Quick Navigation

Report Overview

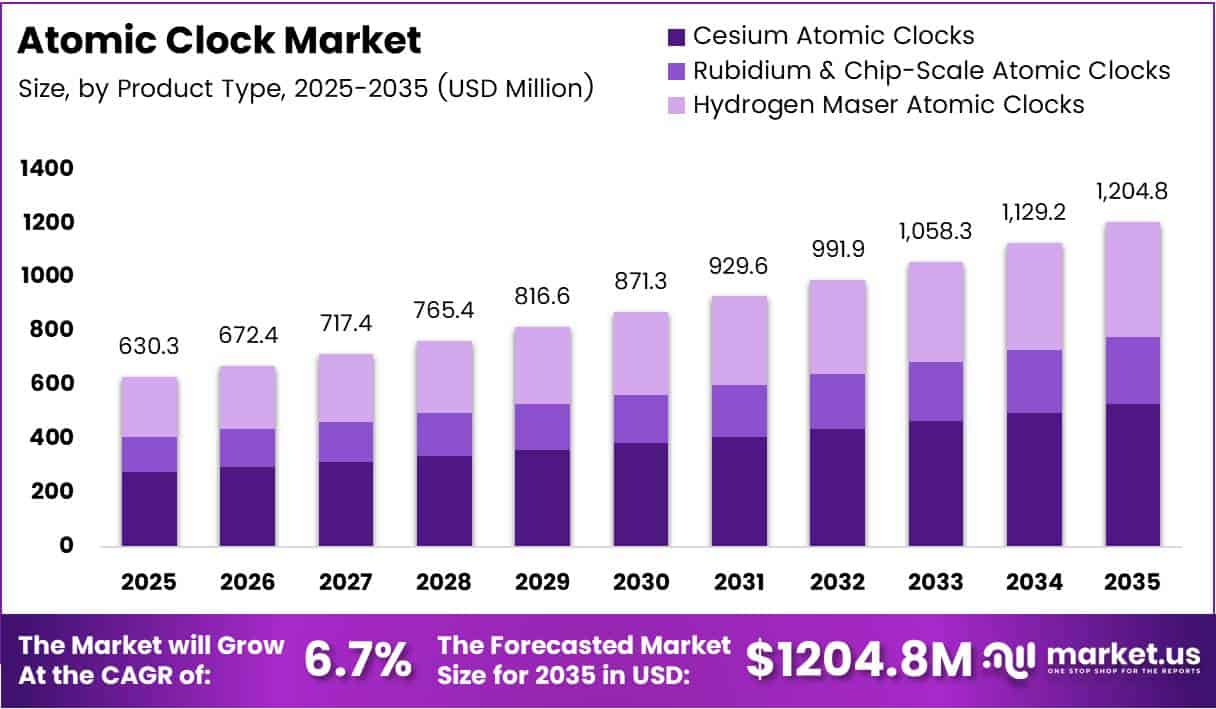

Global Atomic Clock Market size is expected to be worth around USD 1,204.8 Million by 2035 from USD 630.3 Million in 2025, growing at a CAGR of 6.7% during the forecast period 2026 to 2035.

Atomic clocks are precision timing devices that use the natural resonance frequencies of atoms — most commonly cesium, rubidium, or hydrogen — to measure time with extraordinary accuracy. These instruments serve as the backbone of satellite navigation, defense communication, scientific metrology, and telecommunications synchronization infrastructure worldwide.

The market spans three core product categories: cesium atomic clocks, rubidium and chip-scale atomic clocks, and hydrogen maser atomic clocks. Each category addresses distinct precision and deployment requirements, from space-grade systems to compact portable units for field applications in defense and autonomous vehicles.

Defense and aerospace buyers drive the largest share of demand, as secure positioning and communication systems depend entirely on atomic-level timing accuracy. A single timing error in military navigation or missile guidance can cascade into mission-critical failures, which is why defense agencies treat precision clocks as strategic infrastructure rather than commodity hardware.

Telecommunications networks form the second-largest demand pool. As 5G rollout accelerates globally, network operators require atomic-precision synchronization to maintain signal integrity across distributed radio units. This dependency creates a durable, contract-driven revenue base for atomic clock suppliers operating in the telecom infrastructure segment.

Space missions and satellite constellation deployments add another structural layer of demand. The rapid expansion of commercial and government satellite programs — spanning navigation, earth observation, and communications — means atomic clock procurement volumes are directly tied to launch schedules rather than economic cycles. In April 2025, QuantX Labs announced plans to launch a key component of its TEMPO optical atomic clock into orbit aboard a SpaceX mission, backed by an AUD 3.7 million Moon to Mars grant, signaling how even next-generation optical timing technology is transitioning from lab to orbital deployment.

According to drishtiias.com, optical atomic clocks maintain timekeeping with drift of only 1 second over 15 billion years — 100 times more accurate than traditional cesium clocks, which lose 1 second every 300 million years. This precision gap explains why defense agencies and space programs are willing to absorb the high unit costs associated with advanced atomic timing systems — the accuracy is not incremental, it is structurally different.

According to kb.veexinc.com, GNSS-based time sources disciplined by atomic clocks hold phase errors under ±1,100 ns for up to 24 hours during signal outages. For 5G radio operators, this holdover capability is not a premium feature — it is a network resilience requirement, and it directly anchors atomic clock procurement decisions in telecom infrastructure spending cycles.

Key Takeaways

- The Global Atomic Clock Market was valued at USD 630.3 Million in 2025 and is forecast to reach USD 1,204.8 Million by 2035.

- The market advances at a CAGR of 6.7% during the forecast period 2026 to 2035.

- By Product Type, Cesium Atomic Clocks lead with a 43.8% share in 2025.

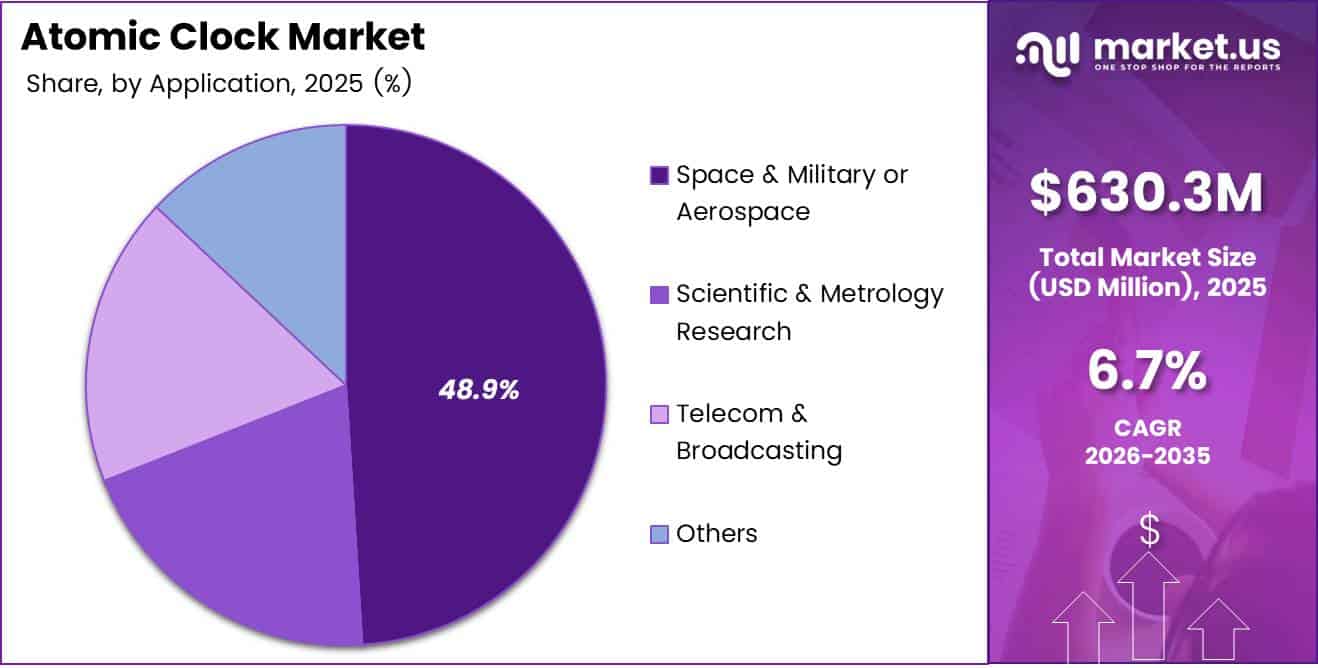

- By Application, Space and Military or Aerospace accounts for the largest share at 48.9%.

- By End User, Defense holds the dominant position with a 47.1% share.

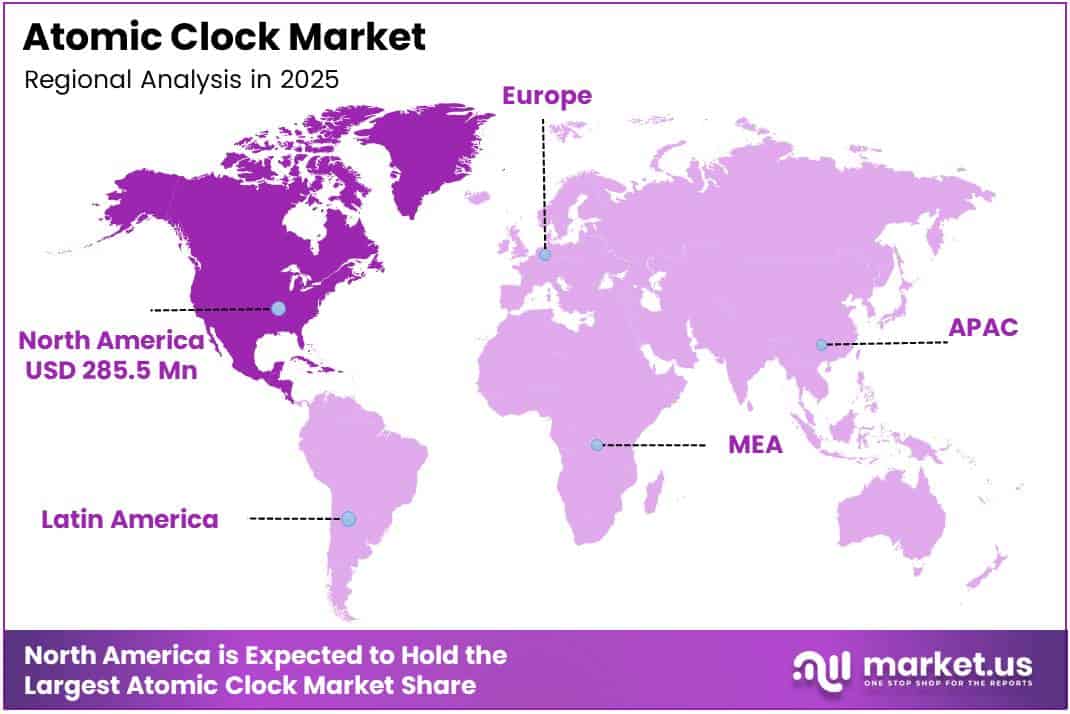

- North America is the leading region, commanding 45.30% of the global market, valued at USD 285.5 Million.

Product Analysis

Cesium Atomic Clocks dominate with 43.8% due to established defense and navigation standards.

In 2025, Cesium Atomic Clocks held a dominant market position in the By Product Type segment of the Atomic Clock Market, with a 43.8% share. Cesium remains the international standard for timekeeping — the SI definition of one second is based on cesium-133 resonance — which locks procurement across government, defense, and satellite navigation programs into this technology by regulatory default.

Rubidium and Chip-Scale Atomic Clocks serve as the cost-accessible entry point for mid-tier precision applications. Their smaller footprint and lower power draw make them the preferred choice for unmanned vehicles, portable military systems, and commercial satellite payloads. In January 2024, China’s Academy for Precision Measurement Science and Technology set a new international record for rubidium clock stability, advancing next-generation BeiDou satellite clock technology — a signal that rubidium platform performance is narrowing the gap with cesium for satellite-grade applications.

Hydrogen Maser Atomic Clocks occupy the high-accuracy end of the product spectrum, used primarily in deep-space missions and national metrology institutes. Their superior short-term stability makes them irreplaceable in applications where even microsecond deviations have consequences. However, their large physical size and high cost limit deployment to fixed, high-budget installations rather than mobile or commercial platforms.

Application Analysis

Space and Military or Aerospace dominates with 48.9% due to mission-critical timing dependency.

In 2025, Space and Military or Aerospace held a dominant market position in the By Application segment of the Atomic Clock Market, with a 48.9% share. Defense navigation, missile guidance, and satellite payloads cannot tolerate timing errors — even nanosecond deviations compromise positioning accuracy across long distances, making atomic clocks non-negotiable components rather than optional upgrades in these systems.

Scientific and Metrology Research drives atomic clock development at the frontier of physical science. National labs and research institutes use these systems to probe fundamental constants, redefine measurement standards, and test theories in physics. While this segment is smaller in revenue terms, it functions as the primary source of precision benchmarks that eventually migrate into commercial and defense specifications.

Telecom and Broadcasting applications depend on atomic clock synchronization to maintain network timing coherence across distributed infrastructure. As 5G radio units proliferate, each node requires precise holdover timing during GNSS signal outages. This demand pattern ties telecom atomic clock procurement directly to network buildout schedules, creating predictable volume cycles for suppliers.

Others encompasses financial trading networks, power grid synchronization, and scientific instrumentation. High-frequency trading platforms, in particular, use atomic clock timestamping to adjudicate trade sequencing at nanosecond resolution — a compliance and competitive requirement that creates a durable, recurring procurement base outside traditional defense and telecom channels.

End User Analysis

Defense dominates with 47.1% due to non-negotiable precision requirements in combat systems.

In 2025, Defense held a dominant market position in the By End User segment of the Atomic Clock Market, with a 47.1% share. Defense platforms from combat aircraft to armored vehicles require onboard timing systems that operate independently of external GNSS signals — particularly in contested or denied-signal environments. This requirement elevates atomic clocks from instruments to mission-critical hardware.

Combat Aircraft and Helicopters integrate atomic clocks for navigation, weapons targeting, and secure communication synchronization. These platforms require timing accuracy that holds across high-vibration, high-altitude operating conditions — specifications that push procurement toward ruggedized cesium and chip-scale units rather than standard commercial-grade devices.

Unmanned Vehicles represent one of the fastest-scaling subsegments within Defense. As UAV and UGV fleets expand globally, each platform requires an onboard atomic or chip-scale clock to operate autonomously in GNSS-degraded environments. The drive to miniaturize these systems without sacrificing accuracy is directly shaping chip-scale atomic clock development roadmaps.

Armoured Vehicles use atomic clock synchronization to coordinate fire control and battlefield communication across distributed ground forces. Timing precision in network-centric warfare determines how effectively multiple platforms can act in coordinated sequence — making clock accuracy a direct determinant of tactical effectiveness.

Portable Systems serve special operations and field intelligence units requiring compact, battery-powered atomic timing. Chip-scale atomic clocks have made portable precision timing operationally viable for the first time, enabling soldiers in the field to maintain timing accuracy without reliance on GPS infrastructure.

Naval Ships — including destroyers and frigates — depend on atomic clocks for sonar synchronization, electronic warfare timing, and secure fleet communication. The marine environment adds mechanical stress and electromagnetic interference challenges that demand both timing precision and physical ruggedization in the same unit.

Submarines require atomic clocks with exceptional holdover performance because they operate submerged for extended periods without access to any external timing signals. A submarine’s navigation accuracy over a multi-week deployment depends entirely on the stability of its onboard atomic clock — making this one of the most uncompromising specifications in the entire defense timing market.

Patrol Vessels use atomic timing primarily for navigation and communication coordination in coastal and maritime border enforcement roles. Their requirements are less extreme than deep-ocean submarines but still demand certified precision beyond commercial-grade GPS disciplined oscillators.

Space end users — satellite operators and launch vehicle programs — consume high-accuracy clocks for payload timing, orbital mechanics calculations, and inter-satellite link synchronization. Commercial satellite constellation growth has expanded this buyer segment beyond government space agencies to include private operators with recurring procurement budgets.

Civil and Commercial end users span telecommunications, financial networks, power utilities, and scientific institutions. This segment is the most price-sensitive but also the broadest in addressable volume — and as chip-scale atomic clock costs decline, commercial adoption rates will expand the addressable buyer base significantly.

Key Market Segments

By Product Type

- Cesium Atomic Clocks

- Rubidium & Chip-Scale Atomic Clocks

- Hydrogen Maser Atomic Clocks

By Application

- Space & Military or Aerospace

- Scientific & Metrology Research

- Telecom & Broadcasting

- Others

By End User

- Defense

- Combat Aircraft and Helicopters

- Unmanned Vehicles

- Armoured Vehicles

- Portable Systems

- Naval Ships (Destroyers, Frigates)

- Submarines

- Patrol Vessels

- Space

- Civil and Commercial

Drivers

Defense Modernization and Satellite Navigation Expansion Drive Structural Demand for High-Precision Timing Systems

Defense agencies worldwide treat atomic clocks as strategic infrastructure because combat systems — from missile guidance to network-centric battlefield communication — fail without precise timing. The shift toward denied-GPS operating environments has made onboard atomic timing systems mandatory across combat aircraft, unmanned vehicles, and armored platforms, removing buyer discretion from procurement decisions.

Satellite navigation infrastructure compounds this demand. GPS, Galileo, BeiDou, and GLONASS constellations all carry atomic clocks as payload essentials. As these programs expand their satellite counts and upgrade to next-generation systems, clock procurement scales in direct proportion. According to Physical Review Letters (January 2025), Germany’s PTB demonstrated a new ion crystal optical clock with accuracy close to 18 decimal places — establishing that the precision ceiling for navigation-grade timing is still rising, which keeps development investment active across government and commercial satellite programs.

In October 2025, MIT physicists published a method in Nature that doubles optical atomic clock precision using quantum-amplification of ytterbium atoms — enabling a clock to resolve twice as many ticks per second compared to conventional setups. For defense procurement planners, advances of this magnitude signal that next-generation atomic clocks will deliver qualitatively better performance, justifying platform upgrade budgets ahead of scheduled replacement cycles.

Restraints

High Development Costs and Technical Complexity Limit Adoption Beyond High-Budget Defense and Space Programs

Advanced atomic clocks — particularly hydrogen masers and optical frequency standards — require specialized manufacturing environments, exotic materials, and highly trained engineering teams to build and maintain. These structural cost factors make unit prices prohibitive for mid-tier commercial buyers, effectively concentrating the market among defense agencies, space programs, and national metrology institutes with large, protected procurement budgets.

Technical complexity extends beyond manufacturing into maintenance and calibration. Ultra-high precision systems require periodic recertification against national standards, controlled operating environments, and specialized support infrastructure. For commercial or smaller institutional buyers, the total cost of ownership extends well beyond acquisition price — and this gap between purchase cost and operational cost acts as a structural barrier to broader adoption.

In March 2024, the European Space Agency signed a EUR 12 million contract with Leonardo S.p.A. and INRiM to develop a new rubidium atomic clock for the Galileo Second Generation system — targeting a mass reduction of more than 40% compared to current hydrogen maser clocks. The scale of investment required to achieve even incremental improvements in size and cost underscores why only government-backed programs can absorb the R&D burden of advancing atomic timing technology, leaving commercial developers in a structurally dependent position.

Growth Factors

Next-Generation Satellite Programs, 5G Synchronization, and Quantum Timing Research Open New Revenue Channels

GPS III and equivalent next-generation satellite programs are replacing older satellites with payloads requiring higher-accuracy onboard clocks. Each new satellite launched represents a direct procurement event for atomic clock suppliers. Commercial constellation operators — building broadband and earth observation networks — add a private-sector dimension to this demand that did not exist at scale a decade ago.

5G network synchronization creates a recurring demand base in telecommunications. Base stations and radio units require atomic-precision timing for phase synchronization, and as 6G research advances, the timing accuracy threshold for network operation will increase further. This positions atomic clock suppliers as essential infrastructure partners for telecom operators managing dense, distributed antenna networks. According to Physical Review Letters (October 2025), a JILA/NIST/University of Chicago strontium optical lattice clock achieved a record coherence time of 118(9) seconds and atomic instability of 1.5×10⁻¹⁸ — research milestones that directly feed into future commercial timing specifications.

In April 2025, QuantX Labs announced the planned orbital deployment of its TEMPO optical frequency comb — the world’s first optical frequency comb in space — supported by an AUD 3.7 million Australian Space Agency grant. This milestone bridges laboratory optical clock research and operational space deployment, creating a commercially viable pathway for optical atomic clocks to enter satellite payloads and displace current cesium and rubidium standards over the next decade.

Emerging Trends

Miniaturization of Chip-Scale Clocks and Optical Clock Advances Reshape the Competitive Landscape

Chip-scale atomic clock miniaturization is expanding the addressable market well beyond traditional defense and space buyers. Compact, low-power rubidium and CSAC units now fit inside unmanned vehicles, portable soldier systems, and commercial IoT infrastructure. This democratization of precision timing is creating volume demand segments where atomic clocks were previously too large and expensive to deploy.

Optical atomic clock research is advancing faster than commercial roadmaps anticipated. According to Physical Review Letters (October 2025), a JILA/NIST/University of Chicago strontium optical lattice clock achieved a record atomic coherence time of 118(9) seconds and instability of 1.5×10⁻¹⁸. This level of performance — far exceeding current cesium standards — signals that optical clocks are transitioning from research instruments to viable commercial and defense platforms within the forecast period.

Autonomous navigation systems are emerging as a new high-growth deployment environment for atomic timing. Self-driving vehicles, maritime autonomous systems, and unmanned aerial platforms all require onboard timing that functions independently of GNSS. As government funding for national timing infrastructure increases and quantum timing research matures, the convergence of miniaturization and optical precision will define the competitive frontier through 2035.

Regional Analysis

North America Dominates the Atomic Clock Market with a Market Share of 45.30%, Valued at USD 285.5 Million

North America leads the global atomic clock market with a 45.30% share, valued at USD 285.5 Million in 2025. The United States drives this position through sustained defense spending, GPS infrastructure investment, and the world’s highest concentration of national metrology and space program procurement. Federal agencies — from the Department of Defense to NIST — create a protected, large-volume demand base that shields North American suppliers from cyclical commercial market pressures.

Europe Atomic Clock Market Trends

Europe holds a strong secondary position, anchored by programs such as the Galileo satellite navigation system and national metrology institutes including Germany’s PTB and Finland’s VTT MIKES. The European Space Agency’s active investment in next-generation navigation clock development — including the EUR 12 million Leonardo S.p.A. contract for Galileo Second Generation — signals that European public procurement will sustain above-average demand through the forecast period.

Asia Pacific Atomic Clock Market Trends

Asia Pacific represents the most active growth region for atomic clock procurement, led by China’s BeiDou constellation expansion and India’s defense modernization programs. China’s Academy for Precision Measurement Science and Technology set a new international rubidium clock stability record in January 2024, demonstrating that the region is investing not just in deployment but in domestic clock technology development — reducing long-term dependence on foreign suppliers.

Middle East and Africa Atomic Clock Market Trends

Middle East and Africa show selective but growing atomic clock adoption, concentrated in defense modernization programs and telecommunications infrastructure upgrades. Gulf nations investing in national GPS-independent navigation and secure defense communication systems represent the most active procurement centers in this region, while broader commercial adoption remains limited by infrastructure development timelines.

Latin America Atomic Clock Market Trends

Latin America remains the smallest regional contributor, with demand concentrated in telecommunications network synchronization and scientific research institutions. Brazil leads regional procurement through its space agency and military modernization programs. As 5G rollout accelerates across major Latin American markets, telecom-driven atomic clock adoption will become the primary demand driver through the forecast period.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

AccuBeat Ltd. positions itself as a specialist in high-stability atomic frequency standards for defense and space applications. Its focus on ruggedized, field-deployable timing solutions gives it a structural advantage in military procurement cycles, where reliability under adverse conditions outranks unit cost in supplier selection. This specialization insulates AccuBeat from commodity pricing pressure that affects broader commercial timing markets.

Excelitas Technologies Corp. competes across both defense and scientific instrumentation segments, leveraging a broad photonics and detection technology portfolio that complements its atomic clock offerings. This cross-portfolio integration allows Excelitas to bundle timing systems with related optical and sensing components — a procurement convenience that strengthens its position in government and aerospace contracts requiring multi-component sourcing.

Leonardo S.p.A. holds a strategically important position as the contract partner for ESA’s Galileo Second Generation rubidium atomic clock development. The EUR 12 million ESA contract awarded in March 2024 not only validates Leonardo’s technical capability but also locks in a long-duration revenue stream tied directly to European navigation infrastructure spending — a more durable position than competing on commercial open markets.

Microchip Technology Incorporated differentiates through chip-scale atomic clock miniaturization, targeting the expanding portable and unmanned systems market. Its January 2025 launch of the SA65-LN second-generation Low-Noise CSAC — with sub-half-inch profile height and sub-295 mW power draw — directly addresses the size, weight, and power constraints of defense UAV and autonomous sensor network deployments, where incumbent larger-format clocks cannot compete.

Key Players

- AccuBeat Ltd.

- Excelitas Technologies Corp.

- Leonardo S.p.A.

- Microchip Technology Incorporated

- Stanford Research Systems

- VREMYA-CH JSC

- Safran SA

- Thermo Fisher Scientific Inc.

- Frequency Electronics, Inc.

- Abracon LLC

- AOSense, Inc.

Recent Developments

- January 2025 — Microchip Technology launched its second-generation Low-Noise Chip-Scale Atomic Clock, the SA65-LN, featuring a profile height under half an inch, an operating temperature range of -40°C to +80°C, and power consumption below 295 mW. The device targets aerospace and defense applications including mobile radar, autonomous sensor networks, and unmanned vehicles.

- March 2024 — The European Space Agency, on behalf of the European Commission, awarded a EUR 12 million contract to Leonardo S.p.A. and INRiM to design and develop a new ultra-precise pulsed optically pumped rubidium atomic clock for the Galileo Second Generation satellite navigation system. The new clock targets a mass reduction of more than 40% versus current Galileo hydrogen maser clocks.

- March 2026 — QuantX Labs successfully launched its optical frequency comb into orbit as part of the KAIROS mission aboard a SpaceX launch vehicle, marking the world’s first optical frequency comb in space. This milestone advances the TEMPO.Space programme toward the first operational optical atomic clock in orbit.

- December 2025 — Researchers at VTT MIKES in Finland demonstrated a strontium single-ion optical clock with a systematic uncertainty of 7.9×10⁻¹⁹ — among the lowest ever reported — achieving 84% operational uptime over 10 months when measured against International Atomic Time (TAI), with a record total measurement uncertainty of 9.8×10⁻¹⁷.

- January 2026 — PTB developed a new multi-ion optical ytterbium-173 clock combining high single-ion accuracy with improved multi-ion stability, enabling time and frequency measurement up to 1,000 times more accurate than cesium clocks, as published in Physical Review Letters.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 630.3 Million |

| Forecast Revenue (2035) | USD 1,204.8 Million |

| CAGR (2026-2035) | 6.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Cesium Atomic Clocks, Rubidium & Chip-Scale Atomic Clocks, Hydrogen Maser Atomic Clocks), By Application (Space & Military or Aerospace, Scientific & Metrology Research, Telecom & Broadcasting, Others), By End User (Defense, Naval Ships, Space, Civil and Commercial) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | AccuBeat Ltd., Excelitas Technologies Corp., Leonardo S.p.A., Microchip Technology Incorporated, Stanford Research Systems, VREMYA-CH JSC, Safran SA, Thermo Fisher Scientific Inc., Frequency Electronics, Inc., Abracon LLC, AOSense, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |