Quick Navigation

Report Overview

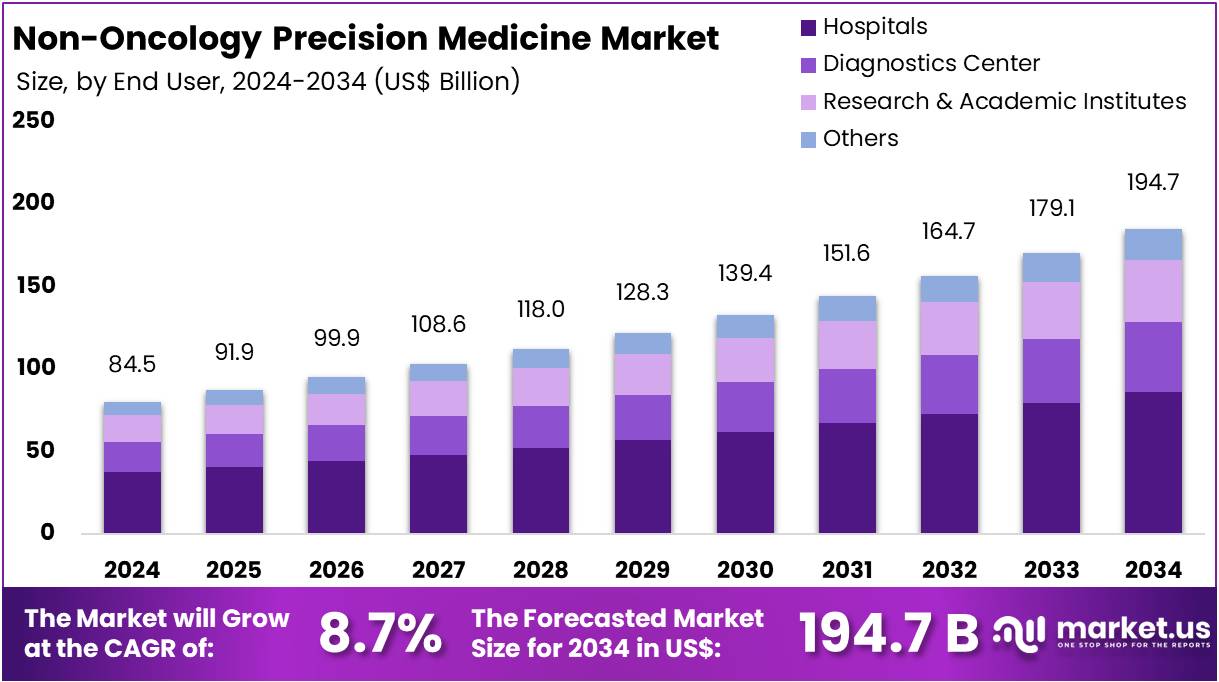

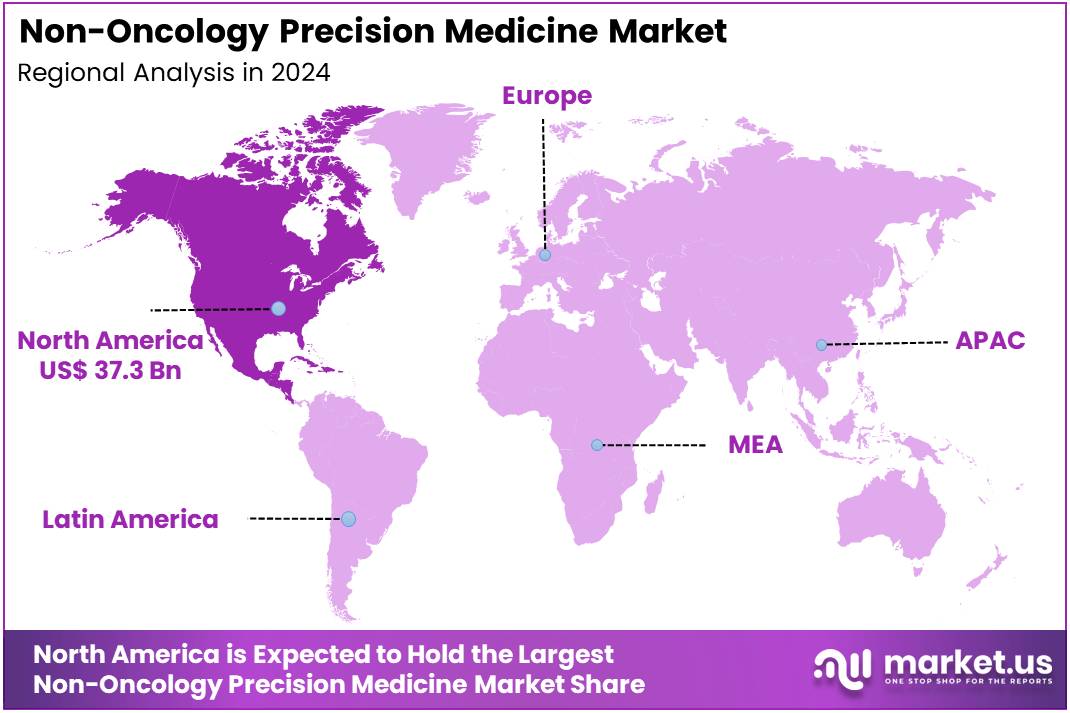

The Global Non-Oncology Precision Medicine Market size is expected to be worth around US$ 194.7 Billion by 2034, from US$ 84.5 Billion in 2024, growing at a CAGR of 8.7% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 44.2% share and holds US$ 37.3 Billion market value for the year.

The non-oncology precision medicine market is witnessing notable growth, primarily driven by advancements in genomic technologies, rising chronic disease prevalence, and digital health integration. According to the World Health Organization (WHO), genomic sequencing is becoming more accessible and affordable. This has improved the identification of genetic variations linked to diseases, enabling personalized therapies. These targeted treatments improve efficacy and minimize side effects, thereby contributing to the transformation of disease management in non-cancer healthcare.

The increasing burden of chronic diseases such as cardiovascular disorders, diabetes, and neurodegenerative conditions is also shaping the precision medicine market. For instance, polygenic risk scores (PRS) have shown potential in identifying high-risk individuals. A study on coronary artery disease (CAD) revealed that those in the highest PRS quintile had a 2.5-fold higher risk than those in the lowest quintile. Similarly, PRS has been used to detect type 2 diabetes risk, although its predictive power remains moderate when compared to traditional risk factors.

Preventive health strategies are being enhanced by large-scale genetic screening programs. A notable example includes a study of over 175,000 participants, where 3.4% were found to carry pathogenic variants linked to disease risk. Integration of PRS with conventional risk factors has shown modest improvements in risk prediction for CAD and type 2 diabetes. This integration supports early intervention strategies and strengthens the foundation for personalized preventive care.

Government initiatives are further accelerating growth in this sector. For example, the U.S.-based Nutrition for Precision Health (NPH) project, funded with $170 million, aims to develop personalized diet algorithms based on genetics and lifestyle. In parallel, the National Institutes of Health (NIH) is conducting the All of Us Research Program, collecting health data from one million individuals to enhance treatment personalization. The UK Biobank also contributes significantly by offering genetic data from 500,000 participants for disease prevention research.

Precision medicine applications are expanding in neurological and psychiatric disorders as well. For example, pharmacogenomic testing is being used to personalize treatment for Alzheimer’s disease, schizophrenia, and depression. A meta-analysis of 3,462 patients showed that pharmacogenomic-guided antidepressant use led to better response and remission rates. Additionally, in Parkinson’s disease, genetic mutations like LRRK2 and SNCA are being studied to optimize dopaminergic therapy, helping reduce side effects.

Autoimmune diseases also benefit from this evolving field. Rheumatoid arthritis (RA), affecting 1% of the global adult population, shows a strong genetic link, especially with the HLA-DRB1 gene. Systemic lupus erythematosus (SLE) affects nearly 5 million people globally, with a significant female predominance. These diseases are now being managed with immune-modulating therapies designed to match genetic susceptibility, improving outcomes and reducing complications.

The non-oncology precision medicine market is advancing rapidly due to a convergence of technology, public health initiatives, and increasing clinical demand. These efforts collectively support a healthcare model that is proactive, individualized, and more effective across multiple non-cancer disease categories.

Key Takeaways

- The global non-oncology precision medicine market is projected to grow from US$ 84.5 billion in 2024 to around US$ 194.7 billion by 2034.

- This market is forecasted to expand at a compound annual growth rate (CAGR) of 8.7% between 2025 and 2034, driven by personalized therapies.

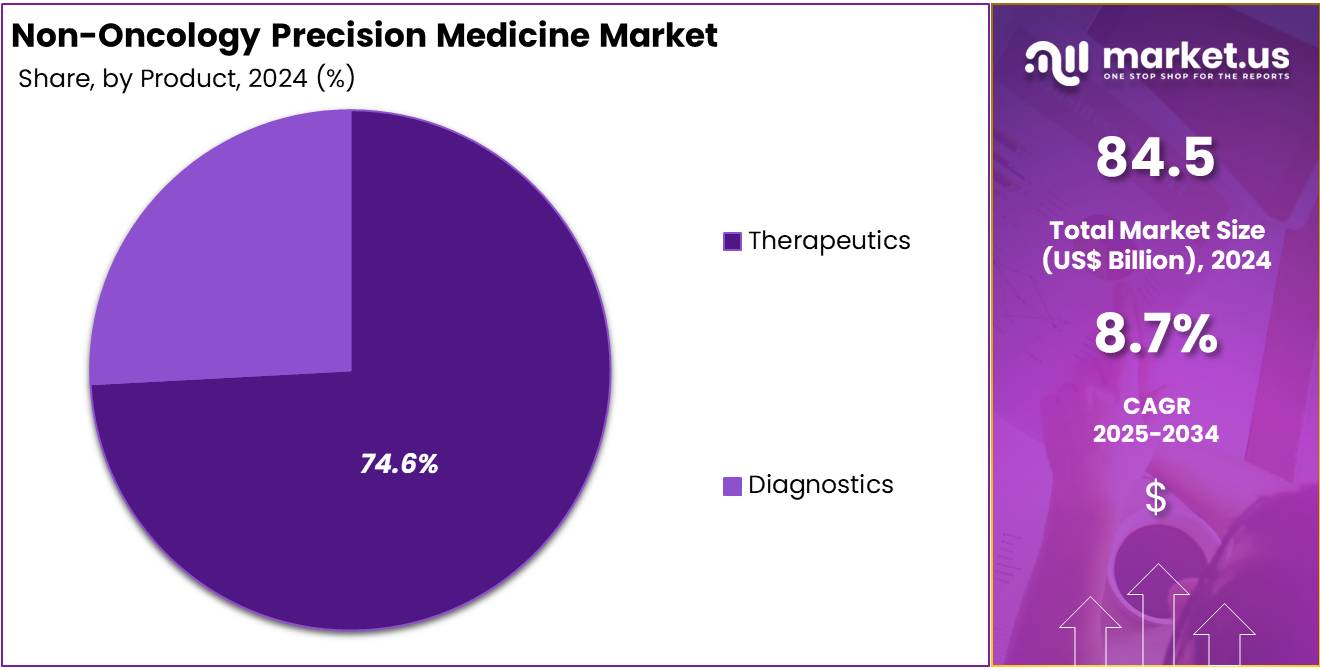

- In 2024, therapeutic products led the product segment, accounting for over 74.6% of the global non-oncology precision medicine market share.

- The central nervous system (CNS) applications segment dominated in 2024, capturing more than 31.2% of the total application-based market share.

- Hospitals were the leading end users in 2024, holding over 31.2% of the total share in the non-oncology precision medicine market.

- North America held the largest regional share in 2024, securing over 44.2% of the market and reaching US$ 37.3 billion in value.

Product Analysis

In 2024, the Therapeutics section held a dominant market position in the Product Segment of the Non-Oncology Precision Medicine Market, and captured more than a 74.6% share. This lead was driven by rising demand for customized treatments across chronic disease areas. Conditions like cardiovascular, autoimmune, and neurological disorders have benefited from tailored therapeutic options. These precision-based drugs are designed to work with a patient’s specific genetic profile. As a result, treatment outcomes have improved and side effects have reduced.

Industry experts point to strong support from health agencies and regulatory bodies as a key driver. The FDA, for example, has approved several precision drugs outside of oncology. These approvals have boosted confidence in non-oncology applications. The use of genomics and pharmacogenomics has also played a major role in the growth. Healthcare professionals now prefer personalized therapies that offer better clinical outcomes and patient satisfaction. Investment in drug development is expected to remain strong.

The Diagnostics segment, while holding a smaller share, is still essential. It supports therapy decisions by identifying key biomarkers. Tools such as genetic testing, companion diagnostics, and molecular diagnostics are widely used. Advances in sequencing technology have made diagnostics more accessible and cost-effective. These tools are critical for guiding treatment plans based on patient data. The segment is expected to grow steadily as awareness and adoption increase in both hospital and outpatient settings.

Application Analysis

In 2024, the CNS section held a dominant market position in the application segment of the Non-Oncology Precision Medicine Market and captured more than a 31.2% share. This leadership was due to the rising burden of neurological diseases such as Alzheimer’s, Parkinson’s, and multiple sclerosis. Experts noted that precision therapies using biomarkers and imaging tools offered better results. Targeted drugs helped reduce adverse effects and improved patient outcomes, making CNS a leading area in personalized treatment solutions.

Following CNS, infectious diseases emerged as a strong application area. Growing public health concerns and frequent disease outbreaks increased the demand for precise diagnostic and treatment tools. Health experts observed that genomic sequencing was being used to identify pathogens and tailor treatments. This helped reduce drug resistance. The immunology segment also gained attention. Autoimmune conditions such as lupus and rheumatoid arthritis were managed with genetic profiling. Personalized biologics showed better control and higher treatment success.

Other notable segments included respiratory and neurology. Respiratory diseases such as asthma and COPD were treated more effectively using precision-based inhalers and therapies. Clinicians applied biomarker testing to create tailored treatment plans. The neurology segment addressed conditions like epilepsy and migraines using targeted drug delivery. Genetic analysis helped customize doses and reduce side effects. Additionally, smaller application areas like cardiology and rare metabolic diseases were beginning to grow. Improved access to testing and rising research activity supported this expansion.

End User Analysis

In 2024, the hospitals section held a dominant market position in the end user segment of the non-oncology precision medicine market and captured more than a 31.2% share. This dominance was mainly due to hospitals having better access to advanced diagnostics and trained professionals. Hospitals also lead in implementing precision medicine tools for personalized treatment. Their ability to integrate genomics into routine care has enhanced clinical outcomes. As a result, hospitals remain the primary setting for precision medicine delivery.

Diagnostic centers held the second-largest share in this segment. These centers are increasingly involved in offering genetic testing and molecular diagnostics. The growing demand for early disease detection and risk assessment has expanded their role. Diagnostic centers also support hospitals and clinics by providing accurate and timely results. This helps healthcare providers make better treatment decisions. As awareness of personalized healthcare increases, diagnostic centers are expected to see continued demand across multiple conditions.

Research and academic institutes also played a crucial role in advancing non-oncology precision medicine. They are engaged in biomarker identification and clinical trial development. These institutions often collaborate with public health agencies and biopharma companies. Their focus on innovation helps in validating new therapies and improving patient care. In addition, other settings like specialty clinics and home care providers are slowly adopting precision medicine tools. These sectors are expected to grow as digital health solutions become more common.

Key Market Segments

By Product

- Diagnostics

- Therapeutics

By Application

- Oncology

- CNS

- Immunology

- Respiratory

- Infectious Diseases

- Neurology

- Other

By End User

- Hospitals

- Diagnostics Center

- Research & Academic Institutes

- Others

Drivers

Expansion of Companion Diagnostics in Non-Oncology Fields

The growth of companion diagnostics beyond oncology is driving advancements in non-oncology precision medicine. These diagnostics are now being used in autoimmune diseases, cardiovascular disorders, and rare genetic conditions. Their role is to help determine which patients will respond best to a specific therapy. This ensures a more targeted treatment approach. As a result, healthcare providers can reduce trial-and-error prescriptions. This shift supports better clinical outcomes and optimizes treatment strategies based on individual patient profiles.

The increasing use of companion diagnostics is enabling the shift from generalized medicine to personalized care. By identifying biomarkers linked to treatment responses, these tools help in selecting therapies that offer the highest benefit for specific patient subgroups. This not only improves efficacy but also minimizes adverse drug reactions. The adoption of such diagnostics is particularly useful in chronic disease management, where long-term therapies require precise targeting. This diagnostic-led personalization enhances patient safety and supports treatment compliance.

Furthermore, the demand for precision in therapeutic decisions is accelerating innovation in diagnostic platforms. Pharmaceutical companies are increasingly collaborating with diagnostic developers to integrate biomarker testing into clinical pathways. This integration enhances the value proposition of new drugs by ensuring they reach the right patient groups. In non-oncology fields like cardiology and immunology, this approach is becoming a cornerstone of clinical decision-making. It also supports cost-effective healthcare by avoiding unnecessary treatments and maximizing therapeutic benefits for patients.

Restraints

Absence of Standardized Clinical Guidelines in Non-Oncology Precision Medicine

One of the major restraints hindering the growth of non-oncology precision medicine is the lack of standardized clinical guidelines. Unlike oncology, where precision approaches are well-established, non-oncology fields such as cardiovascular, neurological, and autoimmune disorders face inconsistent protocols. This absence creates uncertainty for healthcare providers. As a result, many physicians hesitate to adopt precision-based strategies. The variability in clinical practice also raises concerns about patient safety and outcome predictability, which are essential for the widespread acceptance of such approaches.

This inconsistency affects more than just clinical decision-making. Reimbursement policies by payers and insurers are often tied to the availability of evidence-based clinical guidelines. In the absence of standard frameworks, precision therapies in non-oncology areas face limited insurance coverage. This directly impacts patient access and increases out-of-pocket costs. Hospitals and health systems may also be reluctant to invest in precision infrastructure without clear policy support, further slowing integration into routine care practices.

Moreover, the lack of standardization impedes clinical research and data aggregation efforts. Without unified treatment protocols, it becomes challenging to collect comparable data across institutions. This limitation reduces the ability to validate precision therapies effectively in large-scale studies. It also makes it difficult to design multi-center trials, which are critical for regulatory approvals. Thus, the absence of universally accepted clinical guidelines continues to act as a significant barrier to the broader adoption and scalability of non-oncology precision medicine.

Opportunities

Government Support Driving Non-Oncology Precision Medicine Expansion

Public sector involvement is playing a critical role in accelerating non-oncology precision medicine. Government-backed initiatives, such as the U.S. Precision Medicine Initiative, are increasingly targeting chronic diseases beyond cancer. These efforts aim to enhance individualized care by developing large-scale patient databases. The focus is on collecting genetic, lifestyle, and environmental data to inform treatment pathways. This foundational support ensures long-term growth and infrastructure for personalized therapies across areas like metabolic disorders and cardiovascular health.

The European Union’s Horizon Europe program complements this global push. It allocates substantial funding toward research and innovation in personalized medicine. Non-oncology applications, particularly in neurodegenerative diseases like Alzheimer’s, are a key focus. The program supports multi-country clinical trials and cross-border data sharing. These strategies help create evidence-based personalized treatments. With increasing funding, such initiatives position Europe as a strategic hub for next-generation diagnostics and therapies tailored to individual patient needs.

The alignment of public health goals with precision care is enhancing regulatory support and clinical integration. Governments are encouraging partnerships between research institutions, biotech firms, and healthcare providers. These collaborations improve access to advanced diagnostics and reduce treatment variability. As funding continues, the pipeline for non-oncology precision therapies is expected to expand. Conditions such as autoimmune diseases and diabetes are likely to see early adoption of these innovations, reinforcing the sector’s long-term market potential.

Trends

Increasing Adoption of Polygenic Risk Scores in Non-Oncology Precision Medicine

Polygenic Risk Scores (PRS) are emerging as a transformative tool in non-oncology precision medicine. These scores aggregate genetic information across multiple loci to estimate an individual’s predisposition to certain diseases. In recent years, PRS has been widely applied beyond oncology, particularly in cardiometabolic diseases. For example, in coronary artery disease and type 2 diabetes, PRS helps in early detection by identifying individuals at higher genetic risk. This shift supports the transition from reactive treatment to proactive disease management, enabling healthcare providers to act before symptoms appear.

The integration of PRS into non-oncology care pathways enables better patient stratification. This approach allows clinicians to group patients based on their genetic susceptibility rather than just clinical or lifestyle factors. As a result, risk-based categorization becomes more precise and actionable. Health systems and research institutes are now using PRS to guide decisions on screening frequency, lifestyle modifications, and early therapeutic interventions. These applications significantly improve preventive care outcomes and optimize resource allocation.

Moreover, the utility of PRS aligns with the core principles of precision medicine—personalization and prevention. It empowers healthcare providers to develop tailored preventive strategies based on a person’s unique genetic makeup. In population-level health programs, PRS contributes to identifying at-risk individuals before disease onset, thereby reducing long-term healthcare costs. As genomic data becomes more accessible and computational methods more refined, the clinical adoption of PRS in non-oncology settings is expected to rise steadily, further advancing precision-based healthcare models.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 44.2% share and holds US$ 37.3 billion market value for the year. This leading position was driven by the region’s advanced healthcare systems and wide adoption of genomic technologies. Several hospitals and research centers in the United States have integrated precision medicine into routine care. Access to high-end diagnostic tools and strong clinical expertise supported the use of tailored therapies across various non-oncology conditions.

Government initiatives played a crucial role in expanding precision medicine in the region. Programs such as the U.S. Precision Medicine Initiative have increased research funding and encouraged innovation. Public health agencies have supported the use of biomarkers and genomic data in clinical practice. Educational efforts have also improved awareness among both physicians and patients. This has led to earlier diagnoses and better treatment outcomes for diseases like cardiovascular and neurological disorders.

The high burden of chronic illnesses in North America has further increased demand for personalized care. According to the CDC, six in ten American adults live with a chronic disease. This growing patient population benefits from targeted therapies that offer better disease management. Healthcare spending in the region remains high, ensuring continued investment in personalized approaches. With the support of skilled healthcare professionals and infrastructure, North America is expected to sustain its market dominance in the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Non-Oncology Precision Medicine market is driven by leading pharmaceutical, diagnostic, and med-tech companies. Pfizer Inc. is a key player, offering targeted therapies for cardiovascular, endocrine, and inflammatory diseases. Abbott Laboratories strengthens the market with advanced diagnostics, particularly in diabetes and cardiovascular conditions. Medtronic supports precision care with AI-enabled devices for chronic disease management. Each of these companies prioritizes innovation and strategic collaboration. Their efforts align with the rising need for early diagnosis and personalized treatment, making them central to the growth of non-oncology precision medicine.

Novartis AG and Eli Lilly and Company are also major contributors. Novartis invests in genomics and companion diagnostics for inflammatory and neurological disorders. The company’s acquisitions in gene therapy and AI platforms support its personalized care strategies. Eli Lilly focuses on biomarker-driven therapies for CNS and autoimmune diseases. It integrates real-world data to improve treatment precision. Both firms aim to enhance therapeutic outcomes by enabling tailored treatment regimens and improving adherence through digital platforms.

Other influential players include Roche Diagnostics, Thermo Fisher Scientific, Illumina Inc., and Qiagen. These companies lead in molecular diagnostics, genomic sequencing, and data analytics. Their technologies enable precise patient profiling and assist drug developers in designing targeted therapies. The market outlook shows increasing collaboration among pharma, diagnostics, and digital health providers. Emphasis is shifting toward AI-driven solutions, biomarker discovery, and real-world evidence generation. This convergence is expected to expand non-oncology precision medicine applications and improve patient outcomes globally.

Market Key Players

- Pfizer Inc.

- Abbott Laboratories

- Medtronic

- Novartis

- Eli Lilly & Company

- Laboratory Corporation of America Holdings

- Qiagen Inc.

- Quest Diagnostics Inc.

- Bristol Myers Squibb

- Danaher Corporation

Recent Developments

- In September 2023: Abbott Laboratories completed the acquisition of Bigfoot Biomedical, a company specializing in smart insulin management systems. This strategic move aims to integrate Bigfoot’s advanced technology with Abbott’s FreeStyle Libre® portfolio, thereby enhancing personalized diabetes management solutions. The acquisition underscores Abbott’s commitment to expanding its digital health strategy and providing connected care solutions for individuals with diabetes.

- In March 2024: Eli Lilly participated in a $65 million Series B financing round for Ampersand Biomedicines, a precision medicine start-up. Ampersand is developing drugs engineered for more targeted delivery, with two new immunological drug candidates in preclinical development—one focused on inflammation and the other on cancer. This investment underscores Lilly’s commitment to advancing precision medicine approaches in immunology.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 84.5 Billion |

| Forecast Revenue (2034) | US$ 194.7 Billion |

| CAGR (2025-2034) | 8.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Diagnostics, Therapeutics), By Application (Oncology, CNS, Immunology, Respiratory, Infectious Diseases, Neurology, Other), By End User (Hospitals, Diagnostics Center, Research & Academic Institutes, Others) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Pfizer Inc., Abbott Laboratories, Medtronic, Novartis, Eli Lilly & Company, Laboratory Corporation of America Holdings, Qiagen Inc., Quest Diagnostics Inc., Bristol Myers Squibb, Danaher Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |