Quick Navigation

Report Overview

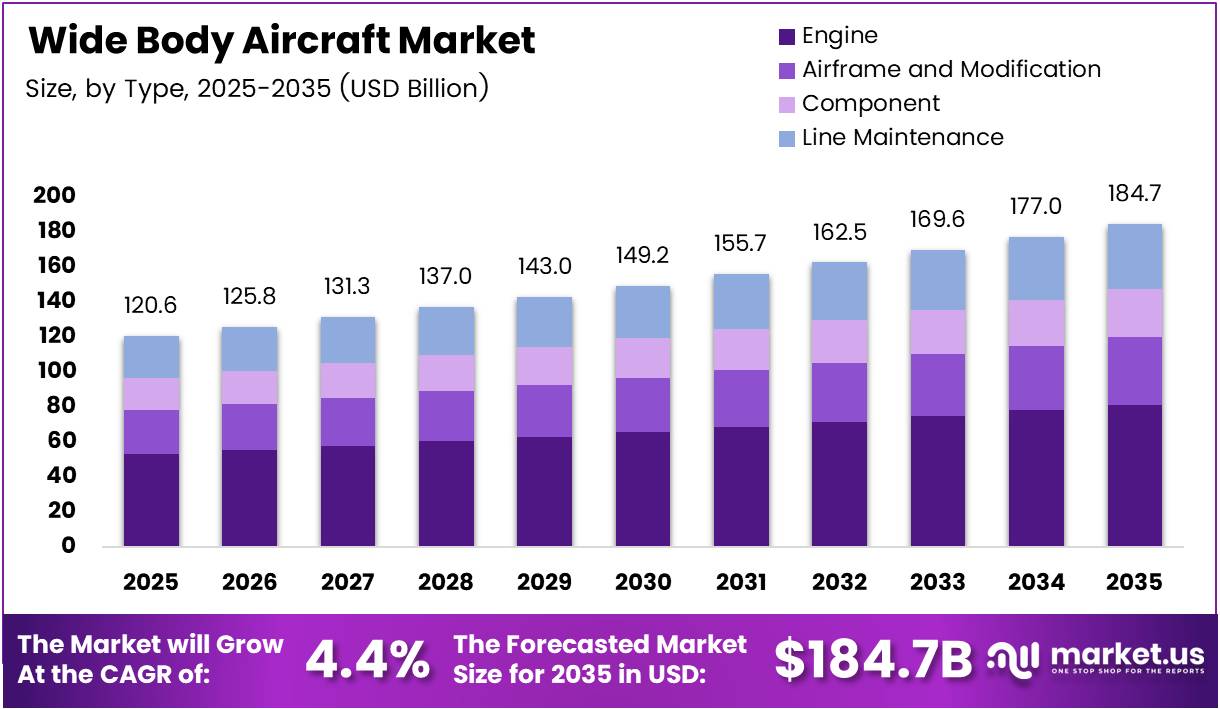

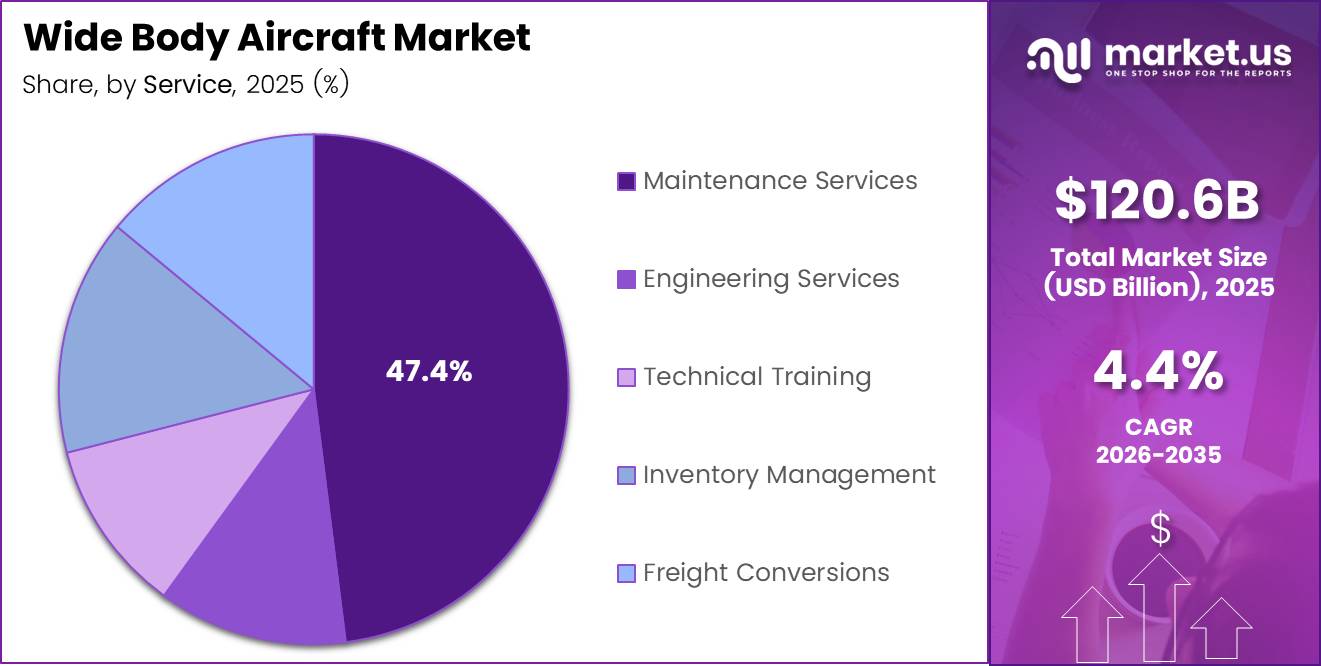

Global Wide Body Aircraft Market size is expected to be worth around USD 184.7 Billion by 2035 from USD 120.6 Billion in 2025, growing at a CAGR of 4.4% during the forecast period 2026 to 2035.

Wide body aircraft are twin-aisle commercial jets designed for long-haul intercontinental operations, carrying between 200 and 600 passengers across routes that narrow body aircraft cannot serve economically. Their wider fuselage supports both passenger capacity and under-floor cargo volume, making them structurally central to airline revenue models on trunk routes.

The market spans four key service layers: engine services, airframe and modification work, component supply, and line maintenance. This structure means market value does not track solely with new aircraft deliveries — it compounds through aftermarket spend over a 25-to-30-year airframe lifecycle. Airlines that operate wide body fleets commit to decades of recurring MRO expenditure, creating durable revenue visibility for service providers.

Airline fleet expansion and route network growth are the primary demand engines. As intercontinental passenger traffic rebounds and exceeds pre-pandemic levels, carriers in Asia Pacific, the Middle East, and Latin America are ordering wide body jets to establish or deepen long-haul presence. This order activity signals a structural shift in where global aviation capacity is being added, not just a cyclical recovery.

Freight conversion demand adds a second growth layer. Passenger wide body aircraft nearing retirement are being converted into dedicated freighters, extending their economic life and meeting e-commerce-driven air cargo capacity needs. This conversion pipeline creates a separate revenue stream within the wide body services ecosystem that is largely independent of new aircraft orders.

According to Aerospace Global News, widebody aircraft deliveries in 2025 reached 246 units, up 43% year-on-year. Widebody orders climbed to 869 aircraft — more than double the 2024 level — and the widebody backlog expanded 24% year-on-year to nearly 3,000 aircraft. These figures confirm that OEM production pipelines are under sustained pressure, and that service providers who scale capacity now will capture the highest-margin aftermarket windows.

According to Aerospace Global News, global commercial aircraft deliveries totalled 1,411 in 2025, a 25% increase on 2024 and the strongest annual performance since 2018. Total orders reached 2,175 aircraft, a 50% year-on-year increase, with the global order backlog reaching a record 16,371 aircraft by year-end. For wide body market participants, this record backlog translates into guaranteed service demand stretching well beyond the current forecast period.

Key Takeaways

- The Wide Body Aircraft Market was valued at USD 120.6 Billion in 2025 and is forecast to reach USD 184.7 Billion by 2035, at a CAGR of 4.4%.

- By Type, Engine services held the largest share at 43.8% in 2025, driven by the high recurring cost of turbofan maintenance and overhaul cycles.

- By Service, Maintenance Services dominated with a 47.4% share, reflecting the MRO-intensive nature of wide body fleet operations.

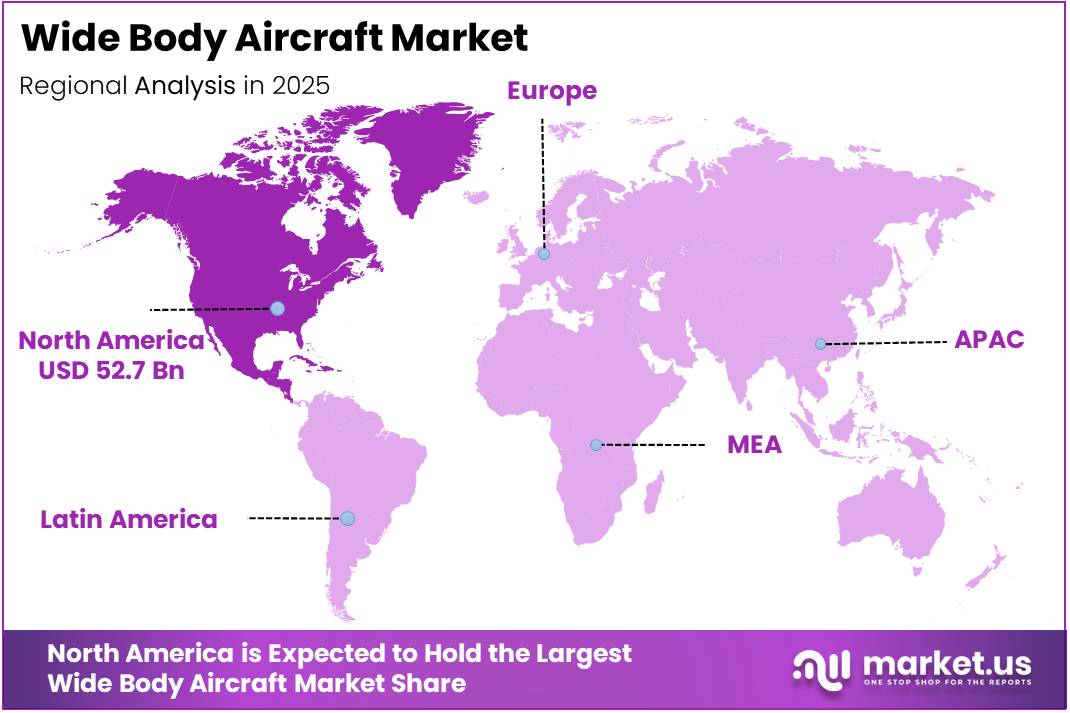

- North America led all regions with a 43.70% market share, valued at USD 52.7 Billion in 2025.

- Widebody orders in 2025 reached 869 aircraft, more than doubling the 2024 level, with the backlog expanding to nearly 3,000 aircraft.

- In May 2025, Qatar Airways placed the largest widebody order in Boeing history — up to 210 jets including 130 Boeing 787 Dreamliners and 30 Boeing 777-9s.

Product Analysis

Engine dominates with 43.8% due to high-frequency, high-cost overhaul cycles.

In 2025, Engine services held a dominant market position in the By Type segment of the Wide Body Aircraft Market, with a 43.8% share. Wide body turbofan engines — particularly large-fan models such as the GE9X and Trent XWB — require shop visits every 4,000 to 6,000 flight hours, generating aftermarket revenue that exceeds initial engine acquisition cost over a full service life. This cycle-driven demand makes engine services the most defensible revenue segment in the market.

Airframe and Modification services capture the structural and conversion opportunity within the wide body fleet. Heavy maintenance checks, structural inspections, and passenger-to-freighter conversions all sit within this segment. According to Boeing, the Boeing 787 Dreamliner airframe is composed of 50% carbon fibre reinforced plastic and other composites by weight — compared to just 12% composites on the Boeing 777 — with each 787 containing approximately 32,000 kg of CFRP. The shift to composite-heavy airframes creates specialized maintenance requirements that favour providers with advanced materials capability over traditional metalwork facilities.

Component services represent the supply chain layer that keeps wide body fleets airworthy between scheduled maintenance events. This segment covers avionics, landing gear, actuation systems, and cabin interiors. Component lead times have extended sharply due to post-pandemic supply chain disruption, creating inventory management pressure across operators and pushing component MRO spend upward.

Line Maintenance differentiates through speed and network reach rather than technical complexity. Wide body operators require rapid turnaround maintenance at hub airports globally to protect schedule reliability. Consequently, line maintenance is increasingly outsourced to specialist providers with on-airport presence, enabling airlines to reduce ground time without maintaining large in-house technical workforces at every station.

Service Analysis

Maintenance Services dominates with 47.4% due to mandatory regulatory compliance driving continuous spend.

In 2025, Maintenance Services held a dominant market position in the By Service segment of the Wide Body Aircraft Market, with a 47.4% share. Airworthiness directives, scheduled maintenance programs, and mandatory overhaul intervals create non-discretionary demand that is structurally immune to airline cost-cutting. In May 2024, Air India launched a USD 400 million widebody fleet retrofit programme for its legacy Boeing 787-8 aircraft — underscoring how maintenance commitments scale with fleet age and operational intensity.

Engineering Services carries the highest margin within the service mix, encompassing modifications, performance upgrades, and fleet-specific technical solutions. Airlines deploy engineering services to extend airframe service life, integrate connectivity systems, and address airworthiness compliance requirements. Providers with OEM-adjacent engineering capability command premium pricing and long-term contracts that insulate them from spot-market rate pressure.

Technical Training serves as the entry point for airline relationships, providing the certified crew and technician capability that underpins all other service segments. As new-generation wide body types enter service — with composite airframes and advanced avionics — training demand intensifies. Airlines cannot operate or maintain aircraft without type-certified personnel, making technical training a strategic dependency rather than a discretionary cost.

Inventory Management differentiates through parts availability speed and supply chain visibility. Wide body operators face significant financial exposure from aircraft-on-ground events caused by missing components. Providers that offer pooling arrangements, consignment stocks, and real-time inventory visibility reduce AOG risk and capture long-term contract value from cost-conscious operators.

Freight Conversions represent the segment with the clearest near-term growth signal, driven by e-commerce air cargo demand and limited dedicated freighter production. Passenger wide body aircraft nearing end-of-passenger-life are converted into dedicated freighters, extending their economic life by 10 to 15 years. This conversion pipeline is growing as cargo-focused operators and logistics companies seek cost-effective capacity alternatives to new freighter procurement.

Key Market Segments

By Type

- Engine

- Airframe and Modification

- Component

- Line Maintenance

By Service

- Maintenance Services

- Engineering Services

- Technical Training

- Inventory Management

- Freight Conversions

Drivers

Long-Haul Traffic Growth and Fleet Modernization Are Accelerating Wide Body Procurement Cycles

Rising international passenger traffic is translating directly into aircraft orders. Airlines expanding intercontinental route networks require high-capacity twin-aisle jets that can sustain operational economics across 10-to-16-hour sectors. According to Boeing, the Boeing 777-9 achieves 20% lower fuel use and emissions, a 40% smaller noise footprint, and 10% lower operating costs than competing aircraft. These numbers make the procurement decision financially straightforward for operators replacing aging fleets.

Fleet modernization programs reinforce demand beyond organic traffic growth. Airlines are retiring older generation wide body types — including early Boeing 777 and Airbus A330 variants — and replacing them with next-generation aircraft that reduce per-seat operating costs. This replacement cycle creates predictable forward demand for both new aircraft and the MRO infrastructure required to support them through their service life.

Air cargo demand adds a parallel procurement driver. Wide body freighter conversions and dedicated freighter orders reflect structural e-commerce volume growth that cannot be served by belly cargo alone. In May 2024, IndiGo placed a firm order for 30 Airbus A350-900 aircraft — its first-ever widebody order — marking a strategic expansion into long-haul operations and signalling the scale of demand building among Asia-Pacific carriers entering the intercontinental market for the first time.

Restraints

High Ownership Costs and Supply Chain Disruption Create Compounding Financial Pressure on Operators

Wide body aircraft carry the highest ownership cost profile in commercial aviation. Acquisition costs for next-generation types exceed USD 200 million per airframe, and annual maintenance obligations add tens of millions more. Jet fuel price volatility compounds this exposure — fuel represents 20 to 30% of airline operating costs, and wide body operations on long-haul routes face proportionally larger absolute fuel bills than short-haul narrow body operations.

According to IATA, supply chain delays forced airlines to operate older aircraft longer than planned. Delayed delivery of new aircraft cost airlines an estimated USD 4.2 billion in foregone fuel efficiency savings and USD 3.1 billion in additional maintenance costs in 2025. These figures reveal that the cost of supply chain dysfunction is not theoretical — it compounds annually and falls disproportionately on carriers with large wide body fleets awaiting replacement deliveries.

Aircraft lease rates further tighten operator margins. Lease rates increased 20 to 30% from 2019 to end of 2024, according to IATA, as constrained OEM output reduced available aircraft supply. For airlines that rely on operating leases to manage fleet flexibility, this rate environment raises the effective cost of wide body capacity and reduces the economic case for network expansion into marginal long-haul routes.

Growth Factors

Next-Generation Aircraft Efficiency, Cargo Conversion Demand, and Leasing Market Expansion Unlock New Revenue Pools

Next-generation wide body types deliver measurable operating cost advantages that justify accelerated fleet renewal. According to Airbus, the A350 achieves a 25% advantage in fuel burn, operating costs, and CO2 emissions versus previous-generation competitor aircraft, and produces 31% lower NOx emissions below the CAEP/6 standard. These performance margins translate into route-level profitability improvements that airlines can quantify at the fleet planning stage — shortening procurement decision cycles.

According to Airbus, the A350 achieved 99.3% operational reliability over the 12 months to end of November 2024, across over 1.6 million revenue flights and 1,270+ routes, carrying 437+ million passengers. This reliability record matters commercially because it reduces spare aircraft requirements, lowers AOG event costs, and strengthens the aircraft’s residual value — factors that carry direct weight in airline and lessor acquisition decisions.

The leasing market creates a structurally important access channel for wide body capacity. In November 2024, Stonepeak announced a definitive agreement to acquire Air Transport Services Group (ATSG) — a global leader in medium widebody freighter leasing — in an all-cash transaction at an enterprise valuation of approximately USD 3.1 billion. Transactions at this scale confirm institutional capital’s conviction that wide body leasing generates durable, asset-backed returns — and that the freighter conversion segment is attracting serious strategic investment.

Emerging Trends

Composite Airframe Adoption, Sustainable Aviation Goals, and Digital Maintenance Systems Are Redefining Wide Body Operations

Advanced composite materials are now structural to wide body competitiveness. According to Airbus, the A350 airframe is made from over 70% advanced materials including carbon fibre composites — a material choice that drives both fuel efficiency and structural performance. This shift away from aluminium-dominant construction is not a design preference; it is a prerequisite for meeting the fuel burn and weight targets that make new-generation aircraft economically viable at launch.

Ultra-long-haul route development is creating demand for aircraft with range profiles that previous wide body generations could not achieve commercially. Airlines deploy purpose-built long-range variants on non-stop city pairs that previously required one-stop itineraries. This route development creates durable demand for specific aircraft types and gives operators with the right fleet a structural competitive advantage over carriers that cannot operate the same city pairs non-stop.

Sustainable aviation commitments and digital maintenance integration are converging into a single operational pressure point. Airlines face regulatory and investor pressure to reduce carbon emissions while simultaneously managing aging fleets with constrained MRO capacity. Predictive analytics and digital maintenance systems allow operators to optimize component replacement timing, reduce unscheduled removals, and extend time-on-wing — outcomes that directly reduce both emissions exposure and maintenance cost per flight hour.

Regional Analysis

North America Dominates the Wide Body Aircraft Market with a Market Share of 43.70%, Valued at USD 52.7 Billion

North America holds a 43.70% share valued at USD 52.7 Billion, anchored by the United States — home to the world’s largest wide body MRO infrastructure, two of the largest commercial aircraft manufacturers, and the highest concentration of wide body operators globally. The depth of procurement, regulatory, and technical capability embedded in the US market creates competitive barriers that other regions have not yet replicated at scale.

Europe Wide Body Aircraft Market Trends

Europe commands a significant share, driven by the presence of Airbus manufacturing operations and a mature airline sector with extensive long-haul networks. European carriers operate large wide body fleets on transatlantic and Asia-Pacific trunk routes, generating substantial MRO demand. Stringent EU emissions regulations accelerate fleet renewal toward fuel-efficient next-generation types, supporting sustained procurement activity through the forecast period.

Asia Pacific Wide Body Aircraft Market Trends

Asia Pacific represents the fastest-expanding regional demand centre. Carriers in China, India, and Southeast Asia are adding wide body capacity to serve both intercontinental passenger routes and intra-regional long-haul demand. IndiGo’s first-ever widebody order for 30 Airbus A350-900 aircraft in May 2024 illustrates how carriers previously confined to domestic and short-haul operations are now entering the intercontinental market, driving structural demand growth.

Middle East and Africa Wide Body Aircraft Market Trends

The Middle East sustains disproportionate wide body demand relative to its geography, due to the hub-and-spoke strategies of its major carriers, which position Gulf airports as transfer nodes between East and West. Qatar Airways’ landmark order for up to 210 widebody Boeing jets in May 2025 confirms the region’s continued appetite for large-scale fleet expansion and its strategic weight in global wide body procurement.

Latin America Wide Body Aircraft Market Trends

Latin America holds a smaller but growing share, with demand concentrated among full-service carriers operating long-haul routes to Europe, North America, and intra-regional South American sectors. Airport infrastructure investment in Brazil, Mexico, and Colombia is expanding hub capacity, gradually enabling carriers in the region to support wider wide body fleet operations and associated maintenance ecosystems.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

GE Aviation holds a structurally dominant position in wide body propulsion through its GE9X engine family, which powers the Boeing 777X. The GE9X-105B1A features a 134-inch fan diameter — the largest commercial turbofan built — and has accumulated over 3,500 hours of flight testing alongside the 777X programme. GE’s engine installed base creates decades of guaranteed aftermarket revenue that competitors cannot displace without displacing the aircraft itself.

Lockheed Martin operates at the intersection of defence and commercial aerospace, with capabilities spanning advanced materials, systems integration, and aircraft modification. Within the wide body context, Lockheed’s strength lies in applying defence-grade engineering discipline to commercial MRO and modification programmes. This cross-sector positioning gives Lockheed access to government procurement channels that purely commercial MRO providers cannot reach.

Rockwell Collins — now integrated into Collins Aerospace — anchors wide body avionics and cabin systems supply. Its connectivity, flight management, and cabin electronics portfolio appears across virtually every modern wide body platform. Collins’ multi-OEM relationships mean it captures value regardless of whether airlines operate Airbus or Boeing fleets, reducing its exposure to any single manufacturer’s production cycle risk.

Airbus shapes wide body market dynamics as both manufacturer and services provider. The A350 family’s 25% fuel burn advantage and 99.3% operational reliability position it as the reference standard for next-generation wide body performance. In April 2025, Aviation Capital Group signed an agreement with Avolon to acquire a portfolio of 20 aircraft including 4 new-technology widebody aircraft on lease to 17 airlines across 16 countries — reinforcing the secondary market depth behind Airbus wide body assets.

Key players

- GE Aviation

- Lockheed Martin

- Rockwell Collins

- Airbus

- Rolls Royce

- Mitsubishi Aircraft Corporation

- Thales Group

- Boeing

- British Aerospace

- Northrop Grumman

- Bombardier

Recent Developments

- May 2025 — Qatar Airways and Boeing announced a historic order for up to 210 widebody jets — the largest widebody order in Boeing history — including 130 Boeing 787 Dreamliners and 30 Boeing 777-9s, with options for an additional 50 aircraft. The deal was signed in the presence of U.S. President Donald J. Trump and the Amir of Qatar, signalling the strategic scale of Gulf carrier fleet ambitions.

- April 2025 — Stonepeak completed its acquisition of Air Transport Services Group (ATSG), with ATSG’s common shares ceasing trading on NASDAQ at a transaction value of USD 22.50 per share in cash. The deal, first announced in November 2024 at an enterprise valuation of approximately USD 3.1 billion, consolidates Stonepeak’s position as a major owner of medium widebody freighter leasing assets globally.

- May 2024 — Air India commenced a USD 400 million widebody fleet retrofit programme for its legacy Boeing 787-8 aircraft, with the first of 26 aircraft flying to a Boeing facility in Victorville, California in July 2025. The programme reflects how mature wide body fleets require substantial capital reinvestment to remain competitive on long-haul routes.

- May 2025 — Vietjet placed a new order with Airbus for 20 widebody A330-900 aircraft to support strategic expansion, signed in Hanoi during an official state visit by French President Emmanuel Macron. The order marks Vietjet’s entry into the widebody segment and illustrates how Southeast Asian low-cost carriers are graduating to twin-aisle operations to serve regional long-haul demand.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 120.6 Billion |

| Forecast Revenue (2035) | USD 184.7 Billion |

| CAGR (2026-2035) | 4.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Engine, Airframe and Modification, Component, Line Maintenance), By Service (Maintenance Services, Engineering Services, Technical Training, Inventory Management, Freight Conversions) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | GE Aviation, Lockheed Martin, Rockwell Collins, Airbus, Rolls Royce, Mitsubishi Aircraft Corporation, Thales Group, Boeing, British Aerospace, Northrop Grumman, Bombardier |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |