Quick Navigation

Report Overview

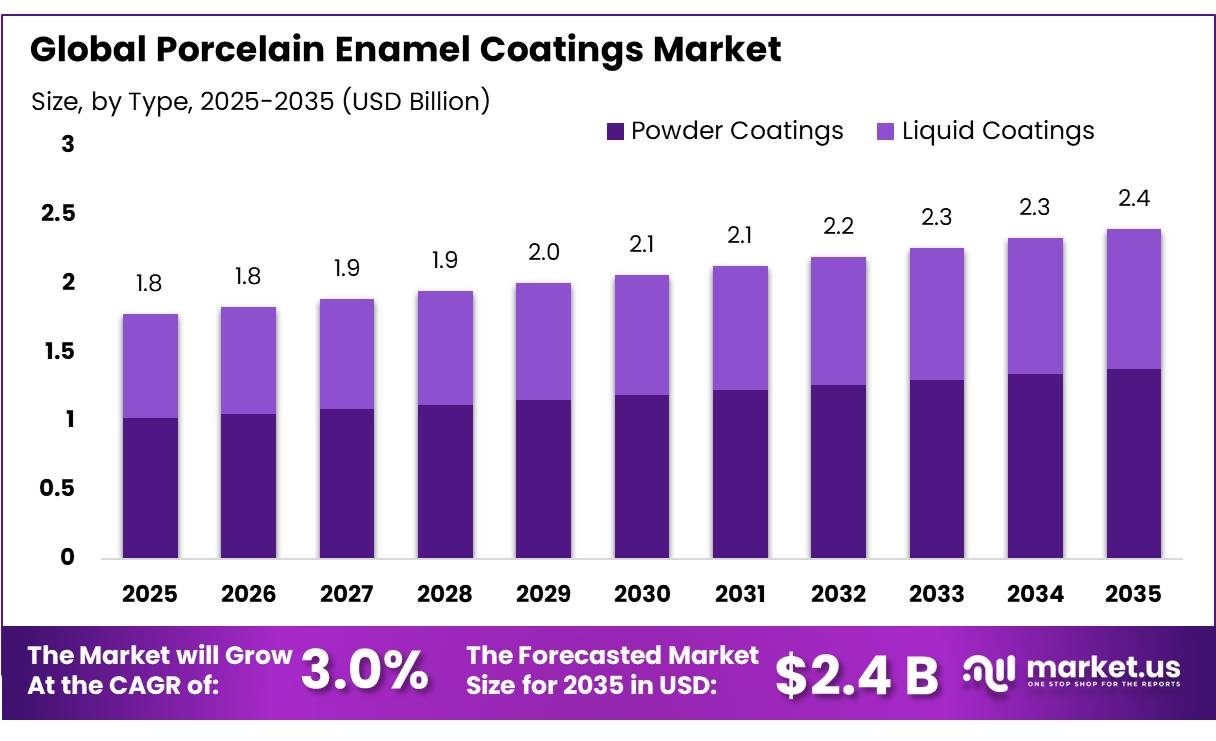

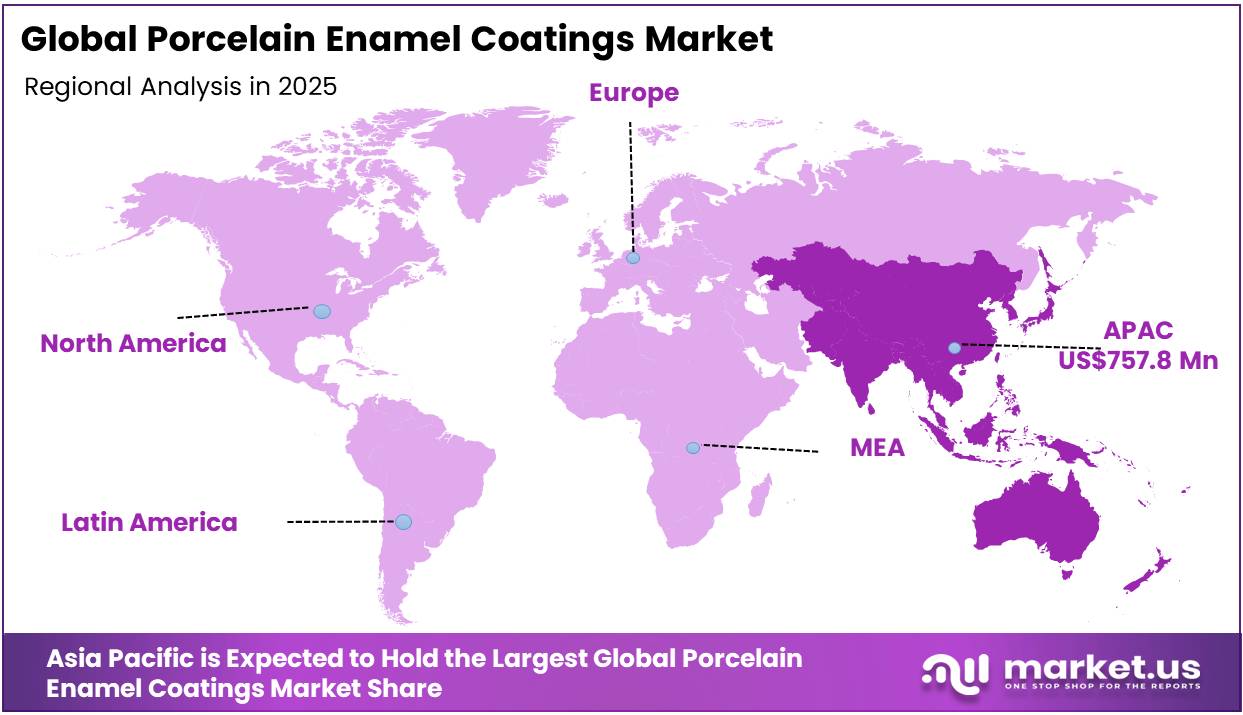

The Global Porcelain Enamel Coatings Market size is expected to be worth around USD 2.4 Billion by 2035, from USD 1.8 Billion in 2025, growing at a CAGR of 3.0% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 39.8% share, holding USD 4.9 Billion revenue.

The porcelain enamel coatings market comprises inorganic, glass-based coatings fused onto metal substrates at high temperatures to provide corrosion resistance, chemical durability, heat stability, and decorative finishes. These coatings are typically applied to steel, cast iron, aluminum, and stainless steel through wet or powder enameling processes followed by firing at temperatures generally ranging from 450°C to over 800°C.

Key Takeaways

- The global porcelain enamel coatings market was valued at US$1.8 billion in 2025.

- The global porcelain enamel coatings market is projected to grow at a CAGR of 3.0% and is estimated to reach US$2.4 billion by 2035.

- On the basis of type, powder coatings dominated the market, constituting 57.6% of the total market share.

- Based on the resin type, most porcelain enamel coatings are made from epoxy-based coatings, with a market share of 35.4%.

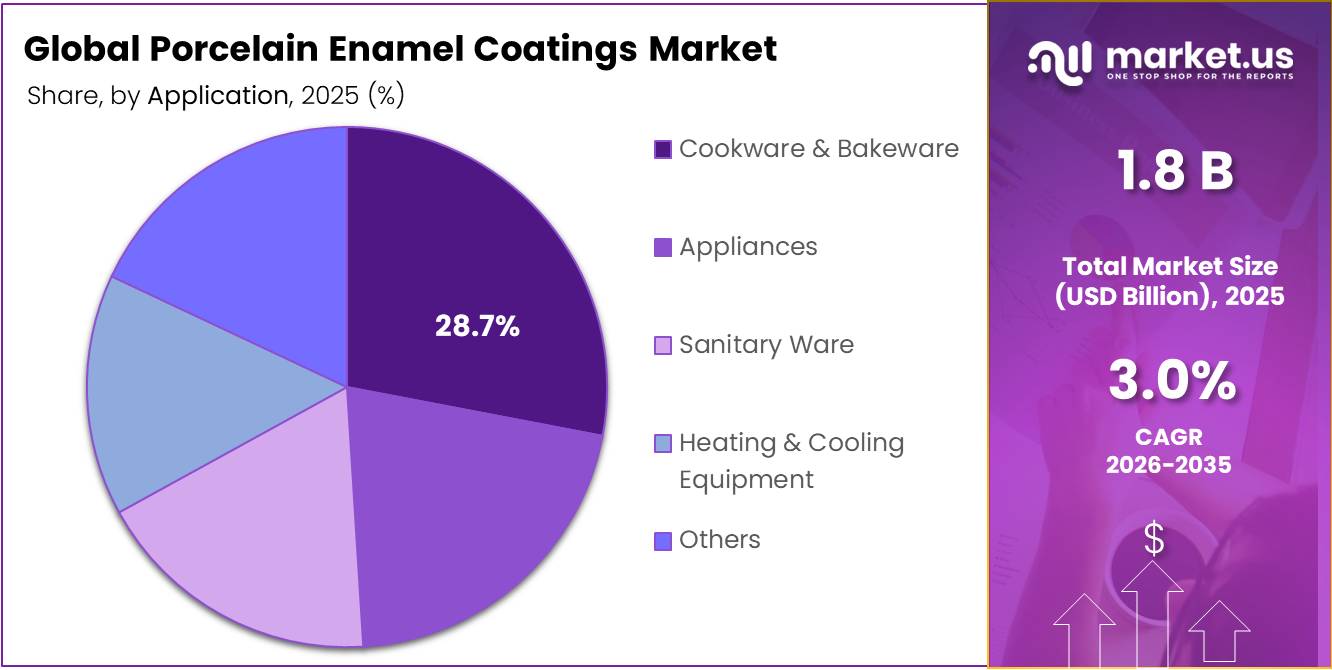

- Among the applications, cookware & bakeware held a major share in the porcelain enamel coatings market, 28.7% of the market share.

- On the basis of end-use industries, residential uses dominated the porcelain enamel coatings market, with 45.6% market share.

- In 2025, the Asia Pacific was the most dominant region in the porcelain enamel coatings market, accounting for 42.1% of the total global consumption.

Porcelain enamel coatings are widely used in cookware, sanitary ware, household appliances, water heaters, architectural panels, chemical-processing equipment, and transport infrastructure because of their scratch resistance, UV stability, non-porous surface properties, and long operational life. The market is increasingly influenced by demand for durable and low-maintenance surfaces in residential, commercial, and industrial applications.

Manufacturers are also integrating powder-based enameling systems, automated spraying technologies, and low-emission production methods to comply with environmental standards and improve process efficiency. In parallel, infrastructure modernization, sanitation expansion, and appliance manufacturing growth across the Asia-Pacific continue to support industrial adoption of porcelain enamel coatings.

Type Analysis

Powder Coatings Dominated the Porcelain Enamel Coatings Market.

Powder coatings are the dominant segment in the porcelain enamel coatings market, driven by their superior environmental performance, application efficiency, and durability. The powder coatings account for approximately 57.6% of the total market share, reflecting their strong adoption across appliances, cookware, sanitary ware, and industrial equipment applications.

Their dominance is primarily supported by low-VOC or solvent-free composition, which ensures compliance with tightening environmental regulations and reduces emissions during high-temperature firing processes. Powder coatings also achieve higher material utilization rates, typically 60-80% transfer efficiency, minimizing waste compared to liquid systems. In addition, they provide uniform film formation, improved corrosion resistance, and consistent finish quality, making them suitable for large-scale industrial enameling operations.

Resin Type Analysis

Epoxy-based Coatings Held Major Share of the Porcelain Enamel Coatings Market.

Epoxy-based coatings represent the leading resin type in the porcelain enamel coatings market, accounting for approximately 35.4% of the total share. Their dominance is primarily attributed to their strong adhesion properties, excellent chemical resistance, and high durability under corrosive and high-moisture environments. These characteristics make epoxy systems particularly suitable for applications such as sanitary ware, industrial equipment, pipelines, and chemical-processing components where long-term surface protection is essential.

Epoxy coatings demonstrate superior mechanical strength and resistance to abrasion, ensuring performance stability in demanding operational conditions. Their cross-linked polymer structure enhances barrier properties against water, acids, and alkalis, reducing substrate degradation over time. Additionally, epoxy systems are widely compatible with powder and hybrid enameling processes, enabling efficient integration into automated manufacturing lines.

Application Analysis

Cookware & Bakeware Led the Porcelain Enamel Coatings Market.

Cookware and bakeware represent the leading application segment in the porcelain enamel coatings market, accounting for approximately 28.7% of the total share. This dominance is driven by the widespread use of enamel-coated surfaces in pots, pans, trays, and baking dishes due to their superior non-stick properties, thermal stability, and food-safe inertness. Porcelain enamel coatings provide a non-porous, stain-resistant surface that prevents food interaction with the metal substrate, ensuring hygiene and long service life.

The segment benefits from strong household and commercial kitchen demand, where durability, ease of cleaning, and resistance to scratching and acidic food reactions are critical performance requirements. Enamel coatings also withstand repeated heating cycles at high temperatures without degradation or release of harmful substances. Additionally, aesthetic versatility through color and gloss finishes enhances product appeal in consumer cookware markets, supporting sustained adoption across both residential and foodservice applications.

End-Use Industry Analysis

Residential Uses Held the Largest Share of the Porcelain Enamel Coatings Market.

The residential segment represents the leading end-use category in the porcelain enamel coatings market, accounting for approximately 45.6% of the total share. This dominance is primarily driven by widespread application in household products such as cookware, bakeware, refrigerators, washing machines, water heaters, and sanitary fixtures. Porcelain enamel coatings are preferred in residential environments due to their high durability, stain resistance, hygienic surface properties, and ability to withstand repeated thermal and chemical exposure.

The segment benefits from growing demand for long-lasting, low-maintenance household appliances and sanitary ware, particularly in urban housing developments and modern kitchen installations. Enamel-coated surfaces offer aesthetic versatility, enabling color customization and glossy finishes that enhance consumer appeal. Additionally, increasing emphasis on hygiene, ease of cleaning, and product longevity in residential settings continues to reinforce adoption. These combined performance and functional advantages sustain the strong position of the residential segment in overall market demand.

Key Market Segments

By Type

- Powder Coatings

- Liquid Coatings

By Resin Type

- Epoxy-based Coatings

- Polyester-based Coatings

- Acrylic-based Coatings

- Others

By Application

- Cookware & Bakeware

- Appliances

- Sanitary Ware

- Heating & Cooling Equipment

- Others

By End-Use Industry

- Residential

- Commercial

- Industrial

Market Dynamics

Driver Analysis - Growing Demand for Durable Cookware Boosts Porcelain Enamel Coatings Market

The rising demand for durable cookware and household appliances is strongly reinforcing the adoption of porcelain enamel coatings, particularly across steel-based kitchenware and white goods manufacturing ecosystems. The material is widely applied in products such as enamel-coated cast iron pots, baking trays, oven interiors, washing machine drums, and refrigerator liners, where resistance to heat, acids, and repeated cleaning cycles is essential.

The enamel-coated cookware is preferred for its non-reactive surface and thermal stability up to several hundred degrees Celsius, making it suitable for prolonged cooking and baking applications in both residential and commercial kitchens. Appliance manufacturers integrate enamel coatings in ovens, dishwashers, and washing machines to improve corrosion resistance and surface durability under cyclic thermal and moisture exposure. For instance, enamel-coated components are engineered to withstand repeated wash cycles operating between approximately 20°C and 60°C, ensuring long-term surface integrity in domestic appliances.

Urban household expansion and rising appliance penetration rates have further strengthened consumption volumes, with residential appliances representing the dominant end-use category in enamel coating usage due to increased ownership of ovens, refrigerators, and washing machines. In manufacturing ecosystems, increasing production of cast iron and mild steel cookware, especially enamel-coated variants used for baking and slow cooking, continues to support steady coating consumption. Demand is further reinforced by appliance design strategies that emphasize durability, hygiene, and aesthetic finish quality, where enamel coatings provide a glass-like surface that resists staining and corrosion over extended usage cycles.

Restraint Analysis - High Energy Consumption and Production Limits Challenge Porcelain Enamel Coatings Market

Porcelain enamel coatings production remains constrained by the high energy intensity of firing and the technical rigidity of kiln operations. Industrial enameling furnaces typically operate between 500°C and 900°C, while porcelain and ceramic firing can exceed 1,200°C. The conventional porcelain production requires firing cycles of 26 hours at 1,000°C and 12 hours at 1,400°C, largely using natural gas. The firing, drying, and casting are the most energy-intensive ceramic production stages, requiring continuous reductions in gas and electricity consumption per ton of output.

Production constraints arise because kiln temperature uniformity directly affects coating adhesion, color, and defect rates. Industrial enameling operators note that minor firing deviations can cause coating failures and rework, increasing energy use further. Thermal processing can account for roughly 90% of total energy consumption in ceramic manufacturing, with firing alone consuming about half of total process energy. Decarbonization efforts further face infrastructure limits. For instance, Roca Group invested about EUR10 million to deploy a fully electric tunnel kiln operating at 1,220°C, highlighting the capital intensity and grid-capacity requirements of lower-emission production systems.

Opportunity Analysis - Sanitary Ware and Infrastructure Expansion Creates Market Opportunities

Expansion of sanitary ware production and public infrastructure modernization is strengthening long-term application demand for porcelain enamel coatings in hygienic, corrosion-resistant surfaces. India’s Ministry of Housing and Urban Affairs reported construction of more than 6.3 million individual household toilets and over 690,000 community and public toilet seats under the Swachh Bharat Mission-Urban by 2023, expanding installed sanitary infrastructure requiring durable coated fixtures. The Government of India further reported rural sanitation coverage rising from 38.7% in 2014 to near-universal coverage by 2019, supported by the construction of more than 100 million toilets.

Porcelain enamel coatings benefit from these projects as they provide high resistance to abrasion, moisture, detergents, and microbial contamination in high-usage environments such as hospitals, transit systems, schools, and residential sanitation facilities. In parallel, sanitary ware manufacturers continue capacity additions tied to urban housing and institutional construction. Electrification and modernization of rail and metro infrastructure also support demand for enamel-coated panels and fixtures because of their durability, fire resistance, and low maintenance characteristics in public transport environments.

Emerging Trend Analysis - Shift Toward Low-Emission Powder-Based Coating Technologies.

The porcelain enamel coatings industry is increasingly integrating low-emission powder-based and reduced-VOC coating technologies to comply with tightening environmental regulations and reduce solvent-related emissions. Powder coating systems release little or no volatile organic compounds (VOCs) because they are applied as dry particulates rather than solvent-based liquids. Industrial coating manufacturers have consequently expanded low-VOC enamel offerings.

For instance, Sherwin-Williams states that its Polane T Plus polyurethane enamel complies with U.S. EPA solvent-emission limits below 3.5 lb/gal VOC, while Rust-Oleum’s ROCAlkyd enamel is formulated to meet California SCAQMD thresholds below 100 g/L VOC for certain applications.

Process efficiency further supports the transition. Powder-based coating transfer efficiency is typically reported at 60-80%, reducing overspray losses and material waste relative to conventional spray systems. Manufacturers additionally emphasize lower odor, reduced hazardous air pollutants, and chromate- and lead-free formulations in industrial enamel products. The trend is particularly visible in appliance, architectural metal, and sanitary applications where environmental compliance and durability requirements increasingly converge.

Geopolitical Impact Analysis

Geopolitical Supply Chain Fragmentation and Energy Market Volatility in Porcelain Enamel Coatings.

Current geopolitical tensions are affecting the porcelain enamel coatings market primarily through energy-cost volatility, freight disruptions, and raw-material supply uncertainty. Porcelain enamel production is highly energy-intensive because firing and fusion processes require sustained kiln temperatures often exceeding 800°C. The industrial gas and electricity prices in Europe remained 2-4 times higher than those of major trading partners after the 2021-2023 energy crisis, constraining competitiveness for energy-intensive ceramic and enamel producers. The geopolitical instability and uncertainty around remaining Russian gas transit routes continued to influence European wholesale gas markets during 2024 despite relatively stable storage levels.

Shipping disruptions linked to the Red Sea conflict have further increased logistical pressures on industrial coatings and ceramic supply chains. The U.S. Energy Information Administration reported that crude and petroleum product flows around the Cape of Good Hope increased nearly 50% in the first five months of 2024 as vessels avoided the Red Sea route. Congressional Research Service and government trade agencies noted that rerouting around Africa increased transit times by up to two weeks and raised freight and insurance costs across Europe-Asia trade corridors. These disruptions affect enamel producers reliant on imported frits, specialty minerals, pigments, and fuel inputs, while also delaying delivery schedules for appliances, sanitary ware, and architectural components that incorporate porcelain enamel coatings.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Porcelain Enamel Coatings Market.

In 2025, the Asia Pacific dominated the global porcelain enamel coatings market, holding about 42.1% of the total global consumption. Asia Pacific represents the largest production and consumption base for porcelain enamel-coated sanitary ware and related ceramic applications due to its concentration of manufacturing capacity, urban infrastructure expansion, and integrated raw-material supply chains.

Demand fundamentals are reinforced by rapid urbanization and sanitation infrastructure expansion across China, India, Indonesia, Vietnam, and ASEAN economies. Asia Pacific further benefits from vertically integrated ceramic manufacturing clusters and extensive mineral availability documented by the U.S. Geological Survey, supporting localized production of enamel frits, ceramic substrates, and coated sanitary fixtures.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of porcelain enamel coatings primarily focus on product innovation, process efficiency, sustainability compliance, and application diversification to strengthen competitiveness. Companies are investing in low-VOC and powder-based enamel technologies to comply with tightening environmental regulations and reduce hazardous emissions during coating operations. Producers also emphasize energy-efficient firing systems, electric kiln integration, and heat-recovery technologies to lower fuel consumption in high-temperature enameling processes.

Another strategic priority is the development of specialized coatings with enhanced corrosion resistance, abrasion durability, antimicrobial performance, and color stability for appliances, sanitary ware, architectural panels, and industrial equipment. Manufacturers increasingly collaborate with appliance and construction-material producers to create customized enamel formulations compatible with automated production lines and advanced substrates.

The Major Players in The Industry

- Vibrantz Technologies

- Colorobbia Group

- Akcoat (Akkök Group)

- Pemco International

- Nolifrit (Hunan Noli Enamel)

- Ferro Corporation

- Enamels Inc.

- Hae Kwang

- Sinopigment & Enamel Chemicals

- Keskin Kimya

- GWIPPO

- The Sherwin-Williams Company

- TIGER Drylac

- Capron Manufacturing

- Venus Home Appliances Pvt Ltd

- Other Key Players

Key Developments

- In January 2026, Lintech International partnered with Vibrantz Technologies to distribute its glass and porcelain enamels along with specialty pigment technologies across the United States, strengthening access to advanced specialty materials and performance solutions for industrial customers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$1.8 Bn |

| Forecast Revenue (2035) | US$2.4 Bn |

| CAGR (2026-2035) | 3.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Powder Coatings and Liquid Coatings), By Resin Type (Epoxy-based Coatings, Polyester-based Coatings, Acrylic-based Coatings, and Others), By Application (Cookware & Bakeware, Appliances, Sanitary Ware, Heating & Cooling Equipment, and Others), By End-Use Industry (Residential, Commercial, and Industrial) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Vibrantz Technologies, Colorobbia Group, Akcoat (Akkök Group), Pemco International, Nolifrit (Hunan Noli Enamel), Ferro Corporation, Enamels Inc., Hae Kwang, Sinopigment & Enamel Chemicals, Keskin Kimya, GWIPPO, The Sherwin-Williams Company, TIGER Drylac, Capron Manufacturing, Venus Home Appliances Pvt Ltd, and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |