Quick Navigation

Report Overview

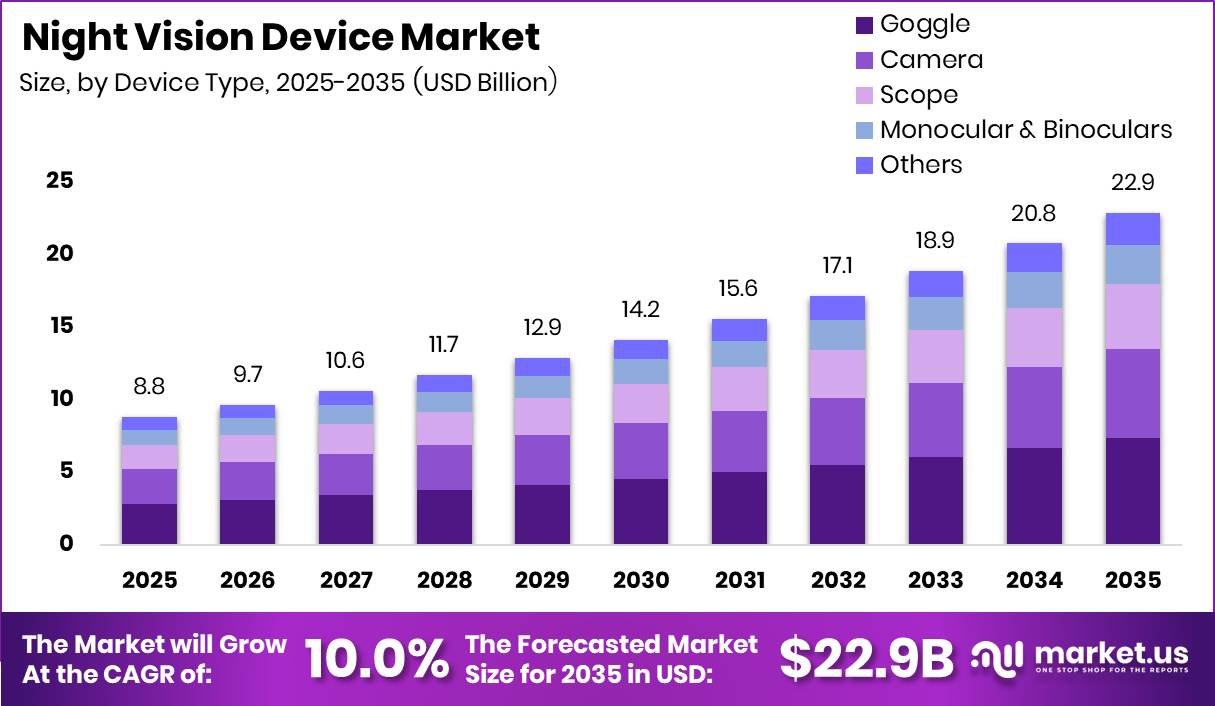

Global Night Vision Device Market size is expected to be worth around USD 22.9 Billion by 2035 from USD 8.8 Billion in 2025, growing at a CAGR of 10.0% during the forecast period 2026 to 2035. This trajectory positions the market as one of the most capital-intensive segments within defense optics, compressing a decade of volume expansion into a period defined by funded military modernization programs and sovereign procurement commitments.

The night vision device market covers optical and electronic systems that enable human or machine perception in low-light, near-dark, or thermally active environments. This market spans image-intensifier goggles, thermal cameras, weapon scopes, monoculars, and binoculars, distributed across defense forces, homeland security agencies, and industrial end users. Products range from single-tube legacy monoculars to fused binocular platforms that combine image intensification with thermal overlays.

North America commands the largest share of global procurement, anchored by U.S. Army infantry modernization programs and multi-year IDIQ contracts that provide vendors with sustained manufacturing volume. Government investment in soldier equipment has shifted from episodic replacement cycles to structured, contract-backed production frameworks. This shift stabilizes revenue predictability for prime contractors and their supply chains.

Key Takeaways

- The global Night Vision Device Market is valued at USD 8.8 Billion in 2025 and is forecast to reach USD 22.9 Billion by 2035 at a CAGR of 10.0%.

- By Device Type, Goggle leads with a 32.2% share in 2025.

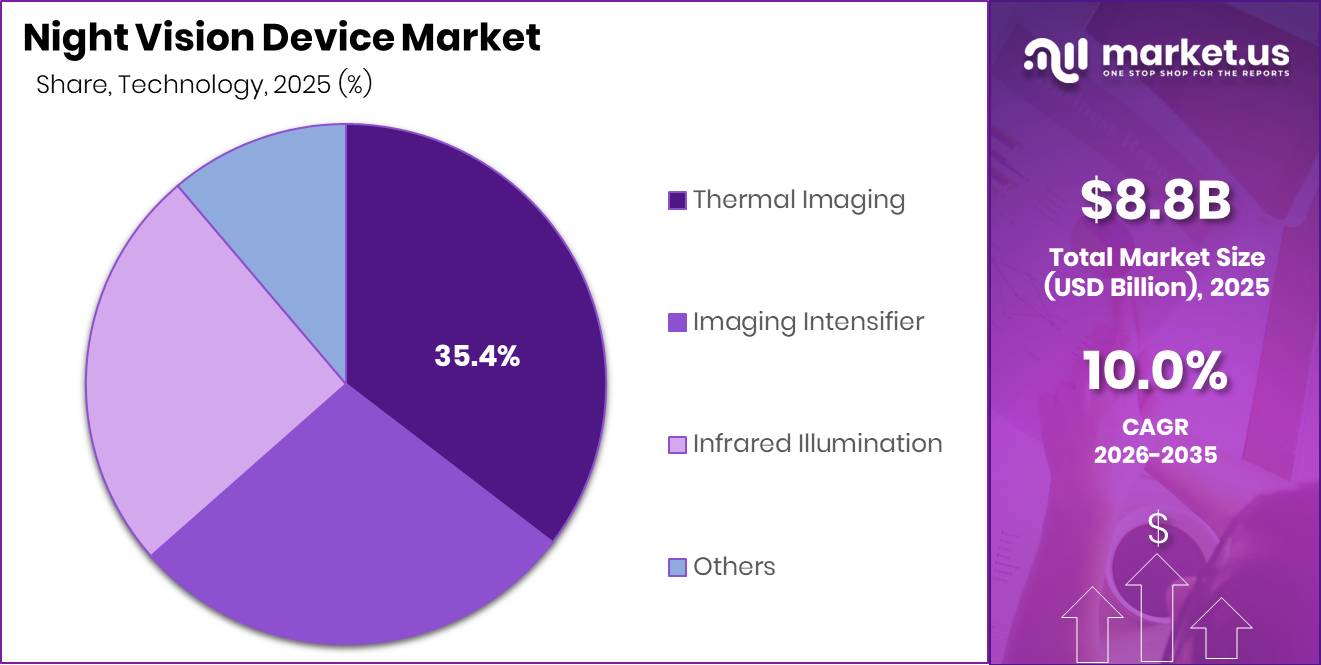

- By Technology, Thermal Imaging holds the dominant position with a 35.4% share in 2025.

- By Application, Border Surveillance accounts for the largest share at 22.1% in 2025.

- By End Users, Defense Forces dominate with a 43.4% share in 2025.

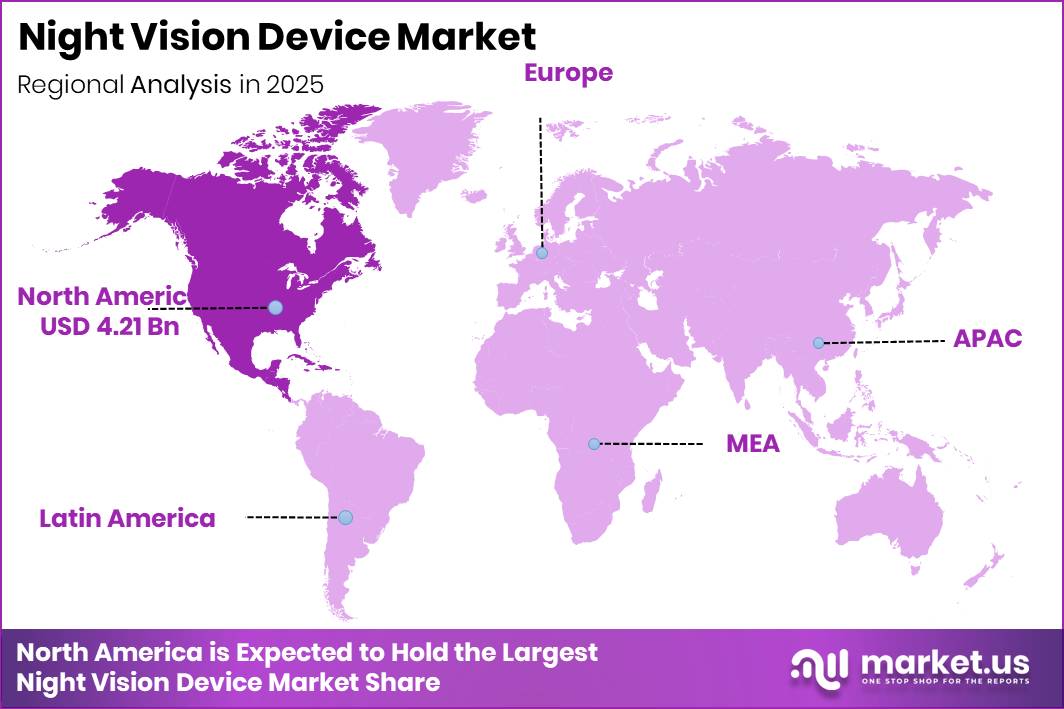

- North America is the dominant region with a 47.9% market share, valued at USD 4.21 Billion in 2025.

As per our research, L3Harris had delivered more than 18,000 ENVG-B systems to the U.S. Army by January 2025, and more than 28,000 advanced vision goggles to military users worldwide by the same date. These figures confirm that premium binocular and fused device configurations are gaining adoption at scale. Vendors positioned in this configuration class carry higher average selling prices and longer sustainment revenue streams.

In March 2025, Deepnight secured $5.5 million in seed funding to commercialize AI-powered night-vision technology designed to reduce reliance on traditional image-intensifier hardware and lower system costs. This investment signals that software-defined architectures are entering the competitive field. Buyers and investors should monitor whether AI-native platforms compress hardware margins for traditional tube-based suppliers over the medium term.

Device Type Analysis

Goggle dominates with 32.2% due to military-grade binocular adoption across infantry programs.

In 2025, Goggle held a dominant market position in the By Device Type segment of Night Vision Device Market, with a 32.2% share. The ENVG-B system delivers a 40-degree field of view for soldiers in low-light conditions, while the Ground Panoramic Night Vision Goggle (GPNVG) extends this to a 97-degree panoramic field of view. This performance gap between legacy monoculars and modern goggle platforms compels defense buyers to prioritize goggle procurement in infantry modernization programs, directly expanding the segment’s revenue base.

Camera systems capture the next significant share within the device type segment. Thermal and low-light cameras serve fixed-site surveillance, vehicle-mounted applications, and unmanned system payloads, which broadens their addressable procurement base beyond individual soldier equipment. This versatility across multiple platforms makes the camera sub-segment a structurally durable revenue contributor outside of pure infantry spending cycles.

Scope systems serve precision engagement roles and remain embedded in long-range marksmanship and sniper programs across defense and law enforcement. Their procurement is typically tied to rifle and weapon system upgrade contracts rather than standalone optics budgets. In May 2026, L3Harris confirmed preparations for initial production orders of the NOVA night-vision system under the U.S. Army BiNOD program, signaling that next-generation scope-compatible digital overlays will expand the addressable range for this sub-segment. Monocular and Binoculars together with Others account for the remaining share, anchored by legacy replacement demand and specialist civilian applications.

Technology Analysis

Thermal Imaging dominates with 35.4% due to all-weather detection capability across defense use cases.

In 2025, Thermal Imaging held a dominant market position in the By Technology segment of Night Vision Device Market, with a 35.4% share. Thermal systems detect heat signatures independent of ambient light or smoke conditions, giving them a performance advantage over image-intensifier platforms in degraded visual environments. Defense procurement programs that require vehicle detection, perimeter surveillance, and aerial reconnaissance consistently specify thermal-capable equipment, driving sustained volume in this technology class.

Imaging Intensifier technology retains a strong position due to its deep integration within soldier-worn goggle programs. Military qualification processes, existing maintenance infrastructure, and established supply chains for image-intensifier tubes create high switching barriers for defense buyers. This inertia sustains demand for intensifier-based platforms even as fusion systems that combine both thermal and intensifier outputs expand their share of premium binocular contracts.

Infrared Illumination technology serves close-range and covert applications where active illumination provides a usable image without generating visible light signatures.cem Law enforent, special operations, and border security units rely on this technology for room-clearing, vehicle identification, and low-altitude aviation applications. Others within this segment cover emerging digital night-vision architectures, including software-defined imaging platforms entering the market through commercial and dual-use procurement channels.

Application Analysis

Border Surveillance dominates with 22.1% due to large-scale government surveillance infrastructure budgets.

In 2025, Border Surveillance held a dominant market position in the By Application segment of Night Vision Device Market, with a 22.1% share. Large defense and interior ministry appropriations for perimeter monitoring, tower surveillance, and patrol support have converted border security into a consistent volume driver for night vision procurement. The scale of these budgets sustains demand across both thermal camera platforms and goggle-equipped patrol units simultaneously.

Law Enforcement represents a high-frequency procurement channel where urban policing, counter-narcotics operations, and tactical team equipment form a recurring replacement market. Agencies purchase across multiple device types depending on operational roles, from weapon-mounted scopes to handheld monoculars. This breadth of configuration demand limits single-product dominance and rewards vendors with broad portfolio coverage.se

Security applications cover commercial facility protection, critical infrastructure monitoring, and private sector installations, which constitute a growing civilian demand channel. Maritime and Coastal Surveillance serves naval patrol, port security, and fisheries enforcement, with ship-mounted and handheld thermal cameras as the primary device type. Engineering, Fire and Rescue, and Medical applications together with Others account for the remaining share, each supported by specialized procurement cycles distinct from defense and law enforcement timelines.

End Users Analysis

Defense Forces dominate with 43.4% due to funded multi-year infantry modernization programs.

In 2025, Defense Forces held a dominant market position in the By End Users segment of Night Vision Device Market, with a 43.4% share. The U.S. Army had procured 35,000 ENVG-B systems by September 2025, confirming that funded infantry modernization programs are converting budget allocations into delivered hardware at scale. Defense dominance in this segment reflects not just volume but also contract structure, as IDIQ and multi-year frameworks lock in demand visibility that no other end user category matches.

Homeland Security Agencies form the second largest end user group, covering border patrol, coast guard, and internal security organizations that operate under separate appropriations from military budgets. Their procurement typically favors camera systems and vehicle-mounted thermal platforms over soldier-worn goggle configurations. This device preference creates a structurally differentiated demand profile within the same geographic markets served by defense customers.

The Industrial Sector purchases night vision devices primarily for infrastructure inspection, energy facility monitoring, and search operations in remote environments. Procurement cycles in this segment are driven by operational efficiency requirements rather than security mandates. Others account for the residual share, covering research institutions, private security firms, and specialist civilian users operating in regulated markets.

Key Market Segments

By Device Type

- Goggle

- Camera

- Scope

- Monocular and Binoculars

- Others

By Technology

- Thermal Imaging

- Imaging Intensifier

- Infrared Illumination

- Others

By Application

- Border Surveillance

- Engineering

- Fire and Rescue

- Law Enforcement

- Maritime and Coastal Surveillance

- Medical

- Security

- Others

By End Users

- Defense Forces

- Homeland Security Agencies

- Industrial Sector

- Others

Drivers

Soldier modernization procurement represents the strongest near-term demand driver, because it converts infantry upgrade programs into funded, contract-backed volume visibility. L3Harris received a $263 million U.S. Army order for continued ENVG-B production in January 2025. In April 2026, the company was also selected for the Army’s NOVA night-vision program under a 7-year contract worth up to $465 million.

Elbit Systems of America received a $112 million Marine Corps delivery order for Squad Binocular Night Vision Goggle systems with production running through December 2026. These awards support premium binocular and fused-device configurations rather than legacy monocular refresh, raising average selling prices and extending sustainment revenue through spare parts and refurbishment. THEON’s total backlog, including options, reached approximately €2.4 billion in December 2025, more than double the level recorded at year-end 2024. This backlog size confirms that funded defense demand is concentrating with established suppliers, strengthening barriers to entry for new competitors across the near term.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soldier modernization procurement surge | +2.1% | North America core, NATO Europe, selective APAC defense programs | Short term (≤ 2 years) |

| Shift to fused thermal + image-intensified systems | +1.7% | North America core, EU, Israel-linked supply chains, APAC premium segments | Medium term (2-4 years) |

| Image intensifier tube capacity localization | +1.3% | U.S. core, France/Germany-led Europe, transatlantic supply base | Medium term (2-4 years) |

| Border and law-enforcement night surveillance expansion | +0.9% | EU external borders, North America, Middle East corridors, South Asia spill-over | Short term (≤ 2 years) |

| Export-control and compliance segmentation | +0.6% | EU, U.S., Middle East import markets, APAC distributors | Medium term (2-4 years) |

| Digital night vision and microdisplay upgrades | +1.1% | U.S. defense R&D, Japan/U.S. component chains, advanced commercial users in EU/APAC | Long term (≥ 4 years) |

Restraints

The most immediate physical bottleneck in this market is image-intensifier-tube throughput, because military binoculars and goggles cannot scale faster than tube output, screening yield, and final integration capacity. Photonis was scheduled to supply 40,000 4G 16 mm tubes for German and Belgian programs over 2024 to 2025. Exosens and Theon subsequently disclosed a much larger OCCAR-linked program for 100,000 binoculars embedding 200,000 tubes, with broader long-term commitments exceeding 400,000 tubes. This concentration of demand around a small number of qualified suppliers creates structural allocation risk for any manufacturer outside the approved supply base.

The OCCAR programme is structured to deliver more than 178,000 night vision goggles by 2030, and more than 50,000 goggle sets had already been delivered to German and Belgian armed forces by December 2025. Even before accounting for commercial and homeland-security demand, this level of defense pull extends lead times into multi-quarter allocation cycles. This supply-side congestion supports an estimated 1.2 percentage-point CAGR deduction, concentrated in 2026 to 2028, as production smoothing rather than demand generation becomes the binding constraint on market velocity.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-control friction | -1.4% | North America core, EU, Middle East, non-NATO APAC | Medium term (2-4 years) |

| Image-tube capacity bottleneck | -1.2% | EU, North America core, allied APAC corridors | Short term (≤ 2 years) |

| IR material concentration | -0.9% | Global, acute in APAC supply hubs and Western defense OEM chains | Medium term (2-4 years) |

| Budget-to-order lag | -0.8% | EU, Indo-Pacific, selective North America programs | Short term (≤ 2 years) |

| Cost inflation in ruggedized optics | -0.7% | Global | Short term (≤ 2 years) |

| Qualification and localization drag | -0.6% | India, EU, Middle East, Southeast Asia | Long term (≥ 4 years) |

Challenges

Defense-led demand is expanding faster than high-end image intensifier capacity can normalize. Exosens disclosed strong defense-driven growth in 2025 alongside a move to expand U.S. production capacity, and confirmed active 5G tube commercialization efforts. Tube manufacturing remains capital-intensive, qualification-heavy, and yield-sensitive, meaning that even when new capacity is added, the ramp typically requires 18 to 36 months to reach qualified output levels.

In practice, this capacity gap leaves OEMs facing intermittent 20 to 40-week procurement windows for premium tubes and reduced schedule confidence on large military tranches. This production constraint creates a modeled 1.0 percentage-point drag on industry CAGR because production smoothing, not demand generation, becomes the binding variable. Vendors must redesign sourcing strategies around long-range offtake agreements, second-source qualification, and closer demand signaling with ministries of defense to prevent order surges from overwhelming the still-narrow supplier base.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Export Licensing Complexity | -1.1% | North America core, EU defense exporters, allied APAC procurement nodes | Medium term (2-4 years) |

| Detector Material Volatility | -1.3% | U.S. defense supply chain, EU sensor makers, East Asian semiconductor corridors | Long term (≥ 4 years) |

| Tube Capacity Tightness | -1.0% | North America military programs, NATO rearmament markets, Middle East procurement channels | Medium term (2-4 years) |

| Photonics Talent Scarcity | -0.8% | U.S. optics clusters, Western Europe precision manufacturing bases, Israel defense electronics hubs | Long term (≥ 4 years) |

| SWaP-C Yield Bottlenecks | -0.9% | Soldier modernization programs in North America, Europe, South Korea, Australia | Medium term (2-4 years) |

| Procurement Cycle Distortion | -0.7% | NATO budgets, Indo-Pacific border/security agencies, Gulf defense buyers | Short term (≤ 2 years) |

Opportunities

Border tower analytics stacks represent the most actionable near-term monetization opportunity for night vision OEMs. U.S. border appropriations in FY2026 include $6.2 billion for border security, technology, and screening, alongside $2.6 billion directed into current surveillance technology programs. The EU’s next budget proposal assigns €15.4 billion to border management and €11.9 billion to Frontex. These appropriations create a technology procurement envelope far larger than hardware replacement cycles alone would generate.

If night vision OEMs capture only 4% to 6% of these surveillance-adjacent technology envelopes through software-linked tower packages, the incremental total addressable market could exceed $900 million to $1.4 billion over five years. Annual software attach rates of 25% to 40% and false-alarm reduction targets of 30% to 50% create a measurable ROI narrative for procuring agencies. Gross margins on bundled analytics stacks run 10 to 15 percentage points above standalone device sales, making this an economically superior product category for vendors that can execute the software integration.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Digital retrofit-as-a-service | +1.6% | North America core, NATO Europe, India | Short term (≤ 2 years) |

| Border tower analytics stacks | +1.3% | U.S., EU frontier states, Middle East | Short term (≤ 2 years) |

| Soldier XR convergence | +2.1% | U.S., NATO, South Korea, Australia | Medium term (2-4 years) |

| Civilian adjacencies scale-out | +1.1% | North America, EU, Japan, GCC | Medium term (2-4 years) |

| APAC local-assembly roll-up | +1.8% | India, Southeast Asia, South Korea | Medium term (2-4 years) |

| Thermal-data monetization layer | +0.9% | U.S., EU, smart infrastructure hubs | Long term (≥ 4 years) |

Regional Analysis

North America Dominates the Night Vision Device Market with a Market Share of 47.9%, Valued at USD 4.21 Billion

North America holds a 47.9% share valued at USD 4.21 Billion in 2025, anchored by U.S. Army infantry modernization contracts and multi-year IDIQ frameworks. The concentration of qualified domestic manufacturers, the depth of Pentagon procurement infrastructure, and the volume of active programs under execution collectively insulate this region’s market position from competitive erosion in the near term.

Europe holds the second largest regional position, driven by NATO rearmament commitments and bilateral procurement programs coordinated through agencies such as OCCAR. Export-control alignment within the alliance reduces trade friction across member state borders and enables consolidated production and delivery programs at scale. This regulatory framework makes Europe a structurally favorable region for suppliers seeking multi-country contract exposure.

Asia Pacific is accelerating through a combination of defense budget increases and indigenous manufacturing ambitions. In October 2025, India’s Ministry of Defence procured image-intensifier night sights capable of supporting target engagement up to 500 meters under low-light and starlight conditions. This procurement confirms that APAC defense ministries are moving from legacy systems toward performance-specified equipment, opening evaluation windows for both domestic and foreign suppliers.

Latin America and the Middle East and Africa regions represent smaller but structurally relevant procurement markets. Gulf security agencies invest in perimeter and maritime surveillance platforms, creating consistent demand for thermal camera and tower-mounted systems. Latin American law enforcement agencies procure lighter monocular and handheld configurations for counter-narcotics and border patrol operations, representing a different device mix than the heavier goggle-dominated procurement seen in NATO markets.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

L3Harris Technologies, Inc. holds a structurally reinforced position across the U.S. soldier modernization supply chain. The U.S. Army awarded L3Harris a $466 million BiNOD contract in 2026 for its NOVA night-vision goggle system, extending a relationship that already spans multi-year ENVG-B production orders. In January 2026, L3Harris also unveiled a commercial version of the NOVA system, targeting large-scale military and adjacent market deployment. This dual-track product strategy amplifies revenue potential while diversifying demand sources beyond single-program concentration risk.

FLIR Systems, Inc. anchors its market position in thermal imaging, where its camera platforms serve defense, law enforcement, and industrial end users across multiple device categories. FLIR’s installed base of vehicle-mounted and handheld thermal systems creates recurring maintenance and upgrade revenue that operates independently of goggle modernization program cycles. However, as fused binocular platforms that combine thermal and image intensifier outputs gain procurement share, FLIR faces competitive pressure to integrate intensifier capabilities into its core product architecture or risk ceding share in premium soldier-worn configurations to dual-technology vendors.

Key Players

- ATN Corp.

- Collins Aerospace

- Vista Outdoor Operations LLC

- L3Harris Technologies, Inc.

- FLIR Systems, Inc.

- BAE Systems

- Bharat Electronics

- Thales

- Bushnell

- Yukon Advanced Optics Worldwide

- Adorama Camera, Inc.

- Elbit Systems Ltd.

- Alpha Design Technologies Pvt Ltd

- MKU Limited

- Bharat Electronics Limited (BEL)

- Other Key Players

Recent Developments

- April 2026 – L3Harris Technologies was selected by the U.S. Army for the Binocular Night Observation Device (BiNOD) program and received a 7-year contract worth up to $465 million to supply its NOVA night-vision goggle system.

- September 2025 – THEON International launched the NYX-BiNOD, a production-ready night-vision binocular developed to meet U.S. Army BiNOD requirements and target upcoming military modernization programs.

- June 2026 – L3Harris announced continued expansion of its BNVD-Fused night-vision platform, including new digital overlay and augmented-reality capabilities for NATO and Five Eyes military customers.

- February 2026 – Photonis Defense (Exosens) was awarded a U.S. Army BiNOD contract, strengthening its position in the military night-vision market as a supplier of complete binocular night-vision systems.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 8.8 Billion |

| Forecast Revenue (2035) | USD 22.9 Billion |

| CAGR (2026-2035) | 10.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Device Type (Goggle, Camera, Scope, Monocular and Binoculars, Others), By Technology (Thermal Imaging, Imaging Intensifier, Infrared Illumination, Others), By Application (Border Surveillance, Engineering, Fire and Rescue, Law Enforcement, Maritime and Coastal Surveillance, Medical, Security, Others), By End Users (Defense Forces, Homeland Security Agencies, Industrial Sector, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | ATN Corp., Collins Aerospace, Vista Outdoor Operations LLC, L3Harris Technologies, Inc., FLIR Systems, Inc., BAE Systems, Bharat Electronics, Thales, Bushnell, Yukon Advanced Optics Worldwide, Adorama Camera, Inc., Elbit Systems Ltd., Alpha Design Technologies Pvt Ltd, MKU Limited, Bharat Electronics Limited (BEL), Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |