Quick Navigation

Report Overview

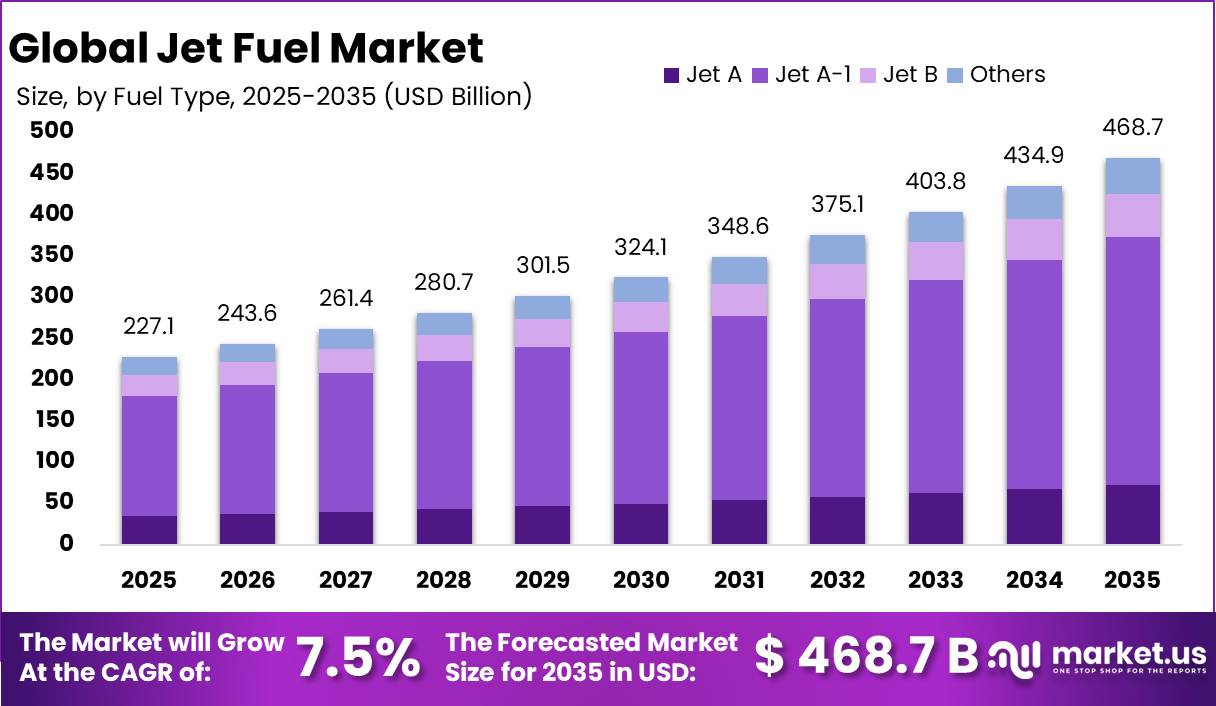

The Global Jet Fuel Market size is expected to be worth around USD 468.7 Billion by 2035, from USD 227.1 Billion in 2025, growing at a CAGR of 7.5% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 37.4% share, holding USD 84.8 Billion revenue.

Jet fuel remains a strategically important aviation energy product, used mainly in turbine-powered aircraft and still dominated by fossil kerosene, while sustainable aviation fuel is emerging as the industry’s main low-carbon substitute. In 2025, the International Energy Agency estimated global jet/kerosene demand at 7.7 million barrels per day, up 2.1% year over year, although still 180,000 barrels per day below 2019 levels.

Key Takeaways

- Jet Fuel Market size is expected to be worth around USD 468.7 Billion by 2035, from USD 227.1 Billion in 2025, growing at a CAGR of 7.5%.

- Jet A-1 held a dominant market position, capturing more than a 64.1% share of the global jet fuel market.

- Into-Plane (On-Airport) held a dominant market position, capturing more than a 72.6% share of the global jet fuel market.

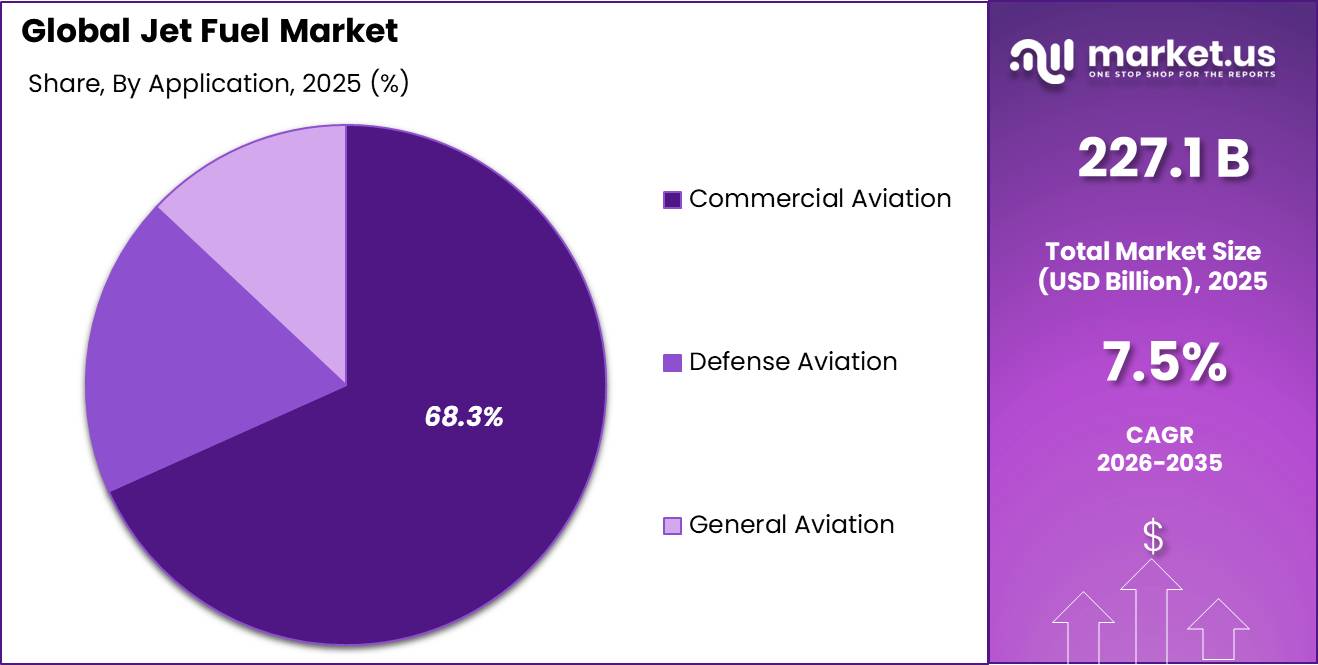

- Commercial Aviation held a dominant market position, capturing more than a 68.3% share of the global jet fuel market.

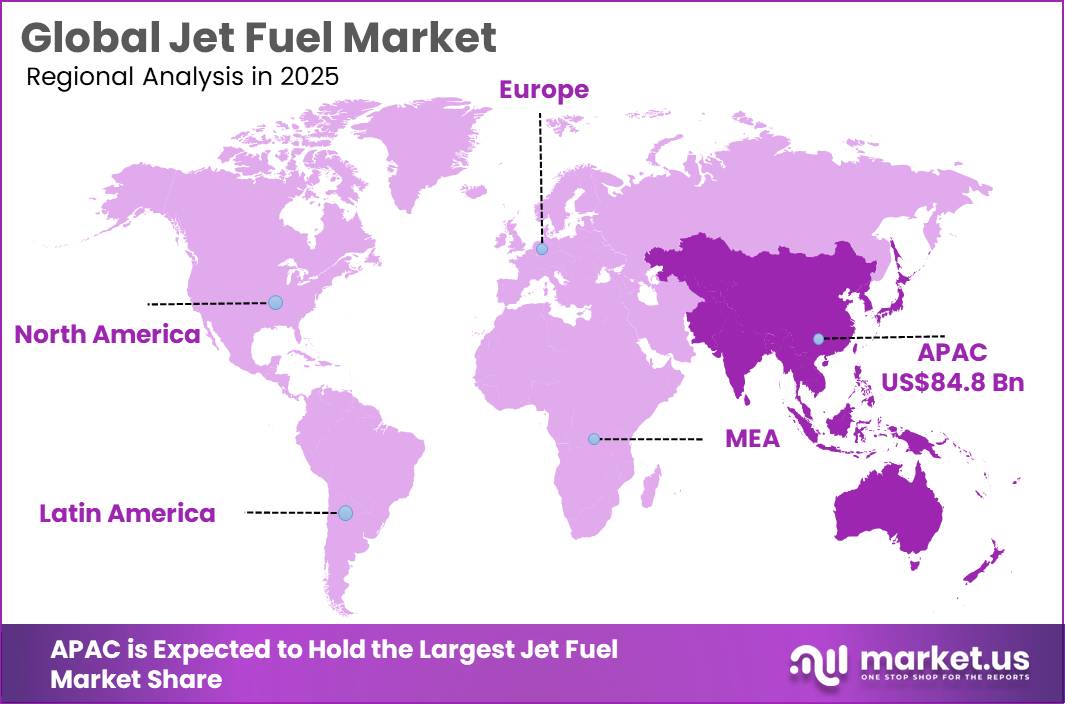

- Asia-Pacific held a dominant position in the global jet fuel market, accounting for 37.4% of the total market share and reaching a market value of USD 84.8 billion.

The industrial scenario is being shaped by airline traffic, refinery availability, fuel-price volatility, and decarbonization mandates. IATA expected 2025 SAF output to reach 1.9 million tonnes, equal to only 0.6% of global jet fuel use, showing that conventional jet fuel will remain dominant while SAF scales from a small base. Aviation’s net-zero pathway is also driving investment, as IATA estimates SAF could deliver about 65% of the emissions reduction needed for aviation to reach net-zero CO₂ by 2050.

Demand is being driven by air traffic recovery, fleet expansion and trade-linked cargo movement. Airbus expects passenger traffic to grow 3.6% annually over 20 years and forecasts 43,400 new aircraft deliveries by 2044, including 34,250 single-aisle and 9,170 widebody aircraft. ICAO also set an aspirational goal to cut international aviation CO₂ emissions by 5% by 2030 through SAF, low-carbon aviation fuels and cleaner energy.

Sustainable aviation fuel is the clearest future opportunity. IATA estimated 2025 SAF production at about 2 million tonnes, equal to only 0.7% of total airline fuel consumption, showing a major supply gap and long-term investment need. SAF can cut lifecycle CO₂ emissions by up to 80% compared with conventional jet fuel, depending on feedstock and process.

Government policy is accelerating demand. The EU’s ReFuelEU Aviation rule requires at least 2% green aviation fuel from 2025, rising to 6% in 2030, 20% in 2035 and 70% by 2050. SAF Grand Challenge targets 3 billion gallons per year by 2030 and 35 billion gallons by 2050, with at least 50% lifecycle emissions reduction.

Shell plc remains active in aviation fuels and SAF commercialization. In 2025, Kintetsu World Express signed a new agreement with Shell Aviation for SAF use, strengthening corporate demand for lower-emission air logistics. Shell’s Avelia platform also facilitated more than 41 million gallons of SAF across 17 airports by mid-2025.

By Fuel Type Analysis

Jet A-1 dominates with 64.1% share due to its wide usage in commercial aviation and international flight operations

In 2025, Jet A-1 held a dominant market position, capturing more than a 64.1% share of the global jet fuel market. The strong demand for Jet A-1 was mainly supported by the continuous rise in international air travel and the growing number of long-haul commercial flights across regions such as Asia-Pacific, Europe, and the Middle East. Airlines preferred Jet A-1 because of its better freezing point and suitability for high-altitude operations, making it the standard fuel for most international aircraft fleets. The fuel also remained widely available across major global airports, which helped airlines maintain operational efficiency and reduce fueling complications during cross-border operations.

By Distribution Channel Analysis

Into-Plane (On-Airport) leads with 72.6% share due to faster aircraft turnaround and direct airport fueling access

In 2025, Into-Plane (On-Airport) held a dominant market position, capturing more than a 72.6% share of the global jet fuel market by distribution channel. The segment maintained its strong position because most commercial and cargo aircraft depend on direct airport fueling systems for efficient operations. Airlines continued to prefer into-plane services as they help reduce delays, improve turnaround time, and support smooth airport ground handling activities. Major international airports invested in advanced fuel storage and hydrant systems during 2025, which further strengthened the use of on-airport fueling services across high-traffic aviation hubs.

By Application Analysis

Commercial Aviation dominates with 68.3% share driven by rising global air passenger traffic and expanding airline networks

In 2025, Commercial Aviation held a dominant market position, capturing more than a 68.3% share of the global jet fuel market by application. The segment continued to lead due to the steady increase in domestic and international air travel across major economies. Airlines expanded their flight operations to meet growing passenger demand, especially across Asia-Pacific, North America, and the Middle East. The recovery of tourism, business travel, and international trade activities played an important role in increasing jet fuel consumption within the commercial aviation sector throughout the year.

Key Market Segments

By Fuel Type

- Jet A

- Jet A-1

- Jet B

- Others (TS-1, Sustainable Aviation Fuel (SAF))

By Distribution Channel

- Into-Plane (On-Airport)

- Bulk Supply to Fixed-Base Operators (FBO)

By Application

- Commercial Aviation

- Defense Aviation

- General Aviation

Emerging Trends

Growing Use of Sustainable Aviation Fuel is Emerging as a Key Trend in the Jet Fuel Market

One of the latest trends shaping the jet fuel market is the growing adoption of sustainable aviation fuel (SAF) by airlines and airport operators worldwide. Aviation companies are increasingly blending SAF with conventional jet fuel to reduce carbon emissions while maintaining normal aircraft performance.

According to the International Air Transport Association (IATA), global SAF production is expected to exceed 2.7 billion liters in 2025, showing strong year-over-year growth as governments and airlines increase sustainability efforts. Several international carriers have already signed long-term SAF supply agreements to meet future environmental targets. Governments in Europe and North America are also introducing blending mandates and financial incentives to encourage production and usage.

Airlines are Focusing on Fuel Efficiency and Modern Aircraft Fleets

Another important trend in the jet fuel market is the increasing focus on fuel-efficient aircraft and smarter airline operations. Airlines are replacing older aircraft with newer generation models that consume less fuel and reduce operational costs. According to the International Civil Aviation Organization (ICAO), modern aircraft can improve fuel efficiency by nearly 15% to 20% compared to previous-generation fleets. This shift is becoming more noticeable as airlines try to balance rising passenger demand with stricter environmental regulations and fuel cost management. In 2025, many global airlines continued expanding fleets with next-generation aircraft designed for longer routes and lower fuel burn.

Governments are also supporting airport modernization projects and digital air traffic management systems to improve operational efficiency and reduce unnecessary fuel consumption during flights. Airlines are increasingly using route optimization software and advanced engine monitoring systems to lower fuel usage while maintaining flight performance. These operational improvements are becoming a major part of long-term aviation fuel management strategies across the global aviation industry.

Drivers

Rising Global Air Passenger Traffic is Increasing Jet Fuel Demand

The steady growth in global air travel is one of the biggest driving factors for the jet fuel market. Airlines across the world are operating more flights to meet the increasing demand from tourists, business travelers, and cargo transportation services.

- According to the International Civil Aviation Organization (ICAO), global passenger traffic reached around 9.4 billion passengers in 2024, showing an 8.4% increase compared to the previous year.

The aviation industry continued this momentum through 2025 as international travel routes expanded across Asia-Pacific, Europe, and the Middle East. At the same time, Airports Council International (ACI) projected that global passenger traffic would reach nearly 9.8 billion passengers in 2025, reflecting continued growth in airline activity. This rise in aircraft movement directly supports higher consumption of jet fuel across commercial aviation networks.

Airline Expansion and Fleet Growth Continue to Support Fuel Consumption

Another important factor supporting the jet fuel market is the ongoing expansion of airline fleets and flight operations worldwide. The International Air Transport Association (IATA) reported that total passenger demand in 2025 increased by 5.3% compared to 2024, while international passenger traffic alone grew by 7.1%.

Airlines continued adding new routes and increasing flight frequency to handle growing travel demand. In addition, global airlines are expected to continue purchasing new aircraft to improve operational efficiency and support long-term passenger growth. This continuous rise in airline operations is creating stable demand for jet fuel across both passenger and cargo aviation sectors.

Restraints

Volatile Crude Oil Prices are Creating Pressure on the Jet Fuel Market

One of the biggest restraining factors for the jet fuel market is the constant fluctuation in global crude oil prices. Since jet fuel is refined from crude oil, any sudden rise in oil prices directly increases airline operating costs. According to the International Energy Agency (IEA), global jet fuel demand crossed 8 million barrels per day in 2025, making airlines highly sensitive to fuel price movements. During periods of geopolitical tension and supply disruptions, crude oil prices often become unstable, creating financial pressure for airline companies.

The U.S. Energy Information Administration (EIA) reported that Brent crude oil prices averaged around USD 84 per barrel in early 2025, compared to lower averages seen during previous recovery years. These rising fuel costs reduce airline profit margins and sometimes force carriers to increase ticket prices, which can affect passenger demand. Several governments are encouraging airlines to improve fuel efficiency and adopt cleaner fuel technologies to reduce dependence on conventional jet fuel and manage long-term cost risks.

Environmental Regulations and Carbon Emission Targets are Slowing Market Flexibility

Another major challenge for the jet fuel market is the growing pressure from environmental regulations and global carbon reduction targets. Aviation remains one of the industries under strong international focus for lowering greenhouse gas emissions. According to the International Air Transport Association (IATA), aviation contributes nearly 2% to 3% of global carbon dioxide emissions, leading governments and regulatory bodies to introduce stricter sustainability policies.

In 2025, many countries continued implementing emission-control frameworks and sustainable aviation fuel (SAF) blending targets to reduce reliance on traditional jet fuel. The European Union also expanded aviation-related carbon policies under its climate programs, increasing operational costs for airlines using conventional fuels. While sustainable aviation fuel adoption is growing, its limited availability and higher production cost remain challenges for carriers and fuel suppliers.

Opportunity

Sustainable Aviation Fuel Adoption is Creating New Growth Opportunities for the Jet Fuel Market

One of the biggest growth opportunities in the jet fuel market is the rapid development of sustainable aviation fuel (SAF). Governments and aviation organizations across the world are investing heavily in cleaner aviation energy solutions to reduce carbon emissions while maintaining air travel growth.

- According to the International Air Transport Association (IATA), sustainable aviation fuel production is expected to reach more than 2.7 billion liters in 2025, nearly double compared to previous years.

This increase is creating new opportunities for fuel producers, airlines, and airport fuel infrastructure providers. Countries such as the United States, the United Kingdom, and members of the European Union are introducing SAF blending mandates and tax incentives to encourage production and usage. The U.S. Department of Energy also supports the Sustainable Aviation Fuel Grand Challenge, which aims to produce 3 billion gallons of SAF annually by 2030. These initiatives are helping fuel companies expand their operations while supporting long-term aviation sustainability goals.

Expansion of Airport Infrastructure and Emerging Aviation Markets is Supporting Fuel Demand

Another major opportunity for the jet fuel market is the fast expansion of airport infrastructure and rising aviation activity in emerging economies. Countries across Asia-Pacific, the Middle East, and Africa are investing in new airports, runway upgrades, and airline connectivity projects to support growing passenger traffic. According to Airports Council International (ACI), global air passenger numbers are expected to approach 10 billion travelers by 2025, creating strong long-term demand for aviation fuel supply systems.

Governments are also supporting regional air connectivity programs to improve transportation access between smaller cities and major commercial hubs. These developments are encouraging airlines to add more aircraft and expand route networks, directly supporting higher jet fuel consumption. Growing tourism activity and increasing middle-class travel demand are also helping airlines maintain steady operational expansion across developing regions.

Regional Insights

Asia-Pacific dominates the jet fuel market with a 37.4% share valued at USD 84.8 billion due to rapid aviation expansion and rising passenger traffic

In 2025, Asia-Pacific held a dominant position in the global jet fuel market, accounting for 37.4% of the total market share and reaching a market value of USD 84.8 billion. The region continued to lead because of strong growth in commercial aviation, expanding airport infrastructure, and rising domestic as well as international passenger traffic. Countries such as China, India, Japan, South Korea, and Southeast Asian nations witnessed a steady increase in airline operations during the year.

China remained one of the largest contributors to regional demand due to its extensive airline network and continuous airport development projects. India also emerged as a fast-growing aviation market supported by government-led regional connectivity programs and investments in new airport terminals. Several low-cost carriers expanded route networks across Asia-Pacific, increasing the number of short-haul and medium-haul flights operating daily.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Shell plc remains one of the leading global jet fuel and sustainable aviation fuel (SAF) suppliers through its Shell Aviation division. The company operates in more than 60 countries and supports commercial, military, and private aviation customers. Shell’s Avelia SAF platform surpassed 33 million gallons of SAF transactions by 2025, while over 57 corporations and airlines participated in the ecosystem. Shell previously targeted 2 million tonnes of SAF production capacity and aimed for SAF to represent 10% of aviation fuel sales by 2030.

Exxon Mobil Corporation is a major aviation fuel supplier with more than 100 years of aviation fuel operations globally. The company supplies conventional jet fuel, aviation gasoline, and SAF to commercial and military sectors. ExxonMobil reported $34 billion in annual earnings during 2024 and maintained global production of approximately 4.736 million barrels of oil equivalent per day in 2025. Its Singapore refining complex supports SAF blending operations, while the company targets production of 200,000 barrels per day of lower-emission fuels by 2030.

Air BP is among the world’s largest aviation fuel suppliers, operating across commercial airports, military bases, and private aviation hubs. The business provides aviation fuel services, storage infrastructure, and SAF solutions globally. Air BP supports fueling operations in more than 600 locations across 45 countries through direct operations and partnerships. The company is actively aligning with the European Union SAF mandate that started with 2% SAF blending in 2025. BP’s aviation infrastructure also includes the 400-mile Olympic Pipeline, which transports gasoline, diesel, and jet fuel in the U.S. market.

Top Key Players Outlook

- Shell PLC

- Exxon Mobil Corp

- BP PLC (Air BP)

- Chevron Corp

- OMV AG

- Gazprom Neft PJSC

- Bharat Petroleum Ltd

- Indian Oil Corporation

- Eni SpA

- TotalEnergies SE

- Qatar Jet Fuel Company (QJet)

- Idemitsu Kosan Co.

- PetroChina Co Ltd

- Neste OYJ

- LanzaJet Inc.

- Gevo Inc.

- World Fuel Services Corp

- Phillips 66 Aviation

- Vitol Aviation

- PETRONAS Dagangan Berhad

- Saudi Aramco (SAF-focused JVs)

Recent Industry Developments

Gazprom Neft had earlier committed RUB 700 billion to modernise its Omsk and Moscow refineries up to 2025, helping widen its aviation fuel product range, including JET A-1 production. Operationally, Gazpromneft-Aero previously sold 3.03 million tonnes of jet fuel in Russia and had a target to raise aviation kerosene sales to 5.3 million tonnes by 2025.

Chevron Renewable Energy Group offers SAF blendstock meeting ASTM D7566 standards. For partnership and agreement activity, Chevron’s earlier Gevo SAF plan remains important, with potential offtake of nearly 150 million gallons per year. In M&A, Chevron completed the Hess acquisition on July 18, 2025, strengthening crude supply security for its wider fuels business. For investment and expansion, Chevron planned US$18–19 billion capex for 2026, while downstream spending was estimated near US$1 billion.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 227.1 Bn |

| Forecast Revenue (2035) | USD 468.7 Bn |

| CAGR (2026-2035) | 7.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Fuel Type (Jet A, Jet A-1, Jet B, Others (TS-1, Sustainable Aviation Fuel)), By Distribution Channel (Into-Plane (On-Airport), Bulk Supply to Fixed-Base Operators (FBO)), By Application (Commercial Aviation, Defense Aviation, General Aviation) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Shell PLC, Exxon Mobil Corp, BP PLC (Air BP), Chevron Corp, OMV AG, Gazprom Neft PJSC, Bharat Petroleum Ltd, Indian Oil Corporation, Eni SpA, TotalEnergies SE, Qatar Jet Fuel Company (QJet), Idemitsu Kosan Co., PetroChina Co Ltd, Neste OYJ, LanzaJet Inc., Gevo Inc., World Fuel Services Corp, Phillips 66 Aviation, Vitol Aviation, PETRONAS Dagangan Berhad, Saudi Aramco (SAF-focused JVs) |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |