Quick Navigation

Report Overview

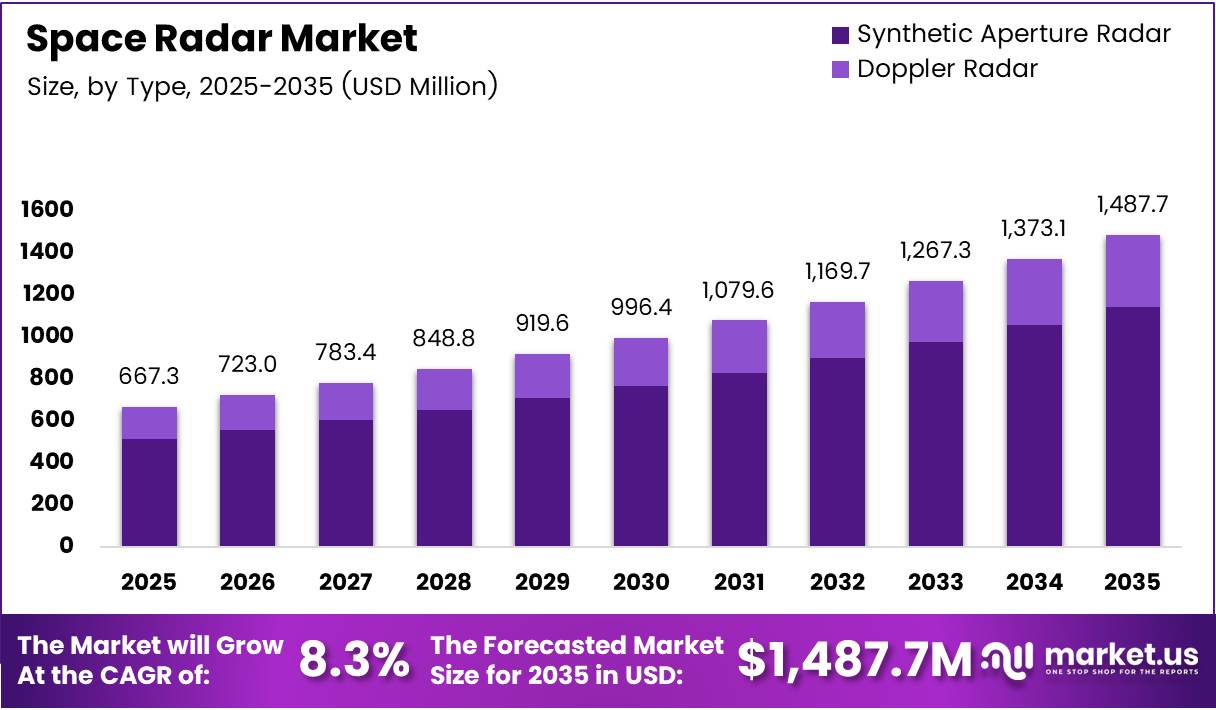

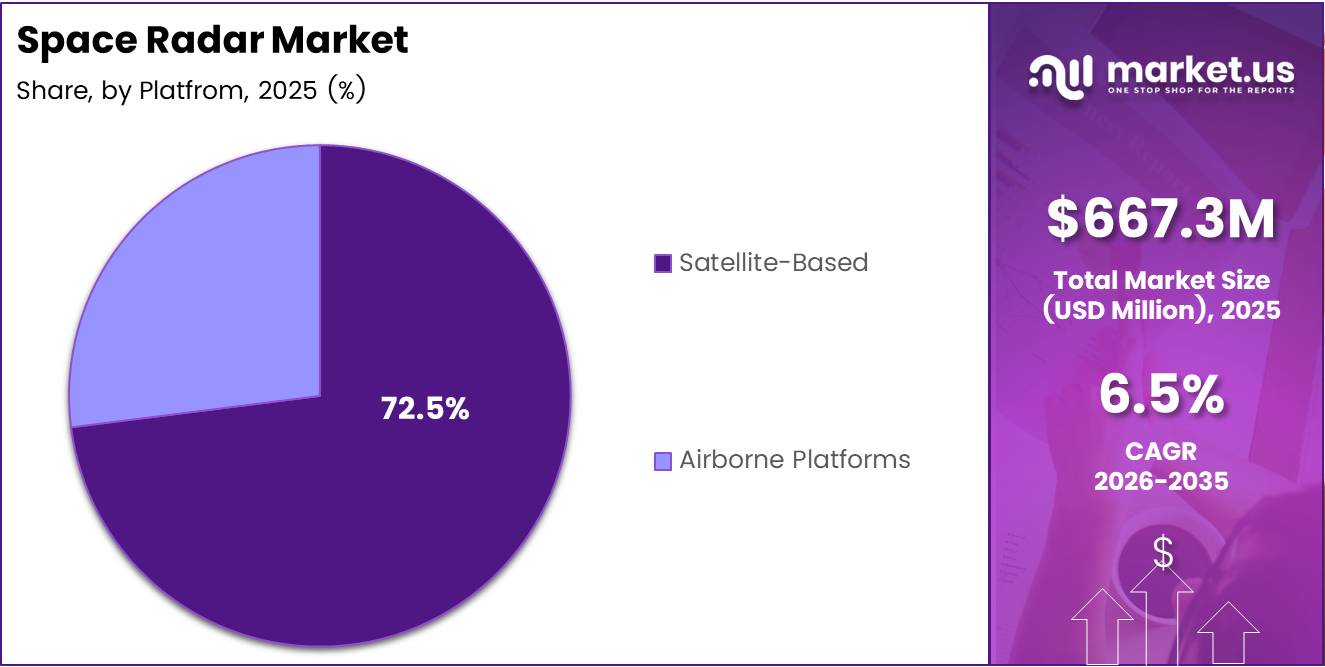

Global Space Radar Market size is expected to be worth around USD 1,487.7 Million by 2035 from USD 667.3 Million in 2025, growing at a CAGR of 8.3% during the forecast period 2026 to 2035.

The space radar market covers radar systems deployed on satellites and airborne platforms to observe Earth, track space objects, and support defense surveillance. These systems use frequency bands including X-Band, C-Band, and L-Band to perform synthetic aperture imaging, Doppler measurement, and orbital traffic monitoring.

Defense agencies worldwide treat space-based radar as a non-negotiable intelligence asset. Governments are expanding national security space surveillance programs, and commercial operators are building parallel constellations for earth observation and disaster response. This dual demand from defense and commercial buyers creates a structurally resilient revenue base.

National investments in space situational awareness are accelerating. Programs to monitor space debris, track satellite constellations, and detect orbital threats require persistent radar coverage that ground-based systems cannot provide alone. Space-based radar fills this gap directly, making it a procurement priority for defense ministries and space agencies.

The 8.3% CAGR reflects a market where buyer requirements are expanding faster than existing radar infrastructure can meet them. The deployment of large commercial satellite constellations — with thousands of new objects entering orbit — creates compounding demand for monitoring systems capable of distinguishing active satellites from debris at scale.

In November 2025, ICEYE successfully launched five new SAR satellites via the SpaceX Transporter-15 rideshare mission from Vandenberg Space Force Base, supporting programs for the Greek National Space Program, the Polish Armed Forces, and BAE Systems’ Azalea constellation. This single launch illustrates how commercial SAR providers now directly serve sovereign defense customers.

According to calibredefence.co.uk, current commercial SAR satellites achieve 25 cm imaging resolution using a maximum radar bandwidth of 1,200 MHz, compared to earlier resolutions of 1 m and 50 cm at 300 MHz and 600 MHz bandwidths. This resolution jump means commercial imagery now rivals classified systems, drawing defense contracts away from government-only suppliers toward the commercial sector.

According to calibredefence.co.uk, ICEYE had successfully launched a total of 40+ SAR satellites as of 2025, with nine satellites launched in 2024 alone. A constellation of this scale gives operators the revisit frequency — multiple passes per day over a target — that defense and disaster-response buyers require, translating raw hardware investment directly into service contract revenue.

Key Takeaways

- The Global Space Radar Market was valued at USD 667.3 Million in 2025 and is forecast to reach USD 1,487.7 Million by 2035, at a CAGR of 8.3%.

- Synthetic Aperture Radar (SAR) leads the By Type segment with a 76.3% market share in 2025.

- Satellite-Based platforms dominate the By Platform segment with a 72.5% share.

- X-Band (8–12 GHz) leads the By Frequency Band segment at 37.4% share.

- Earth Observation is the top application, holding a 43.7% share of the By Application segment.

- Defense and Security commands the By End User segment with a 63.6% share.

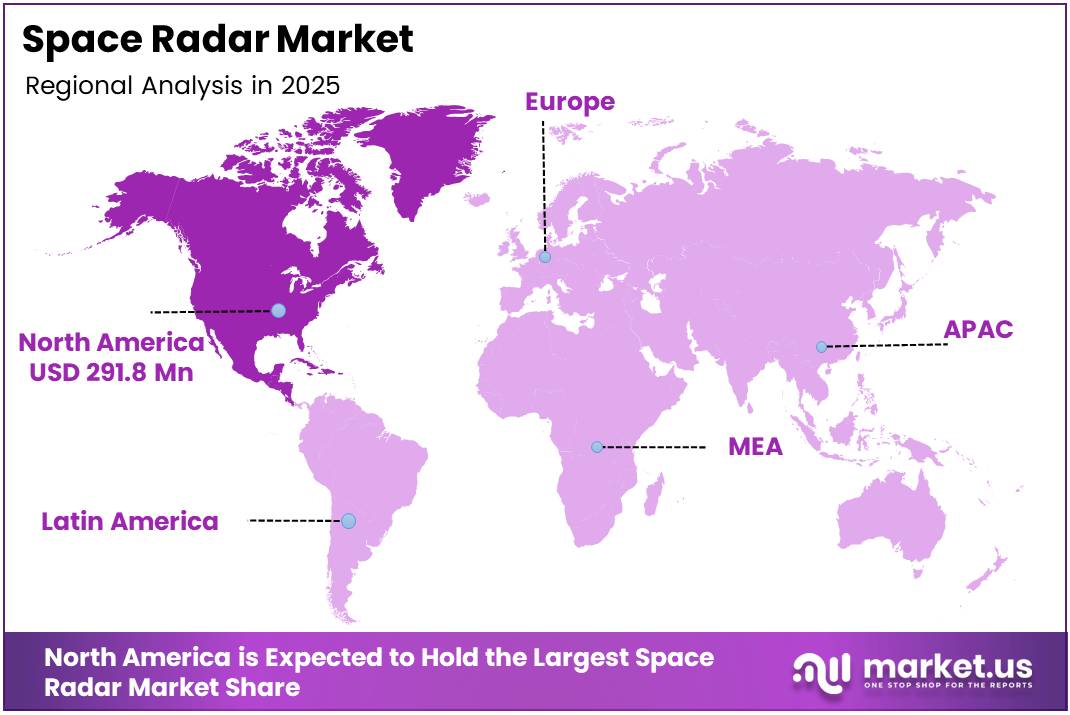

- North America dominates regionally with a 43.70% share, valued at USD 291.8 Million in 2025.

Type Analysis

Synthetic Aperture Radar dominates with 76.3% due to superior imaging resolution over wide areas.

In 2025, Synthetic Aperture Radar (SAR) held a dominant market position in the By Type segment of the Space Radar Market, with a 76.3% share. SAR systems generate high-resolution two-dimensional imagery regardless of cloud cover or daylight conditions, making them the primary choice for earth observation, defense reconnaissance, and disaster response missions where optical sensors fail.

Doppler Radar serves as the preferred solution for velocity measurement and weather tracking applications. Doppler systems measure the frequency shift of return signals to determine object speed and direction, which makes them essential for weather forecasting and moving-target detection. However, their narrower imaging capability limits their share relative to SAR in an earth observation-led market.

Platform Analysis

Satellite-Based platforms dominate with 72.5% due to persistent wide-area coverage capability.

In 2025, Satellite-Based platforms held a dominant market position in the By Platform segment of the Space Radar Market, with a 72.5% share. Orbital deployment enables continuous monitoring of large geographic areas without the range and endurance limits of airborne systems. Defense agencies and commercial operators both prioritize satellite platforms because a single asset covers multiple ground stations simultaneously across its orbital path.

Airborne Platforms carry a cost and flexibility advantage for missions requiring targeted, on-demand radar coverage. Aircraft-mounted radar systems deploy faster than satellite launches and can be repositioned to cover emerging crisis zones. Consequently, airborne radar remains relevant for tactical military reconnaissance and time-critical disaster assessment where waiting for a satellite pass is operationally unacceptable.

Frequency Band Analysis

X-Band dominates with 37.4% due to high spatial resolution for defense and surveillance use.

In 2025, X-Band (8–12 GHz) held a dominant market position in the By Frequency Band segment of the Space Radar Market, with a 37.4% share. X-Band frequencies produce fine spatial resolution, enabling detailed imaging of structures, vessels, and terrain features. Defense programs specifically select X-Band for target identification missions where pixel-level precision determines operational outcomes.

C-Band (4–8 GHz) offers a balance between resolution and all-weather penetration performance. C-Band systems tolerate atmospheric interference better than X-Band, making them the standard choice for wide-area agricultural monitoring, ice mapping, and flood assessment. Major earth observation programs have deployed C-Band sensors precisely because this band delivers consistent image quality under variable atmospheric conditions.

L-Band (1–2 GHz) penetrates vegetation canopy and dry soil, unlocking biomass monitoring and subsurface geological mapping applications that higher frequencies cannot access. The NASA-ISRO NISAR satellite, launched on 30 July 2025, carries an L-Band radar payload alongside S-Band, validating this frequency’s role in next-generation scientific and operational earth monitoring missions.

Ku, Ka, and V Bands address specialized applications including high-throughput data relay, precipitation measurement, and emerging commercial imaging services. These bands operate at millimeter-wave frequencies, supporting compact payload designs suited to small satellites. Their adoption reflects the market’s shift toward miniaturized, cost-efficient radar instruments across non-defense commercial segments.

Application Analysis

Earth Observation dominates with 43.7% due to commercial and government demand for persistent surface monitoring.

In 2025, Earth Observation held a dominant market position in the By Application segment of the Space Radar Market, with a 43.7% share. Commercial operators, national agencies, and international bodies contract SAR-based earth observation to monitor deforestation, urban change, agricultural conditions, and infrastructure stability. This breadth of buyers creates recurring subscription revenue for constellation operators rather than one-time hardware sales.

Weather Forecasting relies on space radar for precipitation mapping, storm tracking, and atmospheric profiling at altitudes and geographic scales that ground-based networks cannot replicate. National meteorological agencies procure radar data products to feed numerical weather models, creating a stable government-driven revenue stream with multi-year contract structures.

Disaster Management applications require near-real-time radar imagery to assess flood extents, earthquake damage, and wildfire boundaries under conditions where cloud cover or smoke blocks optical satellites. Response agencies pay premium rates for guaranteed rapid tasking, which makes disaster management contracts disproportionately valuable relative to their volume within the application mix.

Others within the application segment include maritime domain awareness, border surveillance, and scientific research missions. These applications do not individually generate the contract volumes of earth observation, but they collectively diversify revenue across end-use sectors. Diversification reduces single-sector revenue dependency for constellation operators who serve multiple mission types simultaneously.

End User Analysis

Defense and Security dominates with 63.6% due to sovereign surveillance and space situational awareness mandates.

In 2025, Defense and Security held a dominant market position in the By End User segment of the Space Radar Market, with a 63.6% share. Military and intelligence agencies treat space radar as a strategic asset for target tracking, border monitoring, and detecting adversarial space activities. This segment funds the largest single radar payloads and multi-year constellation programs, anchoring the overall market’s revenue base.

Government and Commercial end users represent the fastest-expanding buyer pool outside defense. Civil space agencies commission radar for climate science and land-use monitoring, while commercial buyers purchase data subscriptions for infrastructure inspection, insurance underwriting, and commodity tracking. The November 2025 ICEYE Transporter-15 launch, which served both sovereign defense customers and BAE Systems’ commercial Azalea constellation, illustrates how a single mission now monetizes both buyer categories simultaneously.

Key Market Segments

By Type

- Synthetic Aperture Radar

- Doppler Radar

By Platform

- Satellite-Based

- Airborne Platforms

By Frequency Band

- X-Band (8-12 GHz)

- C-Band (4-8 GHz)

- L-Band (1-2 GHz)

- Ku, Ka, and V Bands

By Application

- Earth Observation

- Weather Forecasting

- Disaster Management

- Others

By End User

- Defense and Security

- Government and Commercial

Drivers

National Security Mandates and Satellite Constellation Growth Force Accelerated Space Radar Deployment

Governments worldwide now treat space situational awareness as a sovereign security requirement. Defense ministries fund radar programs specifically to detect, track, and characterize orbital objects — including adversarial satellites and debris fields threatening critical infrastructure. This institutional demand does not shrink during budget cycles; it expands as geopolitical competition in orbit intensifies.

The deployment of large commercial satellite constellations adds thousands of new orbital objects annually, compounding the monitoring burden on existing space surveillance networks. National security agencies respond by expanding radar acquisition programs to achieve continuous, multi-orbit coverage. According to phys.org, the NISAR satellite launched on 30 July 2025 detects ground movements as small as one centimeter and pings nearly all land and ice surfaces every 12 days — demonstrating that government radar investments now combine security and scientific objectives within single missions, maximizing procurement value.

Space debris monitoring creates a parallel and self-reinforcing driver. Every additional launch increases the debris population, which in turn raises the operational risk to active constellations. Operators, insurers, and regulators all require radar-based tracking data to assess collision risk, license launches, and price coverage. This dependency converts space radar from a discretionary intelligence tool into a mandatory operational input across both public and private sectors.

Restraints

High Development Costs and Payload Complexity Limit Entry and Slow Deployment Timelines

Developing and launching a space-based radar system requires capital outlays that most commercial and smaller government operators cannot sustain independently. The engineering cost of a radar payload — including antenna design, signal processing hardware, and power systems — constitutes a significant portion of overall satellite program budgets. These costs gate entry at a level that concentrates market supply among a small number of well-funded defense primes and established space agencies.

Technical complexity further extends development timelines beyond those of optical satellite programs. Radar payloads demand precise calibration, high-power radio frequency generation, and large antenna apertures to achieve the resolution levels defense and commercial buyers require. Any compromise on these parameters directly degrades image quality and reduces the system’s commercial value, which means developers cannot simplify designs to reduce cost without sacrificing the performance that justifies the contract.

For smaller nations and commercial start-ups, these combined cost and complexity barriers delay market entry by years. While rideshare launch vehicles have reduced orbital access costs, the radar payload itself remains expensive to build and validate. Consequently, the market’s supply side concentrates around incumbents with existing manufacturing infrastructure, limiting competitive pressure on pricing and slowing the pace at which new capabilities reach smaller defense and government buyers.

Growth Factors

Commercial Space Traffic Management and Small Satellite SAR Platforms Open New Revenue Layers

Commercial space traffic management represents a structurally new service category that did not exist at scale five years ago. As orbital congestion worsens, private operators, launch providers, and national regulators all require verified, real-time tracking data. Radar providers that develop commercial traffic management data products create subscription revenue streams independent of government contracts, fundamentally diversifying their customer base.

According to phys.org, the NISAR satellite carries a dual L-Band and S-Band radar payload with a 39-foot (12-meter) antenna reflector and generates approximately 80 terabytes of data products per day during its prime mission. This data output volume signals that next-generation missions will require sophisticated processing and distribution infrastructure — creating adjacent market opportunities in ground systems, cloud analytics, and value-added data services beyond the radar hardware itself.

Small satellite platforms lower the capital threshold for deploying radar payloads, enabling new entrants and expanding constellation density for established players. According to calibredefence.co.uk, current commercial SAR satellites now achieve 25 cm imaging resolution at 1,200 MHz bandwidth — a step change from earlier 1 m resolution at 300 MHz. This performance improvement, delivered on compact platforms, means defense agencies can now procure commercial SAR data at quality levels previously achievable only through classified programs, widening the addressable commercial customer pool.

Emerging Trends

AI-Driven Object Detection and Miniaturized Payloads Redefine Space Radar Architecture

Miniaturization of radar payloads for small satellites is changing the economics of constellation building. Compact radar instruments reduce satellite mass, lower launch costs per unit, and allow operators to deploy denser constellations that improve revisit frequency over any target. This architectural shift moves competitive advantage from who can afford the largest payload to who can optimize performance-per-kilogram most effectively.

Artificial intelligence integration for space object detection and tracking addresses the data throughput problem that large radar constellations create. According to calibredefence.co.uk, ICEYE SAR Stripmap mode images a strip up to 30 km wide and 50 km long continuously, while Spotlight mode concentrates imaging on a 5 km² area for maximum resolution. Processing the volume of imagery these modes generate at operational tempo requires automated AI classification, not manual analyst review — making AI not an optional enhancement but a required component of any scalable radar service.

Public-private partnerships in space surveillance infrastructure and multi-orbit radar monitoring networks represent a structural shift in how governments fund and source space radar capability. Rather than developing sovereign systems entirely in-house, defense agencies now contract commercial operators for data services while co-investing in constellation development. This model reduces government capital expenditure while accelerating capability deployment timelines — a trade-off that both sides find commercially and strategically attractive.

Regional Analysis

North America Dominates the Space Radar Market with a Market Share of 43.70%, Valued at USD 291.8 Million

North America holds a 43.70% share of the global space radar market, valued at USD 291.8 Million in 2025. The United States drives this position through sustained Department of Defense investment in space situational awareness, a mature commercial SAR industry, and flagship programs such as the NASA-ISRO NISAR mission. This concentration of procurement and launch infrastructure gives North American suppliers a structural home-market advantage that competitors in other regions take years to replicate.

Europe Space Radar Market Trends

Europe holds a meaningful share of the space radar market, supported by programs under the European Space Agency and national defense procurement in France, Germany, and Italy. European operators actively participate in dual-use SAR constellations that serve both civil earth observation and defense surveillance requirements. The Polish Armed Forces’ MikroSAR program, supported by ICEYE’s November 2025 launch, reflects how European NATO members are building independent space radar capabilities within allied commercial frameworks.

Asia Pacific Space Radar Market Trends

Asia Pacific represents the fastest-expanding regional demand base for space radar, driven by India’s ISRO co-developing NISAR with NASA, China’s expanding surveillance satellite programs, and Japan’s investment in SAR-based disaster monitoring. India’s dual role as both a launch partner and end-user for advanced radar satellites signals that the region’s procurement capacity is shifting from dependent consumer to co-developer, which reshapes competitive dynamics for global suppliers entering this region.

Middle East and Africa Space Radar Market Trends

Middle East governments are investing in space radar as part of broader national security space strategies, with Gulf Cooperation Council states procuring earth observation and surveillance satellite services from established Western and Asian providers. Africa remains primarily a data consumer for radar-derived agricultural and environmental products. Regional infrastructure gaps limit indigenous development capacity, positioning the Middle East and Africa as import-dependent markets for the near term.

Latin America Space Radar Market Trends

Latin America uses space radar data primarily for environmental monitoring, deforestation tracking in the Amazon basin, and disaster response along seismically active Pacific coastlines. Brazil anchors regional demand through INPE and national space programs. The region’s dependency on international SAR data subscriptions rather than sovereign radar assets means Latin American buyers influence the commercial data services market more than the hardware and satellite manufacturing segments.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Saab AB positions itself at the intersection of defense electronics and space systems, leveraging decades of airborne radar expertise to compete in the satellite-based surveillance segment. Its established relationships with European and NATO defense ministries create procurement pathways that newer commercial SAR operators lack. This institutional trust translates into long-cycle, high-value contracts that provide revenue stability regardless of short-term commercial market fluctuations.

ICEYE has built a vertically integrated commercial SAR constellation that now serves both sovereign defense customers and commercial data buyers from the same orbital infrastructure. The company launched 40+ SAR satellites by 2025, achieving the revisit frequency that defense and disaster-response customers require at scale. In February 2026, ICEYE closed a €150 million Series E round led by General Catalyst, valuing the company at approximately USD 2.8 billion — a valuation that reflects investor confidence in recurring data-service revenue rather than hardware sales alone.

Boeing competes in the space radar market through large-scale defense and intelligence contracts where system integration, reliability requirements, and classified performance standards favor established prime contractors with government clearances. Boeing’s access to U.S. Department of Defense satellite programs positions it for the highest-value procurement awards in space surveillance and national security radar, where commercial operators cannot yet compete on certification or access grounds.

Northrop Grumman differentiates through advanced radar payload design for both satellite and airborne platforms, combining sensor development with the systems integration capability required for complex multi-payload surveillance missions. Its role in U.S. space domain awareness programs gives it privileged insight into government radar requirements, allowing earlier product development alignment with procurement cycles than external suppliers can achieve.

Key Players

- Saab AB

- ICEYE

- Boeing

- Northrop Grumman

- Leonardo S.p.A.

- Lockheed Martin Corporation

- LeoLabs

- Capella Space

- Denel Dynamics

- RTX

- PredaSAR Corporation

- Synspective Inc.

Recent Developments

- February 2026 – ICEYE closed a €150 million Series E funding round led by General Catalyst, plus €50 million in secondary transactions, valuing the company at €2.4 billion (approximately USD 2.8 billion). This capital raise funds further constellation expansion and positions ICEYE as Europe’s most highly valued commercial SAR operator.

- July 2025 – NASA and ISRO launched the NISAR satellite, the first dual-band (L-Band and S-Band) synthetic aperture radar mission designed to map nearly all of Earth’s land and ice surfaces every 12 days. The mission detects ground movements as small as one centimeter, setting a new benchmark for civilian SAR precision and establishing a data baseline for global environmental monitoring programs.

- November 2025 – ICEYE deployed five new SAR satellites via the SpaceX Transporter-15 rideshare mission from Vandenberg Space Force Base, supporting the Greek National Space Program, the Polish Armed Forces’ MikroSAR program, and BAE Systems’ Azalea constellation. This single rideshare mission served three distinct sovereign and commercial customers, demonstrating that multi-customer launch batching has become operationally standard for commercial SAR operators.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 667.3 Million |

| Forecast Revenue (2035) | USD 1,487.7 Million |

| CAGR (2026-2035) | 8.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Synthetic Aperture Radar, Doppler Radar), By Platform (Satellite-Based, Airborne Platforms), By Frequency Band (X-Band, C-Band, L-Band, Ku/Ka/V Bands), By Application (Earth Observation, Weather Forecasting, Disaster Management, Others), By End User (Defense and Security, Government and Commercial) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Saab AB, ICEYE, Boeing, Northrop Grumman, Leonardo S.p.A., Lockheed Martin Corporation, LeoLabs, Capella Space, Denel Dynamics, RTX, PredaSAR Corporation, Synspective Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |