Quick Navigation

Report Overview

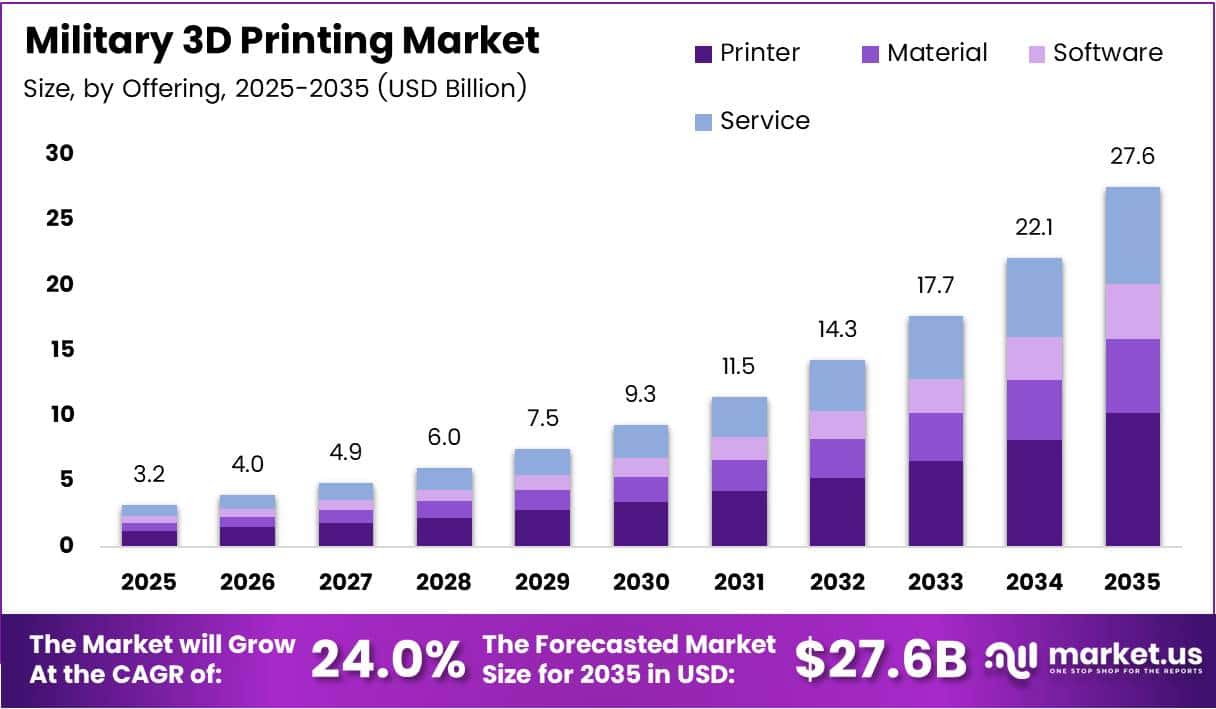

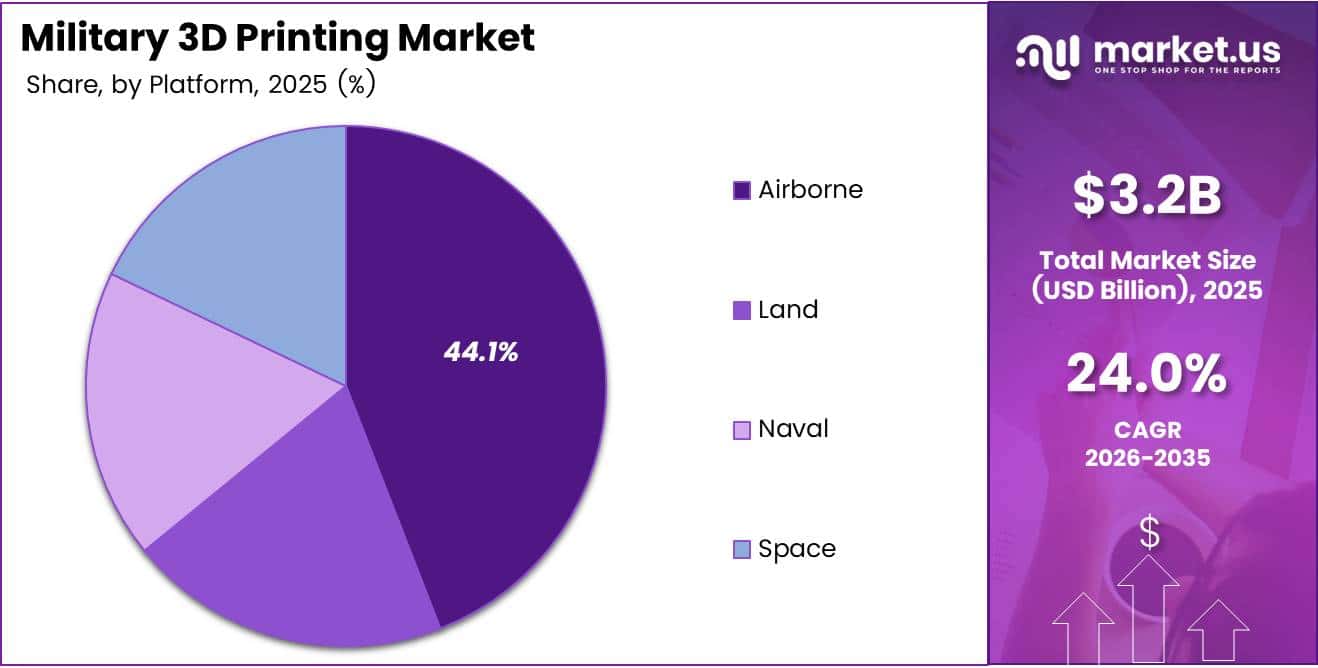

The Global Military 3D Printing Market size is expected to be worth around USD 27.6 Billion by 2035 from USD 3.2 Billion in 2025, growing at a CAGR of 24.0% during the forecast period 2026 to 2035.

Military additive manufacturing has moved beyond prototyping labs into active operational use. Defense forces now use 3D printing to produce functional components directly in combat-support environments, reducing dependence on centralized supply chains that were never built for speed or forward deployment.

The shift is structural, not incremental. Defense procurement cycles traditionally measured in months are giving way to on-demand part production measured in days. This compression creates real tactical advantage — units can restore equipment readiness faster, without waiting for parts to travel through multi-tier logistics networks.

Printer hardware leads adoption, while materials and software investment follows. The Printer segment holds 36.8% of the market, reflecting defense buyers prioritizing physical capability before fully standardizing feedstock and design workflows. This sequencing tells investors where the next wave of spending is heading.

Functional part manufacturing drives the application side, commanding 52.80% of demand. Defense agencies are not primarily buying 3D printing for concept modeling — they are using it to replace broken parts under operational pressure. This distinction matters because it positions military AM as a sustainment tool, not just an R&D investment.

In 2025, the U.S. Navy expanded additive manufacturing to frontline fleet operations, integrating AM components onto nuclear aircraft carriers and Virginia-class submarines. This formalized additive manufacturing as an operational warfighting capability, signaling that defense AM has passed the validation threshold and entered mainstream deployment.

According to NAVSEA, the U.S. Navy’s Southeast Regional Maintenance Center 3D-printed a six-blade cooling rotor for a destroyer’s chilled-water pump at $131.21 per part, against a conventional replacement cost of $316,544.16. That cost gap — over $316,000 per part — illustrates why procurement officers and fleet commanders are now treating AM as a cost discipline tool, not just a technology experiment.

Additionally, according to NAVSEA, the Navy cut a 29-week lead time for a critical valve component by approximately 70% through metal additive manufacturing with partner Marotta. Lead times of that magnitude are not just inefficiencies — they represent real gaps in operational readiness that adversaries can exploit. Eliminating them is a strategic priority, not a cost-saving exercise.

Key Takeaways

- The Military 3D Printing Market was valued at USD 3.2 Billion in 2025 and is forecast to reach USD 27.6 Billion by 2035, at a CAGR of 24.0%.

- By Offering, the Printer segment leads with 36.8% share in 2025.

- By Process, Powder Bed Fusion dominates with 29.7% share.

- By Application, Functional Part Manufacturing holds the largest share at 52.80%.

- By Platform, the Airborne segment leads with 44.1% share.

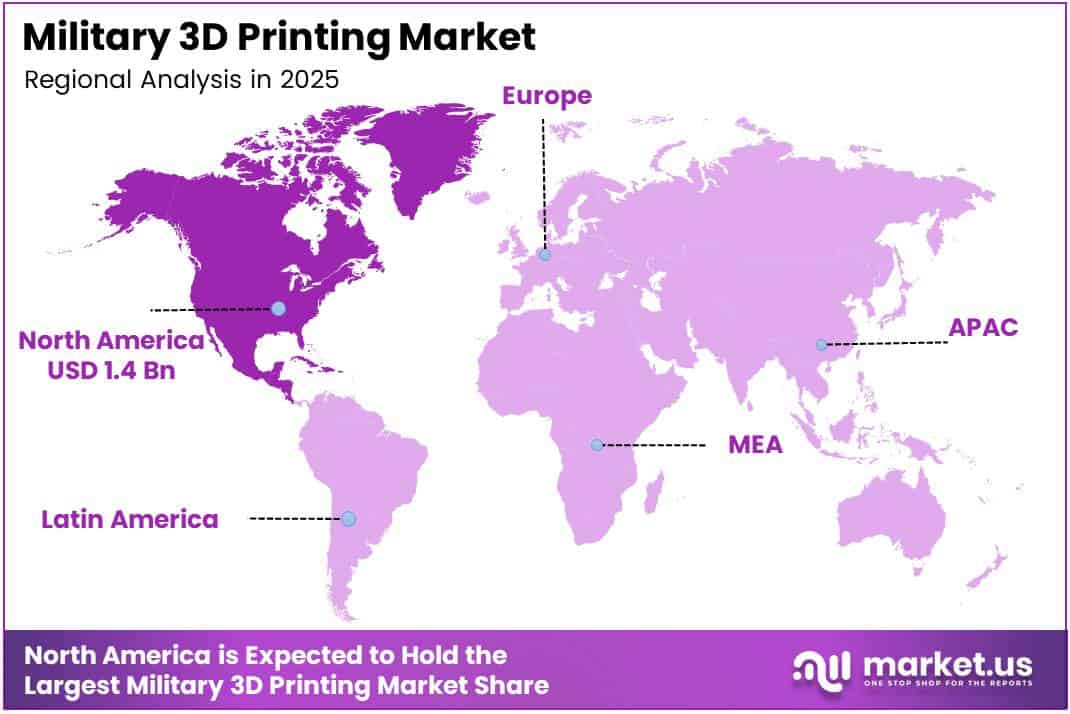

- North America dominates the regional landscape with 43.80% share, valued at USD 1.4 Billion in 2025.

Product Analysis

Printer dominates with 36.8% due to hardware-first defense procurement cycles.

In 2025, Printer held a dominant market position in the By Offering segment of the Military 3D Printing Market, with a 36.8% share. Defense buyers prioritize physical printing capacity first, establishing operational capability before standardizing feedstock and software workflows. This sequencing reflects procurement logic: hardware creates the platform; materials and software investment follows.

Material serves as the second critical layer of defense AM investment. Without qualified feedstocks — particularly metal powders and high-performance polymers — printers cannot produce mission-rated components. As NAVSEA’s specification work demonstrates, material standardization is now a primary focus for scaling AM output across military platforms.

Software carries growing strategic weight as design optimization and digital inventory management become operational tools. Defense agencies that build software infrastructure today create the ability to manufacture certified parts on demand at any location — a capability that shifts the entire supply chain model for spare parts.

Service differentiates through maintenance, training, and integration support, which defense buyers require to sustain AM operations in field environments. As more military units adopt 3D printing at the unit level, demand for specialized technical services will expand beyond the original equipment installations.

Process Analysis

Powder Bed Fusion dominates with 29.7% due to metal part precision for defense-grade components.

In 2025, Powder Bed Fusion held a dominant market position in the By Process segment of the Military 3D Printing Market, with a 29.7% share. The process produces high-density metal parts with tight dimensional tolerances — properties that defense applications demand for structural and functional components. Its dominance reflects the military’s preference for proven, certifiable manufacturing processes.

Binder Jetting offers a faster, lower-cost pathway for producing metal parts at higher volumes. For defense applications requiring large quantities of identical components — such as replacement hardware for fleets — binder jetting creates a production efficiency that powder bed fusion cannot match at scale.

Direct Energy Deposition differentiates through its ability to repair existing components, not just manufacture new ones. This makes it strategically valuable for high-value defense assets — aircraft engine parts, naval hardware — where repair is far more cost-effective than full replacement.

Material Extrusion carries the broadest field deployment profile, given its lower equipment cost and simpler operation. It enables forward-deployed units to produce non-structural parts, brackets, and tooling without requiring the controlled environment that metal processes demand.

Material Jetting serves high-resolution prototyping and multi-material applications where surface quality and dimensional accuracy are priorities. Defense R&D programs use it to validate designs before committing to production processes.

Vat Photopolymerization delivers fine-feature resolution for small components, medical devices, and training aids. Its role in military applications is narrower but precise — producing parts where detail fidelity outweighs material strength requirements.

Sheet Lamination provides a cost-effective method for producing large-format parts using bonded material layers. Its primary military application is in producing composite structures and tooling where complex geometries are needed at lower cost.

Application Analysis

Functional Part Manufacturing dominates with 52.80% due to operational readiness demands in active deployments.

In 2025, Functional Part Manufacturing held a dominant market position in the By Application segment of the Military 3D Printing Market, with a 52.80% share. Defense forces use additive manufacturing primarily to replace broken components under operational pressure — not for concept work. This positions military AM firmly as a sustainment tool, and it signals that defense buyers measure ROI through readiness metrics, not innovation budgets.

Tooling represents a high-value but often overlooked AM application in defense manufacturing. Printed jigs, fixtures, and production aids reduce tooling lead times from weeks to days, enabling maintenance facilities to keep pace with equipment schedules without relying on specialist suppliers.

Prototyping retains a meaningful share as defense R&D programs continue to use AM for validating designs before entering formal production. However, the balance has shifted — prototyping no longer defines military AM. Functional production now leads, which reflects the technology’s maturation from experimental to operational.

Platform Analysis

Airborne dominates with 44.1% due to weight reduction criticality in aerospace defense platforms.

In 2025, Airborne held a dominant market position in the By Platform segment of the Military 3D Printing Market, with a 44.1% share. Weight reduction directly improves fuel efficiency, payload capacity, and aircraft range — making AM components strategically valuable for military aviation. Defense aerospace programs prioritize AM adoption faster than ground or naval counterparts because the performance gains are immediate and quantifiable.

Land platforms benefit from AM’s ability to produce replacement parts at forward operating bases, reducing the logistics burden of moving spare parts through contested or remote supply routes. The U.S. Army’s 2025 policy authorizing unit-level commanders to approve 3D-printed parts reflects how land forces have moved AM from experiment to standard operating procedure.

Naval platforms represent one of the most technically demanding AM environments, where parts must withstand saltwater exposure, pressure cycling, and continuous operation. The U.S. Navy’s installation of a large metal AM valve manifold on a nuclear carrier in 2025 demonstrated that additive manufacturing now meets those standards at scale.

Space applications sit at the highest-value end of defense AM, where weight savings and lead time compression carry outsized mission impact. NASA’s RAMPT program validated that AM rocket thrust chambers deliver approximately 40% weight reduction and cut production costs by at least two-thirds, data points that defense space programs now reference in their own procurement decisions.

Key Market Segments

By Offering

- Printer

- Material

- Software

- Service

By Process

- Powder Bed Fusion

- Binder Jetting

- Direct Energy Deposition

- Material Extrusion

- Material Jetting

- Vat Photopolymerization

- Sheet Lamination

By Application

- Functional Part Manufacturing

- Tooling

- Prototyping

By Platform

- Airborne

- Land

- Naval

- Space

Drivers

On-Demand Battlefield Manufacturing Eliminates Critical Supply Chain Gaps in Military Operations

Defense forces face a fundamental logistics problem: standard supply chains move too slowly for combat tempo. The U.S. Army’s 2025 policy allowing unit commanders to approve locally printed parts — with “a couple thousand” components already fielded on M777 howitzers and infantry squad vehicles — shows how this gap is being closed at the operational level.

According to NAVSEA, the Forward Deployed Regional Maintenance Center in Rota recorded repair time reductions of approximately 80% when parts were manufactured on-site using additive methods instead of ordered through standard supply channels. An 80% reduction in repair time is not a marginal improvement — it directly restores ship readiness and removes the vulnerability that logistics delays create in forward operations.

Additive manufacturing also reduces exposure to single-source supplier risk, which defense agencies increasingly treat as a strategic vulnerability. When a mission-critical part exists only as a digital file and a qualified printer, the dependency on any specific supplier — or their geographic location — disappears. U.S. soldiers in Afghanistan demonstrated this principle by producing replacement parts locally, avoiding weeks-long logistics delays for low-volume components.

Restraints

Military Certification Demands and Cybersecurity Exposure Slow Full-Scale AM Deployment

Defense components must meet strict military performance specifications before they can be used on operational platforms. Certification processes require extensive testing, documentation, and regulatory approval — timelines that counteract the speed advantage additive manufacturing offers. Until qualification pathways become faster and more standardized, AM adoption will remain uneven across military branches.

Cybersecurity risk adds a second structural barrier. Digital manufacturing relies on design files stored and transmitted across networks — files that contain detailed specifications for military hardware. A compromised design file does not just create a defective part; it creates a weaponizable vulnerability. Defense agencies must implement rigorous data security protocols before expanding AM across sensitive weapons programs.

These two barriers reinforce each other. Cybersecurity requirements add complexity to the certification process, and certification delays reduce the incentive to invest in securing the digital infrastructure. Breaking this cycle requires coordinated investment in both standards development and secure digital manufacturing frameworks — an organizational challenge that no single defense contractor can solve alone.

Growth Factors

Deployable AM Units and Metal Additive Manufacturing Open New Operational and Production Frontiers

The development of mobile 3D printing units designed for battlefield deployment creates a new category of defense capability. Forward-deployed AM units eliminate the distance between where parts break and where they get replaced. Defense agencies that field these units reduce operational downtime without expanding their logistics footprint — a structural advantage in extended campaigns.

Metal additive manufacturing for aircraft and naval components represents the highest-value growth pathway in this market. According to NASA’s RAMPT program, additively manufactured rocket thrust chambers deliver approximately 40% weight reduction and cut production time and costs by at least two-thirds versus conventional methods. These figures give defense procurement teams a clear, quantified return on capital investment.

According to NAVSEA, standardizing AM material specifications reduced testing requirements by more than 60%, saving millions in qualification costs. This precedent matters because it shows that scaling AM across a military fleet is achievable through process discipline — not just technology investment. Defense agencies that replicate this specification model will accelerate deployment timelines across all platforms.

Emerging Trends

Multi-Material Printing, AI Design Optimization, and Industrial-Scale AM Reshape Defense Manufacturing Strategy

Multi-material 3D printing enables defense manufacturers to produce components with variable properties — hard outer shells, flexible internal structures, embedded conductors — in a single build cycle. This capability shifts what is manufacturable at the unit level and creates design possibilities that conventional machining cannot replicate at equivalent speed or cost.

AI-driven design optimization is changing how defense engineers approach part geometry. Rather than digitizing existing designs, AI tools generate structurally optimized geometries that reduce weight while maintaining or improving performance. According to documented defense AM outcomes, military 3D-printed parts have delivered weight reductions up to 40%, waste reductions up to 90%, and lead-time improvements of 60–70% — outcomes that AI-assisted design amplifies further.

Growing collaboration between defense agencies and advanced manufacturing startups accelerates the transition of emerging AM technologies into operational use. In 2025, the integration of large-scale industrial 3D printers in military maintenance facilities — including the installation of a metal AM component on a Virginia-class submarine — demonstrated that the technology barrier for high-stakes defense applications has been cleared. The strategic question now is how fast standardization follows.

Regional Analysis

North America Dominates the Military 3D Printing Market with a Market Share of 43.80%, Valued at USD 1.4 Billion

North America commands 43.80% of the global military 3D printing market, valued at USD 1.4 Billion in 2025. The U.S. military’s institutional investment — through NAVSEA, the Army, NASA, and branch-specific AM programs — creates a procurement infrastructure that no other region currently replicates. Policy mandates and documented cost savings continue to accelerate adoption across all service branches.

Europe Military 3D Printing Market Trends

Europe advances military AM adoption through NATO-aligned defense modernization programs and regional industrial partnerships. European defense manufacturers invest in metal additive capabilities for aerospace and armored vehicle applications. The region’s strong aerospace and precision engineering base gives it a structural advantage in qualifying AM components for complex defense platforms.

Asia Pacific Military 3D Printing Market Trends

Asia Pacific defense spending increases drive AM investment across China, India, Japan, and South Korea. Each nation pursues additive manufacturing as part of broader defense self-sufficiency strategies, reducing dependence on imported components. China’s state-directed defense industrial programs place AM adoption at the center of military modernization, creating both competitive pressure and regional demand growth.

Middle East and Africa Military 3D Printing Market Trends

Middle East defense forces invest in AM capabilities as part of broader equipment modernization programs, particularly for airborne and land platforms. The region’s reliance on imported defense hardware creates a strong strategic rationale for local additive manufacturing — reducing lead times and supply dependencies that external procurement creates.

Latin America Military 3D Printing Market Trends

Latin American defense agencies adopt additive manufacturing at an earlier stage, primarily for prototyping and tooling applications. Brazil and Mexico lead regional activity, supported by national defense industrial policies that favor domestic manufacturing capacity. Budget constraints limit the pace of adoption but do not eliminate the long-term procurement trajectory.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

3D Systems Corporation positions itself as a full-spectrum additive manufacturing provider, serving defense programs that require both hardware platforms and qualified materials. Its breadth across printing technologies — from polymer to metal — gives defense buyers a single-vendor pathway for multiple application types, reducing the integration complexity that multi-supplier programs create.

Divergent Technologies focuses on structural component manufacturing using AM-native design principles rather than converting conventional designs to printed formats. This distinction matters strategically: by designing parts specifically for additive processes, Divergent extracts weight and consolidation benefits that companies digitizing legacy designs cannot achieve. Defense aerospace programs reward that performance differential.

DM3D Technologies specializes in Direct Energy Deposition, a process valued in defense for its ability to repair high-value components rather than replace them entirely. For naval and aerospace applications where parts carry long service histories and high replacement costs, DM3D’s repair capability creates a cost-containment argument that procurement officers find compelling.

Elimold serves defense customers requiring rapid, low-volume production of customized components. Its manufacturing model aligns with the defense sector’s need for small-batch, high-specification parts that standard production lines cannot economically support. This positioning makes Elimold relevant as defense forces shift toward more unit-specific equipment customization.

Key players

- 3D Systems Corporation

- Divergent Technologies

- DM3D Technologies

- Elimold

- EOS GmbH

- GE Additive (Colibrium Additive)

- Lockheed Martin Corporation

- Markforged Holding Corporation

- Materialise NV

- Renishaw plc

- Sciaky, Inc.

- Solid Concepts, Inc

- Stratasys Ltd.

Recent Developments

- 2025 — The U.S. Navy expanded additive manufacturing to frontline fleet operations, integrating AM parts onto nuclear aircraft carriers and Virginia-class submarines. This formalized AM as an operational warfighting capability rather than a research and development function, representing a strategic inflection point for defense AM adoption.

- 2025 — Huntington Ingalls Industries installed the first large metal 3D-printed valve manifold — approximately 1.5 m long and 450 kg — aboard a nuclear-powered aircraft carrier. This marked one of the earliest deployments of a large AM structural component in a frontline naval vessel, validating AM at a new scale.

- 2025 — NAVSEA released multiple military performance specifications for additive materials (MIL‑PRF‑32802, MIL‑PRF‑32803, MIL‑PRF‑32804), reducing material testing requirements by over 60%. These specifications establish standardized qualification pathways for AM feedstocks, removing a major barrier to fleet-wide adoption.

- 2025 — The U.S. Army announced a policy change allowing unit-level commanders to approve 3D-printed replacement parts, with a couple thousand such parts already fielded on systems including M777 howitzers and infantry squad vehicles. Several printed parts reportedly outperformed the original components they replaced.

- 2025 — Defense case studies documented lead-time reductions of 60–70%, weight savings up to 40%, and waste reductions up to 90% from military 3D-printed parts. These documented outcomes reinforced the role of additive manufacturing in defense logistics and sustainment planning across multiple branches.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.2 Billion |

| Forecast Revenue (2035) | USD 27.6 Billion |

| CAGR (2026-2035) | 24.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Offering (Printer, Material, Software, Service), By Process (Powder Bed Fusion, Binder Jetting, Direct Energy Deposition, Material Extrusion, Material Jetting, Vat Photopolymerization, Sheet Lamination), By Application (Functional Part Manufacturing, Tooling, Prototyping), By Platform (Airborne, Land, Naval, Space) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | 3D Systems Corporation, Divergent Technologies, DM3D Technologies, Elimold, EOS GmbH, GE Additive (Colibrium Additive), Lockheed Martin Corporation, Markforged Holding Corporation, Materialise NV, Renishaw plc, Sciaky Inc., Solid Concepts Inc., Stratasys Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |