Quick Navigation

- Report Overview

- Key Takeaways

- U.S. Data Center GPU Market

- Analysts’ Viewpoint

- Deployment Mode Analysis

- Function Analysis

- End User Analysis

- Key Market Segments

- Driver

- Restraint

- Investment Opportunity

- Challenge

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Regions and Countries

- Key Players Analysis

- Top Opportunities Awaiting for Players

- Recent Developments

- Report Scope

Report Overview

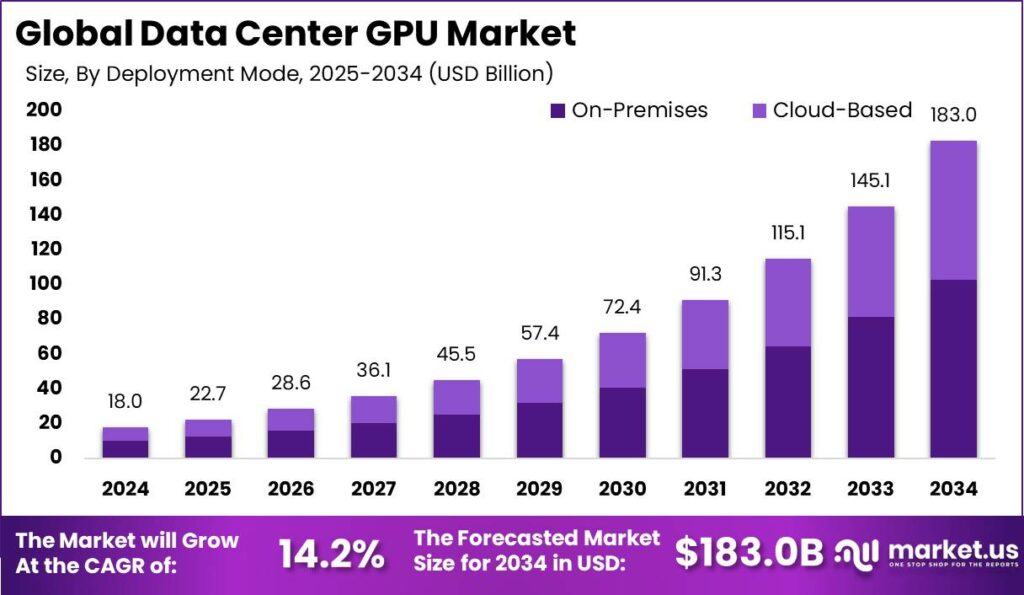

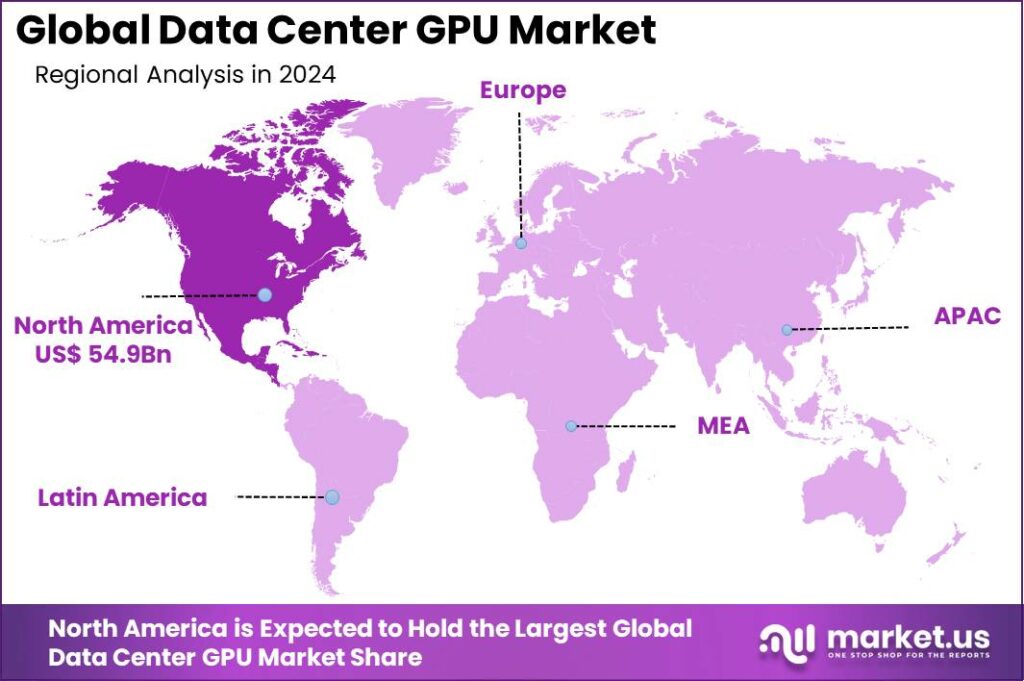

The Global Data Center GPU Market size is expected to be worth around USD 183 billion by 2034, from USD 18 billion in 2024, growing at a CAGR of 14.2% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 37.1% share, holding USD 6.6 Billion revenue.

A Data Center GPU (Graphics Processing Unit) is specifically designed and optimized for handling extensive computational and graphical operations within data centers. These GPUs accelerate processing in applications like artificial intelligence (AI), machine learning, and big data analytics, which are integral to modern IT environments.

The market for Data Center GPUs has witnessed significant growth, driven by the increasing demands for high-performance computing across various industries. This market expansion can be attributed to the rising need for faster data processing and the growth of AI and machine learning applications which require substantial computational power.

For instance, according to PIB.gov, As of November 2024, 5G subscriptions in India, Nepal, and Bhutan are expected to surpass 270 million, accounting for 23% of total mobile subscriptions. By 2030, this number is projected to rise to 970 million, making up 74% of all mobile connections in the region.

According to hpcwire, In 2023, Nvidia experienced a significant expansion in its data-center GPU shipments, which reached an impressive total of approximately 3.76 million units, as reported by TechInsights. This represents a substantial increase from the 2.64 million units shipped in 2022, marking a growth of over 1 million units within a year. Such a rise underscores Nvidia’s continued dominance in this sector.

Nvidia maintained a commanding 98% market share in data-center GPU shipments for 2023, mirroring its market position from the previous year. Including contributions from competitors AMD and Intel, the overall data-center GPU market grew to about 3.85 million units in 2023, up from 2.67 million units in 2022.

Notably, Nvidia’s revenue from data-center GPUs soared to $36.2 billion, a significant leap from $10.9 billion in the prior year, which demonstrates a more than threefold increase in revenue. This financial achievement further highlights Nvidia’s strong market presence and the robust demand for its GPU products in data centers.

Key Takeaways

- In 2024, the On-Premise segment held a dominant market position, capturing more than a 56.4% share of the Global Data Center GPU Market.

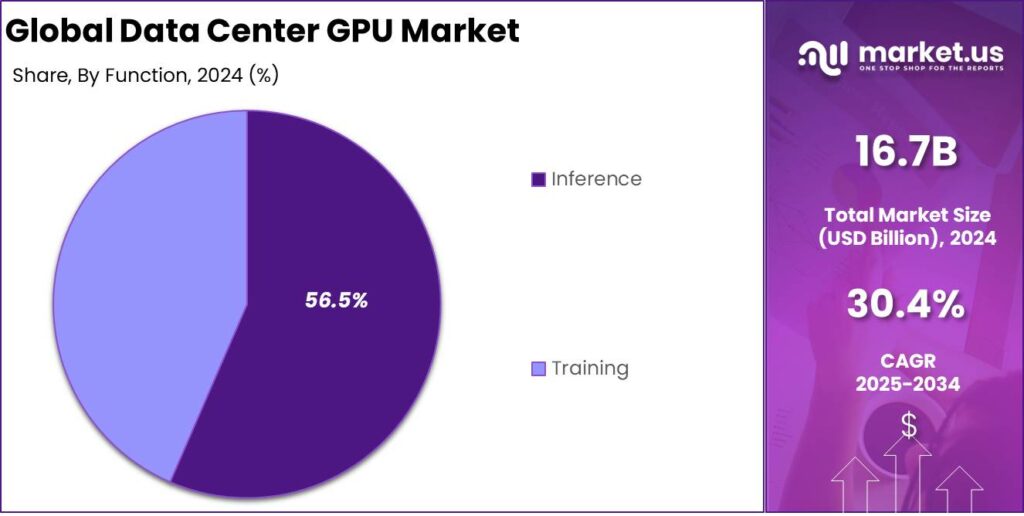

- In 2024, the Inference segment held a dominant market position within the Data Center GPU market, capturing more than a 56.5% share.

- In 2024, the Cloud Service Providers (CSPs) segment held a dominant market position, capturing more than a 48.9% share of the Global Data Center GPU Market.

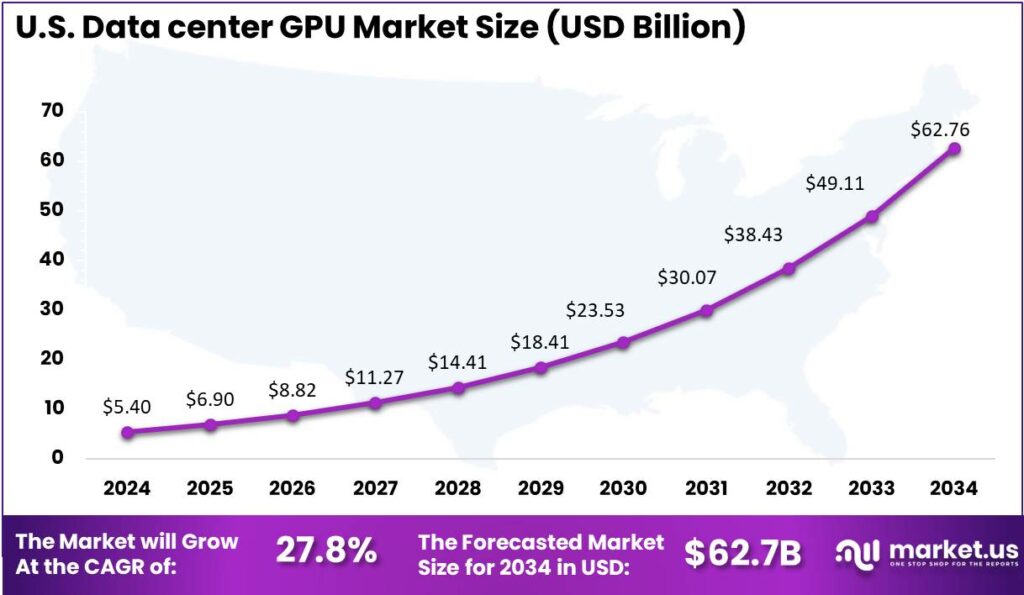

- The US Data Center GPU Market was valued at USD 5.4 billion in 2024, with a robust CAGR of 27.8%.

- In 2024, North America held a dominant market position in the global Data Center GPU Market, capturing more than a 37.1% share.

- According to GBL.gov, data centers consumed about 76 TWh, representing 1.9% of total annual electricity consumption in U.S. data center energy use has continued to grow. This represents the need to adopt data center GPU.

U.S. Data Center GPU Market

The US Data Center GPU Market was valued at USD 5.4 billion in 2024, with a robust CAGR of 27.8%. The US is a home to leading technology companies such as NVIDIA, Intel and AMD, which are at the forefront of GPU innovation and development. These companies invest heavily in research and development, driving advancements in GPU technology.

Additionally, the US has a strong focus on high performance computing (HPC), which needs powerful GPU for complex computations in sectors such as finance, healthcare and autonomous driving. This drives the adoption of GPUs in the data centers to support these advanced applications.

In 2023, North America held a dominant market position in the global Data Center GPU Market, capturing more than a 37.1% share. the North American governments, through initiatives like Better Buildings Data Center Challenge, are encouraging the adoption of energy efficient GPU solutions to minimize the carbon footprints. This support promotes the use of GPUs in data centers for sustainability and efficiency.

Additionally, with the increasing concerns about data security, and regulatory compliance, North American organizations invest in GPUs with strong encryption and multi-tendency capabilities to ensure data integrity and privacy.

Analysts’ Viewpoint

The market is witnessing a surge in demand from cloud service providers and enterprises that are integrating AI to improve efficiency and customer experience. Cloud deployments are expected to see the highest growth due to their scalability and reduced operational costs.

The adoption of GPUs in data centers is crucial for training and deploying AI models, supporting a variety of computationally intensive tasks. GPUs have become an integral component of data centers with a specific focus on applications requiring high computational power.

The increasing volume of data and the complexity of tasks performed by AI and machine learning models have necessitated the widespread adoption of GPUs. The demand is particularly high in regions like North America and Asia Pacific, where technological advancements and digital transformation initiatives are more pronounced.

The Data Center GPU market presents numerous investment opportunities, particularly in developing regions and sectors embracing digital transformation. Investors are particularly keen on companies and startups that are innovating in GPU technology or developing GPU-accelerated applications for sectors such as automotive, healthcare, and public services.

Deployment Mode Analysis

In 2024, the On-Premise segment held a dominant market position, capturing more than a 56.4% share of the Global Data Center GPU Market. This segment’s leading position can be attributed to its ability to offer greater control over hardware and data security, which is particularly valued in sectors handling sensitive information, such as finance and healthcare.

Organizations opting for on-premise deployment tend to prioritize data sovereignty and security, which GPUs installed onsite more reliably ensure compared to cloud-based solutions. The preference for on-premise GPUs is further supported by their role in high-performance computing (HPC) tasks that require rapid processing close to the data source, reducing potential latency issues that can occur with cloud deployments.

For industries like scientific research, engineering, and defense, where real-time data processing and analysis are critical, the reduced latency and direct control over computing assets make on-premise GPUs an indispensable tool.

Moreover, the initial higher capital expenditure for on-premise setups is often offset by long-term benefits such as avoiding ongoing cloud service fees and having direct control over hardware upgrades, which appeals to organizations looking to maximize their investment in GPU capabilities for the long haul. Additionally, having on-premise infrastructure allows companies to customize their computing environment to specific operational requirements, which can lead to optimized performance for specialized tasks.

Function Analysis

In 2024, the Inference segment held a dominant market position within the Data Center GPU market, capturing more than a 56.5% share. This segment’s leadership is primarily attributed to the widespread deployment of AI models in production environments where inference tasks are critical.

The dominance of the Inference segment is strengthened by the growing use of AI in consumer services and IoT devices, which require rapid data processing for timely outputs. This demand for high-speed inference GPUs is especially prominent in sectors like automotive, healthcare, and retail, where real-time data interpretation and decision-making are essential.

Moreover, advancements in GPU technology have significantly enhanced their efficiency and cost-effectiveness for inference tasks. Modern inference GPUs are designed to deliver greater throughput at lower latency, which is vital for applications such as video analytics and autonomous vehicles.

The growth of edge computing has significantly driven the inference segment, as data is processed closer to its source. GPUs are well-suited for providing the powerful inference capabilities required at the edge. With the rise of smart devices and edge data centers, the demand for efficient, localized data processing solutions is expected to keep growing.

End User Analysis

In 2024, the Cloud Service Providers (CSPs) segment of the Data Center GPU market held a dominant market position, capturing more than a 48.9% share. This leadership is primarily due to the escalating demand for high-performance computing powered by GPUs, which are crucial for running advanced artificial intelligence (AI) and machine learning (ML) workloads efficiently.

CSPs such as Amazon Web Services, Microsoft Azure, and Google Cloud have been at the forefront of integrating GPUs into their cloud infrastructures to cater to the growing needs of industries ranging from healthcare to finance, where rapid data processing and deep learning capabilities are vital. The substantial market share held by CSPs is also a reflection of the broader trend towards digital transformation and cloud adoption across sectors.

For instance, according to According to the 2024 Global Public Sector Enterprise Cloud Index (ECI) report, 45% of public sector is using a hybrid cloud operating model, while 8% is using a hybrid multi-cloud model. This landscape is expected to change dramatically within 1-3 years, with 33% planning to adopt a hybrid multi-cloud model and 31% planning to use multiple public clouds.

Enterprises are increasingly reliant on cloud platforms for not only data storage but also for computational power to handle intensive tasks that require real-time processing. This has spurred CSPs to enhance their offerings by deploying GPUs extensively to ensure they can meet customer demands for speed and efficiency.

Moreover, the strategic partnerships and continuous innovations by major tech companies have fortified the CSPs’ market position. Collaborations aimed at optimizing cloud services with advanced GPU capabilities ensure that CSPs can offer cutting-edge solutions, thereby attracting a broader customer base seeking to leverage AI for business transformation. These factors collectively underpin the strong performance and growth prospects of the CSP segment in the Data Center GPU market.

Key Market Segments

By Deployment Mode

- Cloud-Based

- On-Premise

By Function

- Training

- Inference

By End User

- Cloud Service Providers (CSPs)

- Enterprises

- Government

Driver

Increased Demand for AI and Machine Learning Workloads

The growth in the data center GPU market is significantly driven by the increasing demand for artificial intelligence (AI) and machine learning (ML) applications. GPUs are pivotal in managing and accelerating AI workloads because of their ability to perform parallel processing efficiently. This capability is crucial in handling complex algorithms and large datasets typical in AI applications.

Industries such as healthcare, finance, and autonomous driving, which rely heavily on AI and ML technologies, are particularly instrumental in propelling the demand for GPUs in data centers. The adoption of cloud services and the expansion of AI capabilities in enterprises further amplify this demand, as cloud service providers like AWS, Microsoft Azure, and Google Cloud continuously enhance their AI infrastructure with high-performance GPUs.

Restraint

Supply Chain Disruptions and High Cost of Implementation

One of the main restraints facing the data center GPU market is the vulnerability of the supply chain, which can lead to fluctuations in GPU availability and prices. The semiconductor supply chain has faced significant disruptions, which affect the production and distribution of GPUs.

Additionally, the high cost associated with implementing and maintaining advanced GPU-accelerated data centers poses a significant barrier, especially for small to medium-sized enterprises. These costs are not limited to the initial acquisition of the hardware but also extend to ongoing expenses related to energy consumption, cooling, and technical support, making it a considerable investment.

Investment Opportunity

Expansion into Emerging Technologies and Regions

The data center GPU market holds substantial opportunities for growth through the integration of emerging technologies such as high-performance computing (HPC), big data analytics, and the Internet of Things (IoT). GPUs are essential for the efficient processing and analysis of the vast amounts of data generated by these technologies.

Additionally, the expansion of 5G networks enhances the capabilities of edge computing, where data is processed closer to its source, thus requiring robust GPU support. Geographically, the Asia Pacific region presents significant opportunities due to its rapid technological adoption and the development of digital infrastructure, particularly in countries like China, India, and Japan.

Challenge

Technological Complexity and Energy Consumption

A major challenge in the data center GPU market is managing the technological complexity and high energy consumption associated with GPU deployments. As data centers expand their GPU capabilities to support more advanced applications, the complexity of the infrastructure also increases. This complexity requires skilled personnel for management and maintenance. F

urthermore, GPUs are high-energy-consuming devices, which adds to the operational costs and impacts the environmental footprint of data centers. Balancing the need for high computational power with energy efficiency and cost-effectiveness remains a significant challenge for the industry.

Growth Factors

Rapid Expansion of AI and Cloud Computing

The data center GPU market is experiencing substantial growth primarily due to the rapid expansion of artificial intelligence (AI) and cloud computing applications. GPUs are essential for efficiently processing complex computations needed in AI training and inference tasks across various industries, including healthcare, finance, and automotive sectors.

The demand is further propelled by the shift towards cloud services, where major providers such as Amazon Web Services, Microsoft Azure, and Google Cloud are intensifying their GPU capabilities to offer enhanced AI and machine learning services. This demand is supported by the globalization of digital services necessitating robust, high-performance computing infrastructures that can handle large-scale AI workloads.

Emerging Trends

Adoption of Edge Computing and AI Advancements

Emerging trends within the data center GPU market include the significant adoption of edge computing and ongoing advancements in AI technologies. Edge computing involves processing data closer to the source of data generation, which reduces latency and accelerates data processing times, crucial for real-time applications such as IoT and autonomous systems.

Concurrently, advancements in AI, including deeper and more complex neural networks, require the parallel processing capabilities that GPUs provide, making them increasingly vital in data centers. This trend is compounded by technological innovations in GPU architecture that enhance performance and energy efficiency, thereby supporting the sophisticated requirements of modern AI applications.

Business Benefits

Enhanced workflow efficiency is another advantage. With faster rendering and processing times, teams can collaborate more effectively, reducing bottlenecks and improving productivity. This efficiency is crucial in industries where time-to-market and rapid innovation are competitive differentiators.

Over 80% of data center operators report significant capacity expansions specifically for AI workloads, with 64% actively deploying GPU clusters optimized for machine learning as per Data Center World report.

GPU adoption drives cost savings by shifting tasks from CPUs to GPUs, optimizing hardware usage, and potentially reducing the need for extra servers. This results in lower capital and operational costs, along with reduced energy consumption and space requirements.

GPUs allow data centers to handle increasing workloads without significant infrastructure changes. Breakthroughs in energy efficiency are transforming data centers, with liquid-cooled GPU systems reducing energy use by up to 40%. Meanwhile, new NVIDIA chips are slashing AI training times from 32 hours to just 1 second according to Data Center Frontier report.

GPUs provide the necessary computational power to develop and deploy cutting-edge technologies, driving business growth and opening new revenue streams. According to Sohu, a $130 million GPU cluster project in China aims to support surging AI demand, targeting a 32% revenue boost for its developers by 2026

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Several leading companies dominate the GPU market, each bringing their own innovations to meet the growing demand for computational power in data centers.

NVIDIA is widely recognized as the leader in the GPU market, especially when it comes to data centers. NVIDIA transformed the GPU industry with high-performance products for AI and machine learning, leveraging technologies like CUDA and DGX systems to stay at the market’s forefront.

Intel Corporation, traditionally known for its CPUs, has made significant inroads into the GPU market with its acquisition of Habana Labs and the development of its own line of GPUs tailored for data centers. The Intel Xe graphics architecture is designed for high-performance computing workloads, offering strong performance in AI, deep learning, and data analytics.

Advanced Micro Devices, Inc. (AMD) has emerged as a major challenger to NVIDIA’s dominance in the GPU space. AMD’s Radeon Instinct series, targeting high-performance computing and data centers, competes directly with NVIDIA’s offerings. The company has made significant strides in offering GPUs with competitive performance and cost efficiency, appealing to a broad range of data center users.

Top Key Players in the Market

- NVIDIA Corporation

- Intel Corporation

- Advanced Micro Devices, Inc.

- Micron Technology, Inc.

- IBM

- Samsung SDS

- Qualcomm Technologies, Inc.

- Google Cloud

- Imagination Technologies

- Huawei Cloud Computing Technologies Co., Ltd.

- Others

Top Opportunities Awaiting for Players

In analyzing the data center GPU market, several key opportunities have emerged for market players.

- Adoption of Edge Computing and 5G Technologies: The market is witnessing significant growth due to the increasing adoption of edge computing and the proliferation of 5G technologies. These advancements require substantial computational power, driving the demand for GPUs capable of supporting high-performance AI models and IoT device operations.

- Expanding Cloud Services: Cloud services are continuously growing, driven by their cost-efficiency, scalability, and ease of access. The increasing use of cloud computing services across various sectors, including healthcare, finance, and technology, is propelling the demand for GPUs that enhance the performance and scalability of cloud-based solutions.

- High-Performance AI and Machine Learning Workloads: There is a rising demand for GPUs due to their efficiency in training AI models and managing high-performance machine learning workloads. This is particularly relevant in training complex AI models and processing large datasets, which are integral in fields like healthcare and autonomous driving.

- Regional Market Expansion: The Asia-Pacific region is exhibiting rapid growth, influenced by advancements in digital infrastructure, smart city projects, and large-scale technology adoption. This regional dynamism presents a substantial opportunity for GPU market expansion, as local enterprises and governments invest in advanced computational infrastructure to support digital transformation initiatives.

- Sustainable and Energy-Efficient Computing Solutions: There is an increasing focus on developing sustainable and energy-efficient computing solutions. This trend is particularly pronounced in Europe, where there is a strong drive towards reducing carbon emissions and enhancing the energy efficiency of data centers. The adoption of GPUs that offer high performance with reduced energy consumption is becoming a critical factor in the market.

Recent Developments

- In January 2025, Nvidia revealed new chips for desktop and laptop PCs that use the same Blackwell architecture underpinning the company’s fastest artificial intelligence processors for servers and data centers.

- In November 2024, AMD launched new chip designs across its portfolio-datacenter, AI, networking, PC-with the software to back it up. The new generation of EPYC, codenamed “Turin,” includes different versions suited for scale-out (cloud) and scale-up (enterprise) workloads.

- In August 2024, NTT DATA announced the launch of its new Accelerated AI Platform in India today. This solution is designed to simplify the adoption of artificial intelligence (AI) for businesses of all sizes, from startups to large enterprises.

- In Feb. 2024, Iris Energy, a leading provider in renewable energy-powered data centers, disclosed its strategic move to provide GPU cloud services to Poolside, an AI company. This decision comes after rigorous testing and is set to involve the integration of 248 NVIDIA H100 GPUs.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 18.0 Bn |

| Forecast Revenue (2034) | USD 183.0 Bn |

| CAGR (2025-2034) | 14.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Deployment Mode (Cloud-Based, On-Premise), by Function (Inference, Training), by End User (Cloud Service Providers (CSPs), Enterprises, Government), Region |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | NVIDIA Corporation, Intel Corporation, Advanced Micro Devices, Inc., Micron Technology, Inc., IBM, Samsung SDS, Qualcomm Technologies, Inc., Google Cloud, Imagination Technologies, Huawei Cloud Computing Technologies Co., Ltd., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |