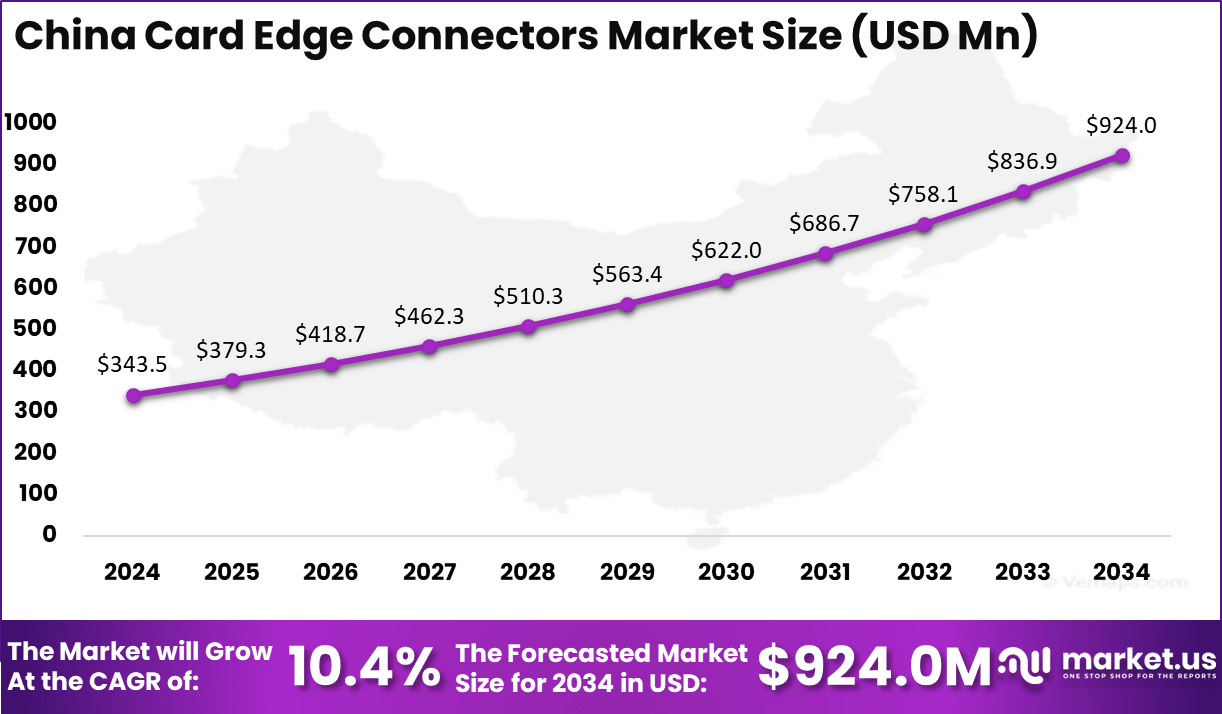

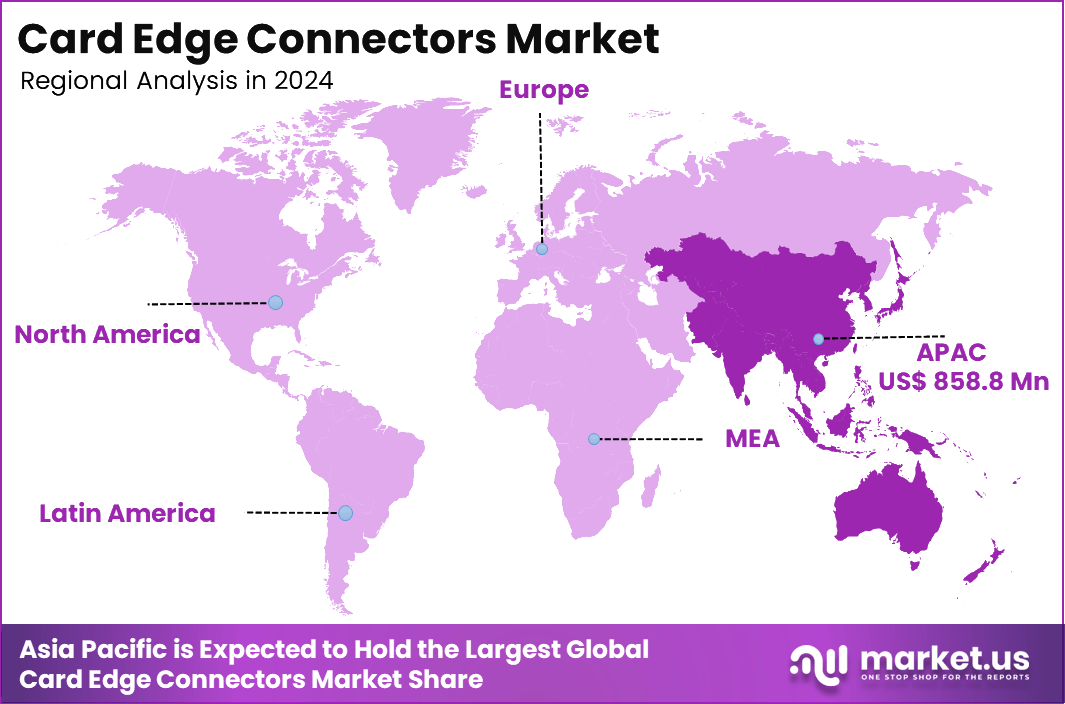

In 2024, Asia-Pacific held a dominant market position, capturing over a 34.7% share and earning USD 858.8 Million in revenue. Further, China dominates the market by USD 343.54 Million, steadily holding a strong position with a CAGR of 10.4%.

The Card Edge Connectors Market is a crucial segment within the electronics and semiconductor industry. These connectors are widely used in printed circuit boards (PCBs) to establish secure electrical connections in various electronic devices.

They are commonly found in consumer electronics, automotive applications, industrial equipment, and telecommunications infrastructure. The market has been witnessing steady growth due to the increasing adoption of high-performance computing systems, automation technologies, and advancements in electronic manufacturing.

Several key factors are driving the growth of the Card Edge Connectors Market. One of the most significant drivers is the rising demand for electronic devices across multiple industries, including consumer electronics, automotive, and telecommunications.

The increasing need for high-speed data transfer, efficient power management, and compact electronic designs is further fueling demand for advanced card edge connectors. Additionally, the growth of industrial automation and the rapid expansion of data centers worldwide are pushing manufacturers to develop innovative and high-quality connectors.

Key Takeaways

- Market Growth: The Card Edge Connectors Market is projected to grow from USD 2,475.1 million in 2024 to USD 6,078.1 million by 2034, registering a CAGR of 9.40%.

- Dominant Connector Type: PCI Express/PCI connectors hold the largest market share, accounting for 62.4% of the segment.

- Mounting Preference: Right-angle mounting connectors are the most widely used, capturing 59.3% of the market share.

- Voltage Segment: 50V-rated connectors dominate the market, with a substantial share of 73.8%.

- Key Application: The consumer electronics sector is the primary application area, contributing 56.4% to the overall demand.

- Regional Insights: The Asia-Pacific region leads the market, accounting for 34.7% of the global share.

- China’s Market Share: China is a significant player, with the market value projected at USD 343.54 million and a CAGR of 10.4%, indicating strong regional growth.

Analysts’ Viewpoint

The demand for card edge connectors is growing significantly due to the surge in digital transformation and the rise of next-generation technologies. The expansion of 5G networks, cloud computing, and the Internet of Things (IoT) has increased the need for reliable and high-performance connectors.

The automotive sector, particularly the electric vehicle (EV) segment, is also a major contributor to market demand. EVs require efficient power and data transmission systems, making card edge connectors a vital component in vehicle electronics.

The market presents several growth opportunities for manufacturers and suppliers. One of the biggest opportunities lies in the increasing miniaturization of electronic devices, which calls for compact and high-speed connectors. The rapid adoption of electric and hybrid vehicles is another major opportunity, as these vehicles require robust electrical systems for optimal performance.

Additionally, developing regions such as Asia-Pacific, particularly China and India, offer lucrative growth prospects due to the expansion of the electronics and telecom industries. Companies investing in customized and high-durability connectors will likely gain a competitive edge in the market.

Technological advancements are playing a critical role in shaping the Card Edge Connectors Market. Manufacturers are focusing on developing connectors with enhanced durability, higher data transfer speeds, and better thermal management. The integration of AI and IoT-driven applications in electronics has led to the need for smarter and more efficient connectors.

Innovations such as gold-plated contacts for improved conductivity, high-density connectors, and environmentally friendly materials are gaining traction in the industry. Additionally, 3D printing and automation in manufacturing are helping companies produce high-precision connectors while reducing production costs.

Key Statistics

Quantity and Production

- In 2022, the global production of card edge connectors was estimated to be around 1.5 billion units.

- This number is expected to increase by 15% annually due to growing demand from emerging markets.

Users

- The number of users is not directly quantifiable but includes manufacturers and consumers across various industries that utilize card edge connectors for their electronic devices.

- It is estimated that over 10,000 companies worldwide use card edge connectors in their products.

Socket Types

- Common socket types include 2.54 mm pitch, 3.96 mm pitch, and 4 mm pitch card edge sockets.

- The 2.54 mm pitch type accounts for about 60% of the market share.

Signal Integrity

- Card edge connectors are engineered to provide high signal integrity on PCBs, ensuring reliable data transmission with signal loss as low as 0.5 dB.

Applications

- They are used for connecting removable modules or expansion cards to the principal PCB in devices.

- Over 80% of modern computer systems use card edge connectors for expansion slots.

Material Usage

- The primary materials used in card edge connectors include copper (for contacts), plastic (for housing), and brass (for some structural components).

- The average connector uses about 0.5 grams of copper.

Manufacturing Process

- The manufacturing process involves injection molding for plastic parts and stamping for metal contacts.

- It takes approximately 5 minutes to assemble a single connector.

Regional Analysis

China Region Market Size

In Asia-Pacific, China dominates the market size by USD 343.54 million, holding a strong position steadily with a strong CAGR of 10.4%. The country remains a key player in the Card Edge Connectors Market, benefiting from its extensive electronic manufacturing capabilities, growing demand for consumer electronics, and rapid advancements in industrial automation. The expansion of data centers, increasing adoption of 5G technology, and the rise of electric vehicles (EVs) further contribute to the market’s strong growth trajectory.

The demand for PCI Express/PCI connectors continues to surge due to their widespread application in computing and high-speed networking devices. Additionally, right-angle connectors are preferred in compact electronic designs, particularly in high-performance industrial and telecom applications. With the increasing need for efficient power distribution and high-reliability components, 50V-rated connectors remain a dominant choice across various sectors.

The consumer electronics industry plays a crucial role in market expansion, driven by the rising penetration of smart devices, gaming consoles, and home automation systems. As Asia-Pacific continues to lead in electronics manufacturing, China’s strong position in the market ensures sustained growth, with ongoing technological advancements and rising investments in high-speed connectivity and automation solutions.

Asia Pacific Market Size

In 2024, Asia-Pacific held a dominant market position in the card edge connectors market, capturing more than a 34.7% share, equating to USD 858.8 million in revenue. This leadership is primarily driven by the region’s robust electronics manufacturing sector, particularly in countries like China, Japan, and South Korea. The widespread adoption of consumer electronics, such as smartphones and laptops, has significantly boosted the demand for card edge connectors in this region.

China, as a central hub for electronics production, has been instrumental in propelling the market forward. The country’s focus on technological innovation and substantial investments in 5G infrastructure have further augmented the demand for high-quality connectors. Additionally, the rise of electric vehicles (EVs) in China necessitates reliable connectors, thereby contributing to market growth.

Japan and South Korea also play pivotal roles, given their advancements in technology and significant contributions to the automotive and consumer electronics industries. The integration of sophisticated electronic systems in vehicles and the continuous evolution of consumer gadgets have led to an increased need for efficient card edge connectors.

Moreover, the expansion of data centers across Asia-Pacific, driven by the surge in internet usage and cloud computing, has created substantial opportunities for the card edge connectors market. The region’s commitment to embracing new technologies and its strong manufacturing capabilities position it to maintain its leading stance in the global market.

By Type

In 2024, the PCI Express (PCIe) Connectors segment held a dominant position in the card edge connectors market, capturing more than a 62.4% share. This leadership is primarily attributed to the widespread adoption of PCIe technology across various applications, including data centers, telecommunications, consumer electronics, and automotive sectors.

The increasing demand for high-speed data transfer and efficient connectivity solutions has propelled the use of PCIe connectors. In data centers, for instance, the need for rapid data processing and storage has led to the integration of PCIe connectors in servers and storage systems. Similarly, in consumer electronics, devices such as laptops and desktops utilize PCIe connectors to enhance performance and support advanced functionalities.

Moreover, the automotive industry’s shift towards advanced driver-assistance systems (ADAS) and infotainment solutions has further boosted the demand for PCIe connectors. These connectors facilitate reliable and fast communication between various electronic components within vehicles, ensuring seamless operation and improved user experience.

The continuous evolution of PCIe standards, offering higher data transfer rates and improved efficiency, has also contributed to the segment’s dominance. Manufacturers are increasingly adopting PCIe connectors to meet the growing requirements for speed and performance in modern electronic applications, solidifying the segment’s leading position in the market.

By Mounting Angle

In 2024, the Right Angle segment held a dominant market position, capturing more than a 59.3% share in the Card Edge Connectors Market. This dominance is primarily attributed to the widespread use of right-angle connectors in compact electronic designs, particularly in consumer electronics, industrial automation, and telecommunications. Right-angle connectors are preferred due to their space-saving design, easy PCB integration, and superior durability, making them ideal for applications requiring efficient board-to-board connections in limited spaces.

One of the key drivers for this segment’s growth is the increasing adoption of miniaturized and high-performance electronic devices. With manufacturers continuously striving to reduce the size of electronic components while maintaining optimal performance, right-angle card edge connectors provide the perfect solution by ensuring better cable management, reduced signal interference, and enhanced mechanical stability.

Additionally, industries such as automotive and aerospace are rapidly integrating right-angle connectors into their systems due to their ability to withstand high-vibration environments and maintain secure connections. As demand for high-density, high-speed, and robust connectivity solutions rises across various industries, the right-angle segment is expected to maintain its leadership in the Card Edge Connectors Market for the foreseeable future.

By Voltage

In 2024, the 50V segment held a dominant market position, capturing more than a 73.8% share in the Card Edge Connectors Market. This dominance is largely due to the increasing demand for high-power, reliable, and efficient connectors across multiple industries, including telecommunications, industrial automation, and automotive electronics. The 50V-rated connectors provide superior power handling capacity, ensuring stable electrical connections in high-performance applications where power efficiency and signal integrity are critical.

One of the key factors driving the growth of this segment is the rising adoption of high-speed networking, cloud computing, and data centers. These industries require robust and durable connectors capable of managing higher voltage levels without compromising performance. Additionally, electric vehicles (EVs) and renewable energy systems are creating further demand for 50V connectors, as they are essential for power distribution and battery management in modern energy-efficient technologies.

The consumer electronics sector is another major contributor to this segment’s growth. With increasing advancements in gaming consoles, smart appliances, and computing devices, the need for compact, high-voltage, and high-density connectors continues to rise. As industries continue to prioritize power efficiency and high-performance electronics, the 50V segment is expected to maintain its leading position in the Card Edge Connectors Market for the foreseeable future.

By Application

In 2024, the Consumer Electronics segment held a dominant market position, capturing more than a 56.4% share in the Card Edge Connectors Market. This leadership is driven by the growing demand for high-performance electronic devices, including smartphones, laptops, tablets, gaming consoles, and smart home appliances.

As technology advances, the need for compact, efficient, and high-speed connectors in modern electronic gadgets has surged, making card edge connectors a preferred choice due to their durability, ease of integration, and superior electrical performance.

One of the key factors supporting this segment’s dominance is the rising global adoption of smart devices and the continuous innovation in consumer electronics manufacturing. The shift towards smaller, more powerful devices with faster data transfer rates has further fueled the demand for high-density and high-speed connectors. Additionally, the expansion of 5G networks, artificial intelligence (AI)-driven devices, and Internet of Things (IoT) applications has significantly boosted the need for reliable connectivity solutions.

With the increasing popularity of wearable technology, gaming systems, and home automation devices, the consumer electronics segment is expected to maintain its leading position. As manufacturers continue to push the boundaries of device miniaturization and efficiency, the demand for advanced card edge connectors in this sector will continue to rise, securing its dominance in the Card Edge Connectors Market.

Key Market Segments

By Type

- Standard Card Edge Connectors

- PCI Express/PCI Connectors

Others

By Mounting Angle

- Right Angle

Verticle

Others

By Voltage

- 25V

50V

Others

By Application

- Consumer Electronics

Storage Devices

Navigational Equipment

Industrial Controls

Others

Driving Factors

Rising Demand for Consumer Electronics

The surge in consumer electronics has significantly propelled the card edge connectors market. Devices such as smartphones, tablets, laptops, and gaming consoles have become integral to daily life, leading to an increased need for reliable and efficient connectors.

Card edge connectors are essential in these devices, facilitating seamless connections between various components on printed circuit boards (PCBs). Their ability to support high-speed data transmission and maintain signal integrity makes them indispensable in modern electronics.

The trend towards miniaturization in electronics has further boosted the demand for compact and efficient connectors. Manufacturers are continually innovating to produce smaller, more powerful devices, necessitating connectors that can handle increased performance requirements without occupying excessive space. Card edge connectors, with their compact design and robust functionality, meet these criteria effectively.

Restraining Factors

High Cost of Raw Materials

The card edge connectors market faces challenges due to the escalating costs of raw materials. Metals such as copper and gold, essential for manufacturing connectors due to their excellent conductivity and durability, have experienced significant price volatility. This fluctuation directly impacts production costs, leading to higher prices for end products.

Manufacturers often struggle to balance quality and cost-effectiveness under these conditions. While seeking alternative materials or suppliers could mitigate expenses, it may also compromise the performance and reliability of the connectors. Maintaining stringent quality standards is crucial, especially in applications like medical devices and aerospace, where connector failure is not an option.

Moreover, the increased production costs can deter potential customers, particularly in price-sensitive markets. Small-scale manufacturers and startups may find it challenging to compete, leading to reduced innovation and diversity in the market. Thus, the high cost of raw materials serves as a significant restraint, hindering the market’s growth potential.

Growth Opportunities

Expansion of 5G Infrastructure

The global rollout of 5G networks presents a substantial growth opportunity for the card edge connectors market. 5G technology requires advanced infrastructure capable of supporting higher data speeds and increased connectivity. Card edge connectors, known for their high-speed data transmission capabilities and reliability, are integral components in 5G hardware, including routers, switches, and base stations.

As telecommunications companies invest heavily in upgrading their infrastructure to accommodate 5G, the demand for high-quality connectors is expected to rise. This expansion not only pertains to urban areas but also extends to rural regions, aiming to provide widespread high-speed internet access. Consequently, manufacturers of card edge connectors have a lucrative opportunity to cater to this burgeoning demand.

Furthermore, the proliferation of 5G-enabled devices, such as smartphones and IoT gadgets, necessitates robust connectors to ensure optimal performance. The anticipated growth in these markets amplifies the potential for card edge connector manufacturers to expand their product offerings and capture a larger market share.

Challenging Factors

Technological Advancements and Compatibility Issues

Rapid technological advancements pose challenges for the card edge connectors market, particularly concerning compatibility and standardization. As new electronic devices and systems are developed, ensuring that connectors are compatible with various generations of technology becomes complex. Manufacturers must continuously innovate to keep pace with evolving standards, which can be resource-intensive.

Additionally, the lack of universal standards for certain applications leads to fragmentation in the market. This scenario complicates the design and manufacturing processes, as connectors must be tailored to specific requirements, limiting economies of scale. For consumers, incompatibility between connectors and devices can result in frustration and increased costs, hindering the overall adoption of new technologies.

Addressing these challenges requires collaborative efforts among industry stakeholders to establish standardized protocols and ensure backward compatibility. Such initiatives would streamline manufacturing processes, reduce costs, and enhance user experience, thereby supporting the sustained growth of the card edge connectors market.

Growth Factors

Rising Demand for High-Speed Data Transmission

The increasing need for high-speed data transmission is a significant growth factor in the card edge connectors market. As industries such as telecommunications, data centers, and consumer electronics evolve, there is a heightened demand for connectors that can support faster data rates. This growth is largely attributed to the escalating requirements for rapid data transfer capabilities.

In telecommunications, the deployment of 5G networks necessitates connectors capable of handling increased bandwidth and low latency. Similarly, data centers are upgrading their infrastructure to accommodate the surge in cloud computing and big data analytics, driving the demand for advanced card edge connectors. The consumer electronics sector also contributes to this trend, with devices like smartphones and gaming consoles requiring connectors that facilitate swift and reliable data exchange.

Emerging Trends

Miniaturization and Integration of Advanced Features

A prominent emerging trend in the card edge connectors market is the miniaturization of connectors coupled with the integration of advanced features. As electronic devices become more compact, there is a pressing need for smaller connectors without compromising performance. Innovations in connector design have led to higher pin density, allowing more connections within limited spaces.

Moreover, connectors are now being engineered to withstand harsher environments, enhancing their durability. The integration with smart technology is also notable, with connectors designed to seamlessly work with Internet of Things (IoT) devices. These advancements not only meet the physical constraints of modern electronics but also align with the functional requirements of emerging technologies.

Business Benefits

Enhanced Performance and Reliability

The evolution of card edge connectors offers substantial business benefits, particularly in terms of performance and reliability. Advanced connectors support faster data rates, higher power throughput, and improved signal integrity, which are crucial for applications in data centers, telecommunications, and industrial automation.

For businesses, these enhancements translate to more efficient operations, reduced downtime, and the ability to support more complex and data-intensive applications. In the automotive industry, for example, reliable connectors are essential for the functionality of electric vehicles (EVs) and autonomous driving systems. The global connector market’s anticipated growth to USD 147.44 billion by 2032 underscores the increasing reliance on high-quality connectors across various sectors.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

TE Connectivity Ltd. has recently taken significant steps to strengthen its position in the energy sector. In February 2025, the company announced a definitive agreement to acquire Richards Manufacturing Co. for approximately $2.3 billion. This strategic move aims to enhance TE’s presence in the electrical utilities market, particularly in North America, by integrating Richards’ expertise in underground distribution equipment.

Amphenol Corporation has been actively expanding its portfolio through strategic acquisitions. In February 2025, Amphenol completed the acquisition of CommScope’s Outdoor Wireless Networks (OWN) and Distributed Antenna Systems (DAS) businesses. This acquisition brings innovative technologies to Amphenol’s portfolio, enhancing its capabilities in supporting next-generation wireless networks globally.

Molex LLC continues to be a key player in the cable assembly market, focusing on strategic developments to maintain its competitive edge. The company has been involved in various initiatives, including new product launches and partnerships, to strengthen its market position. Molex’s commitment to innovation and its extensive product offerings have solidified its standing in the industry.

Top Key Players in the Market

- TE Connectivity Ltd.

- Molex LLC

- Amphenol Corporation

- Phoenix Contact GmbH & Co. KG

- Samtec, Inc.

- Hirose Electric Co., Ltd.

- JST Mfg. Co., Ltd.

- 3M Company

- Sullins Electronics, Inc.

- Yamaichi Electronics Co., Ltd.

- Other Major Players

Recent Developments

- In 2024, KYOCERA AVX introduced the 9159-800 Series, the industry’s first dual-entry vertical card-edge connectors, featuring a compact design with a low above-board height profile, catering to applications in automotive, industrial manufacturing, and consumer electronics.

- In 2024, the global standard card edge connector market experienced substantial growth, driven by increased demand in sectors like telecommunications and automotive, leading to a notable expansion in market size.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 2475.1 Million |

| Forecast Revenue (2034) | USD 6078.1 Million |

| CAGR (2025-2034) | 9.40% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Standard Card Edge Connectors, PCI Express/PCI Connectors, Others), By Mounting Angle ( Right Angle, Verticle, Others), By Voltage (25V, 50V, Others), By Application (Consumer Electronics, Storage Devices, Navigational Equipment, Industrial Controls, Others), By Revenue Model (Subscription-Based, Ad-Supported, Pay-Per-View, Others) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | TE Connectivity Ltd., Molex LLC, Amphenol Corporation, Phoenix Contact GmbH & Co. KG, Samtec, Inc., Hirose Electric Co., Ltd., JST Mfg. Co., Ltd., 3M Company, Sullins Electronics, Inc., Yamaichi Electronics Co., Ltd., Other Major Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |