Quick Navigation

Report Overview

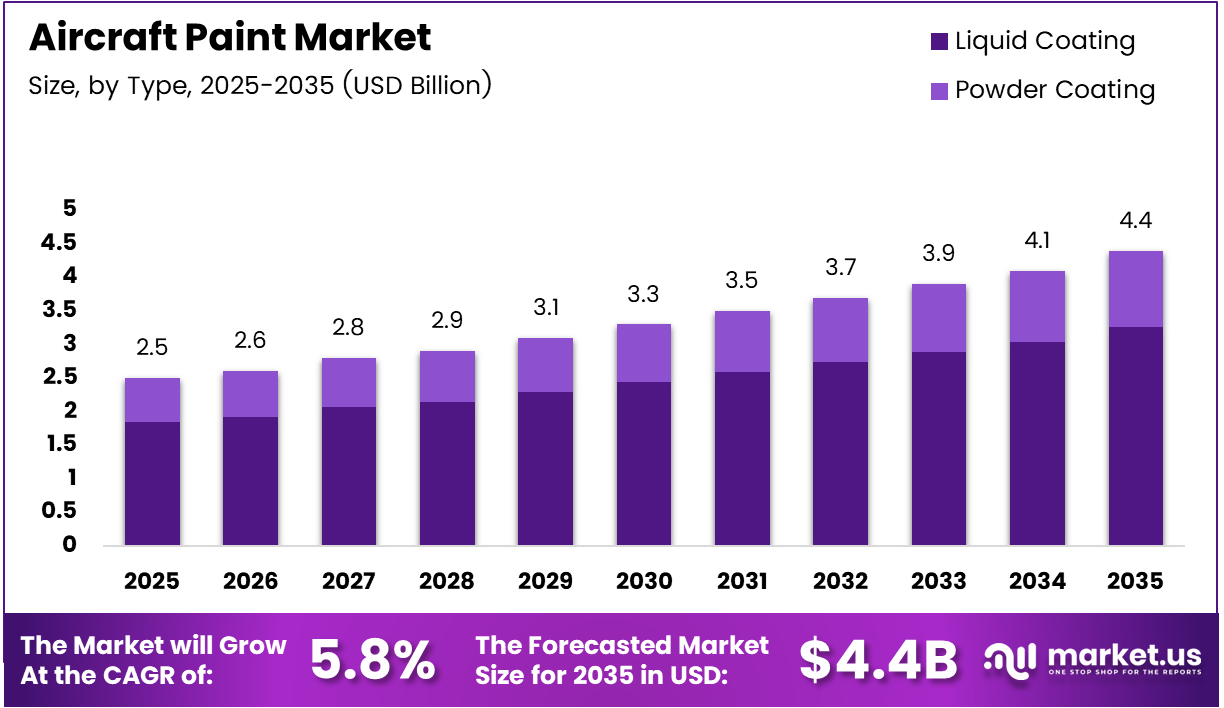

Global Aircraft Paint Market size is expected to be worth around USD 4.4 Billion by 2035 from USD 2.5 Billion in 2025, growing at a CAGR of 5.8% during the forecast period 2026 to 2035.

The aircraft paint market covers specialized coating systems applied to commercial, military, and general aviation aircraft — including exterior protection coatings, interior finishes, and corrosion-resistant formulations. These products serve both original equipment manufacturers and maintenance facilities. The breadth of end-use applications means demand tracks closely with global fleet activity and airline financial health.

Commercial aviation drives the majority of coating volume, as airline operators repainting aircraft every 5 to 7 years create a predictable, recurring demand base. This cycle-driven demand insulates the market from single-event disruptions and gives coating suppliers a relatively stable revenue floor, even when new aircraft deliveries slow. MRO operators, not OEMs, capture most of this recurring volume.

Fleet expansion across Asia Pacific and the Middle East adds a structural growth layer on top of the maintenance-driven base. Airlines in these regions are placing large narrow-body orders, each aircraft requiring full exterior and interior coating before delivery. This pipeline creates a forward revenue lock-in that benefits both paint manufacturers and applicators with long-term supply agreements.

Fuel efficiency has become a direct purchase criterion for aircraft coatings — a shift that changes competitive dynamics. In January 2025, easyJet became the first airline to trial a lower-weight paint system from Mankiewicz Aviation Coatings, achieving a 27 kg weight saving per Airbus A320 family aircraft. A fleet-wide rollout by 2030 is projected to deliver 1,296 tonnes of annual fuel savings and 4,068 tonnes of CO2 reduction per year — proof that paint selection now carries measurable financial and ESG weight for operators.

According to market data, liquid coatings hold a 73.6% share of the aircraft paint market by type. This dominance reflects the technical advantages of liquid systems in adhesion, color uniformity, and compatibility with complex airframe geometries — characteristics that powder coatings cannot yet match at scale for aerospace applications. For suppliers, this concentration signals that liquid coating chemistry will remain the primary R&D and commercial battleground through the forecast period.

According to market data, MRO end-users account for 67.3% of total demand in the aircraft paint market. This share reveals that the market’s economic engine is not new aircraft production but the ongoing repaint and repair of existing fleets. For paint manufacturers, winning MRO contracts means securing high-frequency, lower-margin volume — but also the long-term relationships that lock in brand specifications across a fleet’s operating life.

Regulatory pressure on volatile organic compound emissions adds a cost and complexity layer that favors larger, well-capitalized formulators over smaller specialists. The U.S. EPA finalized amendments to National VOC Emission Standards for Aerosol Coatings in January 2025, updating reactivity limits and compliance requirements that directly affect aircraft paint formulation. Suppliers who cannot fund reformulation at pace risk losing approval status — effectively ceding market access to compliant competitors.

Key Takeaways

- The global Aircraft Paint Market was valued at USD 2.5 Billion in 2025 and is forecast to reach USD 4.4 Billion by 2035.

- The market advances at a CAGR of 5.8% over the forecast period 2026 to 2035.

- By Type, Liquid Coating leads with a 73.6% market share in 2025.

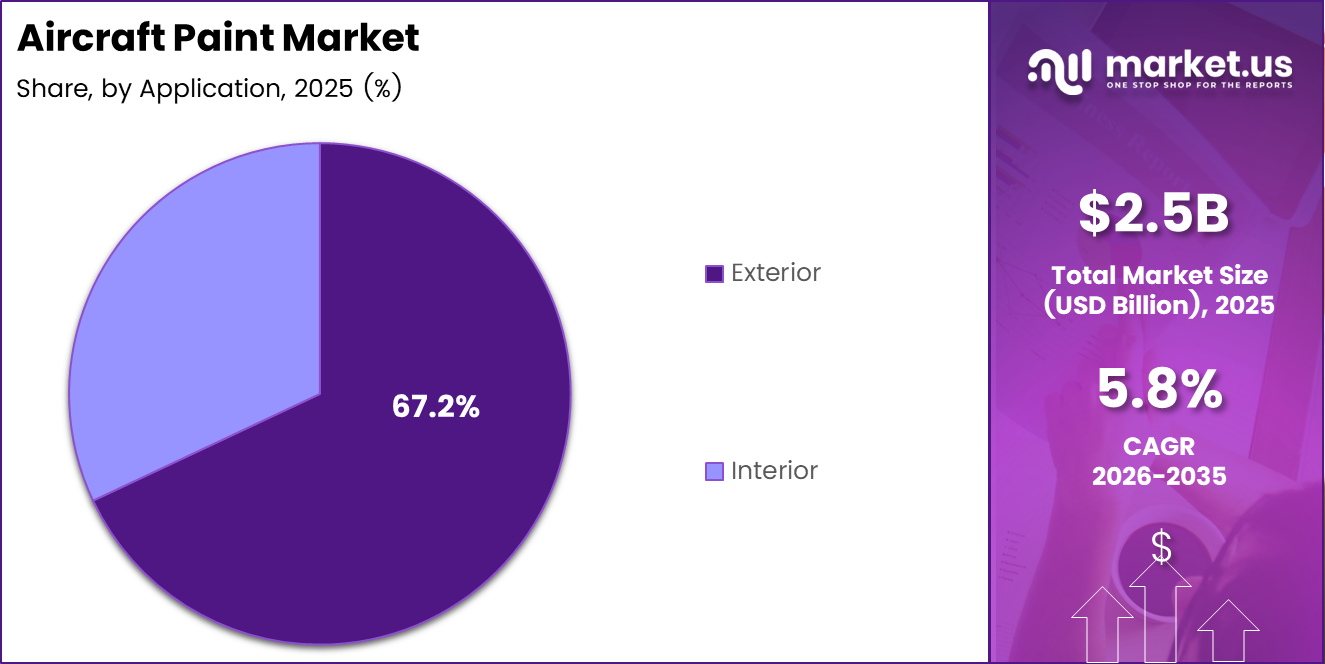

- By Application, Exterior coatings dominate with a 67.2% share.

- By Aircraft Type, Commercial Aviation holds the largest share at 59.1%.

- By End-User, MRO facilities account for 67.3% of total demand.

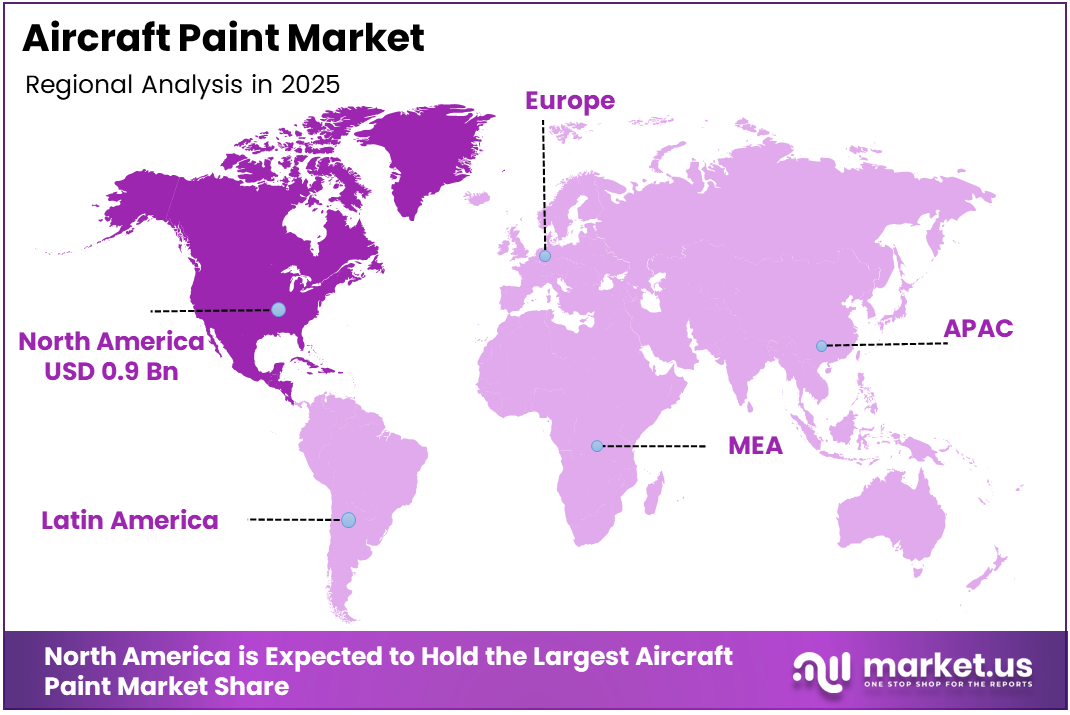

- North America leads regional markets with a 37.5% share, valued at USD 0.9 Billion.

Product Analysis

Liquid Coating dominates with 73.6% due to superior adhesion and airframe compatibility.

In 2025, Liquid Coating held a dominant market position in the By Type segment of the Aircraft Paint Market, with a 73.6% share. Liquid systems bond effectively to complex airframe geometries and deliver consistent color uniformity at scale — qualities that aerospace certification requirements demand. This technical baseline makes liquid coating the default specification across both OEM production lines and MRO facilities worldwide.

Powder Coating serves as an emerging alternative for select interior and structural components where electrostatic application is feasible. However, its inability to conform to large, curved exterior surfaces limits adoption in primary airframe applications. Powder coating’s relevance in aviation grows incrementally as formulators address temperature and flexibility constraints specific to aerospace substrates.

Application Analysis

Exterior dominates with 67.2% due to UV protection and brand livery requirements.

In 2025, Exterior coatings held a dominant market position in the By Application segment of the Aircraft Paint Market, with a 67.2% share. Exterior systems must withstand UV radiation, thermal cycling, moisture, and chemical exposure while maintaining airline livery aesthetics — a multi-performance requirement that commands premium pricing and frequent reapplication. This complexity sustains exterior coating volume even as fleet growth moderates.

Interior coatings address a distinct set of regulatory and performance criteria, including fire resistance, weight minimization, and passenger-facing finish quality. Demand for interior paint systems tracks cabin refurbishment cycles, which airlines accelerate during periods of competitive differentiation. Additionally, the push to reduce total aircraft weight places interior coating formulation under the same efficiency scrutiny as exterior systems.

Aircraft Type Analysis

Commercial Aviation dominates with 59.1% due to large fleet scale and regular repainting cycles.

In 2025, Commercial Aviation held a dominant market position in the By Aircraft Type segment of the Aircraft Paint Market, with a 59.1% share. Commercial fleets repaint aircraft every five to seven years as standard maintenance practice, generating a high-volume, recurring demand that no other aircraft category matches. This cycle predictability makes commercial aviation the anchor segment for coating suppliers planning production capacity and raw material procurement.

Narrow Body aircraft represent the highest-volume sub-segment within commercial aviation, driven by their dominance in short-to-medium haul networks globally. Airlines operating large narrow-body fleets — particularly A320 and 737 family operators — drive disproportionate coating consumption relative to unit count. Consequently, coating suppliers with approved narrow-body specifications hold a structural volume advantage.

Wide Body aircraft require significantly larger surface areas per unit, making each repaint a higher-value contract than narrow-body equivalents. Moreover, wide-body operators apply specialty coatings for long-haul durability and fuel efficiency, including drag-reducing riblet systems. In January 2025, Japan Airlines applied a sharkskin-inspired riblet coating to a Boeing 787-9, delivering a 0.24% drag reduction and saving an estimated 119 tonnes of fuel annually on the Narita–Frankfurt route.

Regional Jets serve point-to-point routes with high sector frequency, which accelerates surface wear and shortens repainting intervals relative to mainline aircraft. Therefore, coating durability and turnaround speed are the primary purchase criteria for regional operators. This segment rewards suppliers who offer fast-cure formulations compatible with tight MRO schedules.

Business Jets carry the highest per-unit coating value in the commercial segment, driven by extensive customization, premium finish standards, and operator willingness to pay for bespoke liveries. Additionally, business jet owners repaint more frequently than airlines — not always for wear, but for aesthetic refresh. This behavior makes the business jet segment a reliable high-margin niche for specialized paint applicators.

Military Aviation demands coatings with operational performance requirements — radar absorbency, infrared suppression, and extreme temperature resistance — that differ fundamentally from commercial specifications. Procurement cycles are longer and contract volumes are government-controlled, creating a stable but less price-responsive demand base. Consequently, military coating suppliers compete primarily on technical qualification rather than cost.

Fighter Jets use stealth and low-observable coatings that represent the highest technology and margin tier in the entire aircraft paint market. These coatings face stringent classification and export control requirements, concentrating supply among a small number of approved defense contractors. Moreover, the technical barrier to qualification effectively limits new entrant competition in this sub-segment.

Military Transport Aircraft require coatings optimized for durability in harsh operational environments — desert heat, arctic cold, and high-humidity tropics — often within a single aircraft’s deployment cycle. Coating performance in multi-climate conditions drives specification decisions more than unit cost. Therefore, suppliers with field-proven multi-environment formulations hold competitive advantage in this sub-segment.

Military Trainer Aircraft operate at very high annual flight hours, which accelerates surface coating wear faster than most other aircraft types. High utilization means more frequent repainting events per aircraft, creating above-average coating consumption relative to fleet size. This dynamic makes the trainer segment a volume-efficient target for MRO-focused paint suppliers.

Helicopters present a structurally distinct coating challenge due to rotor wash, vibration, and frequent low-altitude exposure to particulates and moisture. These operational conditions demand flexible, impact-resistant coating systems that fixed-wing formulations do not always satisfy. The helicopter segment therefore sustains a specialized coating niche with its own qualification and supply chain requirements.

Military Helicopters add operational camouflage and low-observable requirements on top of standard durability specifications, making them the higher-value sub-segment within the helicopter category. Defense budgets and multi-year procurement programs drive demand rather than commercial cycles, providing coating suppliers with long-term contract visibility once qualified.

Commercial Helicopters serve offshore energy, emergency medical, and executive transport sectors — each imposing distinct coating standards around corrosion resistance, visibility markings, and brand presentation. Offshore energy operators, in particular, drive demand for high-performance anti-corrosion systems due to persistent marine environment exposure. This segment benefits when energy sector capital spending expands.

End-User Analysis

MRO dominates with 67.3% due to high-frequency fleet repainting and repair demand.

In 2025, MRO held a dominant market position in the By End-User segment of the Aircraft Paint Market, with a 67.3% share. MRO facilities repaint aircraft across scheduled maintenance events, AOG repairs, and livery changes — generating a continuous, non-discretionary demand stream. For paint suppliers, MRO contracts represent recurring revenue that compounds with fleet age, making them strategically more valuable than single-delivery OEM orders.

OEM end-users apply coatings during new aircraft production, where specifications are locked in during design and rarely changed mid-program. Winning an OEM specification provides long-duration revenue visibility aligned with aircraft production rates, but volume is directly tied to manufacturer output cycles. Additionally, OEM paint requirements increasingly incorporate sustainability criteria — particularly low-VOC and lightweight formulations — which are reshaping supplier qualification standards.

Key Market Segments

By Type

- Liquid Coating

- Powder Coating

By Application

- Exterior

- Interior

By Aircraft Type

- Commercial Aviation

- Narrow Body

- Wide Body

- Regional Jets

- Business Jets

- Military Aviation

- Fighter Jets

- Military Transport Aircraft

- Military Trainer Aircraft

- Helicopters

- Military Helicopters

- Commercial Helicopters

By End-User

- MRO

- OEM

Drivers

Fleet Growth and Mandatory Repainting Cycles Sustain Structural Demand for Aircraft Coatings

Global fleet expansion directly increases the stock of aircraft requiring periodic repainting, creating a demand floor that grows with every new delivery. Airlines repaint aircraft on a fixed maintenance cycle, meaning larger fleets translate into more concurrent paint events at any point in time. This structural mechanic means coating demand rises even when new aircraft order intake temporarily slows.

Increasing aircraft maintenance and repainting cycles across commercial fleets compound this baseline. Exterior coatings degrade from UV exposure, thermal cycling, and abrasion — conditions that make repainting a non-discretionary maintenance event rather than a discretionary upgrade. According to market data, exterior applications account for 67.2% of total coating demand, confirming that repaint-driven volume, not new builds, anchors the market’s revenue base.

The adoption of lightweight coating materials adds a second commercial driver independent of fleet cycles. Airlines now evaluate paint weight as a direct fuel cost input, which elevates coating selection from a procurement function to an operations-level decision. This shift opens a higher-value product tier for suppliers who can quantify and certify weight and fuel savings — a qualification standard that increasingly gates access to major airline accounts.

Restraints

Environmental Compliance Costs and Specialty Material Pricing Constrain Market Participation

Regulatory pressure on chemical-based aircraft paint formulations represents a structural cost burden that disproportionately affects smaller suppliers. The U.S. EPA finalized amendments to the National VOC Emission Standards for Aerosol Coatings on January 6, 2025, updating coating category reactivity limits and compliance requirements that directly govern aircraft paint formulation. Suppliers unable to fund compliant reformulation risk losing regulatory approval — which is equivalent to losing market access.

The high cost of specialized aerospace coating materials creates a second constraint that limits competitive entry and compresses margins for mid-tier suppliers. Aerospace-grade resins, pigments, and adhesion promoters operate in a narrow approved-chemistry space, giving raw material suppliers pricing leverage over paint formulators. This input cost structure means that commodity pricing pressure from airline procurement teams cannot easily be absorbed without margin erosion.

Together, these constraints favor large, well-capitalized formulators who can spread compliance and R&D costs across global revenue bases. However, the same constraints slow the pace of innovation from smaller specialty players who historically introduced new coating chemistries to the market. Consequently, the regulatory and cost environment may reduce the diversity of coating solutions available to operators over the forecast period.

Growth Factors

Eco-Friendly Coating Development and MRO Expansion Create New Revenue Pools

The development of eco-friendly and low-VOC aircraft paint technologies responds directly to both regulatory mandates and airline sustainability commitments. Formulators who achieve compliant chemistries ahead of regulatory deadlines gain a certification head start that translates into preferred supplier status at airlines with public ESG commitments. In January 2026, ZIPAIR applied sharkskin riblet coating to its Boeing 787-8, with JAXA estimating savings of over 154 tonnes of fuel and approximately 492 tonnes of CO2 per aircraft annually — demonstrating that advanced coatings now deliver quantifiable sustainability value, not just regulatory compliance.

The expansion of MRO facilities globally, particularly across Asia Pacific and the Middle East, extends the geographic revenue base for paint suppliers. New MRO capacity requires qualified coating suppliers on-site or within close logistics range — creating regional supply partnerships that are difficult to dislodge once established. This geographic expansion therefore represents both a near-term volume opportunity and a long-term relationship asset for suppliers who enter new MRO markets early.

Increasing aircraft customization and airline branding requirements add a premium revenue layer to standard repaint contracts. Airlines invest in full-body liveries and special edition designs — as demonstrated when AkzoNobel applied 44 colors of its Aerodur 3001 coating system to a COMAC C919 for China Southern Airlines in November 2024. Custom livery work commands higher margins and faster reapplication cycles than standard white or base-color schemes, benefiting suppliers with broad color libraries and airline design partnerships.

Emerging Trends

Nano-Coating and Riblet Technologies Redefine Aircraft Paint as a Performance Asset

The adoption of nano-coating technologies marks a fundamental shift in how aircraft paint is specified and valued. Nano-coatings deliver enhanced surface hardness, hydrophobicity, and corrosion resistance at lower film weights than conventional systems — addressing durability, weight, and environmental performance in a single formulation. For operators, this convergence means coating selection decisions now carry measurable impact on maintenance cost and fuel economics simultaneously.

Riblet drag-reduction coatings represent the most commercially validated emerging technology in the sector. According to peer-reviewed research published in Science Direct, drag-reducing paint coatings with microscopically small riblet structures covering up to 70% of an aircraft’s surface achieve drag and fuel consumption reductions of up to 3%, with wind tunnel tests on wing profiles recording a 6.2% decrease in overall drag. For airlines operating hundreds of aircraft, this translates into fuel savings at a scale that justifies premium coating procurement.

The integration of advanced surface protection technologies — including corrosion-resistant systems and multi-layer protective coatings — responds to the aging of global commercial fleets. Older aircraft require more intensive surface protection to remain airworthy, which increases coating specification complexity and per-event revenue for qualified suppliers. Therefore, suppliers who develop certified multi-function coating systems — combining protection, weight reduction, and drag performance — hold the strongest competitive position as fleet age rises across established aviation markets.

Regional Analysis

North America Dominates the Aircraft Paint Market with a Market Share of 37.5%, Valued at USD 0.9 Billion

North America leads the global aircraft paint market with a 37.5% share valued at USD 0.9 Billion, underpinned by the world’s largest commercial fleet base, major OEM production activity, and a dense MRO infrastructure. The U.S. regulatory framework — including EPA VOC standards updated in January 2025 — also drives faster adoption of compliant next-generation formulations, positioning the region as a technology adoption leader alongside its volume leadership.

Europe Aircraft Paint Market Trends

Europe combines Airbus OEM production demand with a mature MRO base across the UK, France, and Germany, creating balanced coating demand across both new-build and aftermarket channels. European airline sustainability targets accelerate low-VOC and lightweight coating adoption ahead of regulatory minimums. Moreover, the presence of specialized coating applicators and approved formulators in the region supports a competitive and technically advanced supply chain.

Asia Pacific Aircraft Paint Market Trends

Asia Pacific represents the fastest-expanding demand base, driven by record aircraft deliveries to Chinese, Indian, and Southeast Asian carriers building out their fleets. New MRO capacity additions across Malaysia, Singapore, and China create localized coating supply requirements that favor regional partnerships. The Satys Aircraft Painting and AIROD joint venture established in May 2025 specifically targets Asia Pacific MRO painting capacity — signaling that global suppliers recognize the region’s growing structural weight in total demand.

Middle East and Africa Aircraft Paint Market Trends

The Middle East concentrates demand around major hub carriers undertaking continuous fleet renewal and premium cabin refurbishment programs. Gulf airlines’ focus on brand differentiation supports higher-value livery and interior coating work alongside standard repaint contracts. Additionally, the region’s ambition to build domestic MRO capabilities will gradually shift coating procurement from export-dependent supply chains to locally qualified suppliers.

Latin America Aircraft Paint Market Trends

Latin America’s aircraft paint demand tracks the financial recovery of regional carriers, which has been uneven but directionally positive as passenger volumes return to pre-disruption levels. Brazil and Mexico host the region’s primary MRO facilities, concentrating coating procurement within a small number of large operators. Coating suppliers targeting Latin America benefit from establishing local distribution and technical support networks that reduce lead times for MRO facilities managing tight aircraft turnaround schedules.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

3M Co. approaches the aircraft coatings market through its materials science platform, combining adhesive films, surface protection tapes, and specialty coating technologies across both OEM and MRO channels. Its competitive strength lies in cross-portfolio integration — enabling aircraft operators to source multiple surface protection solutions from a single approved supplier. This breadth reduces customer switching costs and gives 3M a structural retention advantage over single-product coating specialists.

Axalta Coating Systems Ltd. positions itself in the aerospace segment through high-performance liquid coating systems engineered for durability and color consistency across large fleet repainting programs. Its investment in waterborne and low-VOC formulations directly addresses the regulatory trajectory set by the EPA’s January 2025 VOC amendments, enabling proactive compliance positioning. Axalta’s ability to align product development with regulatory timelines reduces qualification risk for airline customers managing fleet-wide repaint contracts.

BASF SE leverages its chemistry scale to develop advanced aerospace coating components, including corrosion inhibitors and functional additives that enhance base coat performance beyond what standalone paint formulators typically achieve. This upstream positioning allows BASF to participate in the value chain at the formulation input level — capturing margin regardless of which final paint brand an operator specifies. Moreover, BASF’s R&D investment in eco-efficient chemistries aligns with the market’s shift toward low-VOC and lightweight coating systems.

Chromalloy Gas Turbine LLC focuses its aerospace surface treatment capabilities on turbine and engine components — a technically demanding niche where coating performance directly affects engine efficiency and component life. This specialization creates a defensible position in high-temperature and high-stress coating applications that general aviation paint suppliers cannot address. Chromalloy’s engineering-led approach means its competitive differentiation rests on material qualification and performance data rather than pricing.

Key Players

- 3M Co.

- Axalta Coating Systems Ltd.

- BASF SE

- Chromalloy Gas Turbine LLC

- DuPont de Nemours Inc.

- Hentzen Coatings Inc.

- Hisco Inc.

- Linde Plc

- PPG Industries Inc.

- The Sherwin Williams Co.

- Walter Wurdack Inc.

Recent Developments

- December 2024 — Japan Airlines began deploying a new riblet-shaped, drag-reducing coating on its Boeing 787 fleet, a technology engineered to manage airflow and improve fuel efficiency across long-haul operations. This marked the beginning of large-scale commercial riblet coating adoption on a major carrier’s widebody fleet.

- May 2025 — PPG announced a USD 380 million investment to construct a new 198,000-square-foot aerospace coatings and sealants manufacturing facility in Shelby, North Carolina, with construction commencing in October 2025. The facility, expected to be completed in the first half of 2027, will employ more than 110 people and produce PPG’s full line of aerospace coatings and sealants.

- 2024 — AAL AG (Switzerland) acquired Egli Paint GmbH (Switzerland), a provider of high-performance coating, painting, and refinishing services for industrial equipment and aircraft. The acquisition aimed to bolster AAL AG’s aviation surface treatment capabilities and expand its European aerospace paint footprint.

- May 2025 — Satys Aircraft Painting and AIROD Sdn Bhd (Malaysia) established a joint venture to enhance aircraft exterior painting and finishing MRO capabilities in the Asia-Pacific region, with the agreement signed in Toulouse in the presence of Sarawak’s Premier. The partnership directly targets the fast-expanding MRO demand base across Southeast Asia.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.5 Billion |

| Forecast Revenue (2035) | USD 4.4 Billion |

| CAGR (2026-2035) | 5.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Liquid Coating, Powder Coating), By Application (Exterior, Interior), By Aircraft Type (Commercial Aviation, Regional Jets, Military Aviation, Helicopters), By End-User (MRO, OEM) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | 3M Co., Axalta Coating Systems Ltd., BASF SE, Chromalloy Gas Turbine LLC, DuPont de Nemours Inc., Hentzen Coatings Inc., Hisco Inc., Linde Plc, PPG Industries Inc., The Sherwin Williams Co., Walter Wurdack Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |