Quick Navigation

- Report Overview

- Key Statistics

- Key Takeaways

- China MEMS Automobile Sensors Market Size

- Regional Analysis

- By Sensor Type

- By Application

- Key Market Segments

- Driving Factors

- Restraining Factor

- Growth Opportunities

- Challenging Factors

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

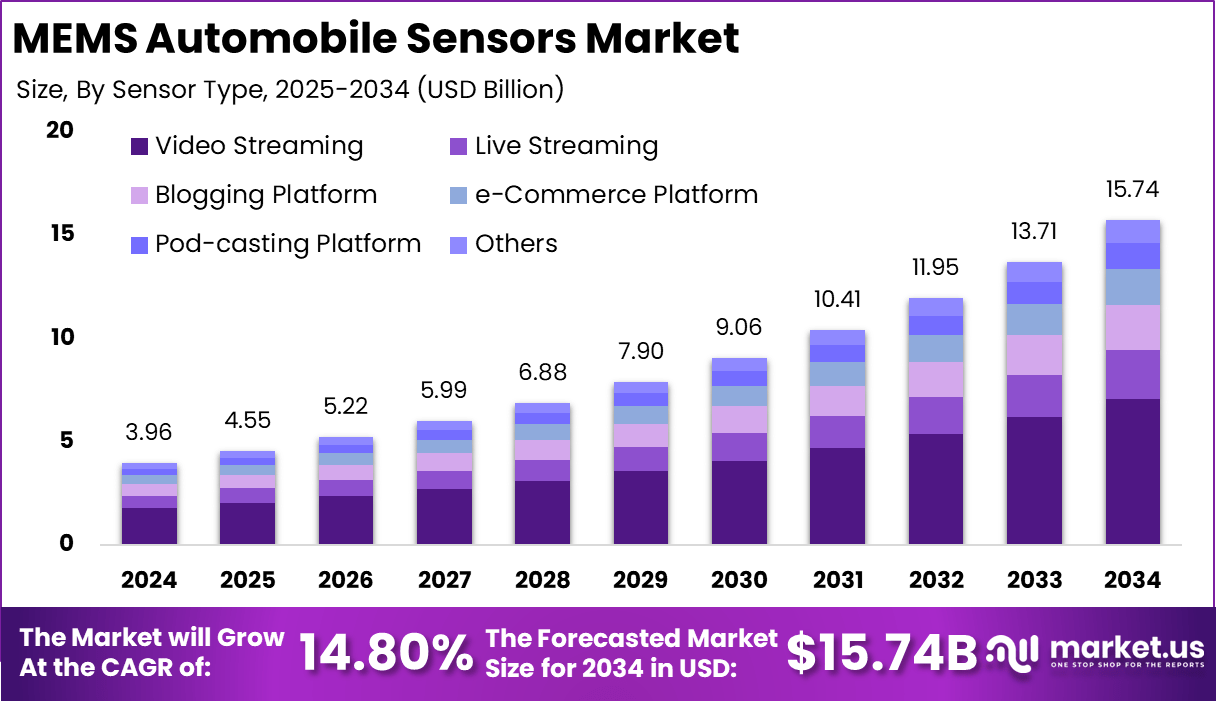

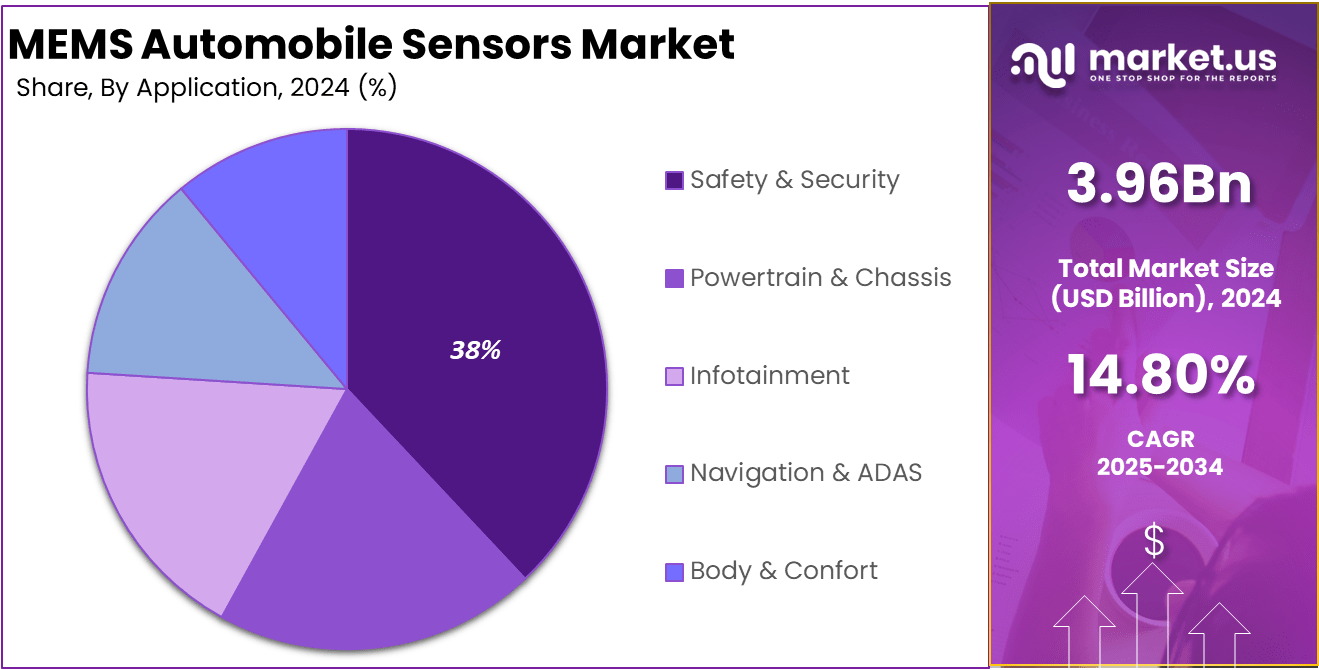

The Global MEMS Automobile Sensors Market size is expected to be worth around USD 15.74 Billion By 2034, from USD 3.96 Billion in 2024, growing at a CAGR of 14.80% during the forecast period from 2025 to 2034.

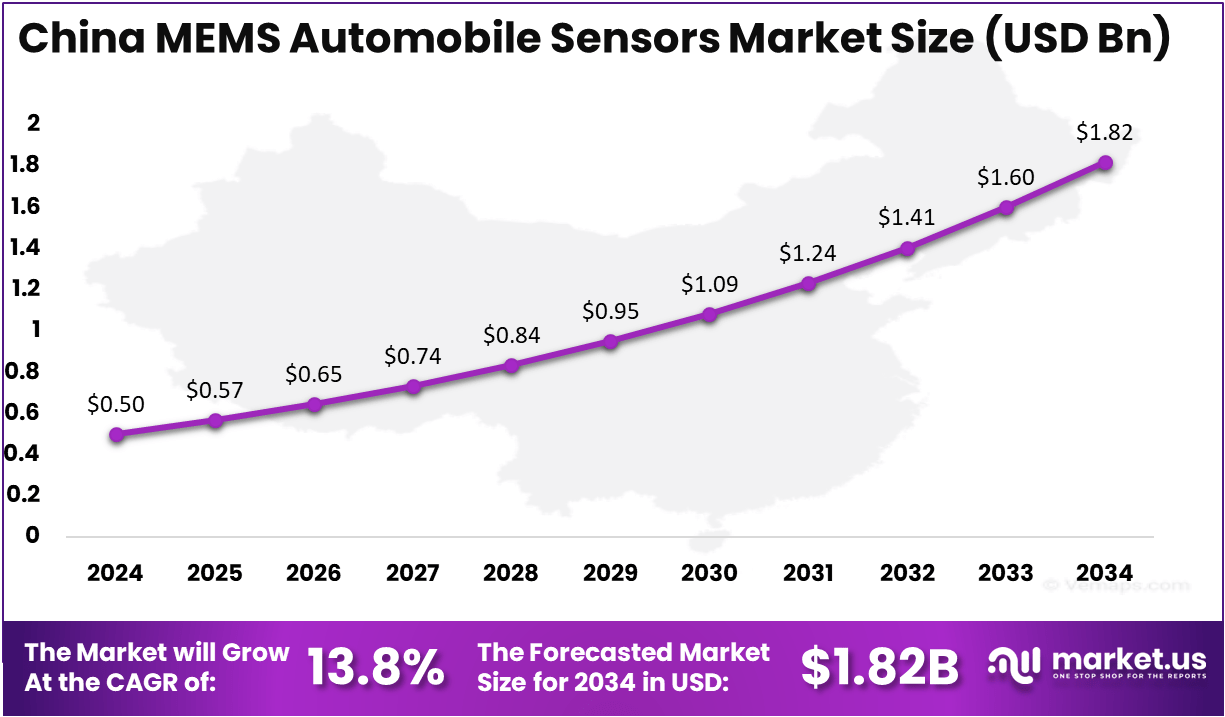

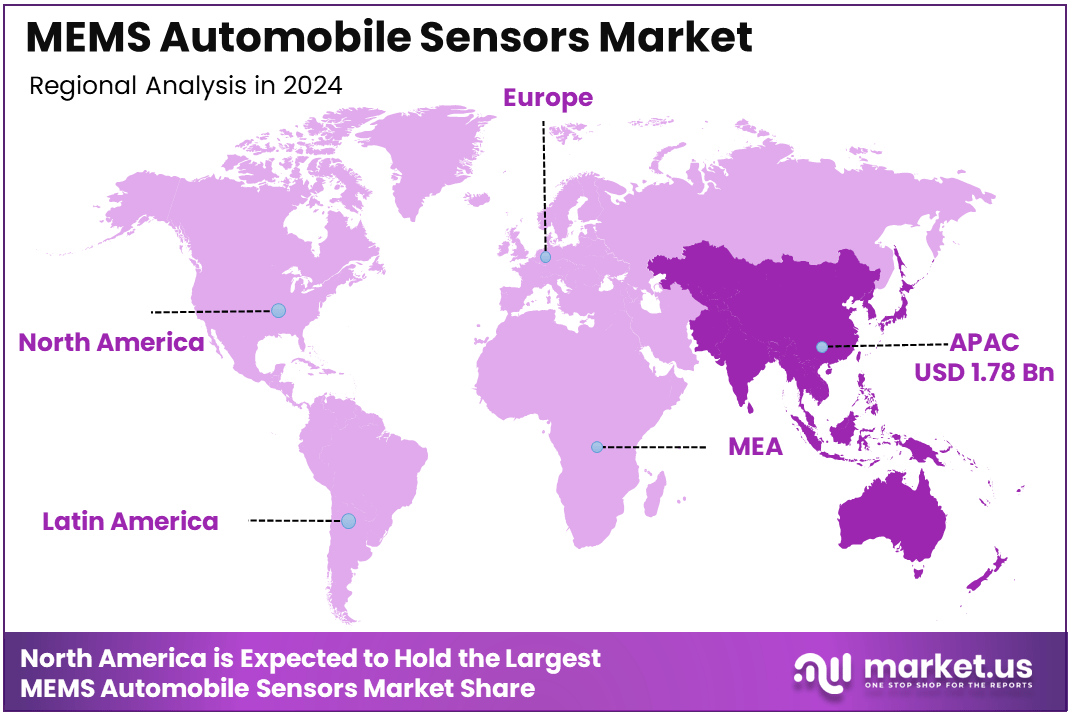

In 2024, Asia-Pacific held a dominant market position, capturing more than a 45% share, holding USD 1.78 Billion in revenue. Further, In Asia-Pacific, China Dominates the market size by USD 0.5 Billion holding a strong position steadily with a CAGR of 13.8%.

MEMS (Microelectromechanical Systems) automobile sensors are small, versatile devices that integrate both mechanical and electrical components on a single microchip. These sensors are designed to measure and detect various physical parameters such as pressure, temperature, acceleration, and speed, providing valuable data to control automotive systems.

MEMS sensors are widely used in advanced driver assistance systems (ADAS), airbag systems, tire pressure monitoring, and engine control units (ECUs). Their small size, high precision, and low power consumption make them ideal for use in the automotive industry. MEMS technology is also essential for enhancing vehicle safety, fuel efficiency, and performance, driving innovation in smart and connected vehicles.

Key Statistics

Sensor Usage and Applications

MEMS sensors are critical in various automotive applications, with the following numerical insights:

- Accelerometers: These sensors account for nearly 40% of the total MEMS sensor market in automotive applications, driven by their essential role in vehicle dynamics measurement.

- Gyroscopes: Representing about 25% of the market, gyroscopes are vital for stability control systems and navigation.

- Microphones: Used in voice recognition systems, they hold a market share of approximately 10%.

Import and Export Data

In terms of trade, the global MEMS sensor market sees substantial import and export activities:

- The United States imports around USD 1.2 billion worth of MEMS sensors annually, primarily from countries like China, Japan, and Germany.

- Exports from the U.S. are valued at approximately USD 800 million, indicating a trade deficit in this sector.

Lifecycle and Quantity

The lifecycle of automotive MEMS sensors typically spans around 5 to 10 years, depending on technological advancements and integration into new vehicle models. The production quantities reflect this demand:

- In 2023, it is estimated that around 500 million MEMS sensors were produced for automotive applications globally.

- By 2032, this number is expected to exceed 1.2 billion units, driven by the increasing adoption of smart vehicles and advanced safety systems.

Market Segmentation by Region

Regionally, the distribution of MEMS sensors in automotive applications is as follows:

- Asia-Pacific: Accounts for approximately 45% of the global market share, with countries like China producing over 200 million units of MEMS sensors annually.

- North America: Holds about 25% of the market share, with the U.S. producing around 100 million units per year.

- Europe: Represents approximately 20%, with production figures nearing 80 million units annually.

Future Projections

Looking ahead, the demand for MEMS sensors is expected to rise significantly due to several factors:

- The growing trend towards electric vehicles (EVs), with projections indicating that by 2030, EVs will account for nearly 30% of total vehicle sales globally.

- The increasing implementation of connected vehicle technologies, which could see the number of connected cars reach approximately 800 million by 2035, further driving the need for advanced sensor technologies.

Several key factors are driving the MEMS automobile sensors market. One of the primary drivers is the increasing demand for safety and performance-enhancing features in modern vehicles. MEMS sensors play a crucial role in systems like airbags, crash detection, and tire pressure monitoring.

Additionally, the shift towards electric vehicles (EVs) and the rising demand for autonomous vehicles are further propelling the market. With EVs and self-driving cars requiring more advanced sensor systems for efficient operation, MEMS technology is gaining significant traction. The growing focus on smart manufacturing and the integration of AI in-vehicle systems also contributes to the rising demand for MEMS sensors.

The demand for MEMS sensors in the automotive sector is driven by the growing need for advanced driver assistance systems (ADAS) and enhanced vehicle safety. With a stronger focus on reducing road accidents and improving fuel efficiency, MEMS sensors are becoming a fundamental part of modern automotive technology.

Additionally, the demand for energy-efficient vehicles and intelligent transportation systems is pushing manufacturers to incorporate MEMS technology into various automotive applications. As vehicles become more connected and smarter, the demand for sensors capable of real-time data processing and communication continues to rise.

The MEMS automobile sensors market offers significant opportunities for growth. As the automotive industry moves towards autonomous vehicles, there will be an increasing need for advanced sensor systems that can detect and respond to various road conditions in real-time. MEMS sensors can provide the required precision and reliability for autonomous driving systems.

Furthermore, as electric vehicles (EVs) become more mainstream, there is an opportunity for MEMS sensors to support various functions, including battery management systems, motor control, and energy efficiency optimization. Additionally, the expansion of smart cities and connected vehicle ecosystems offers a promising opportunity for MEMS sensors in applications related to vehicle-to-everything (V2X) communication.

Technological advancements in MEMS sensors are contributing significantly to their increasing adoption in the automotive sector. Innovations in sensor miniaturization, sensitivity, and integration with other technologies are enabling MEMS sensors to provide more accurate, real-time data for a variety of automotive functions.

Key Takeaways

- Market Growth: The MEMS Automobile Sensors Market is projected to grow from USD 3.96 billion in 2024 to USD 15.74 billion by 2034, at a robust CAGR of 14.80%.

- Sensor Type: Accelerometers dominate the market, holding a significant share of 45% due to their wide use in vehicle safety systems and control applications.

- Application: The Safety & Security application holds a substantial share of 38%, driven by the increasing demand for advanced safety features such as airbag deployment systems, collision avoidance, and driver assistance technologies.

- Regional Leadership: Asia-Pacific holds a dominant market position, capturing over 45% of the global market share, with revenue reaching USD 1.78 billion in 2024. The region’s strong automotive manufacturing base and technological adoption drive this dominance.

- China’s Market Presence: China leads the Asia-Pacific region with a market size of USD 0.5 billion, maintaining a strong growth trajectory with a CAGR of 13.8%, reflecting the rapid adoption of MEMS sensors in the country’s growing automotive industry.

China MEMS Automobile Sensors Market Size

Further, in Asia-Pacific, China dominates the market size with USD 0.5 billion in revenue, holding a strong position steadily with a robust CAGR of 13.8%. This dominance is primarily due to China’s rapidly expanding automotive industry, which is increasingly incorporating MEMS sensors into various vehicle systems.

The country’s push towards electric vehicles (EVs) and autonomous driving technologies has further accelerated the demand for MEMS sensors. In particular, China’s robust manufacturing capabilities, combined with government initiatives promoting smart and green vehicles, create a favorable environment for the growth of MEMS sensor adoption.

Additionally, China’s large consumer base and growing interest in advanced safety features in vehicles are contributing factors to the steady growth in the MEMS automobile sensors market. This growth is further supported by China’s ongoing investments in R&D, which are enhancing the performance and capabilities of MEMS sensors, solidifying the country’s position as a key player in the global automotive sensor market.

Regional Analysis

In 2024, Asia-Pacific held a dominant market position, capturing more than a 45% share, holding USD 1.78 billion in revenue. This region’s leadership in the MEMS automobile sensors market can be attributed to several key factors. Firstly, Asia-Pacific is home to the world’s largest automotive manufacturing hubs, particularly in countries like China, Japan, and South Korea, which are major contributors to the production of vehicles equipped with MEMS sensors.

The region’s automotive industry is rapidly adopting advanced technologies, including electric vehicles (EVs), autonomous driving, and connected cars, which are driving the demand for MEMS sensors in critical systems like safety, engine control, and navigation. In addition to manufacturing, the Asia-Pacific region benefits from strong research and development (R&D) investments.

Companies are continuously innovating MEMS technology to enhance sensor accuracy, reduce power consumption, and improve the overall performance of vehicles. This innovation pipeline is propelling market growth, making the region a key player in the global MEMS automobile sensors market.

The growth of the MEMS automobile sensors market in Asia-Pacific is also supported by the increasing focus on safety and regulatory requirements, particularly for passenger vehicles. As more countries in the region implement stringent safety standards, the demand for MEMS sensors in applications like airbag systems, tire pressure monitoring, and collision detection is expected to rise, further strengthening Asia-Pacific’s market dominance.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

By Sensor Type

In 2024, the Accelerometers segment held a dominant market position, capturing more than a 45% share of the MEMS automobile sensors market. This leadership is largely driven by the widespread adoption of accelerometers in various automotive applications, particularly for safety systems.

Accelerometers are essential in measuring the acceleration and deceleration of vehicles, enabling critical safety features such as airbag deployment, stability control, and collision detection systems. These sensors’ ability to deliver precise motion data in real time makes them indispensable in modern vehicles.

The growing emphasis on vehicle safety and autonomous driving is a significant factor fueling the demand for accelerometers. With increasing regulatory pressure on automakers to improve vehicle safety standards, accelerometers play a crucial role in helping vehicles meet safety certifications and enhance driver protection. Their role in advanced driver-assistance systems (ADAS) is another reason for their dominance in the MEMS sensor market.

Moreover, accelerometers are relatively cost-effective and can be easily integrated into various vehicle systems without significantly impacting the overall cost structure of the vehicle. This affordability and ease of integration make accelerometers a preferred choice for automakers, further reinforcing their market dominance.

By Application

In 2024, the Safety & Security segment held a dominant market position, capturing more than a 38% share of the MEMS automobile sensors market. This significant share is largely driven by the increasing demand for enhanced vehicle safety features.

MEMS sensors, particularly accelerometers and gyroscopes, play a pivotal role in various safety systems such as airbags, collision avoidance, electronic stability control, and advanced driver-assistance systems (ADAS). As consumer demand for safer vehicles grows and regulatory standards tighten, automakers are increasingly relying on MEMS sensors to meet these safety requirements.

The global shift towards autonomous driving is also contributing to the growth of the Safety & Security segment. As autonomous vehicles require precise sensing and data collection for real-time decision-making, MEMS sensors are integral in providing accurate information for systems like automatic braking, lane-keeping assist, and adaptive cruise control.

These safety-critical applications demand highly reliable and sensitive sensors, making MEMS technology a key enabler of autonomous driving. Furthermore, the focus on driver and passenger protection is leading to innovations in MEMS sensor designs, enabling even more sophisticated safety features.

Governments and regulatory bodies are also pushing for improved vehicle safety standards, which is fueling the adoption of MEMS sensors. As a result, the Safety & Security application remains a top priority for both automakers and MEMS sensor manufacturers, securing its dominant position in the market.

Key Market Segments

By Sensor Type

- Accelerometers

- Gyroscopes

- Pressure Sensors

- Magnetic Sources

- Infrared Sensors

- Other Sensors

By Application

- Safety & Security

- Powertrain & Chassis

- Infotainment

- Navigation & ADAS

- Body & Confort

Driving Factors

Increasing Demand for Vehicle Safety Features

The MEMS automobile sensors market is being driven by the increasing demand for advanced vehicle safety features. With road safety becoming a top priority for consumers, manufacturers are under pressure to incorporate cutting-edge technologies that prevent accidents and protect occupants.

This has significantly boosted the adoption of MEMS sensors, especially in systems such as airbags, stability control, and collision detection systems. MEMS accelerometers, gyroscopes, and pressure sensors are critical components in these safety applications. Their ability to measure vehicle dynamics, such as speed, acceleration, and braking, allows automotive systems to react in real-time to prevent accidents.

Regulatory bodies are also playing a significant role in accelerating this trend. Governments worldwide are implementing stricter safety standards for vehicles, including the mandatory inclusion of advanced driver-assistance systems (ADAS) and automatic emergency braking (AEB).

These systems rely heavily on MEMS sensors to function efficiently. For instance, MEMS sensors in airbags trigger immediate deployment when an impact is detected, saving lives and reducing injuries.

Restraining Factor

High Production Costs

Despite the growing demand for MEMS automobile sensors, one of the significant challenges hindering the market’s growth is the high production costs associated with MEMS sensor manufacturing. The advanced technology and precision required for MEMS sensors lead to increased production expenses.

Manufacturing MEMS sensors involves intricate processes, including wafer fabrication, micro-machining, and integration into automotive systems, all of which require specialized equipment and skilled labor. This makes MEMS sensors more expensive compared to traditional sensors, which can discourage cost-sensitive automakers, especially those in emerging markets, from adopting MEMS technology at scale.

Additionally, the miniaturization and complexity of MEMS sensors contribute to higher development and testing costs. Since these sensors are designed to perform accurately in harsh automotive environments—exposed to vibrations, temperature fluctuations, and moisture—their reliability must be thoroughly tested. This testing process adds to the overall cost of production.

Growth Opportunities

Expansion of Autonomous Vehicle Market

A significant growth opportunity for the MEMS automobile sensors market lies in the expansion of the autonomous vehicle (AV) market. Autonomous vehicles are one of the most promising applications of MEMS sensors, as these vehicles require precise and reliable sensors to navigate safely.

MEMS sensors, including accelerometers, gyroscopes, and pressure sensors, are essential for enabling the functionality of critical AV systems, such as obstacle detection, collision avoidance, adaptive cruise control, and lane-keeping assistance.

As governments and private companies continue to invest in autonomous vehicle development, the demand for MEMS sensors is expected to skyrocket. For instance, global tech giants and automotive manufacturers are partnering to roll out self-driving cars in various cities, and many countries are updating infrastructure to support AVs. These vehicles will require increasingly sophisticated MEMS sensors for accurate environmental sensing, real-time decision-making, and system feedback.

Challenging Factors

Competition from Alternative Sensor Technologies

A significant challenge faced by the MEMS automobile sensors market is the competition from alternative sensor technologies. While MEMS sensors are widely used for their small size, low power consumption, and precision, other sensor technologies—such as radar, LiDAR, and vision sensors—are increasingly being adopted in automotive applications.

These sensors, particularly in autonomous driving and ADAS systems, offer certain advantages over MEMS sensors. For example, radar and LiDAR sensors provide better performance in adverse weather conditions, such as fog, rain, or snow, where MEMS sensors may have limited effectiveness.

LiDAR, in particular, has emerged as a key player in autonomous vehicle systems due to its ability to generate high-resolution 3D maps of the vehicle’s surroundings. While MEMS sensors are essential for certain applications like airbag deployment and stability control, they face competition from LiDAR and radar in areas requiring long-range detection and high accuracy, such as object tracking and collision avoidance.

Growth Factors

Expansion of Advanced Driver Assistance Systems (ADAS)

The MEMS automobile sensors market is experiencing substantial growth due to the increasing adoption of Advanced Driver Assistance Systems (ADAS). These systems are designed to improve vehicle safety and automate driving functions, and they rely heavily on MEMS sensors such as accelerometers, gyroscopes, and pressure sensors.

The global market for ADAS is projected to grow at a CAGR of 15% from 2023 to 2030, significantly impacting the MEMS sensor demand. As car manufacturers strive to enhance safety features and comply with stricter regulations, the integration of MEMS sensors into ADAS technologies such as lane-keeping assist, adaptive cruise control, and automatic emergency braking is becoming a top priority.

Emerging Trends

The Rise of Electric and Autonomous Vehicles

As the automotive industry transitions toward electric and autonomous vehicles (EVs and AVs), the demand for MEMS sensors is growing rapidly. MEMS sensors are crucial for the efficient operation of electric vehicles, where precise monitoring of components like battery systems, motor control, and power management is needed.

Additionally, autonomous vehicles require a vast array of sensors for real-time decision-making. As a result, the MEMS sensor market is expected to see a surge in demand from these emerging vehicle technologies. The global electric vehicle market is set to grow at a CAGR of 22% over the next decade, further enhancing the MEMS sensor demand.

Business Benefits

Enhanced Vehicle Efficiency and Performance

The integration of MEMS sensors in automotive systems brings numerous business benefits, primarily by improving vehicle efficiency, safety, and performance. For automotive manufacturers, MEMS sensors enable more precise control of engine performance, reducing fuel consumption and optimizing powertrain systems.

The incorporation of MEMS sensors in safety features like airbags and stability control systems significantly reduces the likelihood of accidents, thus lowering insurance claims and enhancing brand reputation. Additionally, MEMS sensors help streamline manufacturing processes by reducing complexity and cost, leading to more competitive pricing in the market.

With the global automotive market projected to reach USD 4 trillion by 2030, the benefits of MEMS sensors are helping automakers tap into new revenue streams while maintaining compliance with regulatory standards.

Key Players Analysis

Bosch Sensortec, a leading player in the MEMS automobile sensors market, continues to innovate and expand its product portfolio. Bosch, renowned for its expertise in automotive technology, is focusing on the development of high-performance MEMS sensors that cater to applications in safety, powertrain, and comfort. In recent years, Bosch Sensortec has been particularly active in expanding its product range for ADAS and autonomous vehicles.

STMicroelectronics has made significant strides in the MEMS sensor market, particularly in automotive applications. As a major semiconductor company, STMicroelectronics focuses on high-precision MEMS sensors that are integral to vehicle safety and performance. The company’s recent launches include sensors designed for ADAS, including systems for collision avoidance, lane-keeping assistance, and automated driving.

Analog Devices, Inc. has established itself as a key player in the MEMS sensor market, with a strong emphasis on precision and reliability in automotive applications. The company’s MEMS accelerometers and gyroscopes are widely used in safety systems such as airbags and electronic stability control. Recently, Analog Devices has been focusing on expanding its product range with new, advanced MEMS sensors designed to improve the performance of ADAS and autonomous vehicle systems.

Top Key Players in the Market

- Bosch Sensortec (Robert Bosch GmbH)

- STMicroelectronics

- Analog Devices, Inc.

- Murata Manufacturing Co., Ltd.

- Texas Instruments

- Denso Corporation

- NXP Semiconductors

- Honeywell International Inc.

- InvenSense (TDK Corporation)

- Sensata Technologies

- Hitachi Ltd.

- Other Key Players

Recent Developments

- In 2024, Bosch Sensortec launched a new series of MEMS sensors aimed at enhancing vehicle safety features. These sensors, designed for advanced driver-assistance systems (ADAS), provide real-time data for critical applications such as collision avoidance, electronic stability control, and autonomous driving.

- In 2024, STMicroelectronics expanded its portfolio of MEMS sensors with a focus on electric and autonomous vehicles. The company introduced advanced MEMS sensors designed to optimize battery management systems, improve energy efficiency, and enhance vehicle control systems.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 3.96 Bn |

| Forecast Revenue (2034) | USD 15.74 Bn |

| CAGR (2025-2034) | 14.80% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Sensor Type (Accelerometers, Gyroscopes, Pressure Sensors, Magnetic Sources, Infrared Sensors, Other Sensors), By Application (Safety & Security, Powertrain & Chassis, Infotainment, Navigation & ADAS, Body & Confort) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Bosch Sensortec (Robert Bosch GmbH), STMicroelectronics, Analog Devices, Inc., Murata Manufacturing Co., Ltd., Texas Instruments, Denso Corporation, NXP Semiconductors, Honeywell International Inc., InvenSense (TDK Corporation), Sensata Technologies, Hitachi Ltd., Other Key Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |