Quick Navigation

Report Overview

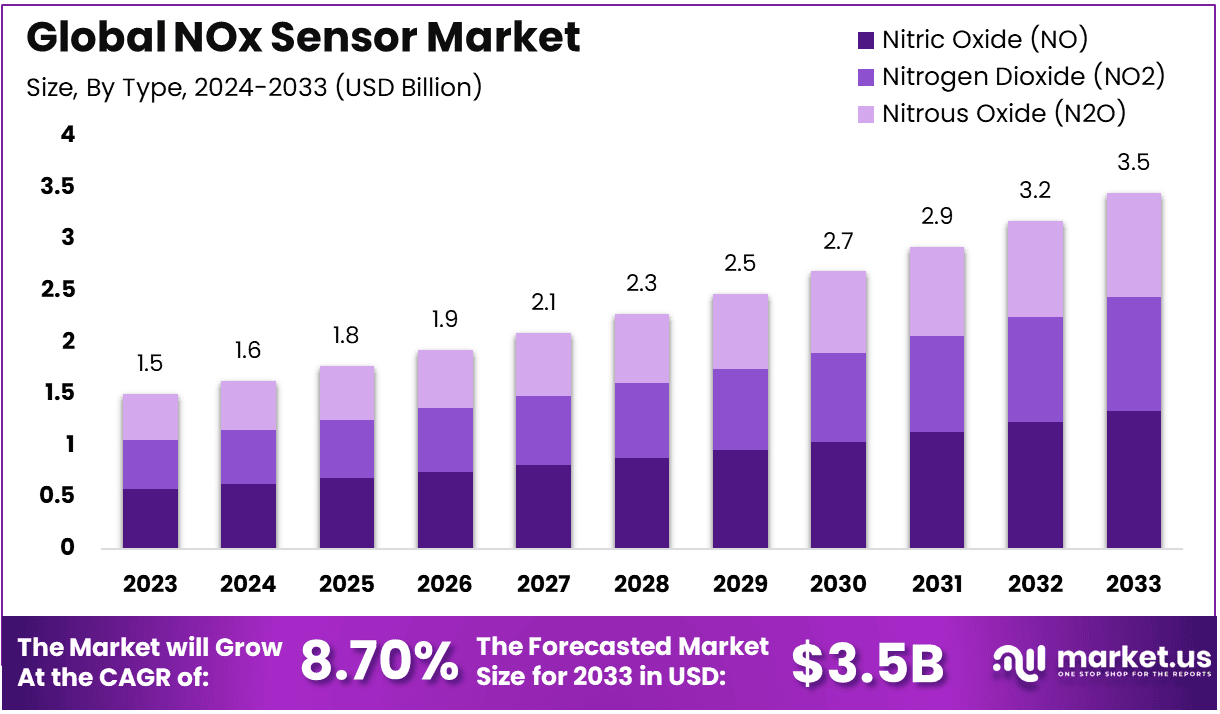

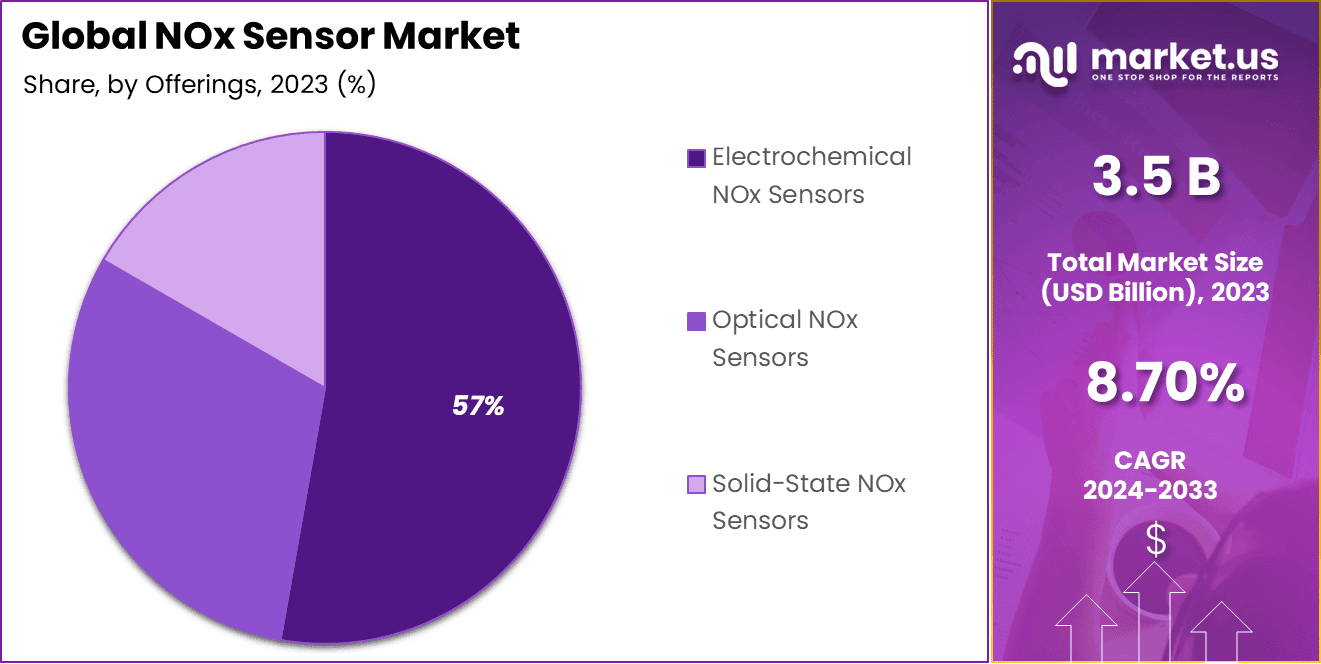

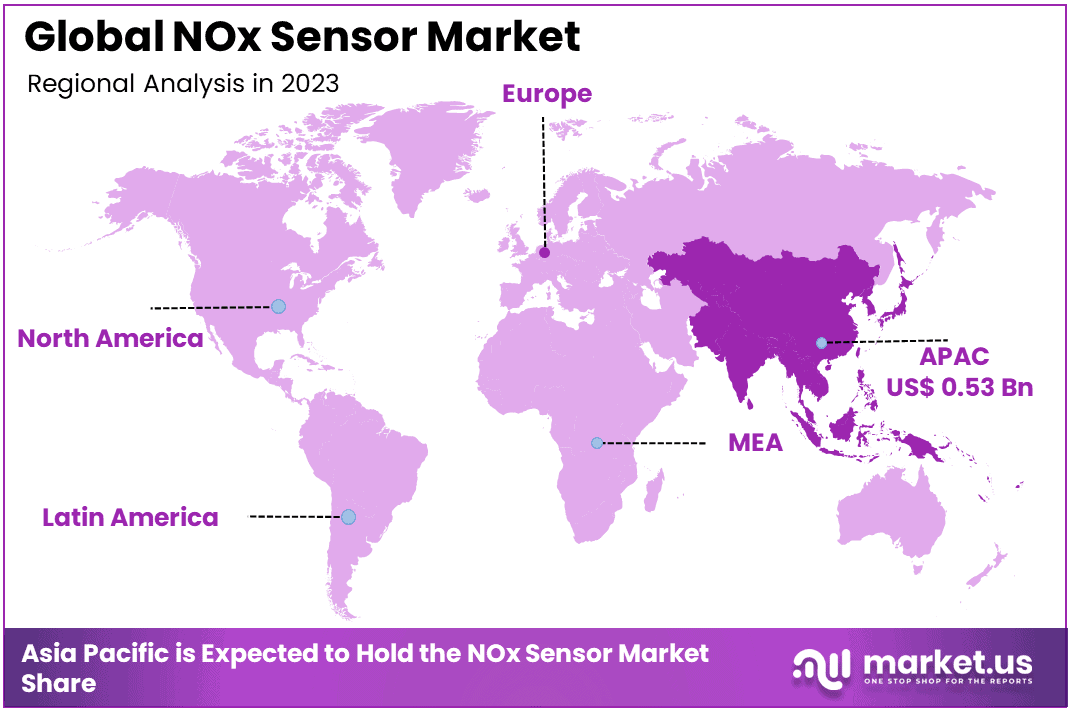

The Global NOx Sensor Market size is expected to be worth around USD 3.5 Billion By 2033, from USD 1.5 Billion in 2023, growing at a CAGR of 8.70% during the forecast period from 2024 to 2033. In 2023, Asia Pacific held a dominant market position, capturing more than a 35.4% share, holding USD 0.53 Billion in revenue.

A NOx sensor is a device used to detect and measure nitrogen oxide (NOx) emissions in various environments, primarily in automotive and industrial applications. NOx refers to a group of gases, including nitric oxide (NO) and nitrogen dioxide (NO₂), which are produced during the combustion of fossil fuels.

These sensors are crucial for monitoring and controlling the emission levels of NOx to ensure compliance with environmental regulations, especially in the context of automotive engines and industrial processes. In vehicles, NOx sensors are typically part of the exhaust system, helping to reduce emissions and improve air quality. As governments worldwide impose stricter emissions standards, the use of NOx sensors has become integral to managing air pollution and achieving sustainability targets.

The NOx sensor market is growing rapidly, driven by increasing environmental concerns and tightening emission regulations across various industries. In recent years, the demand for NOx sensors has surged, particularly in the automotive sector, as manufacturers strive to meet stringent emissions standards such as the Euro 6 (Europe) and Bharat Stage VI (India).

The market is expected to expand as the adoption of electric vehicles (EVs) and hybrid technologies, which also require precise NOx measurements for efficient engine management, continues to rise. The market is also benefiting from growth in the industrial sector, particularly in power generation, manufacturing, and oil & gas, where NOx emissions need to be monitored and reduced.

The primary driver of the NOx sensor market is the growing global emphasis on reducing air pollution and combating climate change. Stringent environmental regulations in Europe, North America, and Asia-Pacific are pushing industries to adopt technologies that can minimize harmful emissions.

Additionally, the increased production of electric vehicles (EVs) and hybrid cars, which use NOx sensors for engine optimization, is fueling market demand. Governments are also providing incentives for the development of cleaner technologies, boosting the need for NOx-sensing solutions.

The demand for NOx sensors is driven by various factors, including stricter emission norms, technological advancements in automotive engines, and the growing need for real-time emissions monitoring. In the automotive sector, the shift towards more fuel-efficient and lower-emission vehicles has led to an increased installation of NOx sensors. Moreover, as industrial sectors such as power plants and manufacturing facilities also face regulatory pressure, the demand for NOx sensors to monitor and control emissions is expected to grow.

The NOx sensor market presents significant opportunities in the automotive and industrial sectors. With the rise in electric vehicles and stricter emission regulations, automotive manufacturers will increasingly rely on NOx sensors to comply with environmental standards. Additionally, the adoption of NOx sensors in industrial sectors to optimize fuel usage and reduce emissions offers a substantial market opportunity. There is also potential for new developments in sensor technology, including improved sensor accuracy, durability, and affordability, which could drive market growth.

Recent advancements in NOx sensor technology include the development of more sensitive, accurate, and durable sensors. For example, new sensor designs can operate in harsh environments, withstand high temperatures, and provide real-time monitoring of NOx levels with greater precision.

Furthermore, the integration of NOx sensors with onboard diagnostic systems (OBD) in vehicles and advanced emissions monitoring systems in industries is enhancing the overall efficiency of emissions control. With the advancement of wireless communication technologies, sensors are now capable of transmitting data remotely, which makes monitoring and managing emissions more streamlined and efficient.

The demand for NOx sensors is primarily driven by the increasing production of vehicles, which reached 85.4 million units globally in 2022, marking a 5.7% increase from the previous year. NOx sensors play a vital role in monitoring and controlling nitrogen oxide emissions, which are strictly regulated due to their harmful environmental effects.

These sensors are categorized into upstream and downstream types; the downstream sensors accounted for over 60% of the market share in 2023. They are essential for ensuring compliance with stringent emission standards such as Euro 6 and Tier 3, as they provide real-time feedback on the performance of NOx reduction technologies.

In terms of application, diesel engines dominate the market segment for NOx sensors, with projections indicating that this segment could be worth around USD 900 million by 2032. This is largely due to the higher NOx emissions from diesel engines compared to gasoline engines, coupled with increasing regulatory pressures for effective emission control solutions.

Key Takeaways

- The global NOx sensor market is projected to experience significant growth, expanding from USD 1.5 billion in 2023 to USD 3.5 billion by 2033, reflecting a robust CAGR of 8.7% over the next decade.

- The electrochemical NOx sensors segment held the largest share in 2023, accounting for 57% of the market, driven by their high accuracy, reliability, and wide adoption in emission control applications.

- Nitric Oxide (NO) sensors were the dominant sensor type in 2023, representing 38.6% of the market share, largely due to their importance in vehicle emissions testing and industrial applications.

- The passenger vehicle segment led the market in terms of application, contributing 65% to the market share in 2023. This is driven by increasing vehicle production and tightening emission regulations in regions like Europe, North America, and Asia-Pacific.

- Asia-Pacific region held the largest regional share of the NOx sensor market in 2023, accounting for 35.4% of the total revenue, owing to rapid industrial growth, rising automotive production, and stringent emission norms in countries such as China and India.

By Types

In 2023, the Nitric Oxide (NO) segment held a dominant market position, capturing more than a 38.6% share. This dominance can be attributed to the prevalent use of nitric oxide sensors in a wide range of applications, particularly in the automotive and industrial sectors. Nitric oxide is a major pollutant emitted from vehicle exhaust systems and industrial processes, making its detection and regulation a key focus for both manufacturers and regulators. The high demand for nitric oxide sensors is driven by the need to monitor and control NO emissions, which is essential for meeting increasingly stringent environmental standards worldwide.

The significant share of the Nitric Oxide (NO) segment is further supported by its role in advanced emission control systems, especially in the automotive industry. With the growing push for cleaner transportation and the implementation of regulations such as Euro 6 and EPA standards, NOx sensors that specifically detect nitric oxide have become critical components in the development of low-emission vehicles. These sensors help optimize the performance of catalytic converters and other emission reduction technologies, ensuring vehicles meet the required limits for NOx emissions.

While other types of NOx sensors, such as those for Nitrogen Dioxide (NO2) and Nitrous Oxide (N2O), also play an important role in emission monitoring, the demand for Nitric Oxide (NO) sensors remains the highest due to the large proportion of NO in vehicle and industrial exhaust gases. NO is a key contributor to air pollution and smog formation, and its real-time monitoring is vital for effective environmental protection. Additionally, nitric oxide sensors offer cost-effective solutions with robust performance, making them the preferred choice for both light-duty and heavy-duty vehicles.

By Offerings

In 2023, the Electrochemical NOx Sensors segment held a dominant market position, capturing more than a 57% share. This dominance can be attributed to the widespread adoption of electrochemical sensors across various industries, particularly in the automotive sector. Electrochemical sensors are favored for their high accuracy, compact design, and cost-effectiveness, making them ideal for monitoring NOx emissions in vehicles and industrial applications. Their ability to operate in a wide range of environmental conditions and provide reliable measurements has further contributed to their leading position in the market.

Electrochemical sensors offer several advantages, including faster response times and greater durability compared to other sensor types. These features are especially important in the automotive industry, where NOx emissions must be closely monitored to comply with stringent environmental regulations. The growing demand for cleaner and more efficient vehicles has driven the widespread adoption of electrochemical NOx sensors in both passenger and commercial vehicles. Additionally, their effectiveness in detecting low concentrations of NOx, which is critical for meeting regulatory limits, has enhanced their appeal.

Although other sensor types, such as Optical NOx Sensors and Solid-State NOx Sensors, are also gaining traction, they have yet to achieve the widespread adoption seen by electrochemical sensors. Optical sensors, while highly accurate, are generally more expensive and less versatile in certain industrial applications. Solid-state sensors, on the other hand, are still in the developmental phase and are typically used in more specialized applications. In contrast, electrochemical sensors strike a balance between performance, cost, and scalability, making them the preferred choice across a variety of industries.

By Applications

In 2023, the Passenger Vehicle segment held a dominant market position, capturing more than 65% of the share in the global NOx sensor market. This leadership is largely driven by the significant adoption of emission control technologies in passenger vehicles, spurred by stringent environmental regulations worldwide. Passenger vehicles, particularly those with internal combustion engines (ICE), are major contributors to nitrogen oxide (NOx) emissions, which are harmful to air quality and public health. As governments across regions, including Europe, North America, and Asia Pacific, continue to implement stricter emissions standards, such as Euro 6 and the U.S. EPA regulations, there has been a surge in demand for advanced NOx sensors that can precisely monitor and control these emissions.

The Passenger Vehicle segment’s dominance is also attributed to the increasing emphasis on sustainability and fuel efficiency in the automotive industry. Modern passenger vehicles are equipped with advanced emission control systems, including selective catalytic reduction (SCR) and lean NOx traps (LNT), which rely heavily on the use of NOx sensors for optimal performance. These sensors ensure that the vehicle meets regulatory standards, improves fuel efficiency, and reduces the overall environmental footprint of the vehicle. As consumer preference continues to shift towards eco-friendly and energy-efficient vehicles, the demand for precise NOx sensing technology will only intensify.

Furthermore, the rise in the adoption of electric vehicles (EVs) is also expected to influence the Passenger Vehicle segment, although EVs do not directly emit NOx. As part of the broader transition to greener transportation solutions, hybrid and plug-in hybrid vehicles that still rely on internal combustion engines are increasingly incorporating NOx sensors to ensure their emissions stay within regulatory limits. This transition further drives growth in the passenger vehicle market, as automakers seek to enhance their compliance with emission regulations while offering consumers cleaner and more efficient vehicle options.

Key Market Segments

By Offerings

- Optical NOx Sensors

- Electrochemical NOx Sensors

- Solid-State NOx Sensors

By Type

- Nitric Oxide (NO)

- Nitrogen Dioxide (NO2)

- Nitrous Oxide (N2O)

By Application

- Passenger Vehicle

- Commercial Vehicle

Driving Factors

Increasing Stringency of Emission Regulations

One of the primary drivers for the growth of the NOx sensor market is the rising stringency of global emission regulations. Governments worldwide are implementing stricter emission standards to mitigate air pollution and address the environmental and health impacts caused by nitrogen oxide (NOx) emissions from vehicles, industrial plants, and other sources. In particular, the automotive industry has been a focal point of regulatory efforts, with authorities like the European Union, the U.S. Environmental Protection Agency (EPA), and the Chinese government tightening regulations around the permissible levels of NOx emissions.

For example, the European Union’s Euro 6 standards, which limit the amount of NOx emitted by passenger vehicles, have been a significant catalyst in the adoption of NOx sensors in vehicles. Similarly, the U.S. EPA’s Tier 3 standards and the Clean Air Act have pushed automakers to adopt more advanced emission control technologies. These regulations mandate the use of NOx sensors in both gasoline and diesel vehicles to monitor emissions in real-time and ensure compliance with environmental standards. The global push for cleaner air has driven not only the adoption of NOx sensors but also the continuous innovation in sensor technologies, leading to more efficient, accurate, and durable devices.

As industries such as transportation, manufacturing, and power generation continue to face increasing pressure to reduce their environmental footprint, the demand for NOx sensors will remain high. Moreover, these sensors are critical components in technologies like Selective Catalytic Reduction (SCR) and Lean NOx Traps (LNT), which help to reduce NOx emissions in vehicles. As a result, stringent emission standards are expected to be a major driver in the continued expansion of the NOx sensor market, leading to both increased market adoption and technological innovation.

Restraining Factors

High Cost of Advanced NOx Sensor Technologies

Despite the growing demand for NOx sensors, a significant restraint in the market is the high cost associated with advanced sensor technologies. NOx sensors, especially those used in automotive and industrial applications, can be expensive to manufacture, install, and maintain. These sensors rely on sophisticated materials, such as electrochemical cells and semiconductor components, which contribute to their overall cost. For industries that operate on tight margins, such as small and medium-sized automotive manufacturers, the adoption of these sensors can be a financial burden.

For instance, high-performance electrochemical NOx sensors, which are used in modern vehicles to comply with strict emission standards, require a substantial investment in research and development to ensure they deliver accurate and reliable readings under diverse operating conditions. This cost is passed on to consumers in the form of higher vehicle prices. In addition, maintenance and calibration of NOx sensors can add to the overall cost of ownership, further discouraging widespread adoption, particularly in cost-sensitive markets or applications.

For industries like transportation and power generation, where NOx emissions need to be monitored on a large scale, the cost of implementing NOx sensors across fleets of vehicles or industrial facilities can be prohibitively high. As a result, businesses may be reluctant to invest in NOx sensor technologies, particularly in developing regions where budget constraints are more significant. Overcoming this financial barrier and making NOx sensors more affordable will be key to unlocking the full potential of the market.

Growth Opportunities

Growth of Electric and Hybrid Vehicles

The growing adoption of electric and hybrid vehicles (EVs and HEVs) presents a significant opportunity for the NOx sensor market. While electric vehicles do not produce NOx emissions, hybrid vehicles, which combine internal combustion engines with electric motors, still rely on traditional engines for power generation. As the shift toward more sustainable transportation solutions accelerates, hybrid vehicles are expected to become a critical component of the global automotive market. This presents a unique opportunity for NOx sensor manufacturers, as these vehicles will continue to require sensors to monitor and control their emissions.

In addition, as global automotive manufacturers expand their portfolios of electric and hybrid vehicles, the demand for more efficient and advanced NOx sensors is expected to grow. Hybrid vehicles that rely on gasoline or diesel engines for longer-range capabilities will require precise NOx sensors to reduce emissions and meet regulatory standards. This means that even as electric vehicles become more prevalent, the hybrid vehicle segment will continue to require robust emission monitoring solutions, ensuring a sustained demand for NOx sensors.

Furthermore, government incentives and policies aimed at reducing the environmental impact of transportation are likely to accelerate the adoption of hybrid and electric vehicles. In countries where EV adoption is still in its early stages, hybrids serve as a bridge technology, helping to meet emissions targets while still offering the flexibility of an internal combustion engine. As a result, NOx sensor manufacturers have a significant opportunity to position themselves as key suppliers in the evolving automotive ecosystem, meeting the demands of hybrid vehicle manufacturers and regulators alike.

Challenging Factors

Technological Advancements and Integration

One of the primary challenges in the NOx sensor market is the rapid pace of technological advancements and the complexity of sensor integration. As emission standards become more stringent, the demand for more accurate, durable, and efficient NOx sensors increases. This places pressure on manufacturers to develop sensors that not only meet regulatory requirements but also perform effectively in diverse and challenging environments.

The integration of advanced NOx sensors into existing emission control systems, such as Selective Catalytic Reduction (SCR) and Lean NOx Traps (LNT), presents another challenge. As vehicles and industrial systems become more complex, the ability to seamlessly integrate NOx sensors with other components, such as exhaust gas recirculation (EGR) systems and aftertreatment technologies, becomes increasingly difficult. Furthermore, the sensors must be able to operate reliably under extreme conditions, including high temperatures and pressures, which require continuous innovation in materials and design.

Another challenge lies in the need for ongoing calibration and maintenance. NOx sensors must be periodically calibrated to ensure accurate readings and compliance with regulatory standards. This adds to the cost and complexity of their deployment, particularly for industries with large fleets or facilities. Additionally, the long-term reliability of NOx sensors remains a concern, as sensors can degrade over time due to exposure to harsh operating environments. Addressing these challenges requires ongoing investment in research and development to create sensors that are not only more accurate but also more durable and cost-effective, ensuring that they meet the evolving needs of industries and governments.

Growth Factors

The NOx sensor market has been witnessing significant growth driven by several key factors. One of the primary growth drivers is the increasing global focus on reducing air pollution and improving air quality. Stringent environmental regulations, particularly in the automotive and industrial sectors, are pushing for the adoption of advanced emission control technologies.

Countries and regions with high pollution levels, such as China, India, and the European Union, have set stricter standards for nitrogen oxide (NOx) emissions, which has driven the demand for NOx sensors. Additionally, the growing adoption of electric and hybrid vehicles, which require more sophisticated emission management systems, is also fueling market expansion. The rising awareness of environmental sustainability and the push for cleaner energy sources are expected to continue driving demand for NOx sensors over the coming years.

Emerging Trends

In the NOx sensor market, several emerging trends are shaping its future. One of the most notable trends is the increasing integration of NOx sensors with advanced emission control technologies like Selective Catalytic Reduction (SCR) and Lean NOx Traps (LNT). These systems help reduce NOx emissions from diesel engines, and their integration with NOx sensors is becoming more advanced and sophisticated.

Another key trend is the growing adoption of solid-state NOx sensors, which offer improved accuracy, durability, and response time compared to traditional electrochemical sensors. With the rise in smart cities and the Internet of Things (IoT), there is also a growing demand for real-time emission monitoring and data analytics, which is pushing the development of more connected and automated NOx sensing solutions.

Business Benefits

For businesses, adopting NOx sensors offers significant benefits, both in terms of regulatory compliance and operational efficiency. Companies in the automotive, industrial, and power sectors face increasing pressure to comply with government regulations concerning air quality and emissions. By integrating NOx sensors into their systems, businesses can ensure they meet emission standards and avoid costly fines or penalties.

Furthermore, the use of NOx sensors enables more efficient operation of emission control systems, improving fuel efficiency, reducing operational costs, and extending the lifespan of critical components. The data gathered by NOx sensors can also be used to optimize performance and identify areas for improvement, contributing to enhanced overall operational efficiency. These benefits are driving the adoption of NOx sensors in various industries, especially in regions with stringent environmental regulations.

Regional Analysis

In 2023, Asia Pacific held a dominant market position in the NOx sensor market, capturing more than 35.4% of the global market share, with a revenue of USD 0.53 billion. The region’s strong performance can be attributed to the rapid industrialization, urbanization, and the growing number of vehicles, particularly in countries like China and India. Asia Pacific has seen a significant increase in the adoption of stringent environmental policies, which has accelerated the demand for NOx sensors, particularly in the automotive sector. Furthermore, the increasing focus on improving air quality and reducing emissions has driven the need for advanced emission control technologies, such as NOx sensors, in the region. China, being the largest automotive market in the world, continues to play a key role in this growth.

North America, with its robust regulatory environment, also holds a significant share of the NOx sensor market. In 2023, the region accounted for over 20% of the market, driven by stringent emission standards set by governments, particularly the United States. The growing demand for both passenger and commercial vehicles equipped with advanced emission control systems has spurred market growth. Additionally, the increasing adoption of electric and hybrid vehicles, which require sophisticated emissions management, is further driving the demand for NOx sensors in the region. The presence of major automotive manufacturers, coupled with advancements in sensor technologies, strengthens North America’s market position.

Europe follows closely as another key region, accounting for around 25% of the global market share. Europe’s commitment to environmental sustainability, including the European Union’s strict emission regulations, has pushed automotive manufacturers to adopt NOx sensors as part of their compliance strategies. The region is also witnessing growth in industrial applications where NOx sensors are essential for meeting stringent air quality standards. The transition to electric vehicles and hybrid technologies in Europe further boosts the demand for high-performance NOx sensors.

In Latin America and Middle East & Africa, the market share remains relatively small compared to the leading regions, but these markets are expected to experience gradual growth in the coming years. Factors such as improving air quality awareness, increasing industrialization, and stricter environmental regulations are expected to drive adoption in these regions. The demand for NOx sensors in these areas is also linked to the growing automotive and transportation sectors, which are aligning with global environmental trends.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

Continental AG, a global leader in automotive technology, has significantly strengthened its position in the NOx sensor market through strategic acquisitions and product development. In 2023, the company reported a 5.4% increase in revenue from its emissions control solutions, which includes NOx sensor technology. Continental’s acquisition of Vitesco Technologies’ sensor division has enabled the company to enhance its sensor technology, increasing its capacity to develop advanced NOx sensors for both passenger and commercial vehicles.

Bosch, another major player in the NOx sensor market, continues to expand its portfolio with cutting-edge technology. In 2023, Bosch launched its next-generation NOx sensor, designed to offer superior accuracy and performance, meeting the Euro 7 emissions standards. Bosch reported that its automotive division, which includes NOx sensors, generated approximately €40.5 billion in revenue in 2023, contributing to a significant portion of its global automotive sales. The company’s NOx sensors are used in more than 200 million vehicles worldwide, further solidifying Bosch’s dominance in the market.

Delphi Technologies, now part of BorgWarner, has made significant advancements in NOx sensor technology. In 2023, Delphi reported a 6.7% year-over-year increase in revenue from its emissions products, which include NOx sensors, as part of its automotive solutions segment. Delphi’s new range of NOx sensors is designed for both passenger vehicles and heavy-duty commercial trucks. The company has integrated smart sensor technologies that are more durable and cost-effective.

Top Key Players in the Market

- Continental AG

- Bosch

- Delphi Technologies

- Denso Corporation

- Honeywell

- NGK Insulators, Ltd.

- Sensata Technologies

- Amphenol Advanced Sensors

- Hella GmbH & Co. KGaA

- Other Key Players

Recent Developments

- In March 2024, Bosch launched its new generation of NOx sensors, which are designed to meet the latest Euro 7 emission standards.

- In February 2024, Continental AG expanded its sensor portfolio with the introduction of a new NOx sensor aimed at electric and hybrid vehicles.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 1.5 Bn |

| Forecast Revenue (2033) | USD 3.5 Bn |

| CAGR (2024-2033) | 8.70% |

| Largest Market | Asia Pacific |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Offering (Optical NOx Sensors, Electrochemical NOx Sensors, Solid-State NOx Sensors), By Type (Nitric Oxide (NO), Nitrogen Dioxide (NO2), Nitrous Oxide (N2O)), By Application (Passenger Vehicle, Commercial Vehicle) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Continental AG, Bosch, Delphi Technologies, Denso Corporation, Honeywell, NGK Insulators, Ltd., Sensata Technologies, Amphenol Advanced Sensors, Hella GmbH & Co. KGaA, Other Key Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |