Quick Navigation

Report Overview

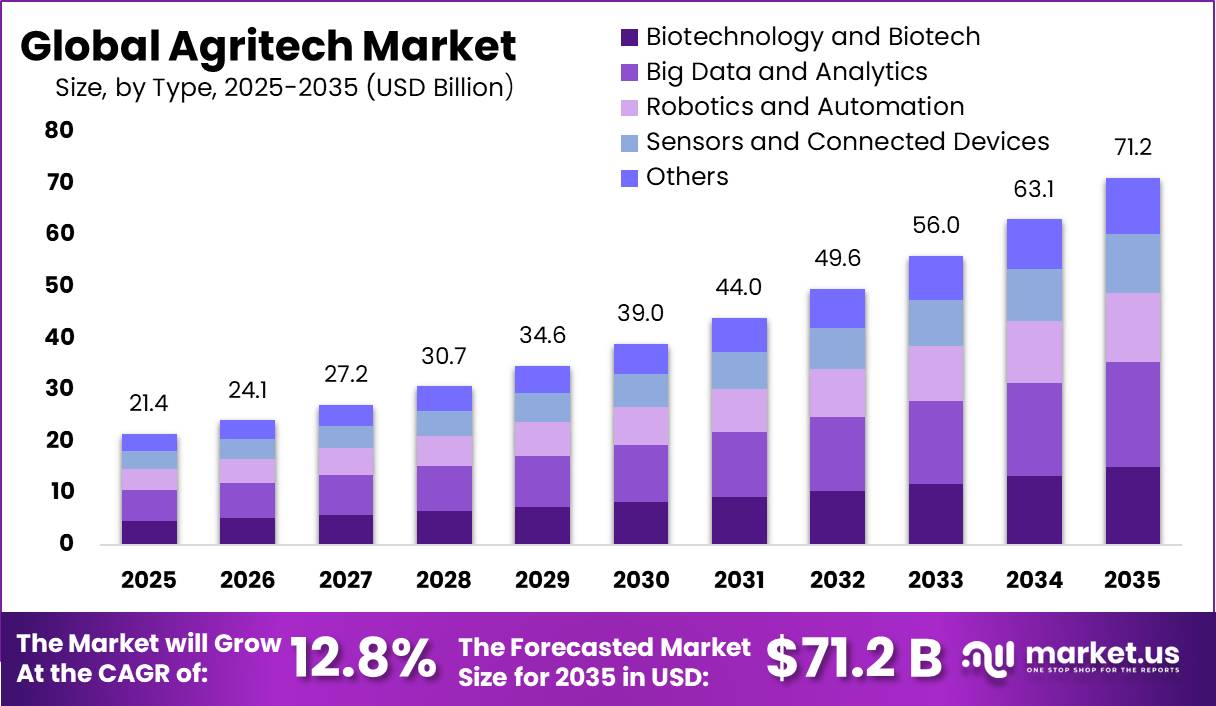

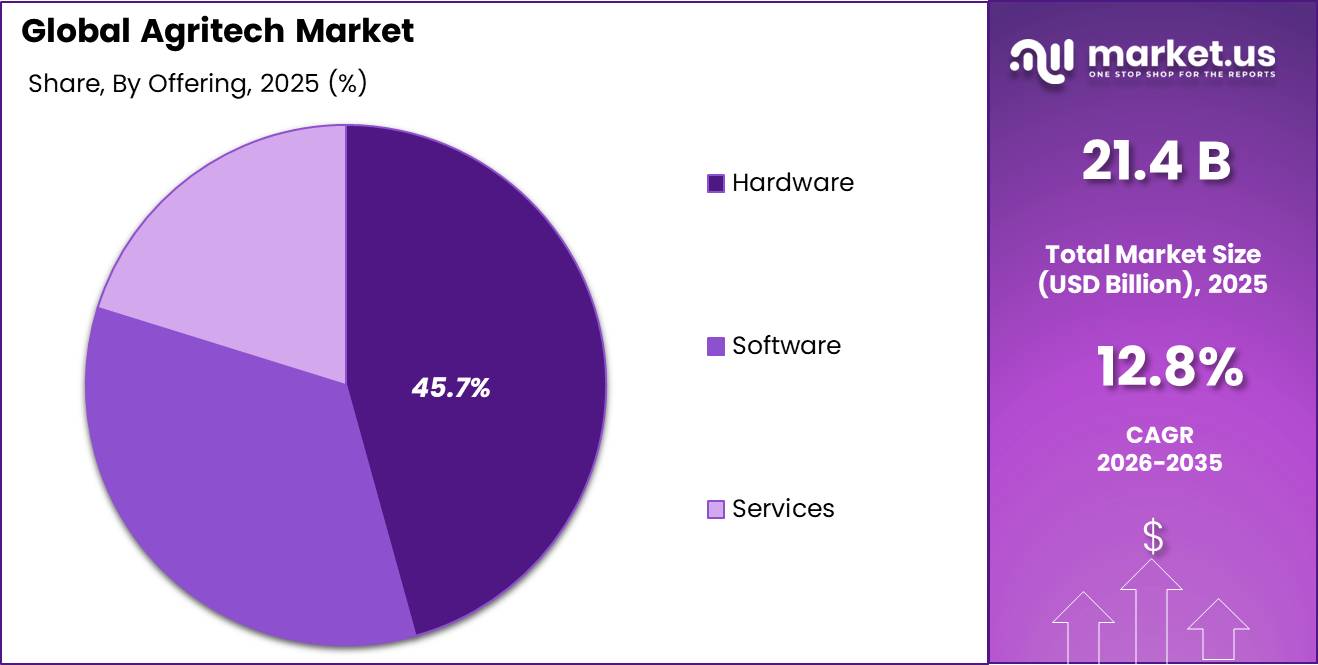

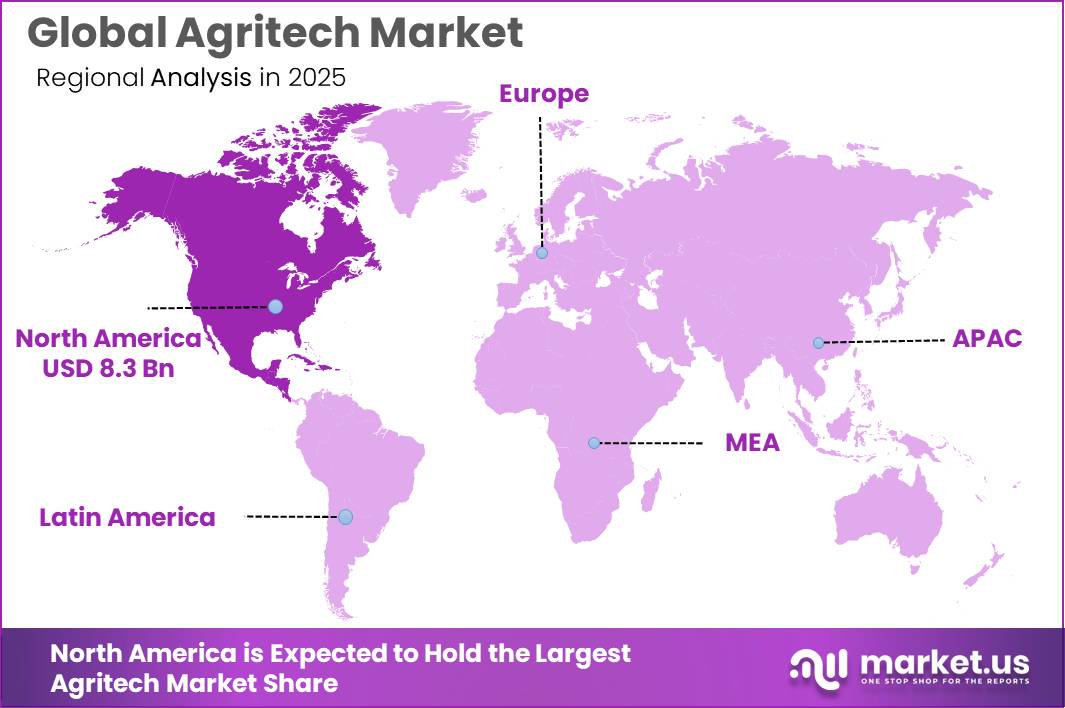

The Global Agritech Market size is expected to be worth around USD 71.2 Billion by 2035, from USD 21.4 Billion in 2025, growing at a CAGR of 12.8% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 39.2% share, holding USD 8.3 Billion revenue.

Agritech is entering a productivity-led growth phase as farms face higher food demand, climate risk, labour shortages and pressure to reduce input waste. Globally, the World Bank notes that food demand must rise to serve a projected 9.7 billion people by 2050, while agrifood systems already generate about one-third of global emissions. FAO reported agrifood-system emissions of 16.5 Gt CO₂e in 2023, equal to 32% of total emissions, creating demand for precision irrigation, robotics, digital monitoring and low-emission farm machinery.

Key Takeaways

- Agritech Market size is expected to be worth around USD 71.2 Billion by 2035, from USD 21.4 Billion in 2025, growing at a CAGR of 12.8%.

- Big Data and Analytics held a dominant market position, capturing more than a 28.6% share in the agritech market.

- Hardware held a dominant market position, capturing more than a 45.7% share in the agritech market.

- Broad Acre Applications held a dominant market position, capturing more than a 29.9% share in the agritech market.

- North America held a dominant position in the global agritech market, accounting for 39.2% of the total market share and reaching a valuation of nearly USD 8.3 Billion.

The industrial scenario is increasingly technology-led, with precision farming, robotics, AI, sensors, autonomous tractors, variable-rate spraying, and farm-data platforms moving from pilots to commercial use. Water efficiency is a core driver because agriculture uses about 70% of global freshwater withdrawals, and food production may need to rise by around 50% by 2050, creating strong demand for digital irrigation, yield optimization, and automated field operations.

FAO-linked SOFI 2025 estimates that 638–720 million people, or 7.8%–8.8% of the global population, faced hunger in 2024, supporting demand for technologies that improve production reliability, reduce crop losses and optimize inputs. The EU, where agricultural policy is being reshaped around resilience, competitiveness and sustainability, while future CAP support may cap larger area-based payments at €100,000 per farmer.

Government initiatives are also strengthening adoption. USDA’s Agriculture Innovation Agenda targets a 40% increase in agricultural production by 2050 while cutting the environmental footprint of U.S. agriculture by 50%. The World Bank has also stated that it plans to double agricultural and agribusiness commitments to USD 9 billion annually by 2030, supporting climate-smart agriculture, digitalization and private-capital mobilization.

USDA’s Partnerships for Climate-Smart Commodities program listed US$3.1 billion across 141 selected projects, supporting soil health, emissions reduction and climate-smart production systems. The World Bank has also scaled climate-smart agriculture financing to nearly US$3 billion annually, supporting technologies that improve resilience and resource efficiency.

Deere & Company remains a major industrial participant in precision and autonomous agriculture. In January 2025, Deere announced six companies for its 2025 Startup Collaborator program, aimed at exploring technologies for agriculture and construction customers. At CES 2025, Deere introduced new autonomous machines using connectivity, AI, renewable fuels and electrification, including autonomous tractors and an electric commercial mower.

By Type Analysis

Big Data and Analytics dominates with 28.6% share due to growing use of data-driven farming decisions and smart agricultural planning.

In 2025, Big Data and Analytics held a dominant market position, capturing more than a 28.6% share in the agritech market by type. The strong growth of this segment is mainly linked to the rising need for accurate farm data, weather tracking, crop monitoring, and yield forecasting across modern agriculture practices. Farmers and agribusiness companies are increasingly using analytics platforms to understand soil conditions, irrigation needs, and pest risks in real time. The availability of connected devices, farm sensors, drones, and satellite imagery has also increased the volume of agricultural data, creating higher demand for advanced analytics tools.

By Offering Analysis

Hardware dominates with 45.7% share due to rising adoption of smart farming equipment and connected agricultural devices.

In 2025, Hardware held a dominant market position, capturing more than a 45.7% share in the agritech market by offering. The segment gained strong momentum as farmers increasingly invested in physical technologies such as sensors, drones, GPS-enabled machinery, automated irrigation systems, and climate monitoring devices. These tools became essential for improving farm productivity, reducing manual labor, and supporting precision agriculture practices. The demand for reliable field equipment also increased as growers looked for better ways to monitor crops, livestock, and soil conditions in real time.

By Application Analysis

Broad Acre Applications dominate with 29.9% share due to increasing use of precision farming technologies across large agricultural lands.

In 2025, Broad Acre Applications held a dominant market position, capturing more than a 29.9% share in the agritech market by application. The segment experienced strong demand as large-scale crop producers increasingly adopted smart farming technologies to improve productivity and manage vast agricultural areas more efficiently. Farmers operating broad acre farms focused heavily on technologies such as GPS-guided tractors, variable rate technology, soil monitoring systems, and drone-based crop analysis to increase operational accuracy and reduce input waste.

Key Market Segments

By Type

- Biotechnology and Biotech

- Big Data and Analytics

- Robotics and Automation

- Sensors and Connected Devices

- Others

By Offering

- Hardware

- Software

- Services

By Application

- Broad Acre Applications

- Field Mapping

- Seeding and Planting

- Fertilizing and Irrigation

- Intercultural Operations

- Picking and Harvesting

- Livestock Farm Management

- Milking

- Shepherding and Herding

- Others

- Indoor Farming

- Agrochemicals

- Aerial Data Collection

- Weather Tracking and Forecasting

- Supply Chain Management

- Inventory Management

- Others

Emerging Trends

Artificial Intelligence and Precision Farming are Becoming the Biggest Trends in Agritech

One of the latest trends shaping the agritech market is the rapid use of artificial intelligence (AI) and precision farming technologies across modern agriculture. Farmers are increasingly using AI-powered tools, drones, IoT sensors, and satellite imaging systems to improve crop monitoring and make better farming decisions. According to the Food and Agriculture Organization (FAO), digital technologies and AI are creating major opportunities for precision farming, climate-smart agriculture, and supply chain optimization.

The use of precision agriculture is helping farmers improve productivity while reducing waste. Recent agricultural studies published in 2025 showed that precision farming technologies can improve crop yields by 20% to 30% while reducing input waste such as fertilizers and pesticides by nearly 40% to 60%. Governments and agricultural organizations are also promoting AI-driven farming to support food security and sustainable agriculture goals. Many farmers are now relying on real-time field data and predictive analytics to manage irrigation, weather risks, and crop diseases more effectively.

Smart Irrigation and Agricultural Automation are Expanding Across Global Farms

Another major trend in the agritech market is the growing adoption of smart irrigation systems and agricultural automation technologies. Farmers worldwide are facing rising pressure to reduce water usage while maintaining stable food production levels. According to the FAO, agriculture accounts for nearly 70% of global freshwater withdrawals, increasing the demand for efficient irrigation technologies. Smart irrigation systems equipped with sensors and automated controls are helping farmers monitor soil moisture levels and reduce unnecessary water consumption.

Automation is also becoming more common due to labor shortages and rising operational costs in agriculture. Technologies such as robotic harvesters, autonomous tractors, and AI-enabled spraying systems are helping improve farming efficiency and reduce manual labor dependency. Research published in 2025 highlighted that agricultural automation technologies can reduce farming labor costs by nearly 25%, while smart irrigation systems can improve water-use efficiency by 40% to 60%.

Drivers

Rising Global Food Demand is Pushing Farmers Toward Smart Agriculture

Precision agriculture tools help farmers monitor soil conditions, weather patterns, and fertilizer usage more accurately. The use of automated equipment and connected sensors is helping reduce operational costs while improving farm productivity. Agritech solutions are also becoming important for reducing food losses caused by climate change, water shortages, and pest outbreaks. As food consumption continues to rise globally, the demand for technology-supported farming is expected to grow steadily across both developed and developing agricultural economies.

- According to the Food and Agriculture Organization (FAO), global food production will need to increase by nearly 70% by 2050 to feed a population expected to reach around 9.1 billion people. One of the biggest driving factors for the agritech market is the growing global demand for food. Farmers today are under pressure to produce more crops using limited land, water, and labor resources. According to the Food and Agriculture Organization (FAO), global food production will need to increase by nearly 70% by 2050 to feed a population expected to reach around 9.1 billion people.

Government Support and Precision Farming Adoption are Accelerating Agritech Growth

Government support programs and the increasing adoption of precision agriculture technologies are also driving the agritech market forward. Many governments are investing in digital farming initiatives to improve agricultural efficiency and strengthen food security. According to the U.S. Government Accountability Office (GAO), the USDA and the National Science Foundation provided nearly USD 200 million for precision agriculture research and development between 2017 and 2021. These investments are helping farmers gain access to smart farming tools, automation systems, and advanced crop management technologies.

Precision farming adoption continues to rise among large agricultural operations. USDA data shows that 68% of large crop farms in the United States use technologies such as yield maps, soil maps, and precision guidance systems. Farmers are increasingly using these technologies to improve planting accuracy, optimize fertilizer application, and manage water consumption more efficiently.

Restraints

High Initial Investment Costs are Limiting Agritech Adoption Among Small Farmers

One of the major restraining factors for the agritech market is the high cost of implementing advanced farming technologies. Many small and medium-sized farmers struggle to afford equipment such as drones, smart irrigation systems, GPS-enabled tractors, farm management software, and automated sensors. According to the Food and Agriculture Organization (FAO), around 80% of the world’s food is produced by smallholder farmers, yet many of them have limited financial access to modern agricultural technologies.

The cost challenge becomes even greater when technology adoption also requires internet connectivity, software subscriptions, maintenance services, and technical training. Many rural farming communities still lack proper digital infrastructure, which slows the adoption of smart agriculture solutions. Even though governments are introducing subsidy programs and rural modernization initiatives, adoption remains uneven across different regions.

Limited Digital Skills and Rural Connectivity Continue to Slow Market Expansion

Another important challenge for the agritech industry is the lack of digital literacy and weak internet access in rural farming areas. Many farmers still rely on traditional farming methods and may not have the technical knowledge needed to operate data-driven agricultural systems.

- According to the International Telecommunication Union (ITU), nearly 2.6 billion people around the world remained offline in 2023, with rural populations facing the largest connectivity gaps. This directly affects the adoption of cloud-based farm platforms, remote monitoring systems, and AI-powered agricultural tools.

In several developing countries, unstable internet networks and limited access to digital devices make it difficult for farmers to fully benefit from smart agriculture technologies. Even when governments launch digital agriculture programs, the lack of training and technical support often reduces long-term usage. Many older farmers also prefer conventional farming practices because they are more familiar and easier to manage. This digital divide creates a gap between large commercial farms and smaller rural farms in terms of technology adoption.

Opportunity

Expansion of Precision Farming is Creating Strong Growth Opportunities for Agritech Companies

One of the biggest growth opportunities in the agritech market is the rapid expansion of precision farming across global agricultural regions. Farmers are increasingly adopting technologies that help improve crop productivity while reducing water, fertilizer, and pesticide usage. According to the United States Department of Agriculture (USDA), more than 70% of U.S. corn-planted acreage and nearly 60% of soybean-planted acreage already use precision agriculture technologies such as yield monitoring and GPS mapping systems.

Precision farming is becoming highly important as climate change, labor shortages, and rising food demand continue to affect agricultural productivity. Technologies such as AI-based crop monitoring, automated irrigation systems, and drone-assisted field analysis are helping farmers make faster and more accurate decisions. Governments in several countries are also supporting digital agriculture programs through subsidies and smart farming initiatives.

Growing Demand for Sustainable Agriculture is Opening New Areas for Agritech Innovation

The global push toward sustainable agriculture is another major growth opportunity for the agritech market. Farmers and governments are under increasing pressure to reduce environmental impact while maintaining food production levels. According to the Food and Agriculture Organization (FAO), agriculture accounts for nearly 70% of global freshwater withdrawals. This has increased the demand for technologies that improve irrigation efficiency, monitor soil health, and reduce resource wastage during farming operations.

Agritech companies are responding by developing smart irrigation systems, climate monitoring platforms, and precision nutrient management tools that help farmers use resources more efficiently. Sustainable farming technologies are also gaining attention because they support lower carbon emissions and better land management practices. Governments across Europe, North America, and Asia are introducing sustainability-focused agricultural policies and funding programs to encourage technology adoption in farming communities.

Regional Insights

North America dominates the Agritech market with 39.2% share, reaching nearly USD 8.3 Billion due to strong precision farming adoption and advanced agricultural infrastructure.

North America held a dominant position in the global agritech market, accounting for 39.2% of the total market share and reaching a valuation of nearly USD 8.3 Billion. The region’s leadership is mainly supported by the widespread adoption of precision agriculture technologies, strong digital infrastructure, and the presence of large commercial farming operations across the United States and Canada.

The United States remains the largest contributor to regional growth due to strong investments in smart farming and agricultural automation. According to the United States Department of Agriculture (USDA), precision agriculture technologies are widely adopted across major crop farms, especially in corn and soybean production areas. Large-scale agricultural businesses are continuously investing in data-driven farming solutions to improve yield efficiency and resource management.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Harvest Automation, Inc. focuses on agricultural robotics and automation systems designed for greenhouse and nursery operations. The company is recognized for developing mobile robots that automate plant spacing, transport, and material handling tasks. Its robotic systems help reduce labor dependency and improve operational efficiency for growers. The company’s automation technologies can lower manual labor requirements by more than 30% in some nursery applications.

AGCO Corporation is a major global agritech and agricultural equipment manufacturer known for brands such as Fendt, Massey Ferguson, and Valtra. In 2025, AGCO reported approximately USD 10.1 billion in annual revenue and employed nearly 22,000 workers globally. The company invests strongly in precision farming, autonomous machinery, smart planting technologies, and sustainable agricultural solutions. AGCO spent approximately USD 487.7 million on research and development activities in 2025, highlighting its focus on digital farming innovation and productivity improvement for modern agriculture operations.

International Business Machines Corporation (IBM) plays an important role in agritech through artificial intelligence, cloud computing, IoT, and weather analytics solutions. IBM’s agriculture-focused technologies help farmers improve crop forecasting, irrigation planning, and supply chain efficiency using real-time data analysis. In 2025, IBM generated annual revenue exceeding USD 62 billion globally. The company’s AI platforms support precision agriculture initiatives by enabling predictive farming models and climate-risk assessments.

Top Key Players Outlook

- Deere & Company

- Harvest Automation, Inc.

- AGCO Corporation

- Naïo Technologies SAS

- AgEagle Aerial Systems Inc.

- International Business Machines Corporation

- Corteva Agriscience

- Datacor, Inc

- Trimble Inc.

- CropX Technologies Ltd.

- Alltech Inc.

- Kubota Corporation

- Valmont Industries, Inc.

- Syngenta Group

Recent Industry Developments

In 2025, AgEagle Aerial Systems strengthened its agritech role through drone-based crop monitoring, mapping, soil analysis, water management, pest detection, and yield estimation. The company entered a strategic alliance with Vyom Drones to manufacture and sell eBee X drones in India, targeting over 345 million acres of arable land and a projected USD 631 million agriculture drone opportunity by 2030. It also advanced product development with eBee VISION software version 2.1.0, adding 2D/3D mapping, GNSS-denied operation, and NATO-standard video support.

In 2025, Corteva Agriscience strengthened its agritech work through seed technology, crop protection, biologicals, and digital farming solutions. The company reported USD 17.4 billion in full-year net sales, with Seed net sales of USD 9.9 billion and Crop Protection net sales of USD 7.5 billion. Its Crop Protection volume grew 5%, supported by demand for new products, herbicides, and biologicals. In partnership activity, Corteva formed a multi-million-dollar joint venture with Hexagon Bio in 2025 to develop nature-inspired crop protection products using AI, microbial genetics, and synthetic biology.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 21.4 Bn |

| Forecast Revenue (2035) | USD 71.2 Bn |

| CAGR (2026-2035) | 12.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Biotechnology and Biotech, Big Data and Analytics, Robotics and Automation, Sensors and Connected Devices, Others), By Offering (Hardware, Software, Services), By Application (Broad Acre Applications, Livestock Farm Management, Indoor Farming, Agrochemicals, Aerial Data Collection, Weather Tracking and Forecasting, Supply Chain Management, Inventory Management, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Deere & Company, Harvest Automation, Inc., AGCO Corporation, Naïo Technologies SAS, AgEagle Aerial Systems Inc., International Business Machines Corporation, Corteva Agriscience, Datacor, Inc, Trimble Inc., CropX Technologies Ltd., Alltech Inc., Kubota Corporation, Valmont Industries, Inc., Syngenta Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |