Quick Navigation

- Report Scope

- Key Takeaways

- Analyst Viewpoint

- Market Key Statistics

- Regional Analysis

- Key Player Analysis

- By Component

- By Deployment Type

- By Enterprise Size

- By End User

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunities

- Challenging Factors

- Growth Factors

- Emerging Trends

- Business Benefits

- Recent Developments

- Report Scope

Report Scope

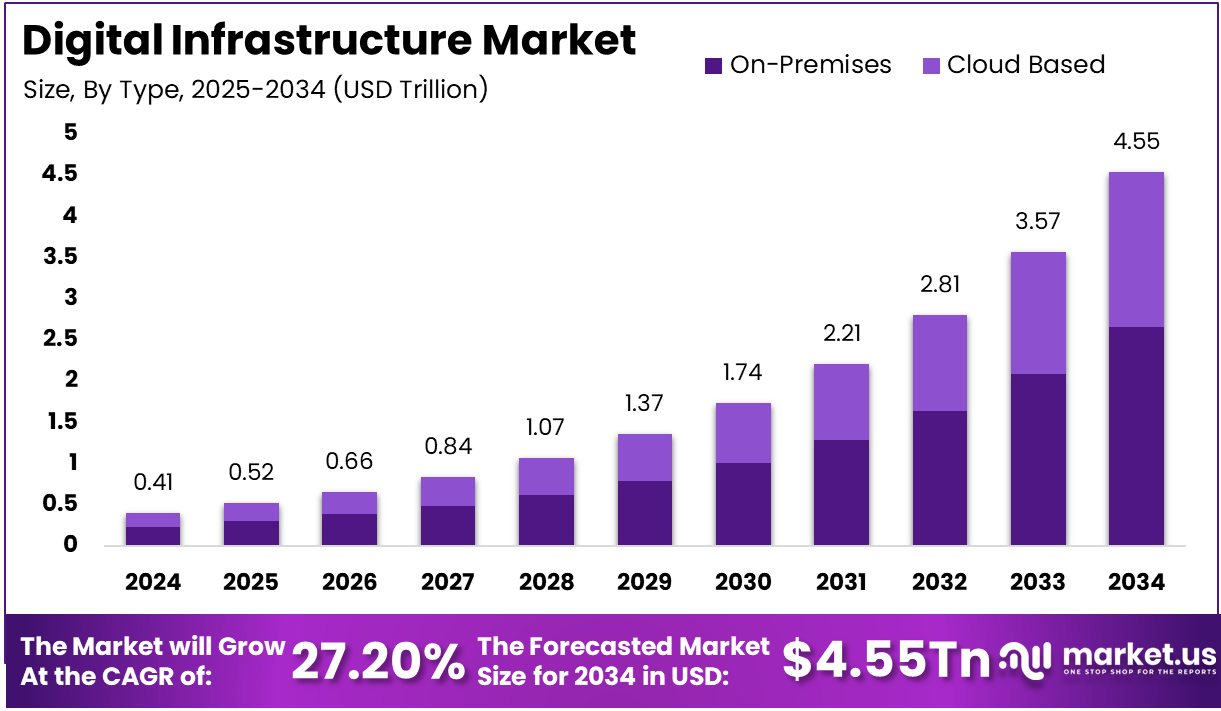

The Global Digital Infrastructure Market is expected to be worth around USD 4.55 Trillion By 2034, up from USD 0.41 Trillion in 2024. It is expected to grow at a CAGR of 27.20% from 2025 to 2034.

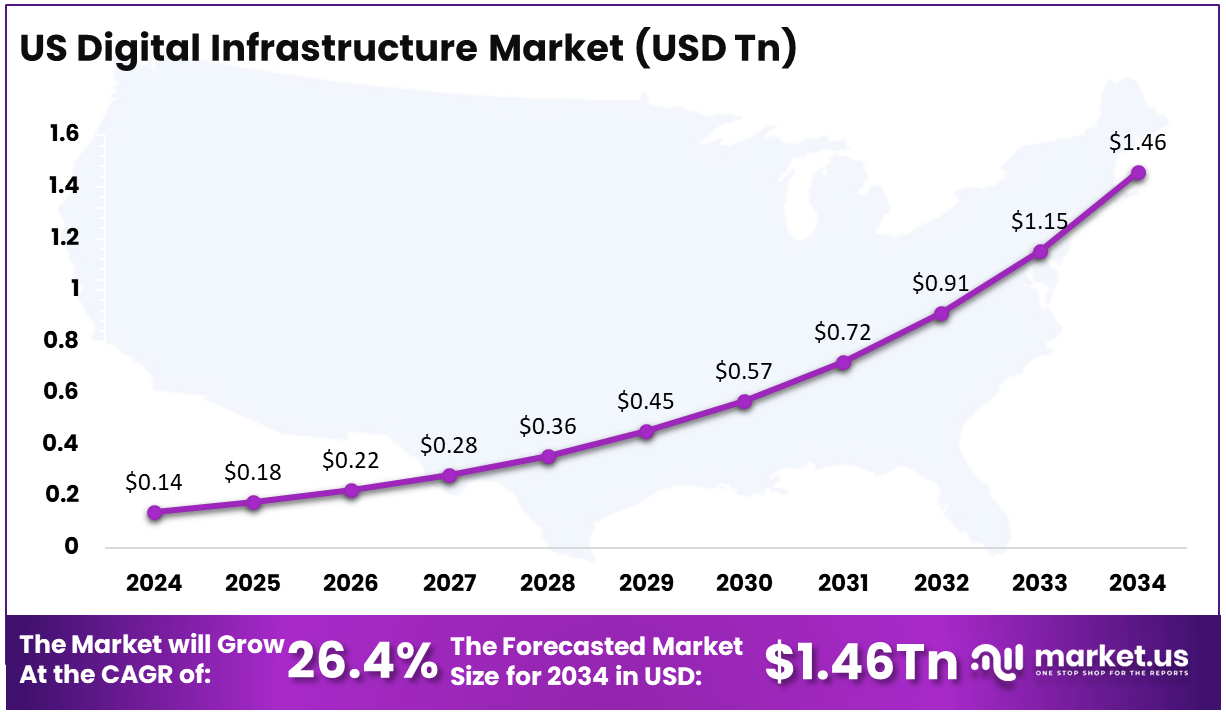

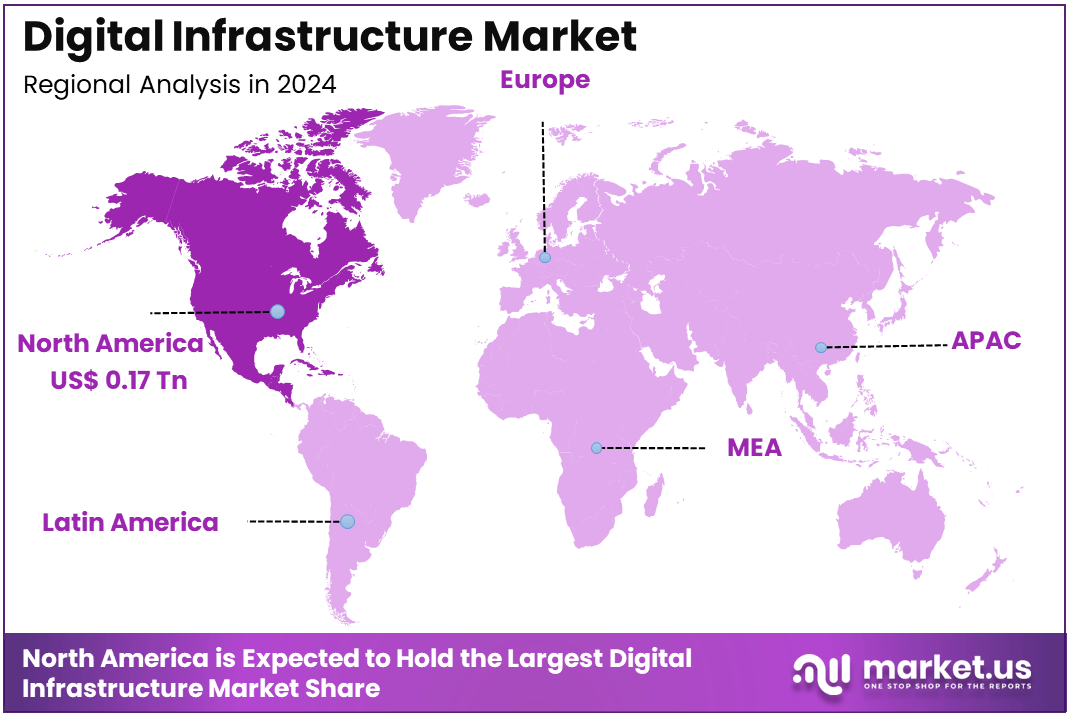

In 2024, North America held a dominant market position, capturing over a 42.8% share and earning USD 0.17 Trillion in revenue. Further, the United States dominates the market size by USD 0.14 Trillion, holding a strong position steadily with a CAGR of 26.4%.

Digital infrastructure refers to the foundational technologies and systems that support the delivery of digital services and applications. This includes physical components like data centers, servers, and networking hardware, as well as software-based technologies such as cloud platforms and communication networks.

Together, these elements enable organizations to operate efficiently, store and process data, and facilitate seamless communication. In essence, digital infrastructure is the backbone that supports modern digital operations and connectivity.

Key Takeaways

- Market Growth: The Digital Infrastructure Market is expected to grow from USD 0.41 trillion in 2024 to USD 4.55 trillion by 2034, expanding at a CAGR of 27.20% over the forecast period.

- By Component: Hardware Dominates the segment by the largest share 53.1% widely.

- Dominant Deployment Type: The On-Premises segment leads the market, accounting for 58.5% of total deployment, as businesses prioritize data security, control, and compliance in their digital operations.

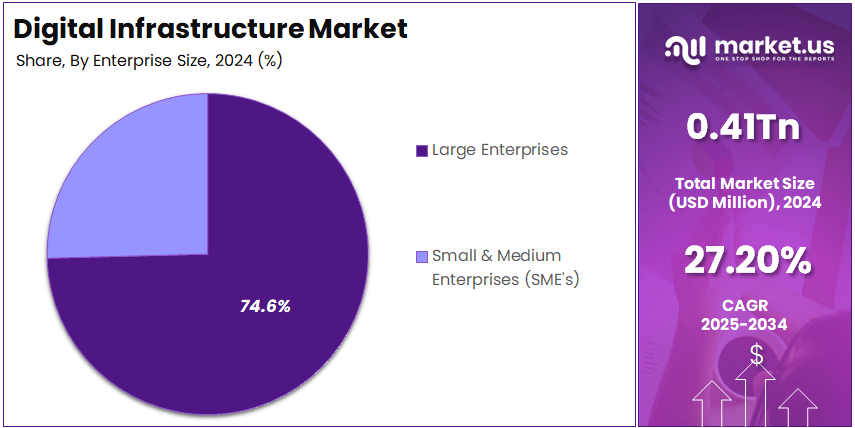

- Enterprise Size Leadership: Large Enterprises hold the largest share at 74.6%, driven by significant investments in cloud computing, data centers, and AI-powered infrastructure.

- Leading End-User Industry: The IT & Telecom sector dominates the market with a 34.6% share, fueled by the expansion of 5G networks, cloud services, and digital transformation initiatives.

- Regional Dominance: North America holds the largest regional share at 42.8%, owing to advanced digital infrastructure, high technology adoption rates, and government investments in smart cities and connectivity.

- The U.S. Market: The United States contributed USD 0.14 trillion to the market in 2024, growing steadily with a CAGR of 26.4%, driven by strong demand for data centers, cloud services, and AI-driven automation.

Analyst Viewpoint

The escalating adoption of digital services in sectors such as finance, healthcare, and education has intensified the demand for reliable digital infrastructure. Organizations are increasingly investing in scalable and secure infrastructure solutions to support their digital transformation initiatives and meet the growing expectations of consumers for seamless digital experiences.

Emerging markets present significant opportunities for digital infrastructure development. Regions with expanding internet penetration and increasing digital adoption are ripe for investments in data centers, network expansion, and cloud services. Additionally, the integration of advanced technologies like artificial intelligence and the Internet of Things (IoT) into infrastructure solutions offers avenues for innovation and enhanced service delivery.

Major Driving Factors

- Rising Demand for Data Centers: The proliferation of cloud computing and data-intensive applications has led to a heightened need for advanced data center facilities. For instance, companies like Keppel Corp have reported significant increases in profits from their data center businesses, indicating strong market demand.

- Expansion of 5G Networks: The rollout of 5G technology is enhancing connectivity and enabling faster data transmission, thereby driving investments in supporting infrastructure. This development is crucial for applications requiring low latency and high-speed communication.

Technological Advancements

- Artificial Intelligence Integration: AI is being utilized to optimize infrastructure management, enhance security protocols, and improve data analytics capabilities, leading to more efficient operations.

- Edge Computing: By processing data closer to its source, edge computing reduces latency and bandwidth usage, which is essential for applications like autonomous vehicles and real-time analytics.

- Sustainable Energy Solutions: There is a growing focus on incorporating renewable energy sources into infrastructure planning to reduce environmental impact and promote sustainability.

Market Key Statistics

- Fixed lines: In 2023, over 1 billion minutes were called from fixed lines, which is less than 88 minutes per capita per year. As of 2023, there were 1,201,245 fixed telephone voice subscriptions.

- Mobile phones: In 2023, 28 billion minutes were used from mobile phones, which is 2.5 thousand per inhabitant per year. Mobile telephone subscriptions totaled 15,550,217 in 2023.

- Fixed Internet connections: There were almost 4 million fixed Internet connections in the Czech Republic in 2023. The number of fixed connections with speeds of 100 Mbit/s or more increased from 800,000 to 1.8 million between 2018 and 2023. Specifically, there were 1,789,832 active connections with speeds of 100 Mbit/s+ in 2023.

- Fixed broadband subscriptions: In 2023, there were 4,080,548 active fixed broadband subscriptions.

- Households: Residential subscriptions numbered 3,381,000.

- Organizations: Business subscriptions numbered 700,000.

- Fixed broadband speed categories (active connections):

- Less than 10 Mbit/s: 95,000

- ≥ 10 and less than 30 Mbit/s: 795,000

- ≥ 30 and less than 100 Mbit/s: 1,404,000

- ≥ 100 Mbit/s: 1,790,000

- Fixed access technology (active connections):

- Wired fixed access, total: 2,504,000

- DSL (including FTTC): 1,014,000

- Fibre (FTTH/B): 884,000

- Cable (CATV): 605,000

- Wireless fixed access, total: 1,577,000

- Fixed WiFi: 1,123,000

- Fixed LTE/5G: 454,000

- Wired fixed access, total: 2,504,000

- Mobile data: The number of residential and business subscriptions with mobile data services in Czechia was almost three times higher than the number of fixed broadband subscriptions at the end of 2023.

Regional Analysis

US Digital Infrastructure Market

Further, in North America, the United States dominates the market size, reaching USD 0.14 trillion in 2024, maintaining its strong position with a steady CAGR of 26.4%. The region’s leadership is driven by rapid advancements in 5G deployment, cloud computing, AI-driven automation, and data center expansions.

With a strong digital economy and high adoption of emerging technologies, North America remains at the forefront of investments in next-generation infrastructure. Businesses across various industries, including IT & Telecom, healthcare, finance, and manufacturing, are heavily investing in on-premises and cloud-based digital solutions to enhance operational efficiency and scalability.

The increasing demand for smart cities, edge computing, and AI-powered automation is further fueling market expansion in North America. The region is also benefiting from government initiatives promoting digital transformation and cybersecurity advancements, ensuring that enterprises can operate efficiently with secure and resilient digital networks.

The U.S. leads due to its robust data center infrastructure, rapid 5G network rollout, and increased enterprise adoption of AI and cloud computing. As businesses continue digitizing their operations, the demand for high-performance, scalable, and secure digital infrastructure will keep growing, reinforcing North America’s leadership in the global market.

North America Digital Infrastructure Market

In 2024, North America held a dominant market position, capturing more than a 42.8% share, holding USD 0.17 trillion in revenue. The region’s leadership is primarily driven by rapid advancements in cloud computing, 5G networks, AI-driven automation, and data center expansions.

The presence of major technology firms, cloud service providers, and telecommunication giants in the U.S. and Canada has fueled significant investments in next-generation digital infrastructure. With enterprises prioritizing on-premises solutions and cloud-based platforms for enhanced security and scalability, North America continues to set the benchmark for global digital transformation.

This growth is attributed to the increasing adoption of AI-powered data centers, IoT integration, and smart city initiatives. Companies across industries such as IT & telecom, healthcare, financial services, and manufacturing are driving demand for high-performance computing, edge computing, and cybersecurity solutions to support their digital operations.

Additionally, the expansion of 5G connectivity and the rising demand for low-latency cloud services are accelerating infrastructure development. North America’s focus on data privacy, regulatory compliance, and cybersecurity has also led to increased investment in secure on-premises infrastructure, which accounts for 58.5% of the regional deployment.

As digital transformation continues, North America is expected to maintain its leadership in the global Digital Infrastructure Market, driven by innovation, large-scale enterprise adoption, and government-backed technology initiatives. With smart cities, AI-driven automation, and cloud computing becoming the new standard, North America’s digital infrastructure is set for continued growth and evolution in the coming years.

Key Player Analysis

The Digital Infrastructure Market is witnessing rapid expansion, driven by the increasing demand for cloud computing, AI-driven data centers, and next-generation networking solutions. Leading market players are making substantial investments in data center expansions, 5G infrastructure, and edge computing technologies to support the growing digital ecosystem.

One of the major areas of focus is the growth of AI-based services, which has significantly boosted data center investments. Companies are increasing their digital infrastructure spending to support high-performance computing, big data analytics, and machine learning applications. Over the past year, data center-related revenue for key players has increased by more than 40%, reflecting the rising demand for secure, scalable, and high-speed computing environments.

The market is also witnessing large-scale acquisitions and infrastructure investments, with firms allocating billions of dollars toward cloud storage, fiber-optic networks, and hyperscale data centers. Several industry players have committed to sustainable energy solutions to power their digital infrastructure, as concerns over carbon emissions and energy consumption continue to rise.

Top Key Players in the Market

- Cisco Systems, Inc.

- International Business Machines Corp (IBM)

- Amazon Web Services, Inc.

- Microsoft Corporation

- Honeywell International, Inc.

- Huawei Technologies Co., Ltd.

- ABB Ltd.

- Schneider Electric SE

- Hitachi, Ltd.

- Johnson Controls International PLC

- Others

With global investments in AI-driven infrastructure, 5G rollouts, and cybersecurity, the Digital Infrastructure Market is set to see sustained growth over the next decade. As enterprises continue their digital transformation journeys, key players are expected to innovate, expand, and enhance their infrastructure offerings to meet the evolving technological landscape.

By Component

In 2024, the Hardware segment held a dominant market position in the Digital Infrastructure Market, capturing more than a 53.1% share. This dominance can be attributed to the increasing demand for physical infrastructure to support growing data and connectivity needs across industries.

Servers, networking equipment (such as routers, switches, and firewalls), and storage devices are fundamental components of digital infrastructure, enabling organizations to manage and secure large volumes of data. As more businesses embrace digital transformation and cloud computing, the demand for reliable, scalable hardware has surged.

The growing adoption of Internet of Things (IoT) devices also contributes to the expansion of this segment, as companies integrate IoT solutions into their operations to drive efficiencies and innovate. In particular, industries like manufacturing, healthcare, and retail are heavily investing in these devices for real-time monitoring and data analytics.

As the need for robust, high-performance hardware continues to rise, it is expected that the hardware segment will maintain its lead, driven by advancements in technology and the increasing reliance on digital platforms for business operations.

By Deployment Type

In 2024, the On-Premises segment held a dominant market position, capturing more than a 58.5% share of the Digital Infrastructure Market. This growth is primarily driven by the increasing demand for data security, regulatory compliance, and full control over digital operations. Many large enterprises, particularly in industries such as banking, financial services, healthcare, and government sectors, prefer on-premises infrastructure due to strict data privacy laws and security concerns.

Unlike cloud-based solutions, on-premises digital infrastructure provides businesses with direct control over their hardware, software, and network resources, ensuring higher customization, security, and operational reliability. This is especially important for companies dealing with sensitive data, intellectual property, or mission-critical applications that require strict access control.

Furthermore, advancements in AI-driven automation, edge computing, and high-performance computing (HPC) have enabled organizations to enhance their on-premises infrastructure while maintaining cost efficiency and scalability. Many enterprises are adopting hybrid models, integrating on-premises infrastructure with private cloud solutions to achieve a balance between security and flexibility.

With businesses continuing to prioritize cybersecurity, regulatory compliance, and performance optimization, the On-Premises segment is expected to remain a key contributor to the Digital Infrastructure Market, reinforcing its dominance in enterprise deployments.

By Enterprise Size

In 2024, the Large Enterprises segment held a dominant market position, capturing more than a 74.6% share of the Digital Infrastructure Market. This dominance is fueled by high investment capacities, advanced technology adoption, and the need for secure, scalable, and high-performance infrastructure to support complex business operations.

Large enterprises operate across multiple locations and handle vast amounts of data, applications, and mission-critical workloads, requiring robust IT infrastructure with advanced computing power, cybersecurity, and data storage capabilities.

These organizations prioritize on-premises and hybrid cloud solutions to maintain greater control, security, and regulatory compliance, especially in industries such as banking, finance, healthcare, and manufacturing where data privacy and operational reliability are crucial.

Furthermore, large corporations are heavily investing in AI-driven automation, IoT connectivity, edge computing, and high-speed networking to enhance their digital transformation efforts. With the increasing demand for big data analytics, cloud computing, and enterprise software solutions, the Large Enterprises segment continues to lead the market, ensuring seamless digital operations while driving innovation and efficiency.

By End User

In 2024, the Large Enterprises segment held a dominant market position, capturing more than a 74.6% share of the Digital Infrastructure Market. This dominance is fueled by high investment capacities, advanced technology adoption, and the need for secure, scalable, and high-performance infrastructure to support complex business operations.

Large enterprises operate across multiple locations and handle vast amounts of data, applications, and mission-critical workloads, requiring robust IT infrastructure with advanced computing power, cybersecurity, and data storage capabilities. These organizations prioritize on-premises and hybrid cloud solutions to maintain greater control, security, and regulatory compliance, especially in industries such as banking, finance, healthcare, and manufacturing where data privacy and operational reliability are crucial.

Furthermore, large corporations are heavily investing in AI-driven automation, IoT connectivity, edge computing, and high-speed networking to enhance their digital transformation efforts. With the increasing demand for big data analytics, cloud computing, and enterprise software solutions, the Large Enterprises segment continues to lead the market, ensuring seamless digital operations while driving innovation and efficiency.

As companies scale their operations globally, the demand for high-performance digital infrastructure will remain strong, reinforcing large enterprises’ dominance in the Digital Infrastructure Market for the foreseeable future.

Key Market Segments

By Component

- Hardware

- Servers

- Networking Equipment

- Routers

- Switches

- Firewalls

- Others

- Storage Devices

- Internet of Things (IoT) Devices

- Others

- Software

- Database Management Systems (DBMS)

- Middleware Software

- Cloud Management Platforms

- Cyber Security Software

- Others (Data Processing, Storage, and Communication, etc.)

- Services

- Professional Services

- Managed Services

By Deployment Type

- On-Premises

- Cloud-Based

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SME’s)

By End User

- IT & Telecom

- BFSI

- Retail

- Government

- Manufacturing

- Healthcare

- Others

Driving Factors

Surge in Data Consumption and Cloud Computing Adoption

The exponential increase in data consumption, coupled with the widespread adoption of cloud computing, is a primary driver of the digital infrastructure market’s growth. As businesses and individuals generate and utilize vast amounts of data daily, the demand for robust and scalable digital infrastructure has intensified.

Cloud computing services have become integral to modern business operations, offering flexibility and cost-efficiency. The convenience of accessing data and applications over the internet has led to increased reliance on cloud platforms, further propelling the need for advanced digital infrastructure.

This trend is not only prevalent in large enterprises but also among small and medium-sized businesses seeking to enhance their digital capabilities. The growing adoption of digital technologies by businesses and consumers alike underscores the necessity for robust digital infrastructure to support the increasing volume of data traffic and processing.

Restraining Factors

High Initial Capital Expenditure and Prolonged Deployment Timelines

Despite the promising growth trajectory, the digital infrastructure market faces challenges related to substantial initial capital investments and extended deployment periods. Establishing state-of-the-art data centers and upgrading network infrastructures require significant financial resources.

These prolonged timelines can deter enterprises from timely market entry, potentially resulting in missed opportunities and reduced competitiveness. Additionally, the rapid pace of technological advancements poses a risk of infrastructure becoming obsolete before achieving a return on investment. Businesses must carefully weigh the benefits against the financial and temporal commitments involved in deploying new digital infrastructure.

Growth Opportunities

Expansion in Emerging Markets and 5G Deployment

Emerging markets present a substantial growth opportunity for the digital infrastructure sector. Regions such as Asia-Pacific, Latin America, and parts of Africa are experiencing rapid digital transformation, characterized by increased internet penetration, smartphone adoption, and a burgeoning middle class.

This digital evolution necessitates the development of robust infrastructure to support connectivity and data services. The Asia Pacific is projected to exhibit substantial growth in the digital infrastructure market during the forecast period, driven by the increasing demand for digital infrastructure solutions in countries like China, India, and Japan.

Furthermore, the global rollout of 5G technology is set to revolutionize communication networks, offering faster speeds and lower latency. The deployment of 5G networks requires significant upgrades to existing infrastructure, including the installation of new base stations and fiber-optic networks. This development opens avenues for investment in both urban and rural areas, aiming to enhance connectivity and support advanced applications such as the Internet of Things (IoT) and autonomous vehicles.

Challenging Factors

Ensuring Cybersecurity and Data Privacy

As digital infrastructure becomes increasingly integral to business operations and daily life, ensuring cybersecurity and data privacy has emerged as a formidable challenge. The proliferation of data breaches, cyber-attacks, and unauthorized data access incidents has heightened concerns among consumers and enterprises alike. Protecting sensitive information from malicious actors requires continuous investment in advanced security measures and protocols.

Moreover, stringent data protection regulations, such as the General Data Protection Regulation (GDPR) in Europe, impose strict compliance requirements on organizations. Non-compliance can result in substantial fines and reputational damage. Organizations must navigate the complex landscape of varying international data privacy laws while implementing robust security frameworks.

Additionally, the rapid integration of IoT devices and the expansion of cloud services increase potential vulnerabilities within digital infrastructures. Ensuring end-to-end security across diverse platforms and devices necessitates a comprehensive and adaptive approach to cybersecurity.

Growth Factors

Rising Data Consumption and Cloud Adoption

The surge in data consumption and the widespread adoption of cloud services are pivotal growth drivers in the digital infrastructure market. This growth is fueled by the increasing reliance on digital technologies across various sectors, necessitating robust and scalable infrastructure solutions.

The proliferation of Internet of Things (IoT) devices and the expansion of cloud computing services have significantly contributed to this upward trend. As businesses and consumers generate and consume more data, the demand for efficient data storage, processing, and transmission continues to escalate.

Emerging Trends

Edge Computing and AI Integration

A notable emerging trend in the digital infrastructure landscape is the integration of edge computing and artificial intelligence (AI). Edge computing brings data processing closer to the data source, reducing latency and enhancing real-time data analysis.

Simultaneously, AI applications are becoming increasingly prevalent, driving the need for infrastructure capable of supporting high computational requirements. The convergence of edge computing and AI enables more efficient data handling and processing, facilitating advancements in sectors such as autonomous vehicles, smart cities, and industrial automation.

Business Benefits

Enhanced Agility and Competitive Advantage

Investing in modern digital infrastructure offers businesses enhanced agility and a competitive edge. With scalable and secure infrastructure, companies can swiftly adapt to changing market dynamics, customer preferences, and technological advancements. This adaptability allows for rapid deployment of new services and applications, meeting customer demands effectively.

Moreover, robust digital infrastructure supports seamless integration of emerging technologies, such as AI and IoT, enabling businesses to innovate and optimize operations. This strategic advantage not only improves operational efficiency but also positions companies to capitalize on new market opportunities, driving growth and profitability.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Recent Developments

- In 2024: RackBank Datacenters unveiled plans for an AI-centric data center in Madhya Pradesh. Located in Indore, the facility will be developed in four phases.

- In 2024: Hewlett Packard Enterprise and Dell Technologies launched new servers designed for training large language models (LLMs).

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 0.41 Trillion |

| Forecast Revenue (2034) | USD 4.55 Trillion |

| CAGR (2025-2034) | 27.20% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Hardware [Servers, Networking Equipment {Routers, Switches, Firewalls, Others}, Storage Devices, Internet of Things (IoT) Devices, Others], Software [Database Management Systems (DBMS), Middleware Software, Cloud Management Platforms, Cyber Security Software, Others (Data Processing, Storage, and Communication, etc.)], Services [Professional Services, Managed Services]), By Deployment Type (On-Premises, Cloud Based), By Enterprise Size (Large Enterprises, Small & Medium Enterprises (SMEs)), By End User (IT & Telecom, BFSI, Retail, Government, Manufacturing, Healthcare, Others) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Cisco Systems, Inc., International Business Machines Corp (IBM), Amazon Web Services, Inc., Microsoft Corporation, Honeywell International, Inc., Huawei Technologies Co., Ltd., ABB Ltd., Schneider Electric SE, Hitachi, Ltd., Johnson Controls International PLC, Others |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |