Quick Navigation

Report Overview

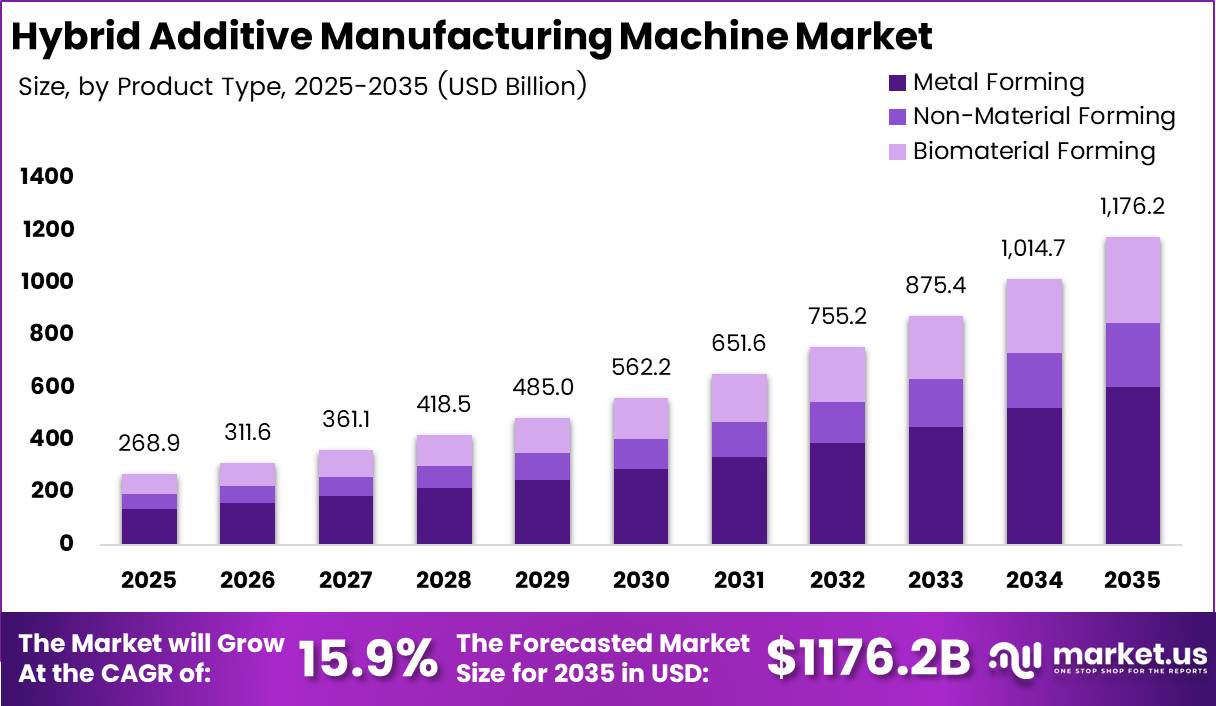

Global Hybrid Additive Manufacturing Machine Market size is expected to be worth around USD 1,176.2 Billion by 2035 from USD 268.9 Billion in 2025, growing at a CAGR of 15.9% during the forecast period 2026 to 2035.

The hybrid additive manufacturing machine market covers systems that combine additive processes with subtractive operations such as milling, turning, and grinding within a single platform. These machines produce complex, high-precision components in fewer steps than traditional multi-machine workflows. This integration reduces floor space requirements and shortens lead times for industrial manufacturers.

The market structure spans three primary segments: type, application, and end-user. By type, metal forming commands the largest share. By application, production use leads the market. By end-user, aerospace and defense holds the top position. This layered structure means demand is concentrated in high-precision, high-stakes industries where component failure carries serious consequences.

Government investment in advanced manufacturing programs directly supports this market. Defense procurement agencies in the United States and Europe fund hybrid manufacturing research to shorten supply chains for critical components. These programs reduce commercial risk for vendors by providing early, large-volume customers. Vendors aligned with defense spending cycles gain a structural revenue buffer unavailable to consumer-facing manufacturers.

Regulatory frameworks around part certification in aerospace and medical sectors shape purchasing decisions. Regulatory bodies require documented traceability and repeatable process outputs. Hybrid systems with integrated monitoring and closed-loop controls are better positioned to meet these requirements. Vendors who build compliance capabilities into their platforms will reduce customer qualification time and accelerate purchase decisions.

As reported by a 2025 research study, applying a deep-learning framework to hybrid manufacturing lines reduced production schedule duration by 12% compared with existing methods on benchmark datasets. This efficiency gain signals that AI integration is no longer experimental. Vendors embedding AI into hybrid platforms will attract buyers seeking measurable productivity improvements, not just hardware upgrades.

Data from a 2025 Meltio case study shows that wire-laser metal deposition within a hybrid context achieved a 62.5% weight reduction and a 35.7% cost reduction for a redesigned component versus the conventionally manufactured version. These figures demonstrate that hybrid manufacturing delivers quantifiable financial returns. Buyers evaluating total cost of ownership will find these outcomes difficult to ignore, accelerating capital allocation toward hybrid systems.

Key Takeaways

- Global Hybrid Additive Manufacturing Machine Market was valued at USD 268.9 Billion in 2025.

- The market is forecast to reach USD 1,176.2 Billion by 2035.

- The market grows at a CAGR of 15.9% during the forecast period 2026 to 2035.

- By Type, Metal Forming dominates with a 51.3% share.

- By Application, Production holds the leading share at 49.5%.

- By End-User, Aerospace and Defense leads with a 31.2% share.

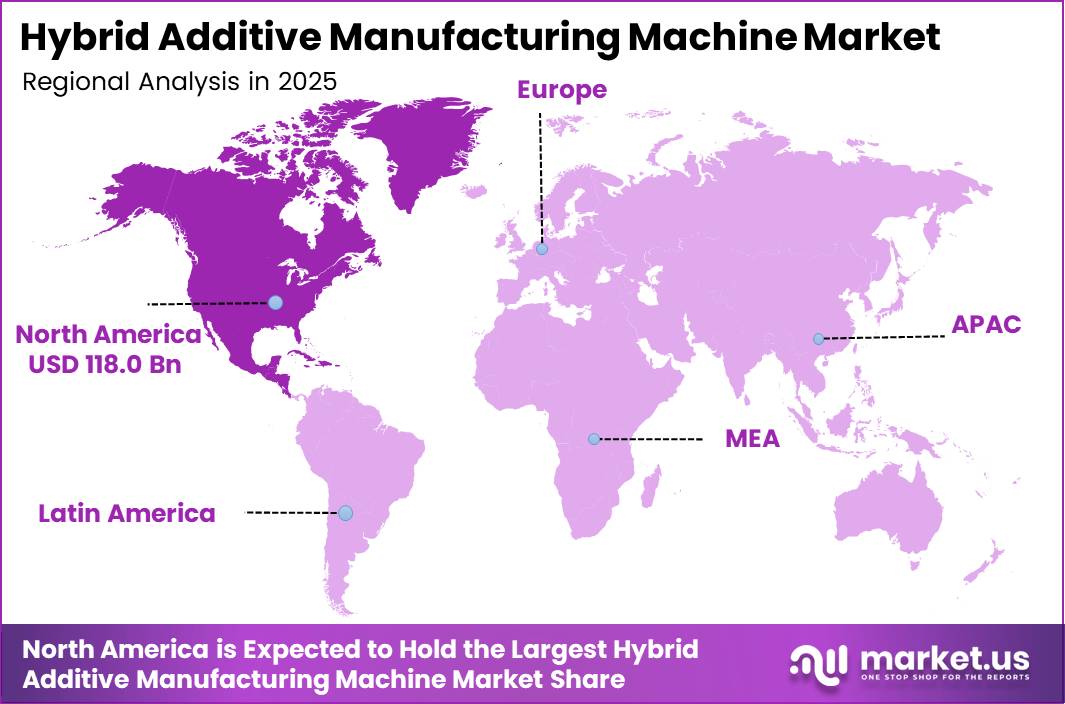

- North America is the dominant region with a 43.90% share, valued at USD 118.0 Billion.

Type Analysis

Metal Forming dominates with 51.3% due to high precision demand in aerospace and defense.

In 2025, Metal Forming held a dominant market position in the By Type segment of the Hybrid Additive Manufacturing Machine Market, with a 51.3% share. Metal forming hybrid systems address the tightest dimensional tolerances required by aerospace, defense, and energy buyers. As reported by industry data, Phillips Corporation reached its 100th hybrid machine installation milestone in 2025, confirming that metal-capable hybrid systems are moving from pilot programs into full production deployments.

Non-Material Forming covers hybrid systems that process polymers, ceramics, and composite feedstocks outside of metallic workflows. Buyers in electronics and medical device manufacturing use these platforms for housings, implants, and custom fixtures. This segment attracts volume from industries where material diversity matters more than the extreme thermal and structural demands placed on metal-forming systems.

Biomaterial Forming applies hybrid additive-subtractive processes to biological and biocompatible materials used in medical and research applications. Precision finishing of scaffold structures and implantable components requires the subtractive step that pure additive systems cannot deliver alone. This segment remains smaller in revenue terms but carries high margins given the regulatory and technical barriers that limit the number of qualified vendors.

Application Analysis

Production dominates with 49.5% due to high-volume industrial component output requirements.

In 2025, Production held a dominant market position in the By Application segment of the Hybrid Additive Manufacturing Machine Market, with a 49.5% share. Production applications require machines that deliver consistent, repeatable output across extended run cycles. Buyers in this segment prioritize uptime, process stability, and integration with existing factory automation rather than flexibility or low unit costs.

Prototype applications use hybrid systems to compress the cycle from design to physical part verification. Engineers in automotive and aerospace firms use hybrid platforms to produce functional prototypes with final-material properties rather than surrogate test pieces. This reduces the gap between prototype validation and production release, shortening overall development timelines.

Repair applications deploy hybrid systems to restore worn or damaged high-value components to original specification. Energy, defense, and aerospace operators use repair workflows to extend the service life of turbine blades, molds, and structural parts. Repair represents a high-margin application because the alternative is full component replacement, making cost justification straightforward for buyers.

End-User Analysis

Aerospace and Defense dominates with 31.2% due to strict precision and certification requirements.

In 2025, Aerospace and Defense held a dominant market position in the By End-User segment of the Hybrid Additive Manufacturing Machine Market, with a 31.2% share. Defense procurement programs prioritize supply chain independence and part traceability, both of which hybrid systems with integrated monitoring address directly. Vendors serving this segment benefit from long contract cycles and repeat orders tied to platform maintenance programs.

Energy and Power operators use hybrid systems to manufacture and repair turbine components, heat exchangers, and pressure vessel parts. The high cost of energy sector downtime makes repair-capable hybrid machines financially attractive. Buyers in this end-user group evaluate machines on speed of restoration and material compatibility with superalloys rather than on acquisition price alone.

Electronics manufacturers apply hybrid systems to produce precision housings, heat sinks, and embedded component carriers at low to medium volumes. The electronics segment values compact machine footprints and multi-material capability over raw throughput. This creates demand for smaller, more flexible hybrid platforms rather than the large-format machines favored in aerospace and energy applications.

Key Market Segments

By Type

- Metal Forming

- Non-Material Forming

- Biomaterial Forming

By Application

- Production

- Prototype

- Repair

By End-User

- Aerospace and Defense

- Energy and Power

- Electronics

- Medical

- Automotive

- Others

Regional Analysis

North America Dominates the Hybrid Additive Manufacturing Machine Market with a Market Share of 43.90%, Valued at USD 118.0 Billion

North America holds 43.90% of the global market, valued at USD 118.0 Billion in 2025. The United States government’s sustained investment in defense manufacturing modernization drives adoption of hybrid systems across prime contractors and their supply chains. In November 2025, Hybrid CNC Parts tripled its hybrid manufacturing capacity by acquiring Phillips Additive Hybrid Laser-Wire systems, confirming that North American operators are scaling production infrastructure at pace.

Europe holds a structurally strong position driven by its concentrated base of precision engineering firms in Germany, France, and the United Kingdom. European manufacturers face strict emissions and efficiency regulations that push investment toward processes with lower energy and material waste. Hybrid systems that reduce per-part energy consumption align directly with these regulatory obligations, making procurement decisions easier to justify at the board level.

Asia Pacific is a high-growth region where China, Japan, and South Korea are investing in domestic advanced manufacturing capability. Government-backed industrial programs in China specifically target hybrid and additive technologies as part of broader manufacturing self-sufficiency initiatives. This policy-driven demand creates a fast-moving buyer base that favors vendors who can offer localized support and training infrastructure.

Latin America shows early-stage adoption concentrated in Brazil and Mexico, where automotive and aerospace supply chain investment is highest. The region lacks deep technical infrastructure for operating and maintaining hybrid systems, which slows purchase decisions. Vendors entering Latin America must budget for extended customer support and operator training beyond what mature markets require.

Middle East and Africa adoption centers on the GCC countries, where national manufacturing diversification programs fund advanced production technology. South Africa holds a secondary position driven by its aerospace maintenance and mining equipment sectors. Both sub-regions remain below global average in hybrid machine density, representing a long runway for vendors willing to invest in regional partnerships and service capability.

Market Dynamics

Drivers - Faster cycle times and complex component demand push hybrid adoption into production workflows

As per our research, a WAAM-based hybrid setup completed parts in 15 minutes per artifact versus 41 minutes for a milling-only baseline. This speed advantage makes hybrid systems directly competitive on production floor economics, not just technical capability. Manufacturers under pressure to reduce throughput time now have a quantified justification for capital investment in hybrid platforms.

The same 2025 study confirms that the WAAM hybrid route cut total cycle time by 63% relative to the milling-only baseline. This reduction compresses production schedules and lowers per-part labor cost simultaneously. Vendors who can demonstrate cycle time data in customer-specific scenarios will accelerate purchase decisions among cost-conscious production managers.

Aerospace and automotive manufacturers are adopting lightweight design strategies that require internal lattice structures and topology-optimized geometries impossible to achieve with subtractive processes alone. Hybrid systems are the only production-ready technology that can build and finish these structures in a single setup. This structural requirement, not preference, drives specification of hybrid machines into new platform development programs.

Restraints - High acquisition costs and missing process standards block adoption among smaller manufacturers

High acquisition and integration costs remain the primary barrier preventing small and mid-size manufacturers from entering the hybrid machine market. A single hybrid platform capable of metal forming can require capital commitments that exceed the annual equipment budgets of many contract manufacturers. This pricing structure concentrates the buyer pool among large primes and well-funded OEMs, limiting the addressable market for vendors.

The absence of standardized production protocols for hybrid manufacturing workflows creates qualification risk for buyers in regulated industries. Each manufacturer must develop its own process parameters, which adds engineering cost and time before a machine generates revenue. This non-standardization inflates the true cost of ownership beyond the purchase price and delays the payback period that justifies investment.

Based on our research, the AI-based hybrid approach delivered a 15% improvement in overall process efficiency compared with prior hybrid configurations. This figure highlights the gap between current hybrid deployments and optimized operations. Buyers operating non-AI-assisted hybrid systems are leaving measurable efficiency on the table, yet the cost and complexity of retrofitting AI capabilities into older platforms acts as a secondary restraint on the installed base.

Growth Factors - Material savings, cost reductions, and energy efficiency open new financial justifications for hybrid investment

Figures from a 2025 AI-driven hybrid manufacturing study show that the AI-enabled hybrid framework achieved a 23% reduction in material wastage relative to existing additive-subtractive methods. For metal feedstocks priced at premium rates, this saving directly reduces variable production costs. Manufacturers with high material spend per part will find that hybrid systems with AI process control offer a faster financial payback than conventional equipment.

According to a 2025 Meltio case study, wire-laser metal deposition within a hybrid manufacturing context delivered a 62.5% weight reduction and a 35.7% cost reduction for a redesigned component versus the original conventionally manufactured part. Weight reduction at this scale carries compounding value in aerospace and automotive applications where every kilogram reduced translates into fuel savings across a product lifetime. This dual benefit makes hybrid systems a design enabler, not just a production tool.

As reported by research on DED-based hybrid additive manufacturing, optimized hybrid toolpaths cut total energy use by approximately 10 to 15% per part compared with non-hybrid DED plus separate machining routes. Energy cost reduction strengthens the business case in markets where industrial electricity prices are elevated. Vendors who quantify energy savings alongside capital cost will reach a broader set of financial decision-makers, not only engineering buyers.

Emerging Trends - AI integration and closed-loop control reshape process performance benchmarks for hybrid systems

Data from a 2025 article on AI-driven hybrid manufacturing shows that applying a deep-learning framework reduced production schedule duration by 12% compared with existing hybrid methods on benchmark datasets. This result signals that software-layer optimization can deliver productivity gains without hardware replacement. Vendors who build AI scheduling tools into their platforms create a switching cost that protects long-term customer retention.

The same 2025 study reports that defect-detection accuracy in the AI-enabled hybrid process reached 98.7%, exceeding earlier hybrid baseline approaches used for comparison. Higher defect detection at this accuracy level reduces scrap rates and post-process inspection costs for buyers in aerospace and medical end-user segments. Vendors who achieve and certify this accuracy level gain a clear qualification advantage in regulated procurement processes.

Closed-loop manufacturing systems using real-time sensor feedback are moving from research environments into commercial hybrid platforms. These systems adjust process parameters during a build cycle based on live measurement data, reducing deviation from design intent without operator intervention. Early movers who deploy closed-loop hybrid systems in customer facilities will establish performance benchmarks that late-adopting competitors will struggle to match without significant re-engineering investment.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

DMG MORI Co., Ltd. holds a leading position in the hybrid additive manufacturing machine market through its LASERTEC platform, which integrates up to six processes including milling, turning, grinding, preheating, directed energy deposition, and 3D scanning into one system. This multi-process consolidation reduces capital expenditure for buyers replacing multiple standalone machines. However, this complexity also raises integration risk for first-time hybrid buyers without dedicated process engineering teams.

Mazak Corporation competes through its established global distribution and service network, which supports customers across North America, Europe, and Asia Pacific. Mazak’s existing relationships with precision machining customers give it a direct channel to buyers ready to upgrade from conventional CNC platforms to hybrid systems. This installed base advantage is difficult for newer entrants to replicate quickly, though Mazak must continue expanding its additive-specific application engineering to convert that access into closed sales.

Key Players

- DMG MORI Co., Ltd.

- Mazak Corporation

- Matsuura Machinery Corporation

- Stratasys Ltd

- voxeljet AG

- Optomec

- SLM SOLUTIONS GROUP AG

- Materialise

- GE Additive

Recent Developments

- November 2025 – Nikon SLM Solutions and Materialise entered a strategic co-development partnership to build an integrated data-preparation workflow combining software and machine controls, targeting scalable industrial production for advanced additive manufacturing systems.

- January 2026 – DMG MORI launched the LASERTEC 65 DED Hybrid 2nd Generation, integrating laser deposition welding, 5-axis milling, turning, grinding, preheating, and 3D scanning within a single machine platform for hybrid manufacturing applications.

- February 2026 – DMG MORI expanded its hybrid manufacturing portfolio with the commercial introduction of the LASERTEC 65 DED Hybrid 2nd Generation, featuring a new MultiJet nozzle, enhanced process monitoring, improved powder management, and closed-loop process control for industrial-scale additive manufacturing.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 268.9 Billion |

| Forecast Revenue (2035) | USD 1,176.2 Billion |

| CAGR (2026-2035) | 15.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Metal Forming, Non-Material Forming, Biomaterial Forming), By Application (Production, Prototype, Repair), By End-User (Aerospace and Defense, Energy and Power, Electronics, Medical, Automotive, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | DMG MORI Co., Ltd., Mazak Corporation, Matsuura Machinery Corporation, Stratasys Ltd, voxeljet AG, Optomec, SLM SOLUTIONS GROUP AG, Materialise, GE Additive |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |