Quick Navigation

Report Overview

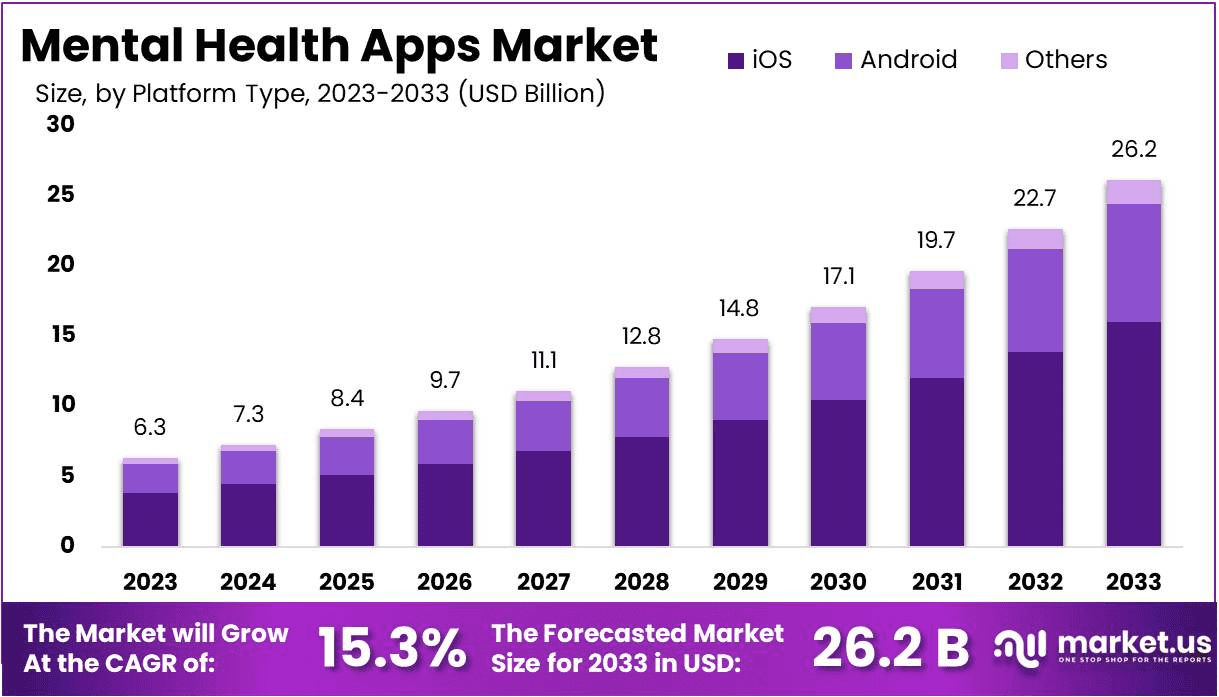

The Mental Health Apps Market Size is expected to be worth around US$ 26.2 billion by 2033 from US$ 6.3 billion in 2023, growing at a CAGR of 15.3% during the forecast period 2024 to 2033.

The increasing adoption of mental health apps stems from their effectiveness in enhancing treatment outcomes and improving overall lifestyle, along with growing awareness of mental health as a significant concern. These apps play a vital role in boosting well-being and productivity, particularly among professionals. The COVID-19 pandemic further accelerated market growth by driving a notable rise in app downloads.

Additionally, the shift from traditional care methods to more personalized and patient-centered approaches has supported the expansion of mental health apps. These apps, which include features for meditation, managing depression and anxiety, and overall wellness, help individuals maintain better health and reduce stress.

For instance, in June 2023, HuddleHumans, a Singapore-based company, launched a global social mental health app designed to build a supportive community. This app enables users to engage in group discussions, share personal stories, and access valuable resources such as mental health articles and self-care tools.

Key Takeaways

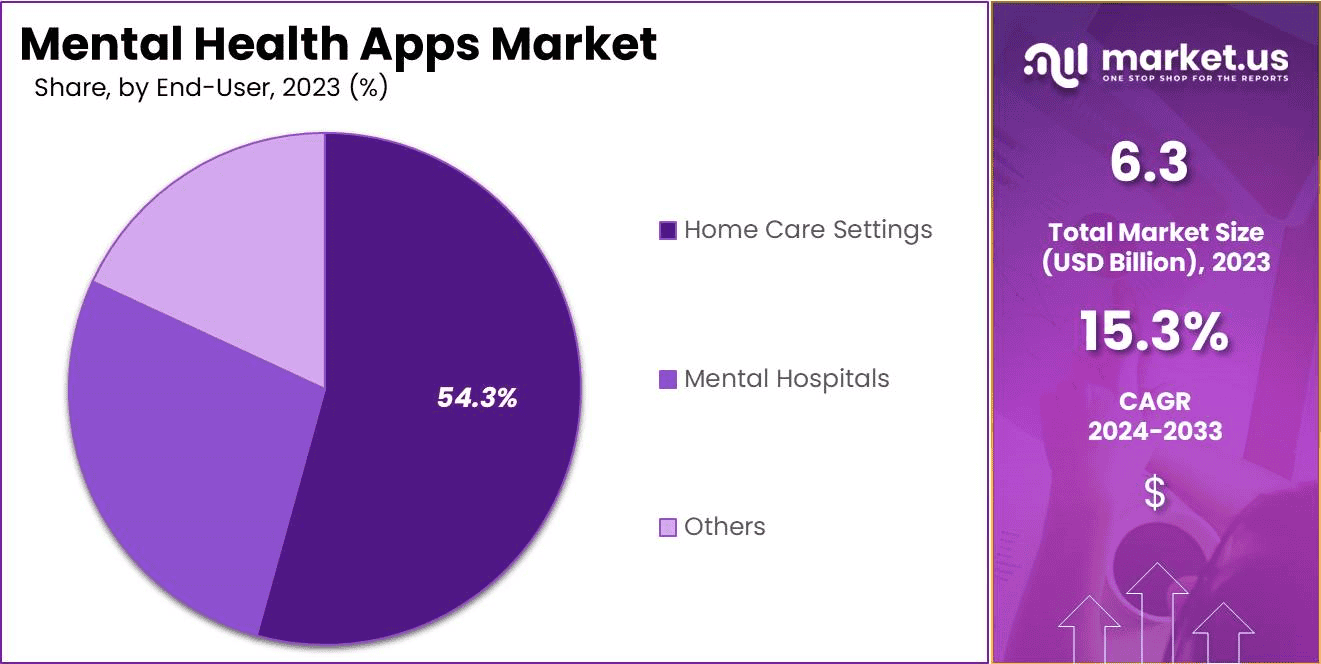

- In 2023, the market for Mental Health Apps generated a revenue of US$ 6.3 billion, with a CAGR of 15.3%, and is expected to reach US$ 26.2 billion by the year 2033.

- The platform type segment is divided into iOS, Android, and others, with iOS taking the lead in 2023 with a market share of 61.2%.

- Considering application, the market is divided into stress management, depression & anxiety management, meditation management, and others. Among these, depression & anxiety management held a significant share of 42.3%.

- Furthermore, concerning the end-user segment, the market is segregated into home care settings, mental hospitals, and others. The home care settings sector stands out as the dominant player, holding the largest revenue share of 54.3% in the Mental Health Apps market.

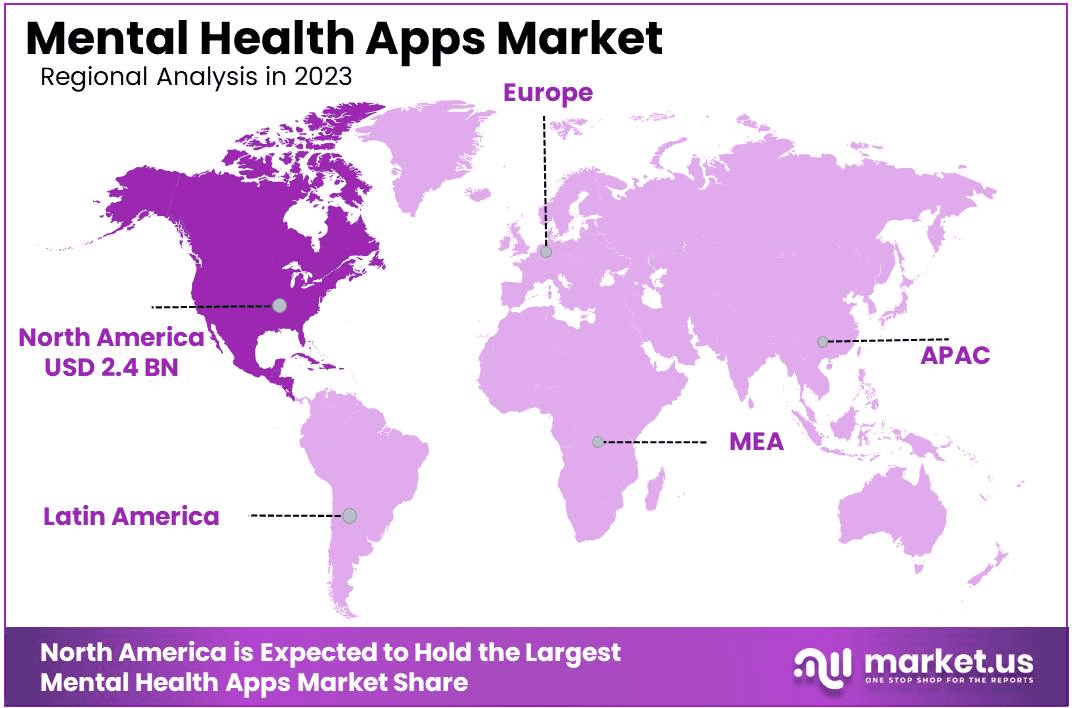

- North America led the market by securing a market share of 38.7% in 2023.

Platform Type Analysis

The iOS segment led in 2023, claiming a market share of 61.2% owing to Apple’s extensive user base and the platform’s strong security features. iOS is expected to see increased adoption as developers favor it for its user-friendly interface and robust ecosystem.

The consistency and reliability of iOS updates enhance the performance and security of mental health apps, making it a preferred choice for both users and developers. Additionally, Apple’s strict app review process ensures high-quality applications, which attracts more users seeking reliable mental health solutions.

This segment is projected to expand further as the popularity of iOS devices continues to rise globally, driving more developers to create and optimize mental health apps for this platform.

Application Analysis

Depression & anxiety management held a significant share of 42.3% due to the rising prevalence of mental health disorders and increasing awareness of mental well-being. This segment is likely to see expansion as individuals seek more accessible and effective tools for managing depression and anxiety.

The development of innovative features, such as real-time mood tracking and personalized therapy, addresses the growing demand for tailored mental health support. Additionally, increasing societal acceptance and reduced stigma around mental health is anticipated to boost user engagement with these specialized apps, further driving the segment’s growth.

End-User Analysis

The home care settings segment had a tremendous growth rate, with a revenue share of 54.3% as more patients and caregivers seek convenient, remote solutions for mental health management. The rise in telehealth adoption and the preference for at-home care, especially among elderly and chronically ill individuals, significantly contribute to this trend.

Home care settings are projected to see a higher demand for mental health apps due to their ability to provide continuous monitoring and support outside of traditional clinical environments. Additionally, the convenience and cost-effectiveness of using apps in a home setting are likely to drive increased adoption, making this segment a key area of growth in the mental health apps market.

Key Market Segments

By Platform Type

- iOS

- Android

- Others

By Application

- Stress Management

- Depression & Anxiety Management

- Meditation Management

- Others

By End-user

- Home Care Settings

- Mental Hospitals

- Others

Drivers

High Prevalence of Depression

Rising global rates of depression significantly drive the demand for digital solutions aimed at improving psychological well-being. The high prevalence of depression creates a substantial market opportunity for technology-based interventions. As more individuals seek accessible and effective support, providers are anticipated to expand their offerings in this space.

The increased focus on mental health is projected to spur innovation in digital platforms designed to address diverse needs, from symptom management to therapy and support. Enhanced by the convenience and scalability of technology, these solutions are expected to become integral to comprehensive mental health care. Consequently, market growth will likely reflect this escalating demand, with new and advanced digital tools emerging to meet the needs of a global audience.

The ongoing emphasis on addressing mental health issues through digital means underscores the critical role these technologies play in contemporary healthcare. According to the World Health Organization (WHO) data from March 2023, approximately 280 million people globally suffer from depression, which represents 3.8% of the global population. This high prevalence of depression underscores the growing need for accessible mental health solutions, fueling the demand for mental health apps that offer support and resources to a significant portion of the population.

Restraints

Lack of Proper Network Connectivity

Rising issues with network connectivity significantly restrain the mental health apps market. Poor or unstable internet connections impede the functionality and accessibility of these applications. Users in areas with limited connectivity experience interruptions and delays, which hampers their engagement and satisfaction with the services.

This issue creates a barrier to the widespread adoption of digital mental health solutions. Areas with inadequate infrastructure may face challenges in fully benefiting from the available resources. As a result, the market’s growth could be restrained in regions where reliable internet access is lacking, limiting the potential user base and affecting overall market expansion.

Opportunities

Increase in Demand for Mental Health Resources

Growing demand for mental health resources presents a significant opportunity for the mental health apps market. As individuals increasingly seek ways to manage their mental well-being, the market for these digital solutions expands.

Consumers are expected to turn to apps for their convenience, anonymity, and tailored support, driving growth in this sector. The surge in interest creates opportunities for developers to innovate and provide diverse offerings that cater to varying needs. The anticipated rise in demand is likely to encourage investment and development in this space, potentially leading to enhanced app features and broader market reach.

This increasing need for mental health support offers a fertile ground for growth and innovation within the industry. In January 2023, the U.K. government unveiled strategies to address major health conditions, including mental illness and chronic diseases. This government-led focus on mental health contributes to the expansion of the mental health app market as it supports the development of digital tools aimed at managing and improving mental health outcomes.

Impact of Macroeconomic / Geopolitical Factors

Economic downturns or recessions can reduce consumer spending on discretionary services, including digital mental health solutions, thereby dampening market growth. Geopolitical tensions and conflicts may disrupt global supply chains and affect the availability of technological resources, potentially hindering app development and distribution.

Conversely, economic stability and international cooperation can foster investment in healthcare technology and expand market opportunities. Additionally, increased awareness and government initiatives focused on mental health, often influenced by both macroeconomic conditions and geopolitical trends, likely drive positive market momentum. Despite these challenges, a supportive policy environment and increasing recognition of mental health’s importance present promising prospects for continued growth and innovation in the sector.

Latest Trends

Surge in Requirement for Personalized Care

Increasing demand for personalized care drives the mental health apps market forward. Users now seek tailored solutions that cater specifically to their individual mental health needs, prompting developers to create more customized and adaptive features. This trend reflects a broader shift towards individualized healthcare approaches, where consumers expect solutions that address their unique challenges and preferences.

As a result, the market is expected to grow as companies innovate to meet this demand, incorporating advanced technologies like AI and machine learning to enhance personalization. The anticipated rise in user interest in bespoke mental health solutions likely encourages further investment and development in this sector, underscoring the growing importance of personalization in shaping the future of digital mental health services.

In November 2022, the Shanghai Institute of Mental Health and the WHO collaborated to train individuals in China on mental health and well-being. This initiative highlights the global push towards improving mental health education and awareness, which drives the adoption and development of mental health apps as tools for delivering essential information and support on a wide scale.

Regional Analysis

North America is leading the Mental Health Apps Market

North America dominated the market with the highest revenue share of 38.7% owing to the heightened awareness and reduced stigma surrounding mental health issues, leading to greater adoption of digital solutions for emotional support. Increased investment from both private and public sectors has driven innovation, enhancing app features and accessibility.

Additionally, the ongoing integration of mental health services into healthcare systems and workplaces has broadened the user base. The COVID-19 pandemic’s enduring impact has also accelerated the shift towards virtual mental health services as people continue to seek remote support. The National Center for Biotechnology Information (NCBI) reported in November 2022 that 9.2% of Americans experienced severe depressive episodes in 2020, with higher rates among young adults.

This data highlights the urgent need for accessible mental health support, driving demand for mental health apps designed to cater to specific demographic needs and provide targeted interventions. The region’s strong technological infrastructure and high smartphone penetration further support the robust growth of these digital tools, making mental health apps an integral part of the North American healthcare landscape.

Key factors driving market expansion include the rising prevalence of smartphone usage, advancements in network coverage, and growing internet and social media penetration. According to GSMA’s The Mobile Economy Report 2023, smartphone adoption in North America was approximately 84% in 2022 and is projected to reach 90% by 2030.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to rising awareness of mental health issues and increasing smartphone penetration across diverse markets. Governments and non-governmental organizations are projected to invest more in mental health initiatives, encouraging the development and adoption of digital solutions. Economic growth in the region is likely to facilitate greater consumer spending on health and wellness technologies.

Additionally, the growing acceptance of telehealth and digital health solutions in countries like India and China supports market expansion. The integration of culturally relevant content and localized features in apps is expected to enhance user engagement and drive further growth in this burgeoning market.

Moreover, the growth in the mental health apps market in this region is driven by the rising prevalence of mental health issues. For example, the WHO reports that approximately 54 million people in China suffer from depression, while nearly 41 million experience anxiety disorders. Additionally, the WHO estimates that by 2030, around 80% of individuals with depression will seek treatment.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The major players in the Mental Health Apps market are actively engaged in the development and introduction of innovative products, as well as implementing strategic initiatives such as collaborations and partnerships aimed at enhancing their competitive positioning. In January 2022, Mayo Clinic partnered with K Health to utilize Artificial Intelligence in improving hypertension treatment.

This collaboration demonstrates the increasing integration of AI technology in healthcare, including mental health. AI-driven insights and solutions are becoming integral to mental health apps, enhancing their effectiveness and precision in addressing various mental health issues, which drives innovation and growth in the app market.

Top Key Players in the Mental Health Apps Market

- Mindscape

- Calm

- MoodMission Pty Ltd.

- Sanvello Health

- Headspace Inc.

- Youper, Inc.

- Happify

- Bearable

- BetterHelp

- Talkspace

- Diago

Recent Developments

- In September 2023: Headspace and One Medical formed a strategic alliance focused on reducing anxiety and promoting preventive health screenings. This collaboration highlights the increasing demand for integrated solutions that address mental health concerns and emphasizes the role of innovative digital platforms in advancing these goals. The partnership underlines the growing recognition of mental health as a critical component of overall well-being and supports the expansion of mental health app offerings that aim to tackle these issues effectively.

- In October 2022: Diago introduced Unmind, a global mental health app, to its workforce in honor of World Mental Health Day. The app provides a range of tools designed to enhance mental well-being, including interactive courses and evidence-based assessments. This launch reflects a broader trend of companies adopting digital solutions to address mental health, which drives the market for mental health apps as organizations seek to support their employees’ psychological health through accessible and practical resources.

- In September 2022: Headspace Health, a leading online meditation company, acquired Shine App, a mental health and well-being platform. This acquisition underscores the expanding role of digital tools in mental health support and highlights the trend of consolidation in the mental health app market. By integrating Shine App’s resources, Headspace Health aims to offer a more comprehensive range of mental health services, contributing to the growth and diversification of the mental health app industry.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 6.3 Billion |

| Forecast Revenue (2033) | US$ 26.2 Billion |

| CAGR (2024-2033) | 15.3% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Platform Type (iOS, Android, and Others), By Application (Stress Management, Depression & Anxiety Management, Meditation Management, and Others), By End-User (Home Care Settings, Mental Hospitals, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Mindscape, Calm, MoodMission Pty Ltd., Sanvello Health, Headspace Inc., Youper, Inc., Happify, Bearable, BetterHelp, Talkspace, and Diago |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |