Quick Navigation

Report Overview

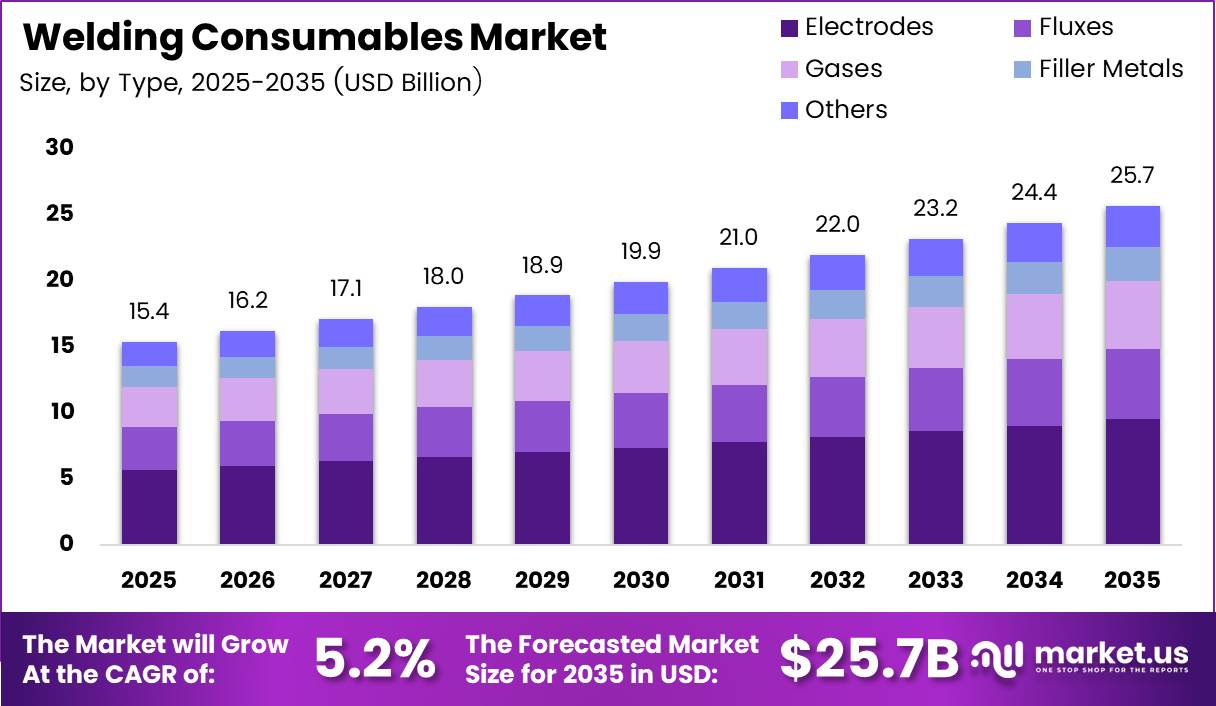

Global Welding Consumables Market size is expected to be worth around USD 25.7 Billion by 2035 from USD 15.4 Billion in 2025, growing at a CAGR of 5.2% during the forecast period 2026 to 2035.

The welding consumables market covers all materials consumed during the welding process, including electrodes, filler metals, fluxes, and shielding gases. These inputs are required for every fusion joining operation across construction, manufacturing, and energy infrastructure. No structural weld is possible without them, making this market non-discretionary within its served industries.

The market structure spans several product categories that serve distinct welding processes. Shielded metal arc welding, gas metal arc welding, submerged arc welding, and flux-cored arc welding each require different consumable formulations. This process diversity creates parallel demand streams that move independently of one another, protecting total market revenue when any single welding method declines.

Governments in Asia Pacific, the Middle East, and North America direct public capital toward infrastructure construction, energy pipelines, and shipbuilding programs. These programs generate multi-year contracted demand for welding consumables. Public procurement timelines are longer than commercial cycles, but they provide revenue visibility that private-sector orders alone cannot deliver.

Regulatory frameworks governing welding fume exposure and weld quality certification influence consumable specifications in developed markets. Buyers in regulated industries such as aerospace, nuclear energy, and offshore construction must procure consumables that meet specific qualification standards. This compliance layer restricts substitution and supports pricing stability for certified product lines.

Based on weldingwire.net data, metal-cored welding wires achieve deposition efficiencies of 92% to 98%, meaning up to 98% of the consumable converts into deposited weld metal. Higher deposition efficiency directly reduces material waste per joint. For high-volume fabricators, this efficiency advantage translates into measurable cost savings that justify a premium price over standard solid wire alternatives.

Figures from weldingwire.net show flux-cored and metal-cored wires using 1.2 mm diameter achieve deposition rates of 5.4 to 6.4 kg per hour in production welding. This rate significantly outpaces solid wire outputs at equivalent diameters. Fabricators who adopt advanced wire formats gain throughput advantages that reduce labor cost per weld, making the consumable upgrade economically self-funding across most production environments.

Key Takeaways

- The global Welding Consumables Market was valued at USD 15.4 Billion in 2025 and is forecast to reach USD 25.7 Billion by 2035.

- The market grows at a CAGR of 5.2% during the forecast period 2026 to 2035.

- Electrodes dominate the By Type segment with a 36.8% share in 2025.

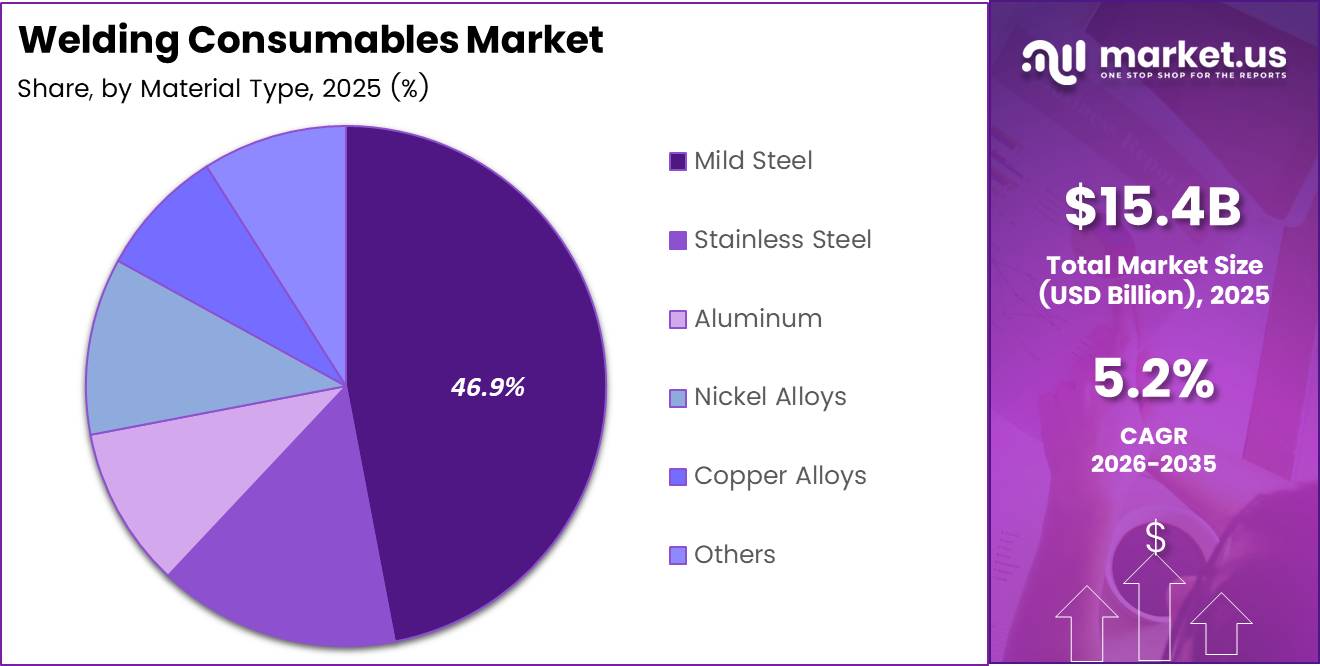

- Mild Steel leads the By Material Type segment with a 46.9% share in 2025.

- Construction leads the By End Use segment with a 31.50% share in 2025.

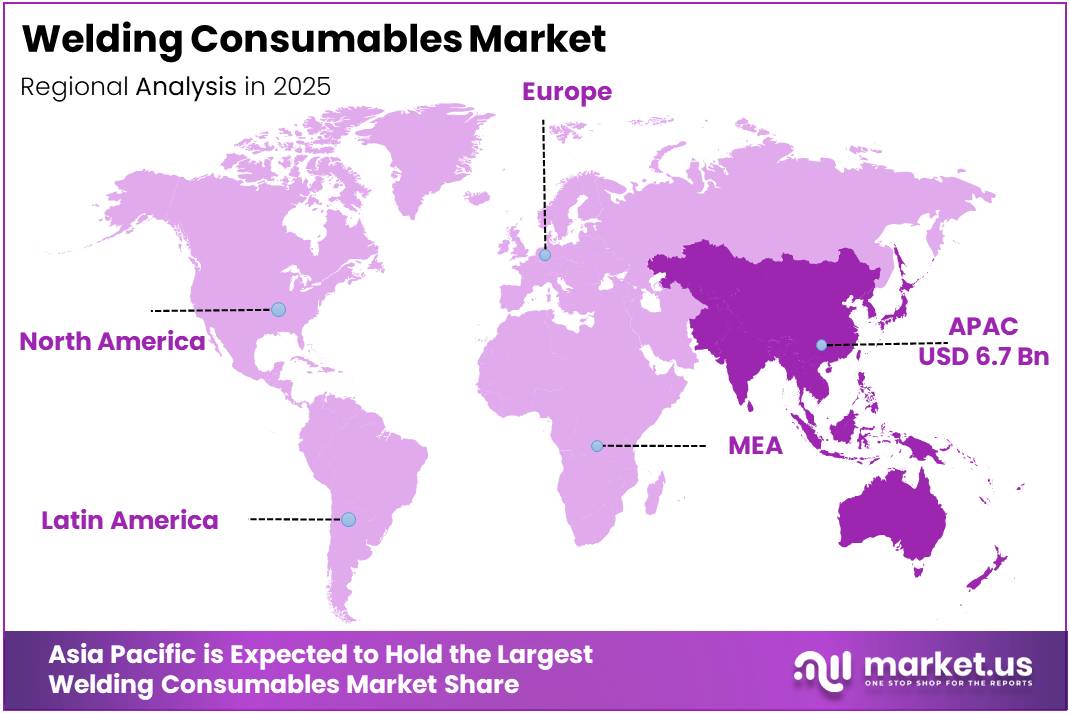

- Asia Pacific is the dominant region with a 43.80% market share, valued at USD 6.7 Billion in 2025.

Type Analysis

Electrodes dominates with 36.8% due to universal applicability across manual and semi-automated welding.

In 2025, Electrodes held a dominant market position in the By Type segment of the Welding Consumables Market, with a 36.8% share. Electrodes serve the broadest range of applications across construction, shipbuilding, and repair operations. Their compatibility with portable, low-cost equipment sustains demand in developing markets where infrastructure investment is accelerating, preserving volume even as automation adoption grows in industrialized economies.

Fluxes serve submerged arc and oxy-fuel welding processes that dominate thick-plate fabrication in shipbuilding, pressure vessel manufacturing, and pipeline construction. Flux consumption scales directly with weld bead size, meaning large-structure fabrication contracts generate disproportionately high flux volume requirements. Buyers in these segments treat flux qualification as a supply chain risk, creating preference for established vendors with consistent batch chemistry.

Gases serve as shielding and backing media across MIG, TIG, and plasma welding processes. Gas consumption is continuous and non-storable at point of use, creating a recurring revenue characteristic not present in solid consumable categories. Industrial gas suppliers and welding consumable vendors who bundle gas supply with wire and electrode products capture a larger share of the customer’s total welding bill-of-materials spend.

Filler Metals represent the broadest product category within the welding consumables market, covering solid wire, flux-cored wire, metal-cored wire, welding rods, and specialty alloy formats. This category captures spend across the widest range of base materials and welding processes. Vendors who offer complete filler metal portfolios eliminate the need for fabricators to source from multiple suppliers, creating a supply chain consolidation argument that supports preferred-vendor positioning.

Material Type Analysis

Mild Steel dominates with 46.9% due to universal use across construction, fabrication, and infrastructure.

In 2025, Mild Steel held a dominant market position in the By Material Type segment of the Welding Consumables Market, with a 46.9% share. Mild steel is the most widely fabricated structural material globally. Its dominance in construction, shipbuilding, and general manufacturing ensures that mild steel welding consumables generate the highest aggregate volume demand across all geographies and end-use sectors simultaneously.

Stainless Steel consumables serve food processing, pharmaceutical, chemical, and offshore industries where corrosion resistance is a structural specification rather than an aesthetic preference. Stainless welding requires tighter shielding gas control and more precise heat input management than mild steel, supporting premium pricing for qualified stainless consumable products. Vendors with demonstrated stainless alloy expertise and AWS or EN qualification documentation command preferred-vendor status in these regulated sectors.

Aluminum welding consumables serve automotive lightweighting programs, aerospace structural components, and marine fabrication where weight reduction directly affects operational performance or fuel economy. Aluminum welding requires specialized wire feeding systems and inert shielding gas chemistry, creating system-level dependencies that tie consumable purchases to specific equipment configurations. This equipment linkage strengthens vendor retention among aluminum fabricators once initial process qualification is completed.

End Use Analysis

Construction dominates with 31.50% due to continuous global infrastructure development and structural steel demand.

In 2025, Construction held a dominant market position in the By End Use segment of the Welding Consumables Market, with a 31.50% share. Infrastructure development across Asia Pacific, the Middle East, and North America generates sustained structural steel fabrication demand. Government-funded programs for roads, bridges, ports, and buildings translate directly into multi-year welding consumable procurement contracts that underpin the segment’s leading position.

Automobile manufacturing uses welding consumables for body-in-white assembly, chassis fabrication, and exhaust system production across high-volume production lines. Automotive welding operates under strict process parameter controls and automated equipment configurations that require consistent consumable chemistry across every production batch. Vendors who achieve automotive supplier qualification gain access to multi-year supply agreements tied to vehicle production volumes rather than annual rebid cycles.

Energy sector buyers consume welding consumables across oil and gas pipeline construction, refinery fabrication, nuclear plant maintenance, and offshore platform assembly. Each sub-sector within energy carries distinct consumable qualification requirements tied to pressure, temperature, and corrosion service conditions. Consumable vendors who hold multiple energy sector certifications simultaneously reduce the number of approved supplier decisions a fabricator must make, increasing their share of wallet per account.

Key Market Segments

By Type

- Electrodes

- Shielded Metal Arc Welding Electrodes

- Gas Metal Arc Welding Electrodes

- Others

- Fluxes

- Submerged Arc Welding Flux

- Oxy-Fuel Welding Flux

- Others

- Gases

- Shielding Gases

- Backing Gases

- Others

- Filler Metals

- Solid Wire

- Flux-Cored Wire

- Metal-Cored Wire

- Welding Rods

- Others

- Others

By Material Type

- Mild Steel

- Stainless Steel

- Aluminum

- Nickel Alloys

- Copper Alloys

- Others

By End Use

- Construction

- Automobile

- Energy

- Shipbuilding

- Aerospace

- Heavy Engineering

- Others

Market Dynamics

Drivers - High-Deposition Welding Wire Technologies Improve Productivity and Lower Fabrication Costs

Data from weldingwire.net shows metal-cored welding wires achieve deposition efficiencies of 92% to 98%, converting nearly all consumable weight into deposited weld metal. This efficiency directly reduces material cost per completed joint. Fabricators running high joint-volume production lines gain a cost-per-weld advantage over competitors relying on lower-efficiency solid wire formats, making consumable selection a measurable competitive variable.

As reported by weldingwire.net, flux-cored welding wires achieve deposition efficiencies of 84% to 89% depending on wire design and welding conditions. While below metal-cored performance, this efficiency level still outperforms many manual electrode processes. Fabricators who transition from manual electrodes to flux-cored wire capture both productivity and efficiency gains simultaneously, reducing per-joint cost across two variables with a single process change.

In June 2024, Lincoln Electric acquired Inrotech A/S, enhancing its automation and robotic welding capabilities. Automated welding systems require consistent consumable chemistry to maintain uninterrupted production output. This acquisition positions Lincoln Electric to offer integrated automation and consumable solutions, capturing procurement decisions at both the equipment and materials level within the same customer relationship.

Restraints - Economic Upgrade Barriers and Skilled Labor Requirements Limit Advanced Consumable Adoption

weldingwire.net indicates comparable 1.2 mm solid MIG wires typically achieve deposition rates of 3.6 to 4.5 kg per hour. This throughput ceiling limits productivity gains available to facilities relying on solid wire without process changes. Fabricators operating below the threshold where advanced wire becomes economical face a market where the performance gap versus competitors widens as deposition technology improves.

weldingwire.net found that a deposition rate of 4 kg per hour or greater is the point where metal-cored wire often becomes economically advantageous over solid wire. Facilities running below this threshold cannot financially justify the premium on advanced wire formats. This economic boundary segments the consumable market between high-volume buyers who upgrade and lower-output buyers who remain on solid wire, creating a two-tier pricing environment that complicates uniform vendor margin strategies.

Based on Lincoln Electric data, the Innershield NR-305 weld deposits provide typical elongation of 25%. Achieving these mechanical properties consistently requires precise operator technique and controlled welding parameters. Facilities that lack trained welding personnel or process monitoring equipment risk weld quality variance that triggers rework costs, effectively penalizing the end-user rather than the consumable, and creating resistance to specification upgrades in cost-sensitive operations.

Growth Factors - Seismic-Qualified and Low-Temperature Toughness Consumables Expand Infrastructure Opportunities

According to Lincoln Electric data, the Innershield NR-305 flux-cored wire produces weld deposits with impact properties exceeding 27 J at minus 29 degrees Celsius. This low-temperature toughness opens the consumable to seismic and cold-climate structural applications. Construction projects in earthquake zones and arctic infrastructure programs require consumables certified to these impact thresholds, creating a qualified product demand pool with limited approved-supplier competition.

Lincoln Electric data indicates the Innershield NR-305 is qualified for seismic welding applications meeting AWS D1.8 and FEMA 353 requirements. These dual qualifications remove a key procurement barrier for structural steel fabricators working on seismic-rated buildings and critical infrastructure. Consumable vendors who hold multiple concurrent weld procedure qualifications reduce the customer’s approval workload, which translates directly into preferred-vendor preference during project procurement decisions.

Lincoln Electric data shows the Innershield NR-305 achieves typical Charpy V-notch impact toughness of 40 J at minus 29 degrees Celsius. This performance level exceeds the minimum qualification threshold, providing fabricators with a safety margin against batch-to-batch variability. Buyers who specify consumables with toughness headroom above minimum requirements reduce the risk of weld procedure re-qualification when environmental conditions in service become more demanding than initially specified.

Emerging Trends - High-Output Flux-Cored Welding Wires Support Automation and Heavy Fabrication Requirements

As reported by testtalkhq.com, gas-shielded flux-cored welding wire with 1/16-inch diameter achieves deposition rates of 12.0 to 20.0 lb per hour at welding currents of 200 to 350 amps. This output range exceeds solid wire performance by a substantial margin at comparable amperages. Fabricators who adopt gas-shielded FCAW on structural joints with extended weld lengths reduce labor cost per meter of completed weld, improving project profitability on steel-intensive contracts.

Lincoln Electric data indicates the Innershield NR-305 weld deposits exhibit a typical tensile strength of 550 MPa and a yield strength of 470 MPa. These mechanical property values support consumable qualification on high-strength structural steel joints that require defined minimum yield and tensile performance. Fabricators working with higher-grade base materials benefit from consumables that match structural steel specifications without requiring supplementary post-weld heat treatment.

testtalkhq.com data shows gas-shielded flux-cored wire with 5/64-inch diameter achieves deposition rates of 15.0 to 28.0 lb per hour at welding currents of 250 to 450 amps. This upper deposition range aligns with the throughput requirements of heavy plate fabrication in shipbuilding and offshore construction. Consumable vendors who offer large-diameter FCAW options qualified for heavy structural applications gain access to the highest-volume weld operations within the most active infrastructure construction sectors.

Regional Analysis

Asia Pacific Dominates the Welding Consumables Market with a Market Share of 43.80%, Valued at USD 6.7 Billion

Asia Pacific holds 43.80% of the global Welding Consumables Market, valued at USD 6.7 Billion in 2025. China, Japan, South Korea, and India drive this dominance through their concentrated shipbuilding, automotive, construction, and heavy engineering industries. Government-backed industrial expansion programs across the region direct continuous capital into infrastructure and manufacturing facilities that consume welding materials at scale throughout construction and operational phases.

North America holds a structurally strong position driven by energy pipeline construction, defense fabrication, and automotive manufacturing concentrated in the US and Canada. The region’s regulatory environment for weld quality and worker safety supports demand for certified premium consumables over unqualified lower-cost alternatives. This compliance structure protects average selling prices in North America relative to less-regulated markets in other geographies.

Europe benefits from established automotive manufacturing in Germany, France, and Italy alongside active offshore energy development in the North Sea region. EU environmental directives are accelerating adoption of low-fume welding consumables across industrial facilities. Vendors who develop compliant low-emission product lines ahead of regulatory implementation dates capture specification positions in European fabricator procedures before competitors complete their own product development cycles.

Latin America presents a growth-stage market anchored by Brazil’s offshore oil and gas sector and Mexico’s automotive manufacturing base. Both industries require certified welding consumables for structural and pressure-containing applications. Import dependence for premium consumable grades limits price competitiveness, but rising domestic manufacturing investment in both countries is gradually expanding local procurement options for fabricators seeking to reduce supply chain exposure.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Lincoln Electric holds the broadest strategic position in this market through its combination of welding equipment, consumables, and automation systems. The company completed three acquisitions between February and August 2025, covering mobile power solutions, robotic welding, and wear plate technologies. This acquisition pace signals an intent to build a full-service welding solutions business rather than competing as a consumable specialist, which expands its addressable revenue per customer relationship.

ESAB Corporation signed a definitive agreement in June 2025 to acquire EWM GmbH for approximately €275 million (USD 317 million), targeting completion in H2 2025. EWM is a German heavy industrial welding equipment and automation specialist. This acquisition gives ESAB a strengthened automation platform alongside its consumable portfolio, positioning the combined entity to compete more directly with Lincoln Electric on integrated solution contracts in European and global heavy industry markets.

Hyundai Welding operates within the shipbuilding and offshore energy supply chain, where its proximity to South Korean and Asian shipyard customers provides a logistics and technical service advantage over Western competitors. The company completed a strategic filler metal production capacity expansion in November 2025 focused on offshore wind and LNG shipbuilding. This capacity investment locks Hyundai Welding into growing clean energy infrastructure procurement before capacity constraints limit competitor response options.

Kobe Steel competes in the welding consumables market from a position of integrated steel and materials science expertise that informs its electrode and filler metal product development. Gas-shielded flux-cored welding wire at 5/64-inch diameter achieves deposition rates of 15.0 to 28.0 lb per hour at welding currents of 250 to 450 amps. Vendors with deep materials metallurgy capabilities develop consumables optimized for these high-output operating parameters, capturing the heavy structural fabrication segment where deposition rate is the primary procurement criterion.

Key Players

- Ador Welding

- Berkenhoff

- D&H Secheron

- Diffusion Engineers

- ESAB

- EWM

- Hilco Welding

- Hobart Welding Products

- Hyundai Welding

- Kobe Steel

- Lincoln Electric

- Miller Electric

- Nouveaux

- Panasonic

- Welding Alloys

Recent Developments

- April 2025 – Lincoln Electric acquired a 35% stake in Alloy Steel Australia, expanding its maintenance, repair, and wear plate technologies.

- August 2025 – Lincoln Electric acquired the remaining 65% of Alloy Steel Australia, completing full ownership of the wear plate and maintenance technology business.

- June 2025 – ESAB Corporation signed a definitive agreement to acquire EWM GmbH (Germany) for approximately €275 million (USD 317 million), targeting completion in H2 2025, to strengthen heavy industrial welding equipment and automation capabilities.

- November 2025 – Hyundai Welding completed a strategic expansion of filler metal production capacity focused on offshore wind and LNG shipbuilding applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 15.4 Billion |

| Forecast Revenue (2035) | USD 25.7 Billion |

| CAGR (2026-2035) | 5.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Electrodes: Shielded Metal Arc Welding Electrodes, Gas Metal Arc Welding Electrodes, Others; Fluxes: Submerged Arc Welding Flux, Oxy-Fuel Welding Flux, Others; Gases: Shielding Gases, Backing Gases, Others; Filler Metals: Solid Wire, Flux-Cored Wire, Metal-Cored Wire, Welding Rods, Others; Others); By Material Type (Mild Steel, Stainless Steel, Aluminum, Nickel Alloys, Copper Alloys, Others); By End Use (Construction, Automobile, Energy, Shipbuilding, Aerospace, Heavy Engineering, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Ador Welding, Berkenhoff, D&H Secheron, Diffusion Engineers, ESAB, EWM, Hilco Welding, Hobart Welding Products, Hyundai Welding, Kobe Steel, Lincoln Electric, Miller Electric, Nouveaux, Panasonic, Welding Alloys |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |