Quick Navigation

Report Overview

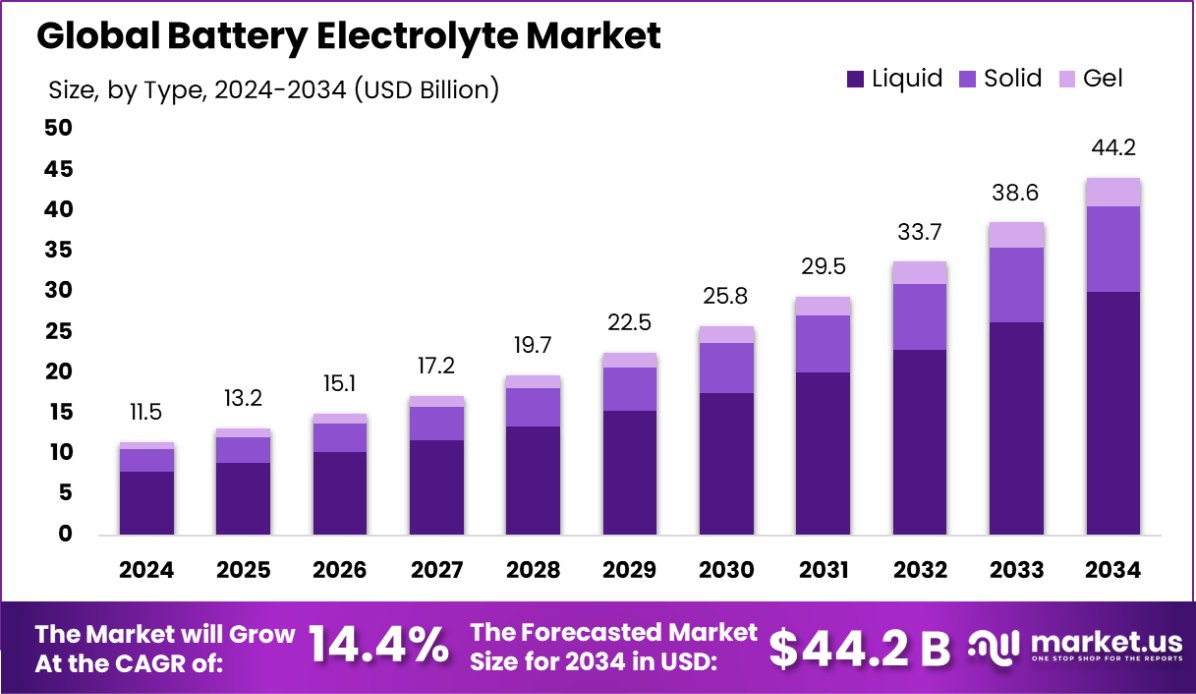

Global Battery Electrolyte Market is expected to be worth around USD 44.2 billion by 2034, up from USD 11.5 billion in 2024, and grow at a CAGR of 14.4% from 2025 to 2034. In the Battery Electrolyte Market, Asia-Pacific’s robust presence is marked by a 42.30% share, totaling USD 4.8 billion.

A battery electrolyte is a key component in batteries, functioning as a conductive medium that allows the flow of electrical charge between the cathode and anode. This medium can be a liquid, gel, or solid, and its composition varies based on the type of battery—such as lithium-ion, lead-acid, or nickel-metal hydride. The electrolyte’s role is critical because it facilitates the movement of ions, which is essential for the electrochemical reactions that power the battery.

The battery electrolyte market is a segment of the broader battery industry, focusing on the production and innovation of electrolytes used in various battery types. This market has seen significant growth due to the rising demand for high-performance batteries in consumer electronics, electric vehicles (EVs), and renewable energy systems.

One major growth factor in the battery electrolyte market is the increasing adoption of electric vehicles. As global efforts to reduce carbon emissions intensify, the demand for EVs continues to rise, driving the need for batteries with longer life spans and higher energy densities. This shift directly impacts the demand for innovative electrolytes that can support these requirements.

The surge in portable electronics also fuels demand within the battery electrolyte market. Devices like smartphones, laptops, and wearables require reliable and efficient batteries, which in turn depend on high-quality electrolytes. This demand is amplified by the ongoing trend toward smarter and more connected devices, which require robust power sources to function effectively.

Opportunities within the battery electrolyte market are plentiful, particularly in the area of research and development for safer and more efficient electrolyte solutions. The exploration of non-flammable electrolytes and those offering higher thermal stability can lead to safer battery systems, opening up new applications in various sectors, including consumer electronics and large-scale energy storage systems, which are essential for managing the intermittency of renewable energy sources.

Supporting this growth, the U.S. Department of Energy (DOE) plans to allocate approximately $725 million for new awards under the Battery Materials Processing and Battery Manufacturing Grant Program, part of a broader $6 billion allocation under the Bipartisan Infrastructure Law. Furthermore, in 2024, corporate funding for energy storage companies reached $19.9 billion across 116 deals, marking an increase from $19 billion across 120 deals in 2023.

Key Takeaways

- Global Battery Electrolyte Market is expected to be worth around USD 44.2 billion by 2034, up from USD 11.5 billion in 2024, and grow at a CAGR of 14.4% from 2025 to 2034.

- Liquid electrolytes dominate the market with a significant 68.30% share.

- Lead acid batteries hold a major share of 38.50% in types.

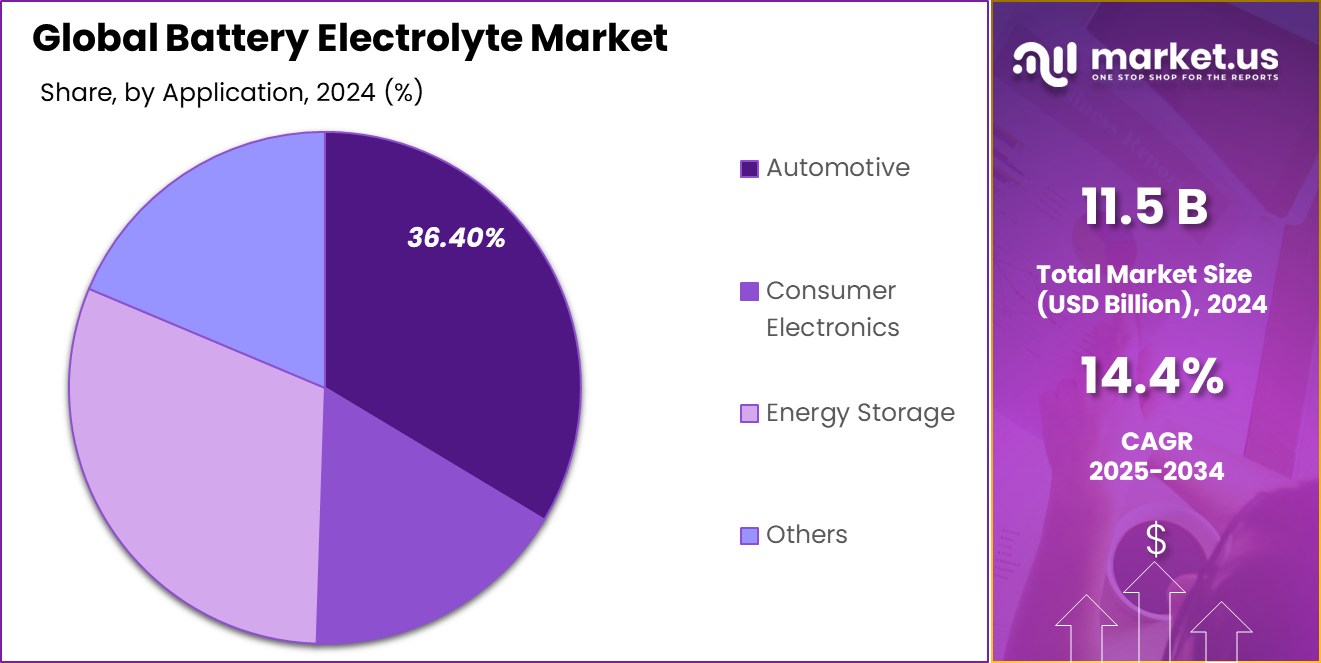

- The automotive sector leads in applications, constituting 36.40% of the market demand.

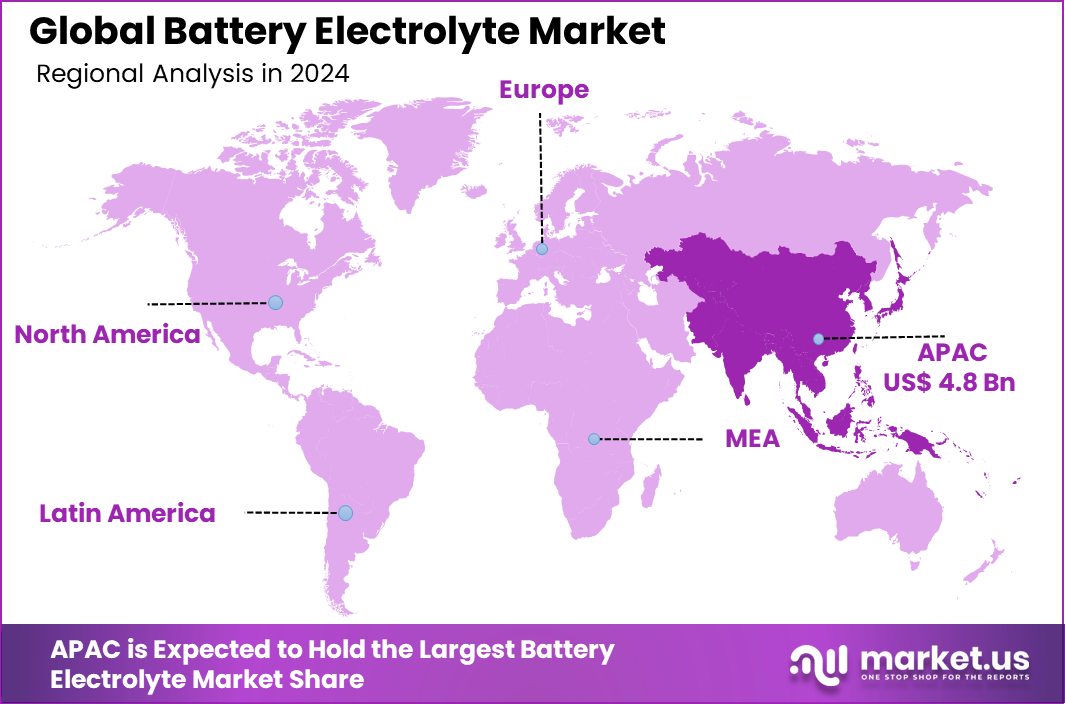

- Holding a 42.30% market share, Asia-Pacific leads in the Battery Electrolyte Market, valued impressively at USD 4.8 billion.

By Type Analysis

Liquid electrolytes dominate the market with a substantial share of 68.30% due to their high conductivity.

In 2024, Liquid held a dominant market position in the “By Type” segment of the Battery Electrolyte Market, with a 68.30% share. This substantial market share can be attributed to the widespread adoption of liquid electrolytes in various battery technologies, particularly in lithium-ion batteries, which are prevalent in consumer electronics and electric vehicles.

Liquid electrolytes are favored for their high ionic conductivity and ability to facilitate efficient electrochemical reactions, which are essential for high-performance batteries.

The preference for liquid electrolytes stems from their established application history and the ongoing innovations aimed at enhancing their electrochemical stability and safety features. As the market for electric vehicles and portable electronics continues to expand, the demand for reliable and efficient batteries is likely to sustain the growth of the liquid electrolyte segment.

Moreover, ongoing research into improving the thermal stability and reducing the flammability of liquid electrolytes could further solidify their position in the market, ensuring continued dominance in the coming years. This segment’s strong performance is indicative of its critical role in supporting the next generation of advanced battery technologies.

By Battery Type Analysis

Lead acid batteries, holding 38.50% of the market, are preferred for their reliability and cost-effectiveness.

In 2024, Lead Acid held a dominant market position in the “By Battery Type” segment of the Battery Electrolyte Market, with a 38.50% share. This prominence is largely due to the robust utilization of lead acid batteries in various applications ranging from automotive to backup power systems and energy storage. Lead acid batteries are highly valued for their cost-effectiveness, reliability, and well-established recycling processes, making them a preferred choice in both developing and developed markets.

The substantial share of lead acid batteries in the electrolyte market is underpinned by their widespread use in internal combustion engine vehicles, uninterruptible power supplies (UPS), and renewable energy systems, where they provide cost-efficient energy storage solutions. The durability and ability to deliver high surge currents make lead acid batteries particularly suitable for automotive starters and industrial power backups.

Despite the growing popularity of lithium-ion batteries in many modern applications, lead acid batteries maintain a strong market position due to their economic advantages and proven track record. Ongoing advancements aimed at increasing the efficiency and lifespan of lead acid batteries are expected to further sustain their significant market share in the battery electrolyte industry.

By Application Analysis

The automotive sector utilizes 36.40% of battery electrolytes, driven by increasing electric vehicle production globally.

In 2024, Automotive held a dominant market position in the “By Application” segment of the Battery Electrolyte Market, with a 36.40% share. This leadership is primarily driven by the accelerating shift toward electric vehicles (EVs) as part of global efforts to reduce carbon emissions and reliance on fossil fuels. The automotive sector’s demand for battery electrolytes is fueled by the need for batteries that not only have high energy densities but also exhibit enhanced safety and longer lifecycles.

The significant share held by the automotive application can be attributed to continuous advancements in battery technology, where manufacturers are increasingly focusing on optimizing electrolyte formulations to improve the overall performance and efficiency of EV batteries. This focus is crucial in meeting the stringent requirements of automotive applications, including quick charging capabilities and high-cycle durability under varying environmental conditions.

As governments worldwide implement stricter emissions regulations and consumers become more environmentally conscious, the demand for EVs is expected to grow, thereby propelling the need for innovative battery electrolytes that can deliver higher performance. The dominance of the automotive sector in the battery electrolyte market highlights its pivotal role in shaping the future of transportation and energy sustainability.

Key Market Segments

By Type

- Liquid

- Solid

- Gel

By Battery Type

- Lithium-ion

- Lead Acid

- Flow Battery

- Others

By Application

- Automotive

- Consumer Electronics

- Energy Storage

- Others

Driving Factors

Surging Demand for Electric Vehicles Drives Growth

One of the primary driving factors for the Battery Electrolyte Market is the surging demand for electric vehicles (EVs). As global awareness and governmental policies increasingly favor environmentally friendly transportation options to combat climate change, the demand for EVs has soared. This surge necessitates advancements in battery technology, particularly in battery electrolytes, which are crucial for improving battery performance, energy density, and charging speeds.

The growing EV market directly influences the demand for more efficient and durable battery electrolytes as manufacturers strive to meet consumer expectations for quicker charging times and longer battery life. This ongoing trend not only propels technological innovation in electrolyte solutions but also significantly boosts the overall growth of the battery electrolyte market.

Restraining Factors

Safety Concerns Limit Battery Electrolyte Market Expansion

A major restraining factor in the Battery Electrolyte Market is the safety concerns associated with battery systems, particularly those related to thermal stability and the risk of fire or explosions in devices like electric vehicles and portable electronics.

Electrolytes, being crucial components in the operation of these batteries, often contain flammable materials, which can pose significant risks under certain conditions, such as overheating or mechanical failure.

These safety challenges can hinder consumer confidence and slow down the adoption of new battery technologies. Consequently, the market’s growth is tempered as manufacturers and researchers invest significant resources into developing safer electrolyte formulations that reduce these risks, aiming to meet stringent safety standards without compromising battery performance.

Growth Opportunity

Research and Development Opens New Market Opportunities

The most significant growth opportunity within the Battery Electrolyte Market lies in the potential for ongoing research and development of new electrolyte chemistries and formulations.

As the demand for more efficient, safer, and higher-capacity batteries increases, particularly in sectors like electric vehicles and renewable energy storage, there is a substantial opportunity for innovation in electrolyte technologies.

Developing non-flammable, more stable electrolytes that can operate at higher temperatures and offer extended battery life could revolutionize the market. This pursuit not only promises to enhance the performance of existing battery types but also paves the way for the introduction of next-generation batteries, potentially capturing new market segments and expanding the overall market footprint significantly.

Latest Trends

Solid-State Electrolytes Trending in Battery Technology

A leading trend in the Battery Electrolyte Market is the shift towards solid-state electrolytes. This move is driven by the need for safer battery technologies with higher energy densities. Solid-state electrolytes are gaining popularity because they significantly reduce the risks of leaks and fires compared to their liquid counterparts.

These electrolytes enable the development of batteries that are not only safer but also can be charged faster and hold more energy, which is particularly beneficial for electric vehicles and mobile devices.

The adoption of solid-state technology is expected to accelerate as advancements continue to overcome current limitations related to cost and large-scale manufacturing capabilities. This trend underscores a pivotal shift in the market, focusing on enhancing safety and efficiency in battery production.

Regional Analysis

Asia-Pacific dominates the Battery Electrolyte Market with a significant 42.30% share, reaching a value of USD 4.8 billion.

The Battery Electrolyte Market is segmented across various regions, including North America, Europe, Asia Pacific, Middle East & Africa, and Latin America, each presenting unique growth dynamics and opportunities. Dominating the global landscape, Asia-Pacific holds a commanding 42.30% market share, valued at USD 4.8 billion.

This region’s dominance is driven by its robust manufacturing base and the rapid expansion of the automotive and electronics sectors, particularly in countries like China, Japan, and South Korea, which are pivotal in the production and deployment of advanced battery technologies.

Europe and North America also exhibit significant activity, focusing on the adoption of green technologies and the development of renewable energy storage solutions. These regions are actively investing in next-generation battery technologies, including solid-state electrolytes, to support their growing electric vehicle markets and renewable energy implementations.

Meanwhile, the Middle East & Africa, and Latin America are emerging as potential growth areas, spurred by increasing investments in energy infrastructure and the gradual adoption of electric vehicles. These regions are exploring ways to integrate advanced battery technologies to enhance their energy security and support sustainable development initiatives. Each region’s focus on enhancing its respective battery ecosystems presents a tapestry of opportunities for market expansion and technological advancements in the battery electrolyte sector.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In the global Battery Electrolyte Market of 2024, several key players, including American Elements, BASF SE, Capchem, Daikin America, Inc., GELEST, INC., and GS Yuasa International Ltd., are poised to play pivotal roles. Each company brings distinct strengths and strategies to the table, shaping the industry’s competitive landscape.

American Elements specializes in producing advanced chemical materials, and its involvement in the battery electrolyte market underscores its commitment to supporting high-tech battery solutions. The company’s focus on developing specialized electrolytes for niche applications makes it a crucial player in meeting specific industry demands.

BASF SE, a global leader in chemical solutions, leverages its extensive R&D capabilities to innovate in the battery materials space. Its investments in high-performance electrolyte solutions are designed to enhance the efficiency and safety of lithium-ion batteries, catering to the burgeoning demand in automotive and consumer electronics sectors.

Capchem is known for its expertise in chemicals for electronic applications, particularly within the battery sector. The company’s continuous innovation in electrolyte formulations is critical for advancing battery performance, particularly for high-energy-density applications, which are essential as the market shifts toward more sustainable energy solutions.

Daikin America, Inc., although primarily recognized for its work in air conditioning, has made significant strides in developing specialty polymers and chemicals for batteries. Its contribution to the battery electrolyte market focuses on enhancing the thermal stability and safety of electrolytes, which is vital for consumer safety and reliability.

GELEST, INC. focuses on silicon-based technology, which plays a crucial role in developing novel battery electrolyte materials that improve performance metrics such as conductivity and cycle life. Their work is integral to pushing the boundaries of what silicon-based electrolytes can achieve in next-generation batteries.

GS Yuasa International Ltd. is a powerhouse in battery technology, especially in automotive and industrial batteries. Their deep expertise in battery development is instrumental in driving forward innovations in electrolyte technology that optimize battery life and performance, particularly in harsh operational environments.

Top Key Players in the Market

- American Elements

- BASF SE

- Capchem

- Daikin America, Inc.

- GELEST, INC.

- GS Yuasa International Ltd.

- Guangzhou Tinci Materials Technology Co. Ltd

- Johnson Controls

- Mitsubishi Chemical Holdings Corporation

- NEI Corporation

- Ohara Corporation

- Shenzhen Capchem Technology Co. Ltd

- Stella Chemifa Corporation.

- Targray Industries Inc

- UBE Industries Ltd

Recent Developments

- In January 2025, SES AI Corporation secured contracts worth up to $10 million for utilizing AI in the discovery of battery materials aimed at commercial applications in science.

- In June 2024, Capchem attended the 22nd International Meeting on Lithium Batteries (IMLB 2024) and announced a lithium battery electrolyte project with a capacity of 40,000 tons/year. Additionally, Capchem signed a long-term order worth about 1.1 billion euros with German customers to supply lithium battery electrolytes from 2025 to 2034.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 11.5 Billion |

| Forecast Revenue (2034) | USD 44.2 Billion |

| CAGR (2025-2034) | 14.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Liquid, Solid, Gel), By Battery Type (Lithium-ion, Lead Acid, Flow Battery, Others), By Application (Automotive, Consumer Electronics, Energy Storage, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | American Elements, BASF SE, Capchem, Daikin America, Inc., GELEST, INC., GS Yuasa International Ltd., Guangzhou Tinci Materials Technology Co. Ltd, Johnson Controls, Mitsubishi Chemical Holdings Corporation, NEI Corporation, Ohara Corporation, Shenzhen Capchem Technology Co. Ltd, Stella Chemifa Corporation., Targray Industries Inc, UBE Industries Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |