Quick Navigation

Report Overview

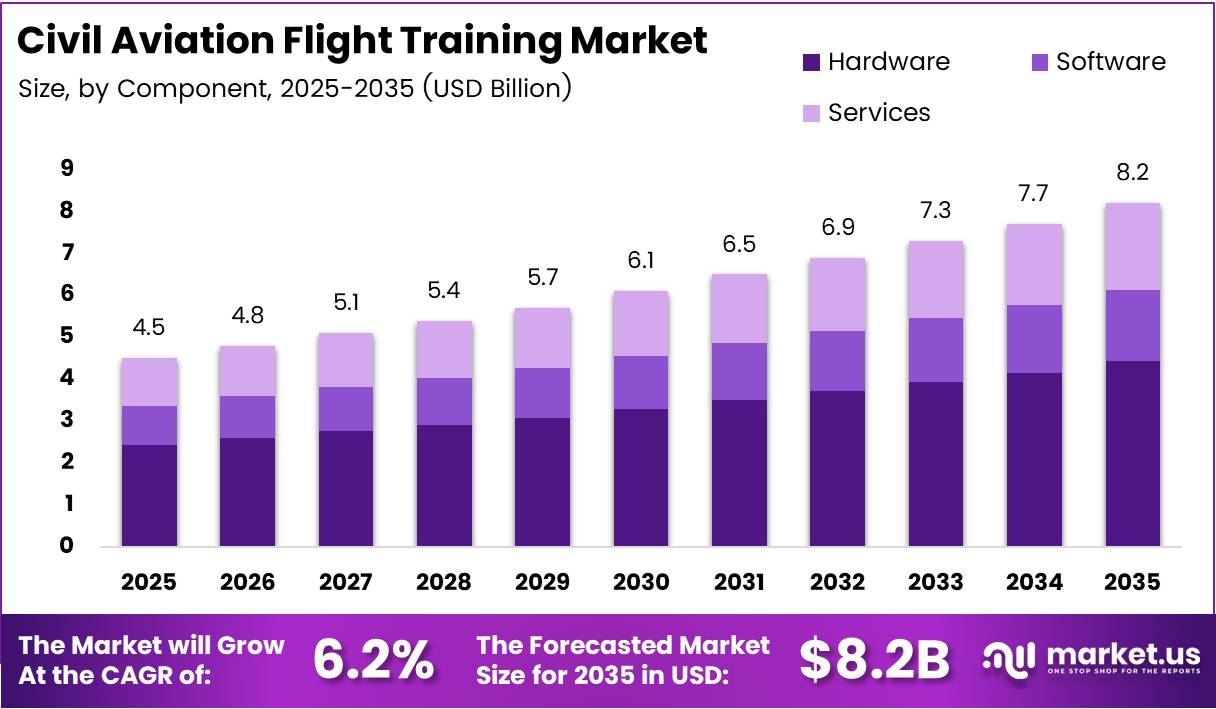

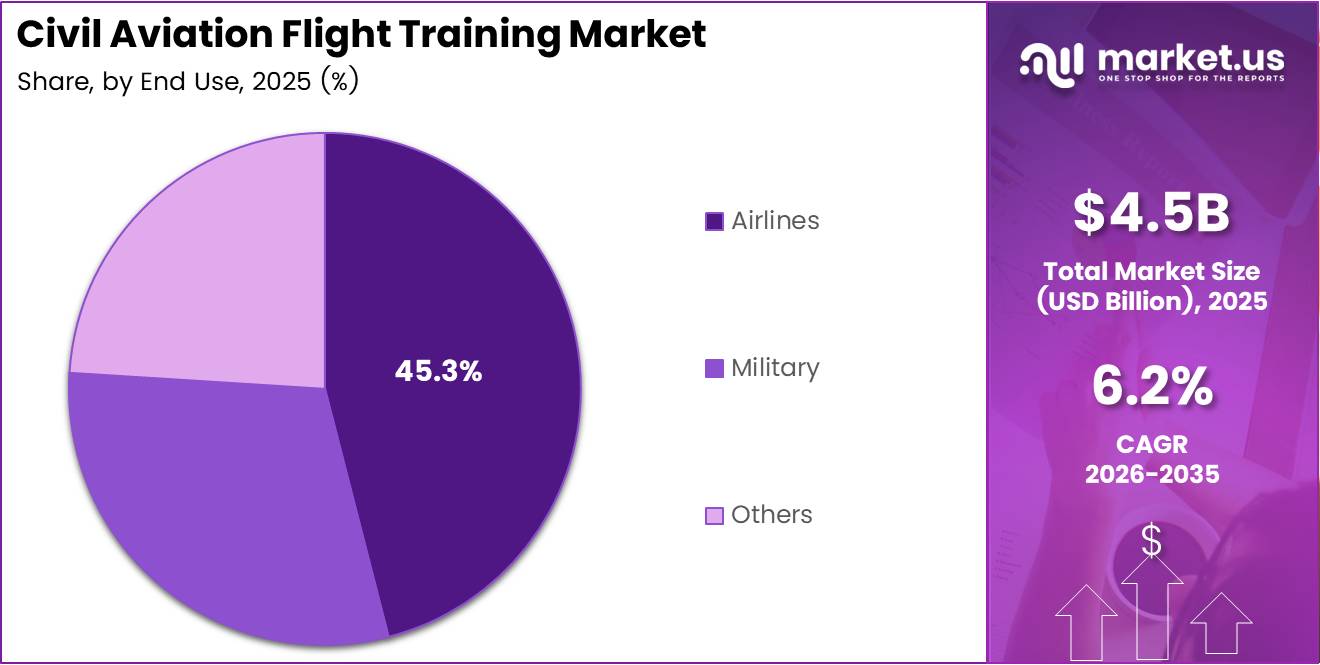

Global Civil Aviation Flight Training Market size is expected to be worth around USD 8.2 Billion by 2035 from USD 4.5 Billion in 2025, growing at a CAGR of 6.2% during the forecast period 2026 to 2035.

The civil aviation flight training market covers the full spectrum of structured instruction, simulation-based learning, and certification programs that prepare commercial pilots, cabin crew, maintenance engineers, and air traffic controllers for active service. Airlines, independent academies, and defense operators all rely on this ecosystem to maintain safety compliance and operational readiness.

Hardware components — including full flight simulators and flight training devices — anchor the market, accounting for 53.8% of total revenue. This reflects a structural preference among airlines and training academies for capital-intensive, regulation-compliant simulation infrastructure over software-only alternatives, where regulatory credit hours remain the dominant procurement trigger.

Pilot training commands the largest share of training-type activity at 58.2%. This concentration signals that airlines treat pilot certification as a non-negotiable compliance cost rather than a discretionary investment, making it the most insulated segment against budget pressure during economic downturns.

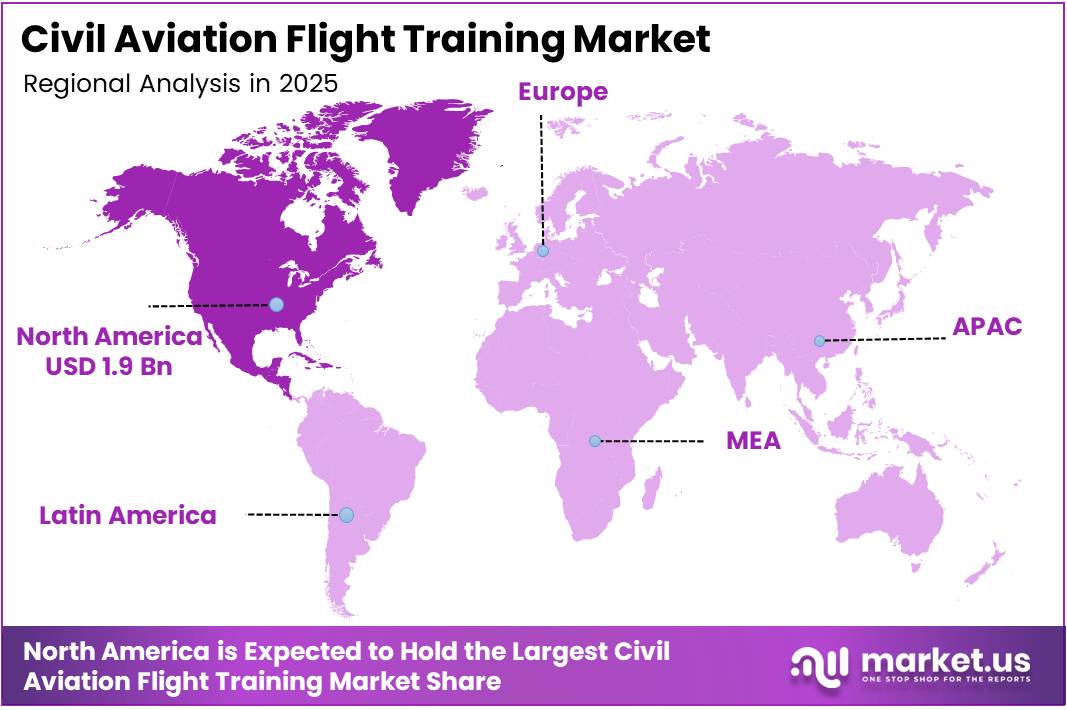

North America leads all regions with a 43.90% share, valued at approximately USD 1.9 Billion. Mature regulatory frameworks from the FAA, combined with the highest concentration of commercial airline hubs globally, have built deep procurement infrastructure that drives consistent capital allocation toward advanced simulation and recurrent training programs.

Fixed-wing aircraft training platforms account for 67.4% of platform-type activity. Commercial airline expansion in both established and emerging markets continues to center on narrow-body and wide-body jet operations, sustaining demand for fixed-wing simulator hours well above rotary or UAV training volumes.

According to aerotime.aero, the global estimate for new pilots needed between 2024 and 2043 rose from 649,000 to 674,000. This upward revision reflects accelerating fleet deliveries from Airbus and Boeing, meaning training academies and simulator operators face a structurally long demand runway — the capacity shortfall alone justifies significant new investment in training infrastructure.

According to pilotsacademy.co.in, simulator training costs USD 60–USD 150 per hour versus USD 150–USD 300+ for actual aircraft rental — representing a 50–80% cost reduction per training hour. This economic advantage accelerates institutional adoption of simulation-based programs, compressing the per-trainee cost curve and making large-scale pilot throughput financially viable for airlines managing tight margins.

Key Takeaways

- The Civil Aviation Flight Training Market was valued at USD 4.5 Billion in 2025 and is forecast to reach USD 8.2 Billion by 2035.

- The market advances at a CAGR of 6.2% over the forecast period 2026–2035.

- By Component, Hardware holds the dominant share at 53.8% of total market revenue.

- By Training Type, Pilot Training leads with a 58.2% share.

- By Training Device, Full Flight Simulators (FFS) account for the largest share at 37.8%.

- By Platform Type, Fixed-Wing Aircraft dominates with a 67.4% share.

- By End Use, Airlines hold the highest share at 45.3%.

- North America leads regional revenue with a 43.90% share, valued at USD 1.9 Billion.

Product Analysis

Hardware dominates with 53.8% due to high simulator capital investment requirements.

In 2025, Hardware held a dominant market position in the By Component segment of the Civil Aviation Flight Training Market, with a 53.8% share. Full flight simulators and flight training devices require substantial upfront procurement from airlines and academies, locking in long hardware replacement cycles that sustain consistent revenue above software and services segments.

Software serves as the integration layer that activates hardware performance across training programs. Scenario libraries, performance analytics engines, and regulatory-compliance modules drive software procurement decisions. As simulation fidelity requirements rise under updated FAA and EASA standards, airlines increasingly treat software upgrades as mandatory operational expenditure rather than optional enhancements.

Services carries a recurring revenue structure that differentiates it from hardware and software purchasing patterns. Maintenance contracts, instructor-led training delivery, and regulatory audit support create long-term client relationships for vendors. Service contracts typically renew annually, providing vendors with predictable income streams regardless of new hardware procurement cycles.

Training Type Analysis

Pilot Training dominates with 58.2% due to mandatory certification and recurrent compliance requirements.

In 2025, Pilot Training held a dominant market position in the By Training Type segment of the Civil Aviation Flight Training Market, with a 58.2% share. Regulatory mandates for initial type ratings, recurrent simulator checks, and route qualifications make pilot training a non-deferrable cost center for every commercial airline, insulating this segment from discretionary budget cuts.

Cabin Crew Training differentiates through safety-critical competency requirements set by aviation authorities globally. Emergency procedure drills, evacuation training, and first-aid certifications must be renewed at fixed intervals. Airlines cannot operate without fully certified cabin crew, making this segment structurally resilient even during capacity reduction periods.

Maintenance Crew Training addresses a distinct skills gap where errors carry direct aircraft-on-ground consequences for operators. Advanced composite materials, next-generation avionics, and engine architecture changes require continuous retraining of licensed engineers. Airlines that delay maintenance crew upskilling face longer AOG cycles and rising compliance liability.

Air Traffic Control (ATC) Training operates under a tighter regulatory framework than any other segment, with national aviation authorities directly controlling curriculum and certification standards. ATC training demand links directly to airspace capacity expansion and new airport infrastructure investment, making it a leading indicator of broader civil aviation development in emerging markets.

Training Device Analysis

Full Flight Simulators (FFS) dominate with 37.8% due to FAA and EASA regulatory credit hour recognition.

In 2025, Full Flight Simulators (FFS) held a dominant market position in the By Training Device segment of the Civil Aviation Flight Training Market, with a 37.8% share. Airlines prioritize FFS procurement because Level C and Level D devices allow pilots to complete the majority of type-rating and recurrent training hours without live aircraft, directly reducing operational costs and scheduling pressure on active fleets.

Flight Training Devices (FTD) provide a cost-accessible alternative to full-motion simulators, particularly for ab initio and instrument rating training programs. FTDs carry lower acquisition and maintenance costs than FFS units, making them the preferred device category for independent academies and regional carriers operating under tighter capital budgets.

Fixed Base Simulators (FBS) serve procedure familiarization and systems knowledge training where motion is not required for regulatory credit. Their lower cost per training hour makes them effective tools for high-volume throughput in initial type rating programs, particularly in markets where academy capacity constraints limit full-motion device access.

Cockpit Procedures Trainers (CPT) focus exclusively on systems knowledge, normal and abnormal checklists, and cockpit resource management skills. CPTs do not generate regulatory flight hours but reduce full-motion simulator utilization time by front-loading procedural competency — improving overall training efficiency and reducing cost per qualified pilot output.

Virtual Reality (VR) Trainers represent the fastest-repositioning device category as EASA and FAA regulatory frameworks begin to recognize VR simulation hours for specific training tasks. Their deployment in maintenance crew training and cabin crew procedures is already demonstrating measurable time and cost advantages over conventional mock-up based instruction.

Computer-Based Training (CBT) delivers ground school, regulatory compliance, and systems knowledge content at scale across distributed learner populations. Airlines use CBT to standardize knowledge baselines across globally dispersed crew bases, reducing variability in trainee preparation before simulator sessions and lowering total training hours per qualification.

Platform Type Analysis

Fixed-Wing Aircraft dominates with 67.4% due to commercial airline fleet composition and volume.

In 2025, Fixed-Wing Aircraft held a dominant market position in the By Platform Type segment of the Civil Aviation Flight Training Market, with a 67.4% share. Commercial airline operations remain centered on narrow-body and wide-body jet platforms, creating sustained demand for type-specific simulator hours and recurrent training cycles that far exceed rotary-wing or UAV training volumes.

Rotary-Wing Aircraft training serves a structurally distinct buyer group, including offshore energy operators, emergency medical services, and military helicopter units. The complexity of rotorcraft systems and the limited transferability of fixed-wing skills to rotary operations maintain a dedicated, specialized training segment that commands premium pricing relative to fixed-wing equivalents.

Unmanned Aerial Vehicles (UAVs) represent the emerging platform segment where regulatory frameworks are still maturing across major jurisdictions. As commercial drone operations scale in logistics, surveillance, and cargo delivery, formal UAV operator certification programs are building a new demand base for structured training infrastructure, particularly in Asia-Pacific and the Middle East.

End Use Analysis

Airlines dominate with 45.3% due to mandatory recurrent training and fleet expansion requirements.

In 2025, Airlines held a dominant market position in the By End Use segment of the Civil Aviation Flight Training Market, with a 45.3% share. Airlines combine the highest volume of training mandates — initial type ratings, recurrent simulator checks, line checks, and crew resource management — with the largest institutional procurement budgets, making them the anchor customer base for every major simulator vendor and training academy globally.

Military end-use training operates under separate regulatory and procurement structures from commercial aviation, with defense budgets and national security priorities determining training investment levels. Military training programs prioritize mission-specific simulation fidelity, including combat scenario replication and adverse condition exposure, which commands higher per-hour training costs than commercial equivalents.

Others — including business aviation operators, charter carriers, and government civil aviation agencies — represent a fragmented buyer segment with growing procurement activity. Business aviation fleet growth and increasing regulatory alignment between business and commercial aviation standards are gradually expanding certified training requirements beyond the traditional airline buyer base.

Key Market Segments

By Component

- Hardware

- Software

- Services

By Training Type

- Pilot Training

- Cabin Crew Training

- Maintenance Crew Training

- Air Traffic Control (ATC) Training

By Training Device

- Full Flight Simulators (FFS)

- Flight Training Devices (FTD)

- Fixed Base Simulators (FBS)

- Cockpit Procedures Trainers (CPT)

- Virtual Reality (VR) Trainers

- Computer-Based Training (CBT)

By Platform Type

- Fixed-Wing Aircraft

- Rotary-Wing Aircraft

- Unmanned Aerial Vehicles (UAVs)

By End Use

- Airlines

- Military

- Others

Drivers

Global Pilot Shortage and Fleet Expansion Force Structural Growth in Aviation Training Programs

Airlines face an acute and quantified personnel gap that makes training investment non-negotiable. According to flightsimcoach.com, completing a full airline pilot training pathway from Private Pilot Certificate through Flight Instructor requires approximately 290 hours of flight time in the US, with cumulative training costs of approximately USD 75,000–USD 100,000. This cost and time burden means training academies must scale significantly to meet fleet-driven throughput requirements.

Rapid commercial airline fleet growth from Airbus and Boeing order backlogs places direct hiring pressure on airlines globally. Airlines cannot add aircraft without certified pilots on roster, which means fleet delivery schedules function as hard deadlines for training program output. This structural linkage between aircraft manufacturers and training academies creates a predictable, supply-constrained demand environment for simulator operators and academies.

Advanced flight simulation technologies have become the primary tool for managing this throughput challenge. Simulation-based training compresses qualification timelines, reduces aircraft availability dependency, and lowers per-hour training costs — making it the most financially rational path for airlines and academies scaling pilot output to meet fleet delivery schedules across high-growth markets.

Restraints

High Certification Costs and Salary Inflation Compress Training Economics for Pilots and Operators

The financial burden of pilot certification creates a structural access barrier that limits training throughput. Full pathway costs of USD 75,000–USD 100,000 per candidate screen out a significant portion of prospective trainees before program entry, particularly in markets without airline sponsorship or government subsidy programs. This supply-side constraint tightens the addressable trainee pool for academies.

According to aerotime.aero, First Officer and Captain median salaries in Europe increased by 27.58% and 49.46% respectively in 2024. While salary growth signals strong demand, it simultaneously inflates airline operating costs and reduces budget availability for additional training investment. Airlines balancing crew retention costs against training expenditure face tighter total compensation budget constraints.

Stringent aviation safety regulations extend training duration and add mandatory certification steps that increase total cost and time-to-qualification. Regulatory processes set by FAA, EASA, and national civil aviation authorities cannot be accelerated by market demand, meaning training throughput has a hard ceiling determined by compliance timelines — not commercial appetite or investment willingness.

Growth Factors

VR Technology Adoption and Emerging Market Investment Unlock New Training Revenue Streams

Virtual reality is shifting from experimental to operationally validated technology within aviation training. According to chevron-recruitment.com, Airbus VR training modules for landing gear replacement and engine overhauls cut training time by 25% and improved task accuracy by 40%. These measurable outcomes provide airlines and MRO operators with a documented business case for replacing mock-up-based training programs with VR alternatives at scale.

In November 2025, Leonardo Helicopters’ Virtual Extended Reality (VxR) training system received EASA FTD Level 3 certification — becoming the first VR-based training solution to hold both FAA FTD Level 7 and EASA FTD Level 3 approvals simultaneously. This dual certification means VR simulation time now formally counts toward official pilot flight training hours, removing the primary regulatory barrier to widespread VR adoption across commercial and military training programs.

Airline-led expansion of proprietary training academies — including programs developed by Boeing and Airbus — alongside rising investment in regional flight training centers across Asia-Pacific, the Middle East, and Latin America creates new geographic markets for simulator vendors and training technology providers. These investments signal a structural shift toward vertically integrated training delivery that increases total addressable market size.

Emerging Trends

AI-Driven Analytics and Certified VR Devices Redefine the Economics of Pilot Skill Development

Full flight simulators now function as data generation platforms, not just training environments. AI-driven performance analytics tools process trainee behavioral data to identify skill gaps, flag fatigue patterns, and personalize training sequences — shifting simulator sessions from standardized exercises toward adaptive, outcome-optimized programs. This capability improvement directly reduces total simulator hours needed per qualification.

According to chevron-recruitment.com, VR/AR-trained engineers complete maintenance tasks 25–38% faster than conventionally trained peers. Knowledge retention after VR training reaches approximately 75–80%, compared to 30–50% via traditional lectures, and error rates drop by 50% or more when trainees complete VR modules before live tasks. These performance differentials give training operators a quantifiable ROI argument for VR capital investment.

In June 2025, Brunner’s NOVASIM MR DA42 received EASA certification as the first-ever mixed reality-based flight training device, with multiple VR and XR simulators now officially EASA- and FAA-qualified for creditable pilot training hours. This regulatory acceptance removes the final structural obstacle to scaling mixed reality training programs, opening a new device category that competes directly with conventional FTD procurement budgets.

Regional Analysis

North America Dominates the Civil Aviation Flight Training Market with a Market Share of 43.90%, Valued at USD 1.9 Billion

North America commands a 43.90% market share, valued at USD 1.9 Billion, driven by the FAA’s rigorous recurrent training mandates, the highest concentration of commercial airline hubs globally, and deep capital markets that sustain large-scale simulator procurement. The region sets regulatory benchmarks that directly influence training standards across all other markets.

Europe Civil Aviation Flight Training Market Trends

Europe maintains a strong second position underpinned by EASA’s unified regulatory framework, which standardizes training requirements across member states and drives consistent simulator investment. The region’s dense aviation network and established MRO sector generate steady demand for maintenance crew and pilot recurrent training programs, with First Officer and Captain salary increases in 2024 reflecting active crew demand across European carriers.

Asia Pacific Civil Aviation Flight Training Market Trends

Asia-Pacific represents the highest-growth regional opportunity, with an estimated structural pilot gap of approximately 371,000 by 2043 according to aerotime.aero. Rapid fleet additions by carriers across China, India, and Southeast Asia are outpacing domestic training capacity, driving airline-led investments in new simulator facilities and partnerships with international training academies.

Middle East and Africa Civil Aviation Flight Training Market Trends

The Middle East continues to face a structural pilot shortage even as global supply projections improve, according to Oliver Wyman’s Q4 2025 Flight Operations Trends report. Gulf carrier expansion programs and new airport infrastructure investments sustain strong demand for pilot and cabin crew training, while Africa’s nascent aviation sector is beginning to attract regional training center investment.

Latin America Civil Aviation Flight Training Market Trends

Latin America represents an emerging investment destination for regional flight training infrastructure, with airline network expansion in Brazil and Mexico creating localized demand for simulator capacity and pilot throughput programs. The region’s training market remains underdeveloped relative to its fleet growth trajectory, creating a supply gap that international training operators and simulator vendors are beginning to address.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

CAE Inc. occupies a structurally advantaged position as the world’s largest independent civil aviation training network, combining simulator manufacturing with academy operations. This vertical integration allows CAE to control both device utilization economics and trainee throughput, generating recurring revenue from simulator lease agreements and training contracts that competitors reliant on hardware sales alone cannot replicate.

FlightSafety International Inc. builds its competitive position around proprietary simulator technology paired with owned learning centers, creating a closed-loop training environment that keeps data, intellectual property, and client relationships within a single organization. This integration strategy reduces customer dependence on third-party academies, making FlightSafety the preferred partner for airlines seeking standardized, auditable training delivery across multiple aircraft types.

L3Harris Technologies approaches aviation training from a defense-adjacent technology base, differentiating through advanced simulation systems that serve both military and civil aviation markets. This dual-market capability gives L3Harris resilience against civil aviation cycle downturns, as defense training budgets operate on separate procurement timelines unaffected by commercial airline financial pressures.

The Boeing Company leverages its original equipment manufacturer relationship with airline customers to position Boeing Global Services as the natural training partner for Boeing-fleet operators. OEM-delivered training programs carry regulatory credibility that independent academies struggle to match for type-specific simulator instruction, giving Boeing a durable procurement advantage tied directly to fleet delivery volume.

Key Players

- CAE Inc.

- FlightSafety International Inc.

- L3Harris Technologies

- The Boeing Company

- Thales Group

- Frasca International Inc.

- Lufthansa Aviation Training GmbH

- Pan Am Flight Academy

- Skyborne Airline Academy

- Epic Flight Academy

- Phoenix East Aviation

- Revv Aviation

- Del Sol Aviation

Recent Developments

- November 2025 — Adani Defence & Aerospace, through subsidiary ADSTL and Horizon Aero Solutions Ltd., acquired a 72.8% majority stake in Flight Simulation Technique Centre Pvt. Ltd. (FSTC), India’s largest independent pilot flight training organization, at an enterprise value of INR 820 crore. FSTC operates 11 advanced full-flight simulators and 17 training aircraft across four certified centers in Gurugram, Hyderabad, Bhiwani, and Narnaul.

- December 2025 — Adani Enterprises completed the first phase of the FSTC acquisition, securing a 39% effective shareholding on December 30, 2025, with the remaining 33.8% stake acquisition planned for January 2026. FSTC generated INR 195 crore in revenue in FY 2024–25, confirming the asset’s commercial scale and positioning Adani as a major force in India’s civil aviation training infrastructure.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.5 Billion |

| Forecast Revenue (2035) | USD 8.2 Billion |

| CAGR (2026-2035) | 6.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Hardware, Software, Services), By Training Type (Pilot Training, Cabin Crew Training, Maintenance Crew Training, Air Traffic Control (ATC) Training), By Training Device (Full Flight Simulators (FFS), Flight Training Devices (FTD), Fixed Base Simulators (FBS), Cockpit Procedures Trainers (CPT), Virtual Reality (VR) Trainers, Computer-Based Training (CBT)), By Platform Type (Fixed-Wing Aircraft, Rotary-Wing Aircraft, Unmanned Aerial Vehicles (UAVs)), By End Use (Airlines, Military, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | CAE Inc., FlightSafety International Inc., L3Harris Technologies, The Boeing Company, Thales Group, Frasca International Inc., Lufthansa Aviation Training GmbH, Pan Am Flight Academy, Skyborne Airline Academy, Epic Flight Academy, Phoenix East Aviation, Revv Aviation, Del Sol Aviation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |