Quick Navigation

Report Overview

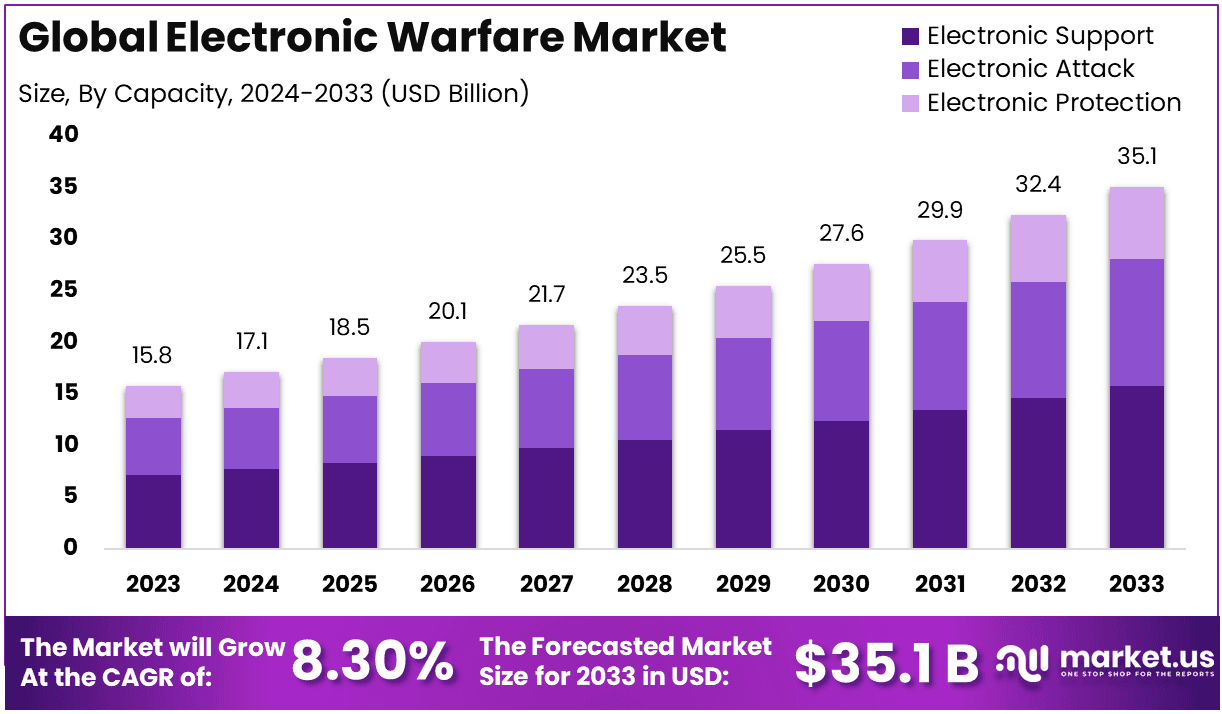

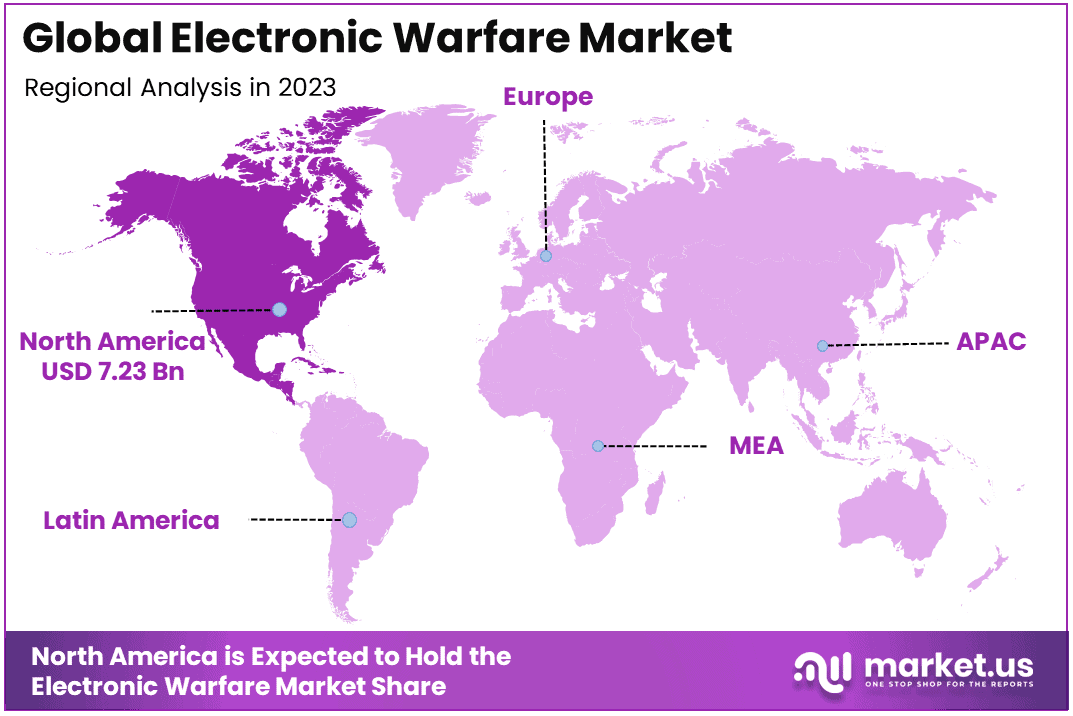

The Global Electronic Warfare Market size is expected to be worth around USD 35.1 Billion By 2033, from USD 15.8 Billion in 2023, growing at a CAGR of 8.30% during the forecast period from 2024 to 2033. In 2023, North America held a dominant position in the global Electronic Warfare (EW) market, capturing more than 45.8% of the total share and generating approximately USD 7.23 billion in revenue.

Electronic Warfare (EW) involves the strategic use of the electromagnetic spectrum to disrupt, intercept, and exploit enemy communications and radar systems while protecting friendly operations from similar threats. EW encompasses three key domains: electronic attack (EA), electronic protection (EP), and electronic support (ES). EA focuses on neutralizing enemy capabilities, EP ensures the safeguarding of friendly systems, and ES involves monitoring and analyzing electromagnetic signals for intelligence purposes. By controlling the electromagnetic environment, EW provides a tactical edge in modern military operations.

The Electronic Warfare market is growing rapidly as global defense organizations prioritize advanced systems to address modern threats. This growth is fueled by the need for sophisticated EW solutions across various domains such as airborne, naval, ground, and space platforms, ensuring adaptability and resilience in diverse operational environments.

Several factors are driving this growth. The evolving threat landscape, characterized by advanced electronic attacks, demands robust EW solutions. Military modernization programs worldwide aim to incorporate cutting-edge EW technologies, improving operational effectiveness. Rising defense budgets, particularly in emerging economies, enable the procurement of advanced EW systems, while continuous innovations in electronics enhance system efficiency and effectiveness.

Demand for EW systems is increasing due to their integration into modern military platforms and the necessity to address unconventional threats. Asymmetric warfare and cybersecurity concerns highlight the critical role of EW in protecting national and infrastructure security. Opportunities include the development of counter-drone systems, space-based EW capabilities for satellite defense, and the integration of artificial intelligence to enhance threat detection and response times.

Technological innovations are reshaping the EW landscape. Advancements in Digital Radio Frequency Memory (DRFM) improve radar deception, while directed energy weapons and high-energy lasers offer new electronic attack methods. Cognitive EW systems leverage AI and machine learning to adapt to rapidly changing threat environments, ensuring real-time decision-making and operational efficiency. These advancements underscore EW’s pivotal role in modern defense strategies.

Electronic Warfare (EW) plays a vital role in modern military strategy, leveraging the electromagnetic spectrum to detect, disrupt, and protect against enemy communications and radar systems. As of 2024, the United States allocated approximately $5 billion to EW initiatives, showcasing its strategic importance in national defense efforts. Globally, the electronic warfare market was valued at $14.14 billion in 2019, with estimates predicting it will grow to $17.88 billion by 2027. This reflects an increasing focus on developing advanced EW capabilities to address evolving threats.

Between 2021 and 2023, the United States dominated global EW spending, accounting for 45% of total investments, followed by Russia and China at 14% and 13%, respectively. These figures highlight the concentration of resources among military superpowers aiming to maintain superiority in the electromagnetic domain. Reports from the conflict in Ukraine further illustrate the operational significance of EW, with Russian jamming technologies rendering U.S.-supplied HIMARS rocket systems “completely ineffective” in certain scenarios, underlining the real-world impact of EW on battlefield dynamics.

Additionally, recent advancements in technology have improved the effectiveness of EW systems. For instance, the integration of Digital Radio Frequency Memory (DRFM) technology enhances radar deception capabilities, while directed energy weapons and AI-driven cognitive systems enable faster adaptation to evolving threats. These developments ensure that EW remains a critical and rapidly advancing component of defense strategies worldwide.

Key Takeaways

- The global Electronic Warfare market is poised for steady growth, rising from USD 15.8 billion in 2023 to an estimated USD 35.1 billion by 2033, at a CAGR of 8.3% over the forecast period.

- The Electronic Support segment dominated the market by capacity, contributing 45% of the total share in 2023, reflecting its critical role in signal detection, interception, and tactical intelligence operations.

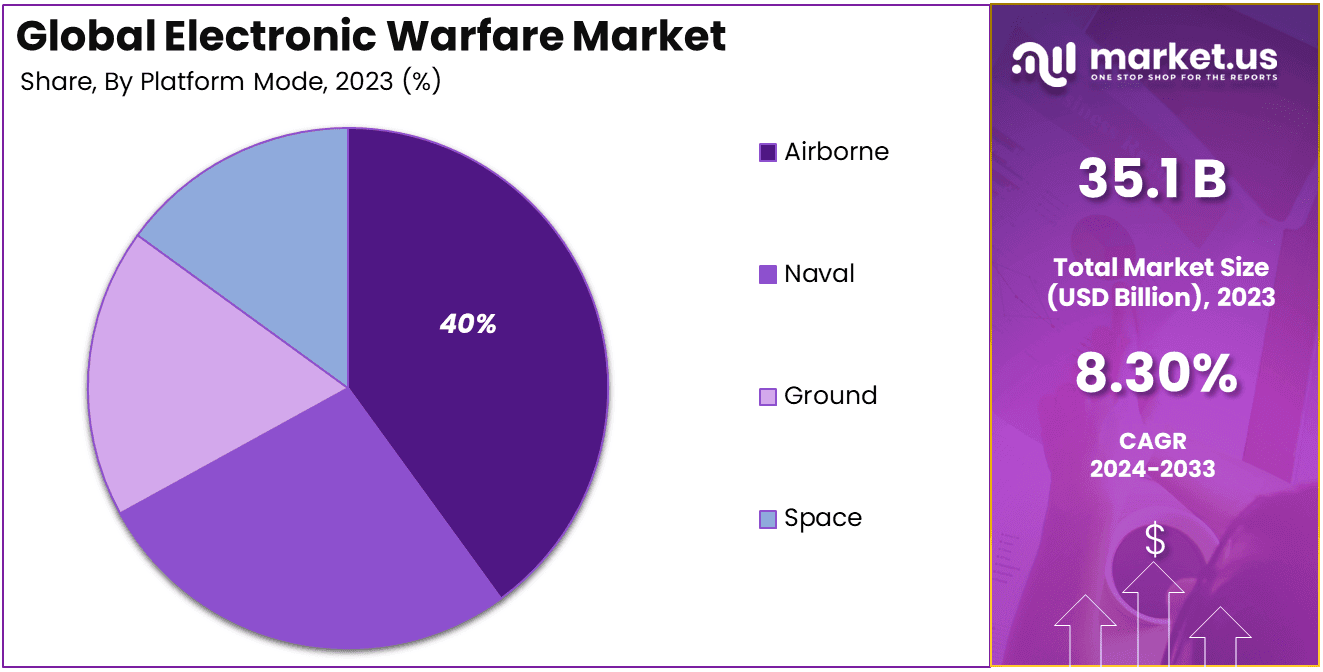

- The Airborne platform emerged as the leading application segment, accounting for 40% of the market share in 2023, driven by the increasing deployment of EW systems on aircraft for surveillance and defense missions.

- Jammer Systems stood out as a key product type, representing 32% of the market share in 2023, underscoring its essential function in disrupting enemy communications and radar systems.

- North America retained its position as the largest regional market, commanding 45.8% of the global share in 2023, supported by substantial defense budgets, cutting-edge technological innovations, and the presence of key EW solution providers.

By Capacity

In 2023, the Electronic Support (ES) segment held a dominant position in the Electronic Warfare market, capturing more than 45% of the market share. This segment’s leadership is attributed to its critical role in detecting, intercepting, and analyzing electromagnetic signals, providing essential intelligence for military operations. ES systems enable real-time situational awareness, helping armed forces identify and monitor potential threats, making them indispensable in both offensive and defensive strategies.

The dominance of the Electronic Support segment is further driven by its versatility across various platforms, including airborne, naval, and ground-based systems. These solutions are vital for identifying enemy radar and communication signals, and ensuring the effective deployment of countermeasures. Moreover, the increasing use of advanced technologies such as Artificial Intelligence (AI) and Machine Learning (ML) in ES systems has enhanced their ability to process large volumes of data, improving decision-making and operational efficiency.

While Electronic Attack (EA) and Electronic Protection (EP) are also significant, their functions are often dependent on the intelligence gathered by ES systems. EA focuses on neutralizing enemy capabilities, such as jamming or disabling radar, while EP safeguards friendly forces from electronic threats. However, without the signal intelligence and situational awareness provided by ES, the effectiveness of EA and EP is significantly reduced, underscoring the foundational role of the ES segment.

By Platform

In 2023, the Airborne segment held a dominant position in the Electronic Warfare market, capturing more than 40.0% of the total share. This leadership is primarily driven by the growing demand for electronic warfare systems integrated into aircraft, including fighter jets, unmanned aerial vehicles (UAVs), and surveillance planes. The airborne platform’s versatility and mobility allow for a wide range of applications, such as signal interception, jamming, and electronic intelligence, making it a vital asset for modern militaries.

The prominence of the airborne segment is also attributed to its critical role in long-range operations. Airborne systems can cover expansive areas, detecting and neutralizing threats far beyond ground or naval capabilities. This advantage is particularly crucial in addressing asymmetric threats, where rapid response and advanced surveillance are required. Additionally, the use of UAVs equipped with electronic warfare technologies has further expanded the scope of the airborne platform, providing cost-effective and efficient solutions for both combat and intelligence missions.

Compared to other platforms like Naval, Ground, and Space, the airborne segment stands out due to its adaptability and strategic importance. While naval and ground platforms are essential for localized and defensive operations, airborne systems provide unmatched operational reach and flexibility. Space-based platforms, though emerging, are still in their nascent stages and are limited in deployment due to high costs and technological constraints.

By Product Type

In 2023, the Jammer Systems in Electronic Warfare segment held a dominant position in the market, capturing more than 32% of the total share. This leadership is largely due to the critical role jammer systems play in disrupting and neutralizing enemy communications and radar systems. These systems are essential for tactical superiority, as they allow military forces to impede the operational effectiveness of adversaries by blocking or confusing their signals during combat scenarios.

The dominance of jammer systems is also driven by their wide applicability across multiple platforms, including airborne, naval, and ground systems. These systems are particularly valuable in creating electronic “denial zones,” preventing enemy forces from effectively using radar or communication devices. With the increasing complexity of modern warfare, where electronic and cyber threats are interlinked, the demand for advanced jammer systems continues to rise, as they provide a robust first line of defense in electronic warfare operations.

Compared to other product types such as Radar Warning Receivers (RWRs) and Directed Energy Weapons (DEWs), jammer systems have a broader range of deployment and versatility. While RWRs are critical for threat detection and DEWs are emerging technologies with promising applications, jammer systems are currently more widely adopted due to their proven effectiveness and ability to be deployed in active combat scenarios. Moreover, the relatively lower cost and ease of integration of jammer systems make them a preferred choice for many defense forces.

Key Market Segments

By Capacity

- Electronic Support

- Electronic Attack

- Electronic Protection

By Platform

- Airborne

- Naval

- Ground

- Space

By Product Type

- Jammer Systems in Electronic Warfare

- Radar Warning Receivers in Electronic Warfare

- Directed Energy Weapons in Electronic Warfare

- Others in Electronic Warfare

Driving Factors

Escalating Geopolitical Tensions and Modernization of Military Forces

The global Electronic Warfare (EW) market is significantly driven by escalating geopolitical tensions and the consequent modernization of military forces. Nations worldwide are increasingly investing in advanced EW systems to enhance their defense capabilities and maintain strategic superiority.

In regions such as the Asia-Pacific, territorial disputes and regional power dynamics have led countries like China and India to bolster their military expenditures, focusing on integrating sophisticated EW technologies into their defense arsenals. Similarly, NATO member states are upgrading their EW capabilities in response to perceived threats from adversarial nations.

The modernization efforts encompass the development and deployment of advanced EW systems, including electronic support measures, electronic attack systems, and electronic protection technologies. These systems are designed to detect, intercept, and neutralize potential threats, ensuring operational effectiveness in complex electromagnetic environments.

Furthermore, the increasing reliance on electronic systems in modern warfare necessitates robust EW capabilities to counteract potential electronic threats. This reliance underscores the critical role of EW in contemporary military strategies, driving continuous investments and advancements in the field.

Restraining Factors

High Development and Maintenance Costs

Despite the growing importance of Electronic Warfare systems, the market faces significant restraints due to the high development and maintenance costs associated with these advanced technologies.

Developing state-of-the-art EW systems requires substantial financial investments in research and development, skilled personnel, and specialized infrastructure. The complexity of these systems, which often involve cutting-edge technologies such as artificial intelligence and machine learning, further escalates the costs.

Additionally, the maintenance of EW systems is both costly and resource-intensive. Regular updates are necessary to address evolving threats and technological advancements, requiring continuous investment. For many countries, especially those with limited defense budgets, these financial demands pose a significant challenge, potentially hindering the widespread adoption and deployment of advanced EW systems.

Growth Opportunities

Integration of Artificial Intelligence in EW Systems

The integration of Artificial Intelligence (AI) into Electronic Warfare systems presents a substantial opportunity for market growth and innovation. AI enhances the capabilities of EW systems by enabling real-time data analysis, adaptive threat response, and predictive maintenance.

AI-driven EW systems can process vast amounts of data from various sources, identifying patterns and anomalies that may indicate potential threats. This capability allows for quicker and more accurate decision-making in complex and dynamic operational environments.

Moreover, AI enables EW systems to adapt to new and evolving threats autonomously, enhancing their effectiveness and resilience. The predictive maintenance facilitated by AI also reduces downtime and maintenance costs, improving the overall efficiency of EW operations.

The ongoing advancements in AI technology and its increasing integration into defense systems are expected to drive significant growth and innovation in the Electronic Warfare market, offering enhanced capabilities to military forces worldwide.

Challenging Factors

Rapid Technological Advancements and Obsolescence

One of the primary challenges in the Electronic Warfare market is the rapid pace of technological advancements, leading to the obsolescence of existing systems.

As new technologies emerge, EW systems must be continuously updated and upgraded to remain effective against evolving threats. This constant need for modernization requires substantial financial and logistical resources, posing a challenge for many defense organizations.

Additionally, the fast-paced technological landscape can lead to shortened lifecycles for EW systems, necessitating frequent replacements or upgrades. This situation creates a continuous cycle of development and deployment, challenging the sustainability and long-term planning of EW capabilities.

Addressing this challenge requires a strategic approach to system design, emphasizing modularity and scalability to accommodate future upgrades. It also necessitates ongoing investment in research and development to stay ahead of technological advancements and emerging threats.

Growth Factors

The Electronic Warfare (EW) market is experiencing significant growth, driven by several key factors. Firstly, escalating geopolitical tensions have led nations to invest heavily in advanced defense systems, including EW capabilities, to maintain strategic superiority. For instance, the United States allocated approximately $5 billion to electronic warfare initiatives in 2024, underscoring the strategic importance of EW in national defense.

Secondly, the rapid advancement of technology has resulted in more sophisticated electronic threats, necessitating the development of robust EW systems. The integration of Artificial Intelligence (AI) and machine learning into EW solutions has enhanced threat detection and response times, providing a competitive edge in modern warfare scenarios.

Additionally, the increasing reliance on electronic systems in military operations has amplified the need for effective EW measures to protect critical infrastructure and communication networks. This reliance underscores the critical role of EW in contemporary military strategies, driving continuous investments and advancements in the field.

Emerging Trends

Several emerging trends are shaping the future of the Electronic Warfare market. One notable trend is the development of counter-drone systems, as the proliferation of unmanned aerial vehicles (UAVs) has created a demand for EW systems capable of detecting and neutralizing drone threats. For example, during the conflict in Ukraine, electronic warfare tactics significantly affected military operations, with reports indicating that Russian jamming technology rendered U.S.-supplied HIMARS rocket systems “completely ineffective” in certain scenarios.

Another trend is the expansion of military operations into space, presenting opportunities for EW applications in satellite communications and navigation systems. The integration of AI in EW systems is also gaining traction, as it can enhance threat detection and response times, offering a competitive edge.

Furthermore, the development of high-energy lasers and microwave weapons provides new avenues for electronic attacks, while advancements in Digital Radio Frequency Memory (DRFM) technology have improved the ability to deceive enemy radar systems by generating false targets.

Business Benefits of Investing

Investing in Electronic Warfare capabilities offers several business benefits for defense contractors and technology firms. Firstly, it opens up new revenue streams, as governments worldwide are allocating substantial budgets to enhance their EW capabilities.

Secondly, companies that develop advanced EW solutions can establish themselves as leaders in a niche but rapidly growing market segment, gaining a competitive advantage. Additionally, the integration of cutting-edge technologies such as AI and machine learning into EW systems can lead to the development of innovative products, enhancing a company’s technological portfolio and market appeal.

Moreover, collaborating with military and government agencies on EW projects can strengthen business relationships and lead to long-term contracts, providing financial stability and growth opportunities. Overall, investing in Electronic Warfare capabilities aligns with the evolving needs of modern defense strategies, positioning businesses for sustained success in the defense sector.

Regional Analysis

In 2023, North America held a dominant position in the global Electronic Warfare (EW) market, capturing more than 45.8% of the total share and generating approximately USD 7.23 billion in revenue. This leadership is primarily driven by the United States, which is the largest spender on defense globally. The U.S. Department of Defense allocates substantial funding to the development and deployment of advanced EW systems, ensuring military superiority in complex and dynamic operational environments.

The region’s dominance is further bolstered by the presence of key EW solution providers, such as Raytheon Technologies, Northrop Grumman, and Lockheed Martin, which are headquartered in the U.S. These companies consistently innovate, introducing cutting-edge technologies like AI-enabled EW systems, directed energy weapons, and advanced radar jamming solutions. Additionally, robust investments in research and development (R&D) have allowed North America to stay at the forefront of technological advancements in EW.

Another contributing factor to North America’s leading position is its strategic focus on countering evolving threats. With rising geopolitical tensions and the increasing use of electronic systems in warfare, the region has prioritized the development of versatile EW capabilities that can operate across airborne, naval, ground, and space platforms. The U.S. military’s significant spending on programs like Next-Generation Jammer (NGJ) and integrated EW systems for the F-35 fighter jet underscores this commitment.

Moreover, partnerships between the public and private sectors play a pivotal role in strengthening North America’s EW capabilities. Collaborative efforts between the U.S. government, academic institutions, and private defense contractors have fostered a culture of innovation and rapid technological advancement. As a result, North America is expected to maintain its leadership in the Electronic Warfare market, driven by continuous investments, advanced infrastructure, and a proactive approach to addressing emerging threats.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

Lockheed Martin has been actively expanding its capabilities through strategic acquisitions and product developments. In August 2024, the company announced its acquisition of satellite products maker Terran Orbital for $450 million. This move aims to enhance Lockheed’s position in the satellite manufacturing sector, consolidating Terran as a supplier for Lockheed’s projects, particularly those with the U.S. Space Development Agency. Additionally, Lockheed Martin continues to innovate in electronic warfare by integrating advanced technologies into its existing platforms, ensuring they meet the evolving demands of modern defense strategies.

L3Harris has focused on refining its business portfolio to concentrate on core competencies. In April 2024, the company agreed to sell its antenna and related businesses to an affiliate of investment firm Kanders & Co. for $200 million. This divestiture includes $175 million in cash and a $25 million seller note, allowing L3Harris to streamline operations and invest in areas with higher growth potential. Furthermore, L3Harris has been developing advanced electronic warfare systems, such as the Viper Shield, which completed rigorous testing in July 2024, enhancing protection for F-16 pilots.

BAE Systems has been actively enhancing its electronic warfare expertise through strategic partnerships and cutting-edge product developments. In September 2023, the company, in collaboration with L3Harris Technologies, successfully delivered the first of 10 EC-37B Compass Call aircraft to the U.S. Air Force. This state-of-the-art platform marks a significant upgrade, advancing the Air Force’s 40-year legacy of employing electromagnetic attack systems to support U.S. and allied air, ground, and special operations missions. Furthermore, BAE Systems is focused on advancing its electronic warfare countermeasure technologies to safeguard U.S. Army combat vehicles, reaffirming its dedication to driving innovation in the defense sector.

Top Key Players in the Market

- Lockheed Martin Corporation

- L3Harris Technologies Inc.

- BAE Systems plc

- ASELSAN A.S.

- Northrop Grumman Corporation

- RTX Corporation

- IAI

- THALES

- Saab AB

- Leonardo S.p.A.

- Elbit Systems Ltd.

- HENSOLDT AG

- Other Key Players

Recent Developments

- In November 2024: A group of European countries announced a collaborative initiative aimed at advancing missile defense, electronic warfare, and various other military technologies. This partnership was spurred by increasing concerns over regional security, particularly due to the ongoing conflict in Ukraine and uncertainties about U.S. support for NATO operations. The European Defence Agency confirmed the participation of 18 nations in a series of joint programs, including a significant focus on electronic warfare capabilities.

- In September 2023: BAE Systems, in partnership with L3Harris Technologies, delivered the first of 10 EC-37B Compass Call aircraft to the U.S. Air Force. These advanced systems represent a major step forward in electromagnetic attack capabilities, continuing the Air Force’s four-decade-long mission to employ electronic warfare tools for air, surface, and special operations missions. This delivery marked the beginning of combined developmental and operational testing for these next-generation aircraft.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 15.8 Bn |

| Forecast Revenue (2033) | USD 35.1 Bn |

| CAGR (2024-2033) | 8.30% |

| Largest Market | North America |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Capacity (Electronic Support, Electronic Attack, Electronic Protection), By Platform (Airborne, Naval, Ground, Space), By Product Type (Jammer Systems in Electronic Warfare, Radar Warning Receivers in Electronic Warfare, Directed Energy Weapons in Electronic Warfare, Others in Electronic Warfare) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Lockheed Martin Corporation, L3Harris Technologies Inc., BAE Systems plc, ASELSAN A.S., Northrop Grumman Corporation, RTX Corporation, IAI, THALES, Saab AB, Leonardo S.p.A., Elbit Systems Ltd., HENSOLDT AG, Other Key Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |