Quick Navigation

Report Overview

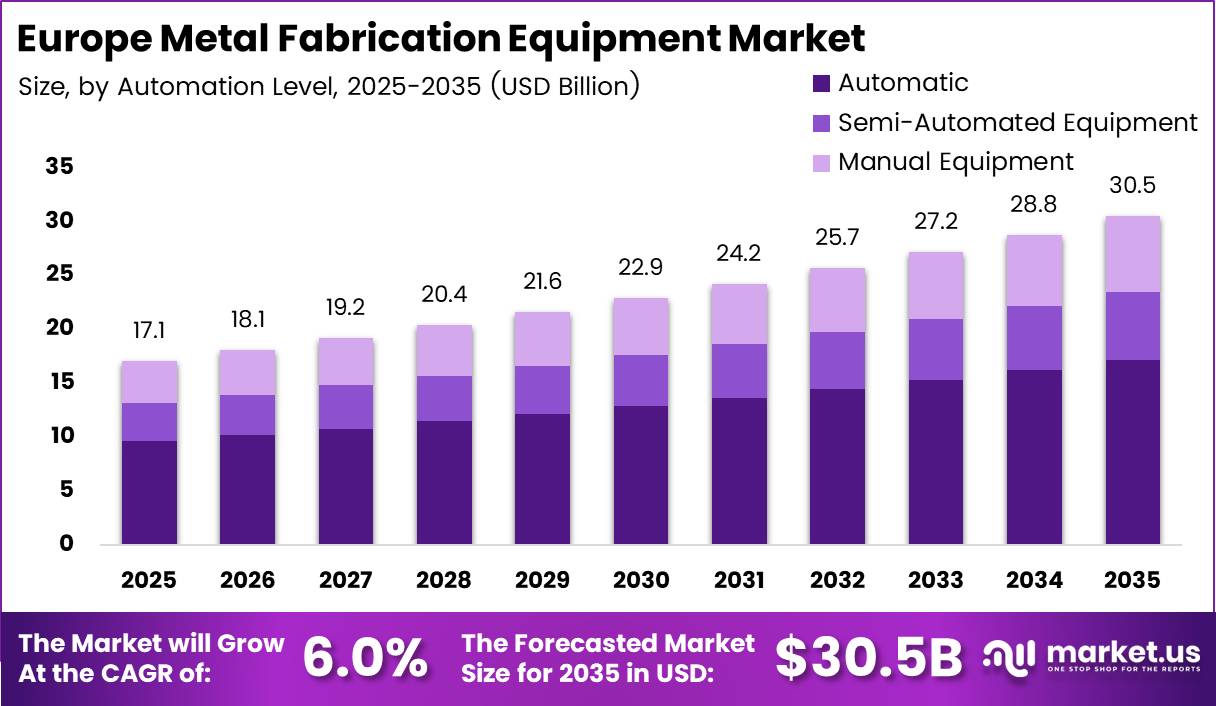

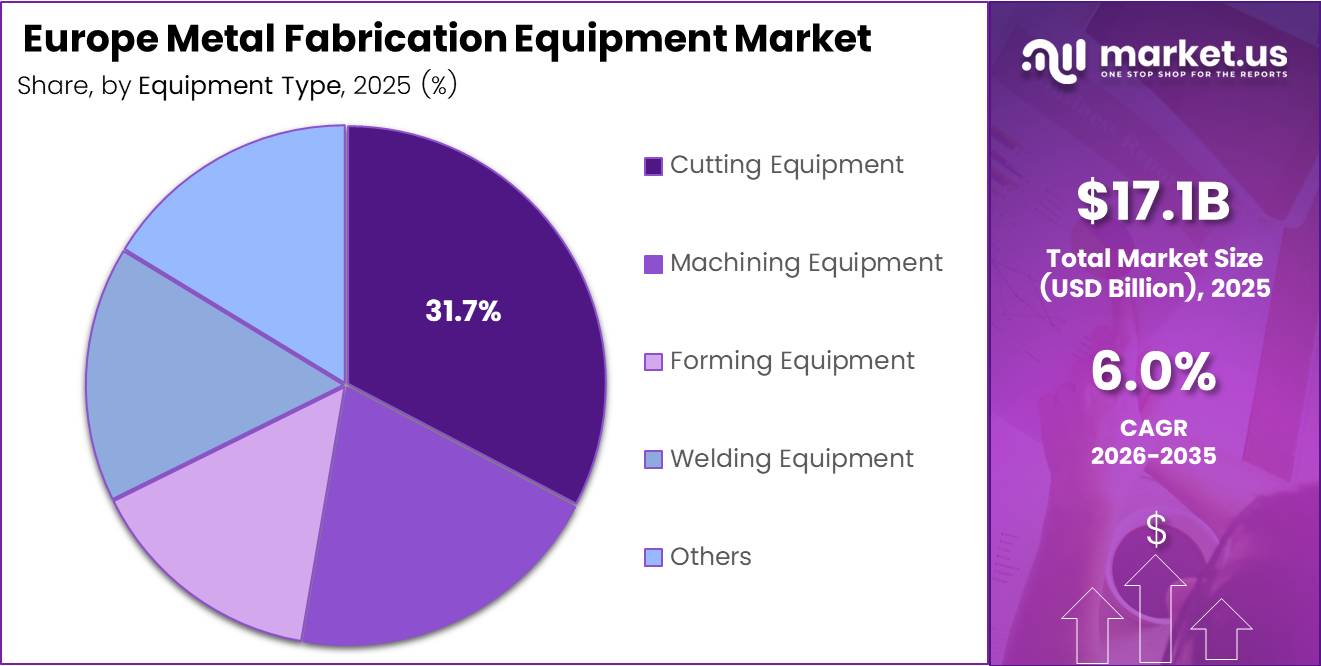

Europe Metal Fabrication Equipment Market size is expected to be worth around USD 30.5 Billion by 2035 from USD 17.1 Billion in 2025, growing at a CAGR of 6.0% during the forecast period 2026 to 2035.

Europe’s metal fabrication equipment sector sits at a structural inflection point. Industrial modernization programs across Germany, Italy, France, and the UK are replacing aging shop-floor machinery with fiber laser, CNC bending, and robotic welding systems. Manufacturers face a clear choice: upgrade or lose competitive ground to Eastern European and Asian rivals with newer installed bases.

The automotive and aerospace sectors anchor demand across the region. Both industries require tighter dimensional tolerances, faster cycle times, and lighter fabricated structures than legacy equipment can deliver. This pressure from end-user specifications is not cyclical. Electrification timelines and next-generation aircraft programs set hard deadlines that force capital investment decisions.

Renewable energy construction adds a parallel demand source. Wind turbine towers, solar mounting frames, and grid infrastructure all require precision-cut and formed steel components at scale. Fabricators supplying these projects need equipment capable of handling both high volume and high-mix orders, which favors automated and semi-automated machinery over manual alternatives.

Government-backed industrial policy reinforces private investment. Programs such as Germany’s National Industrial Strategy and the EU’s Net-Zero Industry Act direct capital toward domestic manufacturing capacity. These frameworks reduce investment risk for fabricators considering large equipment purchases, particularly in energy transition supply chains.

According to MIE Solutions, 80% of manufacturing executives plan to allocate 20% or more of their improvement budgets to smart manufacturing initiatives. This signals that equipment upgrades are no longer discretionary line items. They represent the primary vehicle through which fabricators expect to achieve efficiency and output targets over the next two to three years.

According to MIE Solutions, nearly 22% of manufacturers plan to implement autonomous robots and physical AI systems within two years. For equipment suppliers, this creates a clear product roadmap signal. Customers are not simply replacing machines. They are building automated cells that require integration-ready hardware from day one.

Key Takeaways

- The Europe Metal Fabrication Equipment Market was valued at USD 17.1 Billion in 2025 and is forecast to reach USD 30.5 Billion by 2035.

- The market grows at a CAGR of 6.0% from 2026 to 2035.

- Automatic equipment leads by automation level with a 56.2% market share in 2025.

- Cutting Equipment holds the largest share by equipment type at 31.7% in 2025.

- Automotive & Transportation is the dominant end-user segment with a 36.8% share in 2025.

- According to MIE Solutions, 80% of manufacturing executives are committing at least 20% of improvement budgets to smart manufacturing.

- Nearly 22% of manufacturers plan to deploy autonomous robots and physical AI systems within two years.

Automation Level Analysis

Automatic Equipment dominates with 56.2% due to labor cost reduction and throughput gains.

In 2025, Automatic Equipment held a dominant market position in the By Automation Level segment of the Europe Metal Fabrication Equipment Market, with a 56.2% share. European fabricators face persistent skilled labor shortages and rising wage costs. Automatic systems address both simultaneously, enabling continuous shift operations without proportional headcount increases.

Semi-Automated Equipment serves fabricators operating in high-mix environments where full automation is not economically justified. These systems combine operator skill with mechanized assistance, reducing per-part cycle times without the capital commitment of fully automated cells. However, the segment faces structural pressure as entry-level automation costs continue to fall.

Manual Equipment retains a role in specialist and low-volume fabrication contexts. Small job shops, repair operations, and highly customized one-off work keep manual machinery relevant. However, this segment is shrinking as a share of total market value, since larger fabricators systematically phase out manual processes during equipment refresh cycles.

Equipment Type Analysis

Cutting Equipment dominates with 31.7% due to universal application across all metal fabrication workflows.

In 2025, Cutting Equipment held a dominant market position in the By Equipment Type segment of the Europe Metal Fabrication Equipment Market, with a 31.7% share. Cutting is the entry point for virtually every fabrication process, which creates consistent baseline demand regardless of end-user industry. In August 2024, Bodor Laser launched the L Series large-format fiber laser cutting machine for heavy-duty sheet processing, illustrating how suppliers continue investing in this segment’s product depth.

Machining Equipment addresses precision material removal requirements across aerospace, defense, and industrial machinery fabrication. CNC machining centers and multi-axis turning systems command significant capital spend, particularly as component geometries grow more complex in next-generation power systems and electric drivetrains.

Forming Equipment encompasses press brakes, roll formers, and stamping presses used to create three-dimensional structures from flat sheet. Demand for forming equipment correlates closely with sheet metal enclosure production for electronics, HVAC systems, and transportation applications, all of which operate at high volumes in Europe.

Welding Equipment completes the fabrication process for structural and precision assemblies. Robotic welding cell adoption is accelerating across automotive tier-one suppliers and industrial equipment manufacturers, where consistent weld quality and traceability requirements now exceed what manual operators can reliably deliver at scale.

End-User Analysis

Automotive & Transportation dominates with 36.8% due to volume production demands and electrification tooling cycles.

In 2025, Automotive & Transportation held a dominant market position in the By End-User segment of the Europe Metal Fabrication Equipment Market, with a 36.8% share. Electric vehicle programs are forcing simultaneous retooling across stamping, welding, and cutting lines. OEMs and tier-one suppliers must meet new body structure specifications that existing equipment was not designed to produce efficiently.

Construction & Infrastructure represents the second significant end-user block. European infrastructure renewal programs, including bridge replacement, rail expansion, and urban development, sustain demand for structural steel fabrication capacity. Contractors and steel fabricators supplying these projects invest in forming and cutting equipment capable of processing high-strength steel grades.

Oil & Gas / Energy purchases fabrication equipment for pipeline components, pressure vessels, and offshore structures. Energy transition spending on hydrogen infrastructure and offshore wind foundations is adding new fabrication demand in this segment alongside conventional upstream and midstream work.

Aerospace & Defense fabricators require the highest precision tolerances and full material traceability. Investment in this segment prioritizes five-axis machining, precision laser cutting, and friction stir welding for aluminum and titanium airframe structures. Defense spending increases across Europe are directing new budget toward domestic production capacity.

Heavy Machinery & Industrial Equipment manufacturers maintain consistent replacement demand for forming and welding equipment. Agricultural machinery, mining equipment, and material handling systems all require high-strength fabricated structures produced in moderate volumes, favoring flexible semi-automated equipment configurations.

Key Market Segments

By Automation Level

- Automatic

- Semi-Automated Equipment

- Manual Equipment

By Equipment Type

- Cutting Equipment

- Laser Cutting

- Plasma Cutting

- Waterjet Cutting

- Oxy-fuel Cutting

- Machining Equipment

- Forming Equipment

- Welding Equipment

- Others

By End-User

- Automotive & Transportation

- Construction & Infrastructure

- Oil & Gas / Energy

- Aerospace & Defense

- Heavy Machinery & Industrial Equipment

- Others

Drivers

Factory Modernization Investment and Automation Adoption Are Accelerating Equipment Replacement Across Europe

European manufacturers are accelerating capital equipment cycles under pressure from two simultaneous forces: end-user quality specifications that legacy machinery cannot meet, and labor market conditions that make manual fabrication economically unviable. This combination creates structural replacement demand rather than incremental upgrades. Equipment suppliers benefit from a buyer base that cannot defer investment without losing production contracts.

According to MIE Solutions, ready-made analytic tools used in smart manufacturing operations achieve a median ROI of 140%, compared to 104% for custom-developed solutions. This gap matters because it shortens payback calculations for fabricators evaluating new equipment. When operators can demonstrate a clear return on connected machinery investments, budget approval timelines shorten significantly.

In September 2024, TRUMPF launched the TruMatic 5000 automated punch-laser combination machine with SheetMaster automation, targeting high-productivity sheet metal fabrication operations. This product reflects a broader supplier strategy of combining cutting and punching in integrated automated cells, reducing floor space requirements while increasing output per shift. Fabricators under capacity pressure find this configuration particularly compelling.

Restraints

High Capital Costs and Cybersecurity Exposure Constrain Adoption Among Mid-Size Fabricators

High equipment acquisition costs remain the primary barrier for small and medium-sized fabricators across Europe. A fully automated fiber laser cell with robotic material handling can exceed EUR 1 million before installation and training costs. Many job shops and regional fabricators cannot finance purchases at this scale without customer contract guarantees or government subsidy support, which limits the addressable market for premium systems.

Economic uncertainty compounds capital access problems. When industrial output contracts across key end-user sectors, fabricators defer investment decisions on major equipment even when long-term ROI is clear. Automotive production slowdowns, construction project delays, and energy sector volatility all create hesitation that suppresses purchase decisions in the near term, extending replacement cycles beyond suppliers’ forecasts.

According to MIE Solutions, 55% of manufacturers strongly agree that unauthorized access to operational technology systems is a high concern, while 47% view intellectual property theft as a critical risk. For fabricators evaluating connected equipment, these concerns add hidden costs in the form of cybersecurity infrastructure, OT network segmentation, and compliance requirements, which raise the true total cost of connected fabrication systems above the sticker price.

Growth Factors

Electric Vehicle Supply Chains and Smart Factory Investment Are Creating New Revenue Opportunities for Equipment Suppliers

Electric vehicle manufacturing requires fabricated battery enclosures, motor housings, and lightweight structural components built to specifications that differ fundamentally from internal combustion equivalents. This is not a simple retooling exercise. EV production demands new laser cutting tolerances, specialized welding processes for aluminum and high-strength steel, and forming equipment capable of handling advanced material grades at production volumes.

In April 2025, LVD Group introduced the Easy-Cell, a robotic bending cell integrating an Easy-Form press brake with automated robotic part handling. This product directly addresses the high-mix, low-volume production challenge facing fabricators supplying multiple EV models simultaneously. Automated bending cells that can switch between part programs without manual setup changes reduce the labor cost per component while maintaining schedule flexibility.

According to MIE Solutions, 85% of surveyed manufacturers report that smart manufacturing initiatives attract new talent. This finding matters for equipment procurement decisions because labor recruitment is now a factor in capital investment justification. Fabricators can present equipment upgrades to workforce planners and HR leadership as talent retention tools, broadening the internal stakeholders who support purchasing decisions.

Emerging Trends

AI-Driven Process Optimization and IoT-Connected Equipment Are Reshaping Fabrication Economics Across Europe

Artificial intelligence applications in metal fabrication are moving beyond prototype stage. Machine learning models trained on cutting parameter data now adjust laser power, speed, and focus position in real time to maintain cut quality across material thickness variations. Fabricators using these systems report reduced scrap rates and fewer operator interventions per shift, which directly improves cost per part.

Collaborative robots are expanding into welding, cutting assist, and material handling roles where safety cage requirements previously blocked adoption. New cobots certified for direct human interaction allow fabricators to deploy automation in existing floor layouts without facility modification costs. This removes one of the most common objections to automation investment among mid-size fabricators evaluating their first robotic installations.

According to MIE Solutions, the manufacturing industry generates approximately 2 petabytes of data annually, more than any other sector. IoT-enabled fabrication equipment contributes to this data volume through continuous sensor streams covering machine health, energy consumption, and cycle time metrics. In October 2025, Prima Power received industry recognition for its Giga Laser Next, a four-head 3D laser cutting system for automotive fabrication, illustrating how connected multi-head systems now process complex 3D geometries while generating performance data for continuous process improvement.

Key Company Insights

TRUMPF holds the strongest technology positioning in the European market through its combined fiber laser, punch-laser, and sheet metal storage systems portfolio. The company’s October 2025 acquisition of majority control in STOPA Anlagenbau, raising its stake from 25.1% to 74.9%, signals a deliberate move to control the material handling layer of automated fabrication cells. This vertical integration strategy locks customers into TRUMPF-native workflows across the full cutting and storage cycle.

Bystronic competes on throughput efficiency and software integration for sheet metal specialists. The February 2026 launch of the ByCut Star 3015 fiber laser cutting machine targets fabricators who prioritize cutting speed and operational cost per part over raw machine capability. Bystronic’s strength in software-driven production management gives it a differentiated position as fabricators shift from standalone machines toward connected cell architectures.

Amada builds its European position on deep application engineering capability and its own direct service network. A real-world case study from Smart Manufacturing Ltd in the UK demonstrates the commercial impact of Amada’s approach. After investing more than £1 million in Amada machines and automating overnight lights-out production, Smart Manufacturing grew its turnover from £4 million toward a projected £8 million over five years, representing a doubling of revenue tied directly to the equipment investment.

DMG MORI addresses the precision machining requirements of aerospace, medical, and high-performance automotive fabricators across Europe. Its five-axis machining centers and multi-tasking turning systems serve customers who need both metal removal and turning capability within a single machine envelope. This convergence reduces floor space and setup time for complex components, giving DMG MORI a defensible position among fabricators producing high-value, low-volume parts.

Key Players

- TRUMPF

- Bystronic

- Amada

- DMG MORI

- Mazak

- Salvagnini

- Danobat Group

- Schuler Group

- Prima Industrie

Recent Developments

- February 2026 – Bystronic launched the ByCut Star 3015, a new fiber laser cutting machine designed to improve cutting speed and operational efficiency for sheet metal fabricators across Europe.

- March 2026 – Salvagnini Group introduced the latest generation of its P4 panel bender, featuring enhanced automation and adaptive bending technology for flexible metal fabrication environments.

- October 2025 – TRUMPF increased its shareholding in STOPA Anlagenbau GmbH from 25.1% to 74.9%, acquiring a controlling stake in the automated storage and material-handling systems supplier.

- July 2025 – TRUMPF completed the divestment of its metal additive manufacturing business through acquisition by Lenbach Equity Opportunities III, sharpening its focus on core fabrication equipment.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 17.1 Billion |

| Forecast Revenue (2035) | USD 30.5 Billion |

| CAGR (2026-2035) | 6.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Automation Level (Automatic, Semi-Automated Equipment, Manual Equipment), By Equipment Type (Cutting Equipment, Machining Equipment, Forming Equipment, Welding Equipment, Others), By End-User (Automotive & Transportation, Construction & Infrastructure, Oil & Gas / Energy, Aerospace & Defense, Heavy Machinery & Industrial Equipment, Others) |

| Competitive Landscape | TRUMPF, Bystronic, Amada, DMG MORI, Mazak, Salvagnini, Danobat Group, Schuler Group, Prima Industrie |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |