Quick Navigation

Report Overview

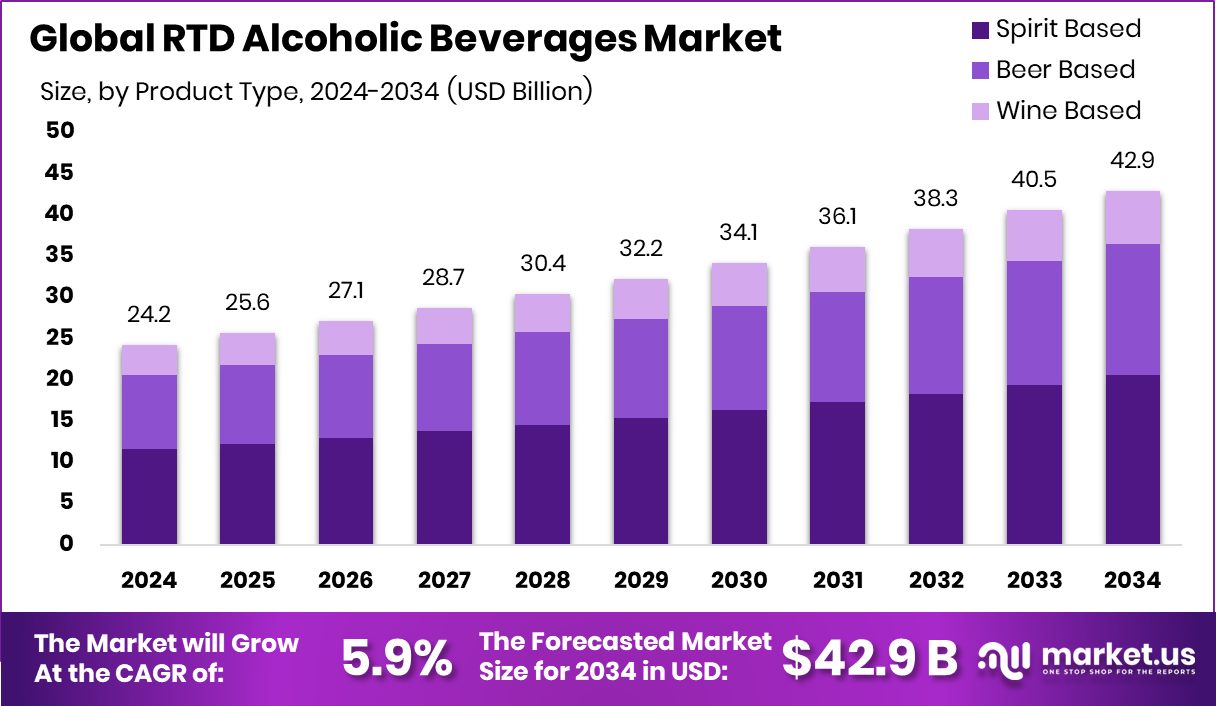

Global RTD Alcoholic Beverages Market is expected to be worth around USD 42.9 billion by 2034, up from USD 24.2 billion in 2024, and grow at a CAGR of 5.9% from 2025 to 2034. Consumer demand in Asia-Pacific continues to drive RTD sales, capturing a strong 37.3% market share.

The Ready-To-Drink (RTD) alcoholic beverages market is rapidly evolving as one of the most dynamic segments of the alcoholic drinks industry. It encompasses a broad range of pre-mixed beverages—from canned cocktails to hard seltzers—catering to consumers who seek convenience and variety. The key appeal lies in portability, shelf stability, and instant consumption without the need for mixing, which is particularly attractive to urban millennials and Gen Z.

Consumer demand for grab-and-go alcoholic options has surged. This demand has coincided with a lifestyle shift toward products that balance indulgence with health; many RTD offerings now feature lower alcohol content, reduced sugar, and natural ingredients. For context, wine typically contains 12% pure alcohol by volume, so an average person consuming 6 liters of pure alcohol per year equals about 67 standard 750 ml bottles of wine. This growing awareness of alcohol content and calorie intake is steering consumption toward lighter, more transparent RTD options.

On the policy front, government regulations are also shaping this space. The U.S. Craft Beverage Modernization and Tax Reform Act has enabled more small and mid-sized producers to enter the market by reducing excise taxes. In contrast, Oregon lawmakers are considering an 8% sales tax on beer and wine, which may impact affordability and retail sales dynamics in that state. Despite such regional headwinds, deregulation in many areas has allowed artisanal brands to flourish.

Sustainability is also becoming a critical growth vector. Australian sustainable packaging company Packamama recently secured a $100,000 government grant under the Business Research and Innovation Initiative (BRII). The funding, part of a $1.43 million allocation, supports wine packaging innovations aimed at reducing emissions and increasing shelf life. This aligns with global efforts to reduce the carbon footprint of beverage logistics.

In India, craft alcohol is gaining ground. Ronin Wines Private Limited, maker of Moonshine mead, raised $2 million in pre-Series A funding to scale operations both domestically and internationally. Such investments highlight growing investor confidence in niche RTD alcohol formats across emerging markets.

Key Takeaways

- Global RTD Alcoholic Beverages Market is expected to be worth around USD 42.9 billion by 2034, up from USD 24.2 billion in 2024, and grow at a CAGR of 5.9% from 2025 to 2034.

- Spirit-based RTD alcoholic beverages dominate the market, accounting for a 47.8% share due to strong demand.

- Bottled packaging holds a 64.2% market share, driven by portability, convenience, and premium presentation appeal.

- Flavored variants lead with a 72.1% share, fueled by consumer preference for taste innovation and variety.

- Young adults aged 18–25 years represent 36.4% of consumption, influenced by lifestyle, trends, and social culture.

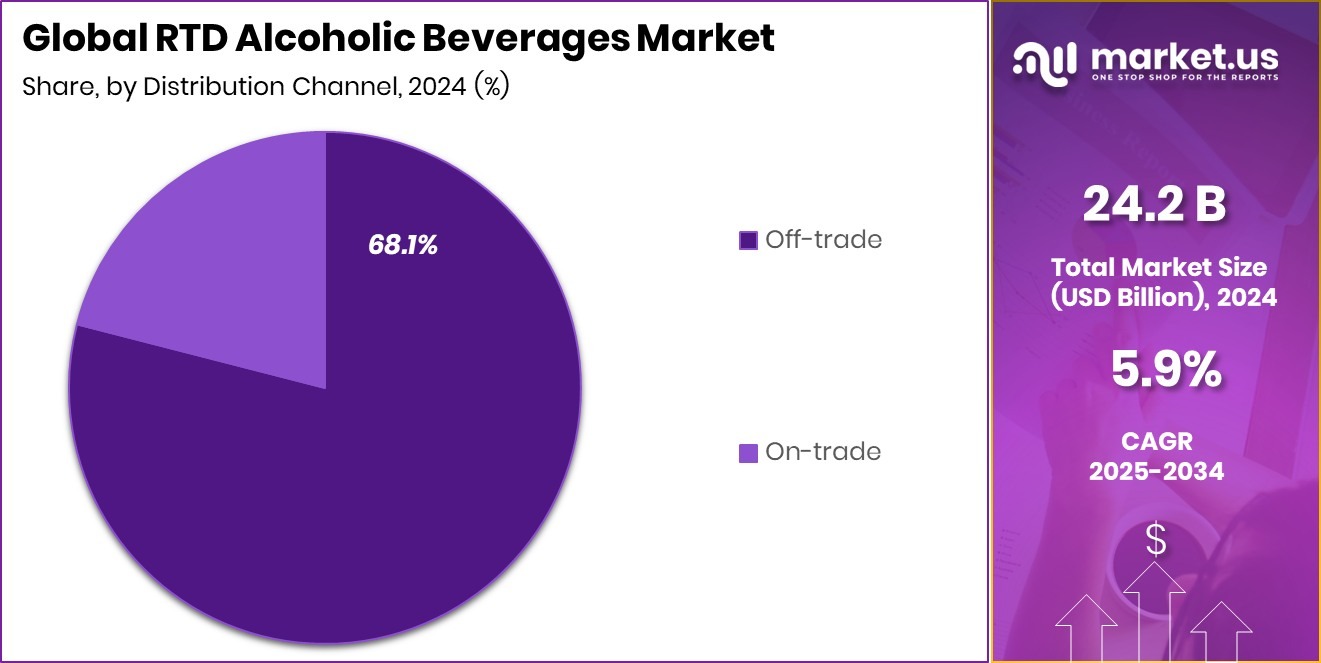

- Off-trade channels command a 68.1% share, reflecting strong retail presence, affordability, and ease of home consumption.

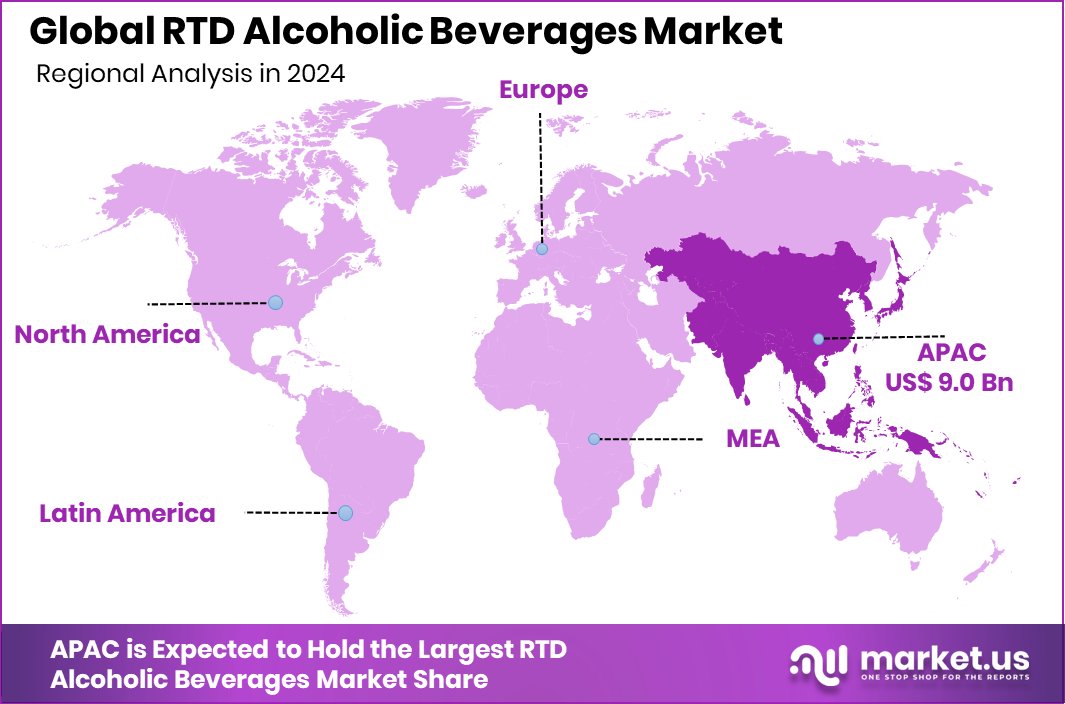

- Asia-Pacific RTD Alcoholic Beverages Market reached USD 9.0 Bn in total market value.

By Product Type Analysis

Spirit-based products dominate the market with a strong 47.8% share globally.

In 2024, Spirit Based held a dominant market position in the By Product Type segment of the RTD Alcoholic Beverages Market, capturing a notable 47.8% share. This dominance underscores a strong consumer preference for spirit-based ready-to-drink (RTD) offerings, such as vodka, gin, rum, and whiskey-based premixes.

The growing demand for premium and craft-style cocktails in convenient formats has significantly contributed to the popularity of this segment. Consumers, especially urban millennials and young adults, are increasingly gravitating toward beverages that offer the classic strength and flavor of spirits without the need for mixing or preparation.

The convenience of grab-and-go options has aligned well with changing social habits, particularly in on-the-move lifestyles and casual gatherings. Moreover, the strong presence of spirit-based RTDs in both on-trade and off-trade channels further consolidates its market advantage.

The variety of flavors and mixology-inspired innovations introduced by producers has also helped spirit-based beverages retain consumer attention. In comparison to other product types, spirit-based RTDs have benefited from higher perceived value and wider appeal across both male and female demographics.

By Packaging Analysis

Bottled RTD alcoholic beverages account for a leading 64.2% packaging market share.

In 2024, Bottle held a dominant market position in the By Packaging segment of the RTD Alcoholic Beverages Market, with a 64.2% share. This significant lead reflects a strong consumer inclination toward bottled RTD formats, which are often associated with premium appeal, better preservation, and aesthetic value.

Bottled packaging has remained the preferred choice for producers aiming to deliver a more refined and brand-centric experience, especially in spirit-based and craft RTD lines. The durability and recyclability of glass bottles also support sustainability goals, which further enhances their acceptance among environmentally conscious consumers.

Bottles continue to dominate off-trade sales channels, particularly in retail outlets and specialty stores, where shelf presentation and product visibility are crucial. Their suitability for premium branding and extended shelf-life makes bottles especially favorable for high-end RTD beverages.

Furthermore, bottles are often used for limited-edition or seasonal variants, adding exclusivity that appeals to collectors and enthusiasts. Despite the growing presence of alternative packaging formats like cans and pouches, bottles retained the majority share in 2024, driven by their association with quality and tradition.

By Type Analysis

Flavored variants dominate the RTD type segment with a massive 72.1% share.

In 2024, Flavored held a dominant market position in the By Type segment of the RTD Alcoholic Beverages Market, with a commanding 72.1% share. This overwhelming share highlights the strong consumer demand for variety and innovation in flavor profiles across ready-to-drink alcoholic options.

Flavored RTDs have gained popularity due to their wide appeal among younger demographics, especially those seeking lighter, fruit-infused, and more approachable alcoholic beverages. These products often feature combinations such as citrus, berries, tropical fruits, and herbal infusions, creating refreshing and unique experiences that differentiate them from traditional alcoholic offerings.

The dominance of flavored RTDs is also driven by their alignment with lifestyle trends, such as lower alcohol content, reduced bitterness, and higher drinkability, making them ideal for casual and social consumption. Their visual appeal, paired with innovative packaging and marketing, has contributed to strong off-trade sales, especially in convenience stores and supermarkets.

Flavored variants are often supported by seasonal launches and limited editions, encouraging trial and repeat purchases. With such a broad consumer base and adaptability across multiple product types, the flavored segment secured its position as the largest and most influential in the RTD alcoholic beverages market in 2024, catering to evolving palates and consumption habits globally.

By Age Group Analysis

Consumers aged 18–25 years contribute significantly, capturing 36.4% market share.

In 2024, 18–25 Years held a dominant market position in the By Age Group segment of the RTD Alcoholic Beverages Market, with a 36.4% share. This age group represents the most active and influential consumer base for RTD alcoholic products, driven by lifestyle preferences that favor convenience, flavor variety, and social drinking occasions.

The popularity of RTDs among younger consumers is rooted in their appeal as trendy, easy-to-consume alternatives to traditional spirits or beer. These beverages are often perceived as more approachable, especially for first-time alcohol consumers within this demographic.

Social media influence, branding, and packaging aesthetics also play a critical role in attracting 18–25-year-olds, who are highly responsive to visual marketing and shareable experiences. This generation also shows a strong interest in new flavor launches, limited-edition offerings, and health-conscious options like low-calorie or low-ABV beverages—all features commonly found in RTD portfolios.

By Distribution Channel Analysis

Off-trade sales channels dominate distribution, holding a commanding 68.1% global share.

In 2024, Off-trade held a dominant market position in the By Distribution Channel segment of the RTD Alcoholic Beverages Market, with a 68.1% share. This segment includes retail formats such as supermarkets, hypermarkets, convenience stores, and online platforms, which have become the primary access points for RTD consumers.

The off-trade channel gained prominence as consumers increasingly opted for at-home consumption, particularly due to changing social behaviors and a growing preference for stocking ready-to-drink options for casual occasions and gatherings.

The dominance of off-trade sales is also supported by the wide availability of product varieties, attractive pricing, and promotional offers that are more accessible in retail settings. Brands leverage this channel to launch new flavors and packaging formats, ensuring broader consumer reach.

Additionally, the growth of e-commerce and digital retailing has further strengthened off-trade dominance, especially among younger demographics accustomed to online shopping. Bulk buying and multi-pack formats are particularly popular in this segment, offering convenience and value.

Key Market Segments

By Product Type

- Spirit Based

- Vodka

- Tequila

- Rum

- Whisky

- Others

- Beer Based

- Wine Based

By Packaging

- Bottle

- Can

By Type

- Flavored

- Plain

By Age Group

- 18-25 Years

- 26-35 Years

- 36-45 Years

- Above 46 Years

By Distribution Channel

- Off-trade

- Supermarkets/Hypermarkets

- Specialty Stores

- Convenience Stores

- Online Stores

- Others

- On-trade

- Pubs, Bars, and Cafes

- Hotels and Restaurants

- Others

Driving Factors

Rising Demand for Convenience Boosts RTD Sales

One of the biggest driving forces behind the RTD alcoholic beverages market in 2024 is the growing consumer demand for convenience. People, especially young adults and working professionals, are looking for drinks that are easy to carry, require no mixing, and are ready to enjoy anytime. RTDs perfectly meet these needs. Whether it’s a picnic, house party, or weekend gathering, consumers prefer pre-mixed, flavorful drinks that save time.

The rise of on-the-go lifestyles and increased social drinking occasions further support this shift. Additionally, the single-serve packaging and variety of flavors make RTDs more appealing than traditional alcohol choices. As convenience remains a top priority, the RTD segment continues to grow quickly across global markets.

Restraining Factors

Strict Alcohol Regulations Limit RTD Market Growth

One major factor holding back the growth of the RTD alcoholic beverages market is the presence of strict alcohol regulations in many countries. Governments often impose age restrictions, high taxes, advertising limitations, and packaging rules on alcoholic drinks. These rules vary by region and can make it harder for brands to launch or expand RTD products.

In some places, RTDs are classified the same as hard liquor, leading to stricter sales and distribution laws. This not only affects pricing and availability but also limits how companies can promote their products. As a result, even with growing consumer demand, regulatory barriers can slow down market entry and expansion, especially for smaller or new brands entering global markets.

Growth Opportunity

Expanding Online Sales Channels Drive RTD Growth

A major growth opportunity in the RTD alcoholic beverages market lies in expanding online sales channels. With more people shopping from home, especially after the pandemic, e-commerce platforms have become a popular way to buy drinks. Younger consumers, in particular, prefer the ease of ordering their favorite RTD beverages online and having them delivered.

Many brands are now building their direct-to-consumer websites or partnering with online retailers and alcohol delivery apps. This digital shift not only increases reach but also allows brands to offer promotions, new product launches, and personalized experiences. As regulations around online alcohol sales continue to relax in some regions, this channel is expected to grow fast and unlock new consumer segments worldwide.

Latest Trends

Innovative Flavors and Premiumization Drive RTD Growth

In 2024, the Ready-to-Drink (RTD) alcoholic beverages market witnessed a significant trend towards innovative flavors and premiumization. Consumers increasingly sought unique taste experiences, leading brands to introduce novel flavor combinations and high-quality ingredients. This shift catered to a growing demand for sophisticated, bar-quality cocktails that could be conveniently enjoyed at home or on the go.

The emphasis on premium ingredients and craftsmanship elevated the RTD category, attracting a broader audience seeking both convenience and quality in their beverage choices. This trend not only diversified product offerings but also allowed brands to differentiate themselves in a competitive market, ultimately driving growth and expanding the consumer base for RTD alcoholic beverages.

Regional Analysis

In 2024, Asia-Pacific led the RTD market with 37.3% regional share dominance.

In 2024, Asia-Pacific emerged as the dominant region in the RTD Alcoholic Beverages Market, accounting for 37.3% of the global share with a market value of USD 9.0 billion. This dominance is driven by rising urbanization, changing social habits, and increasing acceptance of low-alcohol drinks among young consumers across countries like Japan, South Korea, China, and Australia.

The region’s strong growth is further supported by the popularity of fruit-flavored and spirit-based RTDs, especially among millennials and first-time drinkers seeking convenience and variety.

North America also held a significant share, supported by widespread availability of RTDs in retail channels and the popularity of canned cocktails among Gen Z and millennial consumers. Europe followed closely, benefiting from an established culture of social drinking and the rise of premium RTD offerings.

Meanwhile, the Middle East & Africa region is witnessing a slow yet steady increase in RTD adoption, particularly in urban centers where Western lifestyle trends are influencing consumption. Latin America, although a smaller market in comparison, is showing emerging demand with increasing product launches in Brazil and Mexico.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, three prominent players—Anheuser-Busch InBev NV, Asahi Group Holdings, Ltd., and Bacardi Limited—significantly influenced the global RTD alcoholic beverages market through strategic initiatives and product innovations.

Anheuser-Busch InBev NV (AB InBev) continued to expand its ‘Beyond Beer’ portfolio, emphasizing spirits-based RTDs and canned cocktails. The company’s Cutwater Spirits line, featuring offerings like Ranch Water and Rum Mojito, exemplified its commitment to diversifying beyond traditional beer products. This strategic focus aligned with evolving consumer preferences for convenient, flavorful, and ready-to-consume alcoholic beverages.

Asahi Group Holdings, Ltd. reported a 17.4% year-over-year increase in its Alcohol Beverages Business in 2024. The company emphasized investments in ‘Beer Adjacent Categories,’ particularly RTD alcoholic beverages, to enhance its business portfolio. This approach reflects Asahi’s strategy to cater to changing consumer tastes and expand its presence in the growing RTD segment.

In 2024, Pernod Ricard SA demonstrated a strategic focus on the Ready-to-Drink (RTD) alcoholic beverages market, aligning with evolving consumer preferences for convenience and innovation. The company’s RTD portfolio saw significant expansion, notably through the launch of the Absolut & Sprite canned cocktail in partnership with The Coca-Cola Company.

This collaboration combined Absolut Vodka with Sprite, catering to the growing demand for pre-mixed, easy-to-consume beverages. Additionally, Pernod Ricard introduced new RTD offerings under its Havana Club and Malibu brands, featuring flavors like Mango & Passion Fruit and Piña Colada, further diversifying its product range to appeal to a broader consumer base.

Top Key Players in the Market

- Anheuser-Busch InBev NV

- Asahi Group Holdings, Ltd.

- Bacardi Limited

- Carlsberg Breweries A/S

- Suntory Holdings Limited

- Brown-Forman

- Heineken N.V.

- Diageo plc

- Davide Campari-Milano S.p.A

- Molson Coors Brewing Company

- Mark Anthony Brands International Unlimited Co.

- Pernod Ricard SA

- Accolade Wines Australia Ltd.

- Constellation Brands Inc.

- The Boston Beer Co. Inc.

- Other Key Players

Recent Developments

- In September 2024, Bacardi Limited and The Coca-Cola Company announced a new collaboration to launch a ready-to-drink (RTD) cocktail: BACARDÍ Mixed with Coca-Cola. This pre-mixed drink combines Bacardi rum with Coca-Cola in a convenient can. The product is set to debut in select European markets and Mexico in 2025. The drink will have an alcohol by volume (ABV) of around 5%, though this may vary by region.

- In 2024, AB InBev partnered with PepsiCo to introduce “Svns Hard 7Up,” a 7% ABV alcoholic version of 7Up, in the Canadian market. This collaboration aims to cater to the growing demand for flavored RTD beverages.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 24.2 Billion |

| Forecast Revenue (2034) | USD 42.9 Billion |

| CAGR (2025-2034) | 5.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Spirit Based (Vodka, Tequila, Rum, Whisky, Others), Beer Based, Wine Based), By Packaging (Bottle, Can), By Type (Flavored, Plain), By Age Group (18-25 Years, 26-35 Years, 36-45 Years, Above 46 Years), By Distribution Channel (Off-trade (Supermarkets/Hypermarkets, Specialty Stores, Convenience Stores, Online Stores, Others), On-trade (Pubs, Bars and Cafe’s, Hotels and Restaurants, Others)) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Anheuser-Busch InBev NV, Asahi Group Holdings, Ltd., Bacardi Limited, Carlsberg Breweries A/S, Suntory Holdings Limited, Brown-Forman, Heineken N.V., Diageo plc, Davide Campari-Milano S.p.A, Molson Coors Brewing Company, Mark Anthony Brands International Unlimited Co., Pernod Ricard SA, Accolade Wines Australia Ltd., Constellation Brands Inc., The Boston Beer Co. Inc., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |