Quick Navigation

Report Overview

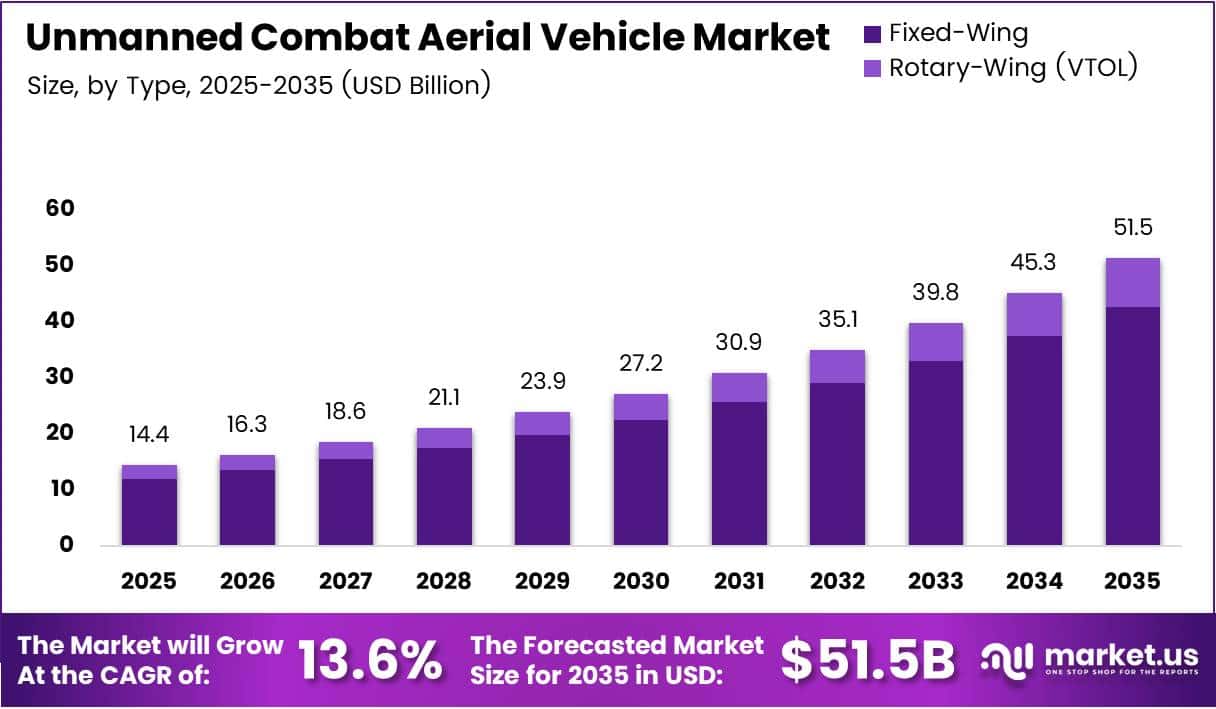

Global Unmanned Combat Aerial Vehicle Market size is expected to be worth around USD 51.5 Billion by 2035 from USD 14.4 Billion in 2025, growing at a CAGR of 13.6% during the forecast period 2026 to 2035.

The unmanned combat aerial vehicle market covers autonomous and remotely piloted aircraft designed for strike, reconnaissance, and electronic warfare missions. These platforms replace or supplement manned aircraft in high-risk environments where pilot safety, mission endurance, and per-sortie cost are critical constraints for defense planners.

Defense budgets across NATO members, Indo-Pacific nations, and Gulf states now allocate dedicated line items for UCAV procurement. This structural budget shift — from optional capability to required force multiplier — means procurement cycles are shortening and order volumes are climbing in tandem.

The 13.6% CAGR signals that military buyers are accelerating platform replacement faster than legacy procurement timelines anticipated. This creates a high-value window for established UCAV suppliers with certified platforms, while compressing the runway for newer entrants still in development stages.

Governments are investing in autonomous combat systems to reduce operational costs and minimize human casualties in contested airspace. The demand for intelligence, surveillance, and reconnaissance missions drives sustained procurement across conflict zones in Eastern Europe, the Middle East, and the South China Sea.

Fixed-wing configurations dominate UCAV design because they deliver superior range, altitude, and payload capacity over rotary alternatives. According to our market data, fixed-wing platforms hold an 82.8% share of the UCAV market by type — a dominance that reflects the fundamental physics of long-duration strike missions, where aerodynamic efficiency outweighs vertical takeoff flexibility.

Air forces command the largest share of UCAV end-users, holding 54.5% of total demand. This concentration confirms that UCAVs remain primarily an air-domain asset rather than a multi-service platform — though ground forces and naval commands are scaling procurement as doctrine evolves to incorporate drone-enabled combined arms operations.

Key Takeaways

- The global UCAV market is valued at USD 14.4 Billion in 2025 and is forecast to reach USD 51.5 Billion by 2035 at a CAGR of 13.6%.

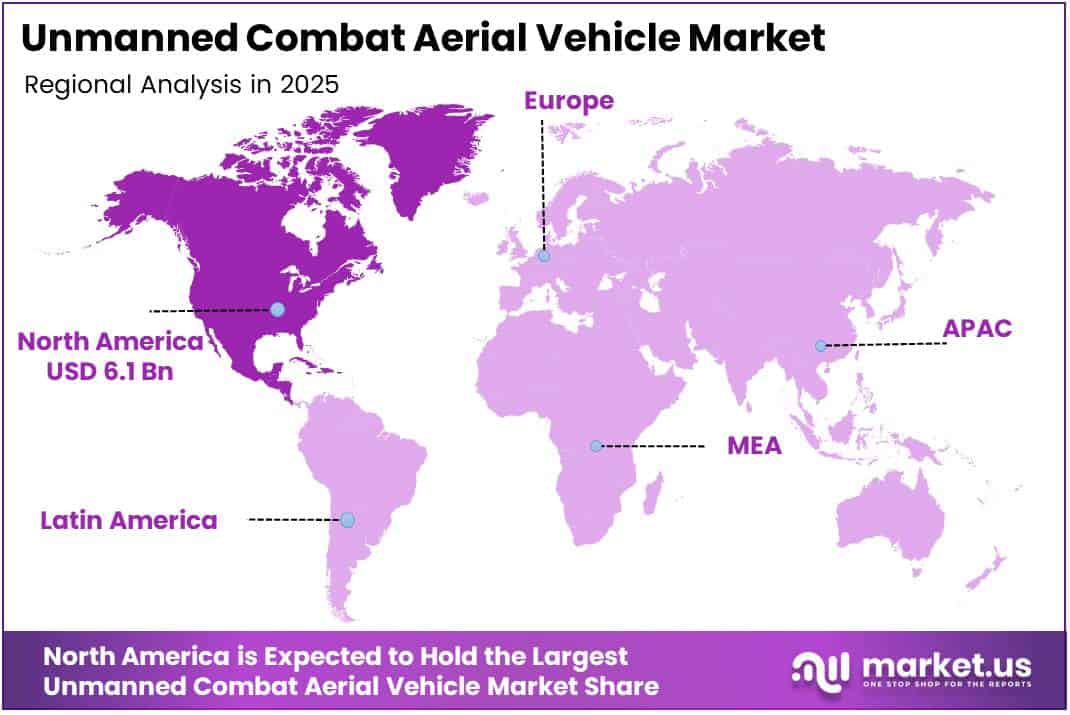

- North America leads all regions with a 42.30% market share, valued at USD 6.1 Billion in 2025.

- Fixed-Wing platforms dominate by type with an 82.8% share, reflecting the preference for long-range strike configurations.

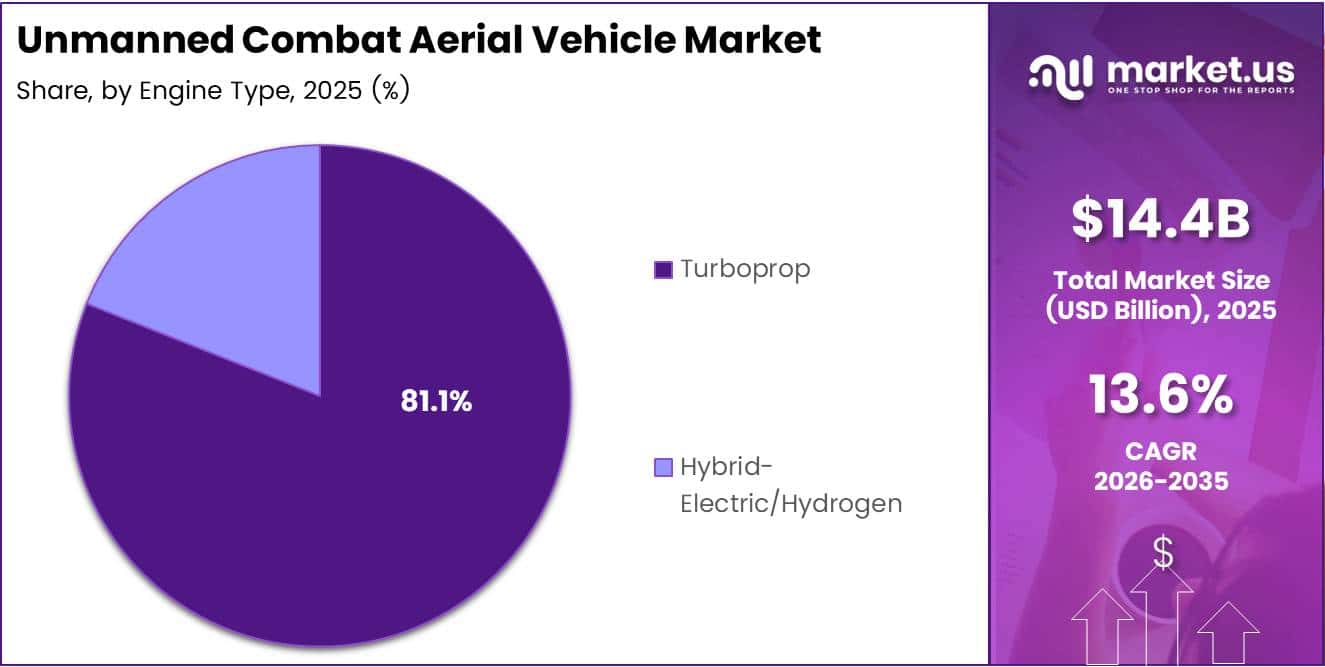

- Turboprop engine type leads with an 81.1% share, driven by its proven reliability in sustained combat operations.

- Long-Range platforms (greater than 1,000 km) hold a 56.2% share in the By Range segment.

- Above 30,000 ft altitude operation accounts for 67.3% of the By Altitude of Operation segment.

- Endurance platforms exceeding 24 hours hold 51.4% of the By Endurance segment.

- Air Force end-users represent 54.5% of demand, the largest share among all end-user categories.

Altitude of Operation Analysis

Above 30,000 ft platforms dominate with 67.3% due to strategic strike range and survivability.

In 2025, Above 30,000 ft platforms held a dominant market position in the By Altitude of Operation segment of the Unmanned Combat Aerial Vehicle Market, with a 67.3% share. High-altitude operation enables UCAVs to operate beyond most man-portable and short-range air defense systems, reducing interception risk while extending sensor coverage across wide operational theaters.

Below 30,000 ft platforms serve tactical and close-air-support roles where lower altitude enables precision engagement. These systems address shorter-range battlefield requirements and operate effectively in permissive or semi-permissive airspace. However, their exposure to medium-altitude air defense systems limits deployment in high-threat environments, constraining their share relative to high-altitude counterparts.

Range Analysis

Long-Range platforms dominate with 56.2% due to strategic deep-strike mission requirements.

In 2025, Long-Range platforms (greater than 1,000 km) held a dominant market position in the By Range segment of the Unmanned Combat Aerial Vehicle Market, with a 56.2% share. According to market data, this majority reflects a doctrine shift toward standoff engagement — militaries increasingly require UCAVs that can strike targets without exposing launch platforms to adversary air defenses. The Bayraktar TB2, with its 150 km operational range and fully automatic takeoff and landing capabilities, illustrates how even tactical platforms now push toward extended-range autonomous operation.

Medium-Range platforms (between 200 and 1,000 km) fill the operational gap between forward-deployed tactical drones and strategic long-range systems. These platforms suit theater-level reconnaissance and precision strike missions where strategic depth is required but full long-range capability is not. Their procurement is rising among mid-tier defense forces that cannot yet fund strategic UCAV programs.

Short-Range platforms (less than 200 km) serve frontline reconnaissance and direct fire-support roles. These systems carry lower unit costs and faster deployment timelines, making them accessible to a broader range of military buyers. However, their limited strike reach restricts their role to contested frontline environments rather than deep-penetration missions.

Endurance Analysis

More than 24 hours endurance dominates with 51.4% due to persistent surveillance and strike requirements.

In 2025, More than 24 hours endurance platforms held a dominant market position in the By Endurance segment of the Unmanned Combat Aerial Vehicle Market, with a 51.4% share. Extended endurance allows UCAVs to maintain persistent intelligence collection and loiter over targets without requiring refueling cycles — a capability that manned aircraft cannot match without crew rotation infrastructure.

6 to 24 hours endurance platforms represent the operational standard for medium-altitude long-endurance (MALE) UCAVs. These systems balance mission persistence with platform cost and ground support requirements. Most established UCAV programs in active procurement — including several used in current conflict zones — fall within this endurance bracket, making it a reliable revenue base for manufacturers.

Up to 6 hours endurance platforms address short-duration tactical missions including forward reconnaissance, artillery spotting, and close air support. Their lower acquisition cost and simpler logistics make them the entry point for armies building initial UCAV capability. However, their limited time-on-station narrows their value in sustained operational campaigns.

Type Analysis

Fixed-Wing dominates with 82.8% due to range, payload, and endurance advantages over rotary alternatives.

In 2025, Fixed-Wing UCAVs held a dominant market position in the By Type segment of the Unmanned Combat Aerial Vehicle Market, with an 82.8% share. Aerodynamic efficiency at cruise speed gives fixed-wing platforms decisive advantages in fuel consumption, altitude ceiling, and weapons payload — the three variables that determine mission utility in long-range strike and persistent surveillance operations.

Rotary-Wing (VTOL) platforms address operational requirements where runway independence is essential. These systems can deploy from forward operating bases, naval vessels, and confined terrain without fixed infrastructure. Consequently, their adoption is concentrated among special operations commands and naval forces where vertical takeoff and landing enables missions that fixed-wing platforms cannot perform.

Engine Type Analysis

Turboprop dominates with 81.1% due to proven performance in long-endurance combat missions.

In 2025, Turboprop engines held a dominant market position in the By Engine Type segment of the Unmanned Combat Aerial Vehicle Market, with an 81.1% share. Turboprop technology delivers the fuel efficiency, altitude performance, and reliability profile required for sustained combat operations — factors that procurement officers weight heavily when selecting platforms for multi-decade service lifecycles.

Hybrid-Electric/Hydrogen propulsion represents the next-generation alternative entering early procurement consideration. These systems promise reduced acoustic and thermal signatures alongside lower per-flight-hour operating costs. However, energy density limitations and immature supply chains mean hybrid and hydrogen platforms remain a development-stage category rather than a deployable operational one at scale.

End-User Analysis

Air Force dominates with 54.5% due to primary responsibility for air-domain strike and ISR missions.

In 2025, Air Force end-users held a dominant market position in the By End-User segment of the Unmanned Combat Aerial Vehicle Market, with a 54.5% share. Air forces control the doctrine, airspace, and procurement authority for strike and intelligence missions — placing them as the natural primary customer for combat-configured UAV platforms across all range and endurance classes.

Army (Ground Forces) procurement focuses on tactical UCAVs that provide organic fire support and reconnaissance without depending on air force allocation. Ground commanders use these platforms to reduce response time between target identification and engagement, a capability that conventional artillery and air-delivered ordnance cannot replicate at the same decision speed.

Navy/Marine Corps UCAV requirements center on maritime patrol, anti-ship reconnaissance, and carrier-launched strike missions. Naval platforms must meet additional durability standards for salt environment operation and deck-launch recovery — requirements that narrow the supplier pool and support premium pricing for maritime-certified UCAV systems.

Joint Special Operations Commands represent a specialized procurement stream focused on low-observable, high-precision platforms for direct action and personnel recovery missions. These buyers prioritize signature reduction and autonomous capability over raw endurance or payload capacity, driving demand for a distinct class of UCAV with different design requirements from conventional military platforms.

Key Market Segments

By Altitude of Operation

- Below 30,000 ft

- Above 30,000 ft

By Range

- Short-Range (Less than 200 km)

- Medium-Range (Between 200 and 1,000 km)

- Long-Range (Greater than 1,000 km)

By Endurance

- Up to 6 hours

- 6 to 24 hours

- More than 24 hours

By Type

- Fixed-Wing

- Rotary-Wing (VTOL)

By Engine Type

- Turboprop

- Hybrid-Electric/Hydrogen

By End-User

- Air Force

- Army (Ground Forces)

- Navy/Marine Corps

- Joint Special Operations Commands

Drivers

Defense Budget Shifts Toward Autonomous Strike Platforms Drive Sustained UCAV Procurement

Defense ministries across NATO, Gulf Cooperation Council states, and Indo-Pacific nations now allocate dedicated program lines for autonomous combat systems. This structural reallocation — away from manned aircraft upgrades and toward unmanned platforms — creates consistent multi-year procurement pipelines that reduce revenue volatility for UCAV manufacturers and prime contractors.

Intelligence, surveillance, and reconnaissance missions increasingly rely on UCAV platforms because they deliver persistent airborne coverage without aircrew fatigue or casualty risk. Border surveillance and counter-terrorism operations demand continuous overwatch across large geographic areas — a requirement that manned rotations cannot meet at the same cost per flight hour. According to market data, the turboprop engine segment commands an 81.1% share, confirming that buyers prioritize proven propulsion reliability over emerging alternatives when committing to operational programs.

Cost economics also drive the platform shift. A UCAV sortie eliminates ejection seat systems, life support equipment, crew training infrastructure, and casualty insurance liability — reducing per-mission costs substantially compared to manned equivalents. In April 2025, the Bayraktar TB2 set a Turkish aviation endurance record of 27 hours and 3 minutes in the tactical class and became the first UCAV to perform autonomous spin recovery, demonstrating that platform maturity now supports operational confidence at the highest military standards.

Restraints

Regulatory Uncertainty and Cybersecurity Exposure Constrain Full-Scale UCAV Deployment

Autonomous weapon systems face unresolved legal frameworks under international humanitarian law. The question of machine-attributed lethal decision-making creates compliance risk for procurement officers in democratic defense establishments, slowing approval timelines for fully autonomous UCAV configurations. Several NATO members require human-in-the-loop authorization for all lethal engagements — a constraint that limits the autonomous capability set available for deployment.

Electronic warfare and cybersecurity vulnerabilities create a structural ceiling on UCAV operational confidence. An adversary capable of jamming GPS navigation, spoofing command links, or intercepting sensor feeds can neutralize a platform costing tens of millions of dollars. This threat is not theoretical — it is documented in active conflict zones and shapes the risk calculus of procurement planners evaluating battlefield reliability.

The commercial success of export-dominant suppliers illustrates the tension. Baykar achieved USD 2.2 billion in UCAV exports in 2025, with 88% of revenue generated from exports — a concentration that signals strong international appetite but also highlights that domestic procurement processes in many markets remain slowed by regulatory and ethical review cycles that commercial export markets bypass.

Growth Factors

Military Modernization Programs and Advanced Capability Development Open New Revenue Streams

Emerging economies in Southeast Asia, South Asia, and Sub-Saharan Africa are accelerating military modernization with UCAV procurement as a centerpiece. These markets cannot afford the full-spectrum fighter aircraft programs that established powers operate. Consequently, they turn to combat drone platforms that deliver strike and ISR capability at a fraction of the lifecycle cost — expanding the UCAV addressable market beyond its traditional base of major defense spenders.

Swarm drone technology represents a structural expansion of the UCAV market rather than a product upgrade. Swarm operations multiply force-projection capacity without proportional increases in procurement cost — a math that appeals to defense planners facing budget constraints. According to market data, altitude performance is a key purchase criterion: the Above 30,000 ft segment holds 67.3% of the altitude-of-operation segment, indicating buyers prioritize platforms that operate above most air defense envelopes regardless of mission type.

Next-generation stealth combat drone development opens an entirely new product category above the current market. Low-observable UCAVs capable of penetrating integrated air defense systems address missions that current platforms cannot perform. Governments investing in these programs — including several fifth-generation aircraft programs now incorporating unmanned wingman concepts — will generate a sustained premium procurement tier above the existing MALE and tactical UCAV market.

Emerging Trends

AI-Enabled Autonomy and Loyal Wingman Concepts Reshape UCAV Mission Architecture

Artificial intelligence integration shifts UCAV capability from remote-controlled tools to semi-autonomous decision systems. AI-enabled target recognition, route adaptation, and threat response reduce the operator workload per platform — enabling single operators to manage multiple UCAVs simultaneously. This multiplier effect changes the force structure math that defense planners use to size drone fleets relative to manned aircraft squadrons.

The loyal wingman concept — pairing manned combat aircraft with unmanned counterparts that execute coordinated mission tasks — represents the most consequential doctrinal shift for UCAV vendors. Rather than replacing manned aircraft, UCAVs extend their lethality while absorbing attrition risk. According to market data, the TB2 surpassed 1 million cumulative flight hours as of December 2024, covering approximately 150 million kilometers — a real-world operational dataset that validates autonomous system reliability at scales previously undemonstrated.

Advanced sensor fusion and hypersonic-capable platform development define the next product generation. Sensor fusion integrates radar, electro-optical, infrared, and electronic intelligence feeds into a single targeting picture — reducing the time between detection and engagement. Hypersonic UCAV research, while still in development, signals that the combat drone category will expand upward into performance envelopes previously exclusive to manned aircraft and cruise missiles.

Regional Analysis

North America Dominates the Unmanned Combat Aerial Vehicle Market with a Market Share of 42.30%, Valued at USD 6.1 Billion

North America holds 42.30% of the global UCAV market, valued at USD 6.1 Billion in 2025. The United States Department of Defense drives this dominance through decades of sustained investment in autonomous combat systems, mature procurement infrastructure, and the operational track record that establishes program confidence. U.S. platforms set the capability benchmarks that other nations reference when structuring their own UCAV requirements.

Europe Unmanned Combat Aerial Vehicle Market Trends

Europe accelerates UCAV investment following the geopolitical realignments triggered by the Russia-Ukraine conflict. NATO member states raised defense spending targets, with autonomous strike and reconnaissance capabilities identified as priority gaps. Several European nations now fund domestic UCAV development programs — reducing dependence on U.S. platforms and creating new competition in the mid-tier combat drone market.

Asia Pacific Unmanned Combat Aerial Vehicle Market Trends

Asia Pacific represents the fastest-scaling UCAV procurement region outside North America. China’s domestically developed combat drone programs set regional capability benchmarks, while India, Australia, Japan, and South Korea accelerate procurement in response. Territorial disputes across the South China Sea and Taiwan Strait provide direct strategic justification for autonomous strike and persistent surveillance investment across the region.

Middle East and Africa Unmanned Combat Aerial Vehicle Market Trends

Middle East nations combine high defense budgets with active conflict experience — a combination that turns regional buyers into operationally validated UCAV customers rather than speculative procurers. Gulf states, in particular, have deployed combat drones in active theaters and now seek next-generation replacements with extended endurance and stealth characteristics, supporting sustained procurement demand.

Latin America Unmanned Combat Aerial Vehicle Market Trends

Latin America represents an emerging procurement tier driven by border security requirements, counter-narcotics operations, and general military capability modernization. Budget constraints limit access to premium long-range UCAV platforms, but the region shows consistent interest in tactical systems that deliver ISR capability without the full acquisition and operating cost of manned platforms.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

General Atomics anchors its market position on the MQ-9 Reaper and MQ-1C Gray Eagle platforms, which established the operational standard for MALE UCAV performance in active combat environments. Its sustained U.S. Department of Defense relationship provides program continuity that commercial competitors cannot replicate — creating a procurement moat that is difficult for new entrants to penetrate through price competition alone.

Northrop Grumman Corporation differentiates through stealth-capable UCAV development, most notably the X-47B carrier-based demonstrator and the RQ-4 Global Hawk ISR platform. Its positioning at the high-end, low-observable tier of the market places it ahead of the next capability threshold that major defense forces are now funding — giving it first-mover advantages as the stealth combat drone category opens for procurement.

Israel Aerospace Industries Ltd. leverages Israel’s operational combat environment as a live testing ground for UCAV systems. Platforms validated in active conflict carry significantly higher procurement confidence than laboratory-certified alternatives — a credibility advantage that IAI exploits in export markets across Europe, Asia, and the Americas, where defense buyers prioritize demonstrated reliability over specification sheets.

BAE Systems plc focuses its UCAV strategy on next-generation loyal wingman concepts and the Tempest sixth-generation program, positioning itself for the emerging combined manned-unmanned teaming market. In January 2026, Baykar was confirmed as the global UCAV export leader with USD 2.2 billion in exports representing 88% of its annual revenue — illustrating the commercial scale that export-focused UCAV specialists can achieve when platforms prove themselves in operational conditions.

Key players

- General Atomics

- Northrop Grumman Corporation

- Israel Aerospace Industries Ltd.

- BAE Systems plc

- China Aerospace Science and Technology Corporation

- Lockheed Martin Corporation

- BAYKAR A.S.

- The Boeing Company

- Elbit Systems Ltd.

- Kratos Defense & Security Solutions, Inc.

- BlueBird Aero Systems Ltd.

- Aviation Industry Corporation of China (AVIC)

- Turkish Aerospace Industries, Inc.

- AeroVironment, Inc.

- Saab AB

Recent Developments

- December 2024 — The Bayraktar TB2 UCAV surpassed 1 million cumulative flight hours, covering approximately 150 million kilometers. This milestone establishes the TB2 as the most operationally validated tactical UCAV platform in commercial history, providing a real-world reliability dataset that directly supports export procurement confidence.

- April 2025 — The Bayraktar TB2 set a Turkish aviation endurance record of 27 hours and 3 minutes in the tactical class and became the first UCAV to perform autonomous spin recovery. This achievement demonstrates that tactical-class platforms now match the endurance profile of MALE systems while adding autonomous recovery capability.

- November 2025 — The Edge–Anduril joint venture debuted the Omen UAV at the Dubai Airshow 2025 alongside three additional uncrewed systems, and announced a USD 7 billion deal with Republikorp to localize defense manufacturing in Indonesia. This deal signals that UCAV supply chain localization is becoming a strategic procurement condition in emerging defense markets.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 14.4 Billion |

| Forecast Revenue (2035) | USD 51.5 Billion |

| CAGR (2026-2035) | 13.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Altitude of Operation (Below 30,000 ft, Above 30,000 ft), By Range (Short-Range, Medium-Range, Long-Range), By Endurance (Up to 6 hours, 6 to 24 hours, More than 24 hours), By Type (Fixed-Wing, Rotary-Wing/VTOL), By Engine Type (Turboprop, Hybrid-Electric/Hydrogen), By End-User (Air Force, Army/Ground Forces, Navy/Marine Corps, Joint Special Operations Commands) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | General Atomics, Northrop Grumman Corporation, Israel Aerospace Industries Ltd., BAE Systems plc, China Aerospace Science and Technology Corporation, Lockheed Martin Corporation, BAYKAR A.S., The Boeing Company, Elbit Systems Ltd., Kratos Defense & Security Solutions Inc., BlueBird Aero Systems Ltd., Aviation Industry Corporation of China (AVIC), Turkish Aerospace Industries Inc., AeroVironment Inc., Saab AB |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |