Quick Navigation

- Report Overview

- Key Takeaways

- Machine Type Analysis

- Automation Level Analysis

- Container / Packaging Type Analysis

- Application / End-Use Industry Analysis

- Distribution Channel Analysis

- Key Market Segments

- Regional Analysis

- Key Regions and Countries

- Drivers

- Restraints

- Challenges

- Opportunities

- Key Company Insights

- Recent Developments

- Report Scope

Report Overview

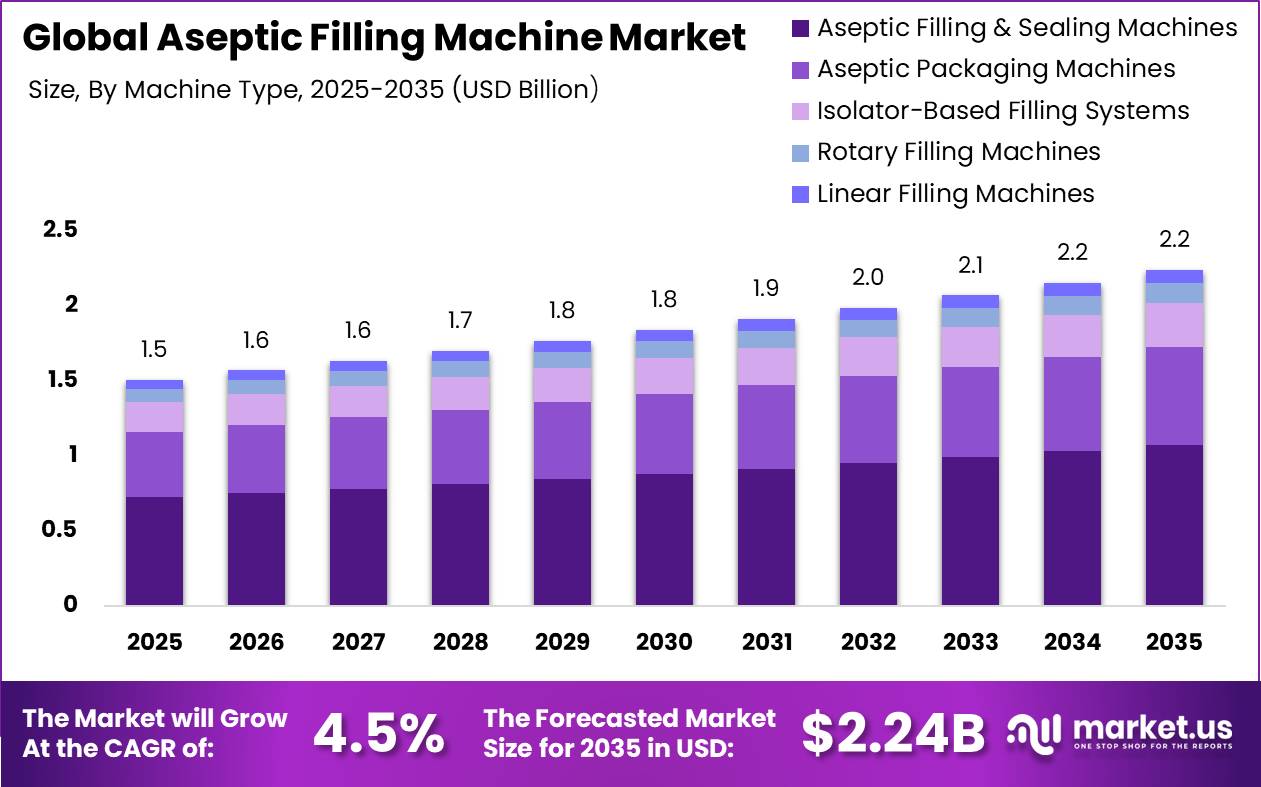

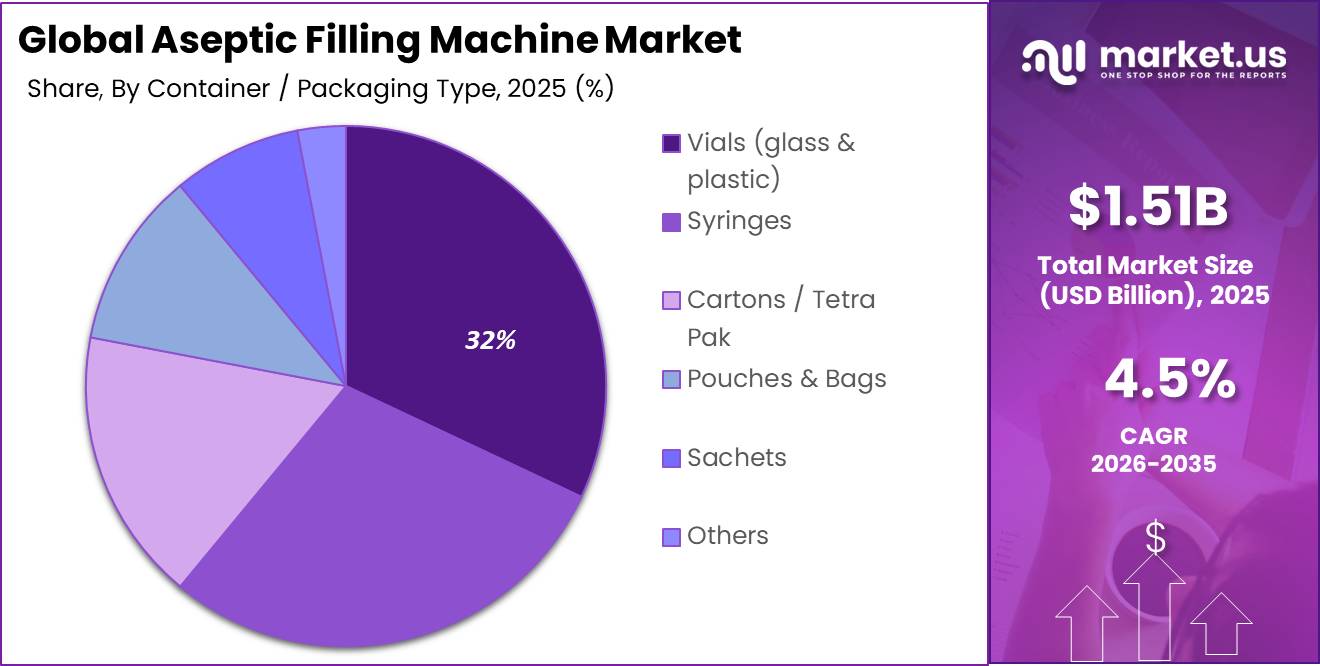

Global Aseptic Filling Machine Market size is expected to be worth around USD 2.24 Billion by 2035 from USD 1.51 Billion in 2025, growing at a CAGR of 4.5% during the forecast period 2026 to 2035. This growth reflects rising sterile production needs across pharmaceutical and food manufacturing facilities worldwide.

This means aseptic filling machines fill and seal products under sterile conditions to prevent microbial contamination. The market spans machine types, automation levels, container formats, and end-use industries. Pharmaceutical, food and beverage, nutraceutical, and cosmetic manufacturers rely on these systems for shelf-stable, contamination-free products.

Key Takeaways

- Global market size is valued at USD 1.51 Billion in 2025 and projected to reach USD 2.24 Billion by 2035.

- The market is set to grow at a CAGR of 4.5% between 2026 and 2035.

- Aseptic Filling & Sealing Machines dominate the By Machine Type segment with a 48.00% share.

- Manual and Semi-Automatic systems lead the By Automation Level segment with a 72.00% share.

- Vials hold the largest share in the By Container Type segment at 32.00%.

- Pharmaceutical and Biopharmaceutical applications dominate the By Application segment with a 52.00% share.

- Direct Sales lead the By Distribution Channel segment with a 58.00% share.

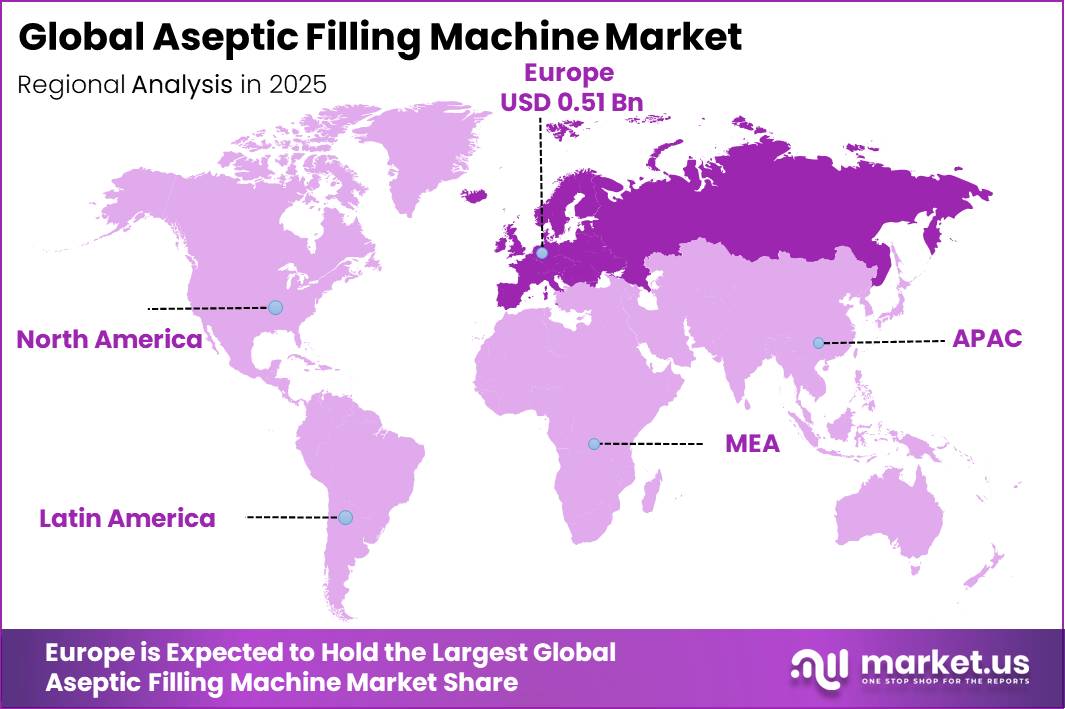

- Europe dominates the regional landscape with a 34.00% share, valued at USD 0.51 Billion.

Governments worldwide continue funding sterile manufacturing infrastructure to secure vaccine and biologic supply chains. This signals sustained capital allocation toward fill-finish capacity across regulated regions. Equipment suppliers offering modular, qualification-ready systems stand to benefit as procurement programs accelerate deployment timelines.

Regulatory bodies enforce strict sterility standards across pharmaceutical and biopharmaceutical manufacturing facilities. According to FDA, aseptic processing requires operations within an ISO Class 5 environment for critical exposure zones during sterile drug manufacturing. This means equipment makers must engineer systems that meet exacting contamination control benchmarks for regulatory approval.

As reported by FDA, aseptic manufacturing validation must demonstrate at least 3 consecutive successful validation runs before process approval. This requirement increases qualification timelines for new filling lines. Consequently, manufacturers favor equipment vendors who provide strong validation documentation and technical support during commissioning.

Machine Type Analysis

Aseptic Filling & Sealing Machines dominates with 48.00% due to high-speed sterile fill-seal integration demand.

In 2025, Aseptic Filling & Sealing Machines held a dominant market position in the By Machine Type segment of Aseptic Filling Machine Market, with a 48.00% share. As reported by ChemDAQ, hydrogen peroxide concentrations of 30% to 35% are typically used in these systems to eliminate microorganisms without residue. This supports reliable contamination control and buyer confidence.

Automation Level Analysis

Manual / Semi-Automatic dominates with 72.00% due to lower upfront capital requirements.

In 2025, Manual / Semi-Automatic systems held a dominant market position in the By Automation Level segment of Aseptic Filling Machine Market, with a 72.00% share. As per our research, production duration between sterility revalidation cycles can extend beyond 150 hours for low-acid products on advanced lines. This shows mature operators still favor flexible manual configurations for varied batch sizes.

Container / Packaging Type Analysis

Vials (glass & plastic) dominates with 32.00% due to broad pharmaceutical compatibility and reuse.

In 2025, Vials (glass & plastic) held a dominant market position in the By Container Type segment of Aseptic Filling Machine Market, with a 32.00% share. Vials remain the preferred format across pharmaceutical and biopharmaceutical fill-finish lines because they support multidose and single-dose formats alike. This versatility keeps vial-compatible filling equipment in steady procurement demand.

Application / End-Use Industry Analysis

Pharmaceutical & Biopharmaceutical dominates with 52.00% due to strict sterile production requirements.

In 2025, Pharmaceutical & Biopharmaceutical held a dominant market position in the By Application segment of Aseptic Filling Machine Market, with a 52.00% share. Pharmaceutical manufacturers require validated sterile fill-finish lines to protect injectable and biologic drug products from contamination. This dependency keeps pharmaceutical buyers as the primary revenue base for aseptic equipment vendors.

Distribution Channel Analysis

Direct Sales dominates with 58.00% due to complex equipment customization needs.

In 2025, Direct Sales held a dominant market position in the By Distribution Channel segment of Aseptic Filling Machine Market, with a 58.00% share. Equipment buyers prefer direct manufacturer engagement to manage complex validation, customization, and qualification requirements. This preference limits the role of intermediaries in high-value aseptic equipment transactions.

Key Market Segments

By Machine Type

- Aseptic Filling & Sealing Machines

- Aseptic Packaging Machines

- Isolator-Based Filling Systems

- Rotary Filling Machines

- Linear Filling Machines

By Automation Level

- Manual / Semi-Automatic

- Fully Automatic

By Container / Packaging Type

By Application / End-Use Industry

- Pharmaceutical & Biopharmaceutical

- Food & Beverage

- Nutraceuticals & Dietary Supplements

- Cosmetics & Personal Care

- Others

By Distribution Channel

- Direct Sales (Manufacturer to end-user)

- Distributors & Agents

- System Integrators

- Others

Regional Analysis

Europe Dominates the Aseptic Filling Machine Market with a Market Share of 34.00%, Valued at USD 0.51 Billion

Europe leads the Aseptic Filling Machine Market with a 34.00% share, valued at USD 0.51 Billion in 2025. Strict regulatory frameworks across the region push pharmaceutical manufacturers toward validated, high-compliance fill-finish equipment. This regulatory pressure sustains steady capital investment in sterile processing infrastructure, reinforcing Europe’s position as the leading regional market for aseptic filling systems.

Asia Pacific is growing as a regional market for aseptic filling equipment. In 2026, Sidel expanded its aseptic PET filling deployments through the Britannia Winkin’ Cow project in India, implementing a high-speed Combi Predis line capable of 24,000 bottles per hour. This signals rising regional demand for high-throughput sterile beverage packaging systems.

North America, Latin America, and the Middle East & Africa complete the regional footprint for aseptic filling equipment. These regions support pharmaceutical, food, and beverage manufacturing activity. As a result, equipment vendors maintain distribution presence across these markets alongside their core European and Asia Pacific operations.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Drivers

Vaccine fill-finish resilience buildout strengthens demand for aseptic filling equipment worldwide. The WHO Immunization Agenda 2030 targets 90% coverage for essential vaccines and aims to halve the number of zero-dose children by 2030. Governments are investing in regional manufacturing capacity to reduce reliance on imported vaccines.

This investment increases demand for modular, technology-transfer-ready filling systems suited to multidose and single-dose vaccine formats. Equipment selection increasingly depends on qualification speed and batch-size flexibility. Therefore, vendors offering rapid-deployment platforms gain an advantage in donor-backed procurement programs.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Annex 1 compliance-driven line upgrades | +2.6% | EU core, UK, Switzerland, advanced APAC | Short term (≤ 2 years) |

| Sterile shortage-led capacity expansion | +2.3% | North America core, EU, India | Short term (≤ 2 years) |

| RTU vial and syringe adoption | +2.0% | North America, EU, Japan, South Korea | Medium term (2-4 years) |

| Vaccine fill-finish resilience buildout | +1.9% | South Asia, Africa, LATAM, ASEAN | Medium term (2-4 years) |

| High-value biologics serialization pressure | +1.7% | North America, EU, major APAC biologics hubs | Medium term (2-4 years) |

| Operator-minimizing robotic asepsis | +1.8% | Global regulated plants | Long term (≥ 4 years) |

Restraints

Regulatory non-compliance shutdown risk restrains the aseptic filling equipment market. FDA identifies manufacturing quality issues as the leading cause of drug shortages, with sterile injectables especially vulnerable due to limited qualified production lines. Enforcement activity during 2025 documented significant CGMP violations at finished-pharmaceutical facilities.

A contamination-control failure can trigger batch rejection, warning letters, or prolonged remediation programs. This raises caution among manufacturers approving new equipment investments. Consequently, buyers demand extensive factory acceptance testing and supplier audits, lengthening procurement cycles and slowing equipment order conversion.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High validation-linked CapEx hurdle | -2.2% | North America, EU, Japan, South Korea | Medium term (2-4 years) |

| Regulatory non-compliance shutdown risk | -1.9% | Global regulated plants | Short term (≤ 2 years) |

| Sterile project payback uncertainty | -1.6% | North America, EU, India, LATAM | Medium term (2-4 years) |

| Long OEM delivery bottlenecks | -1.5% | EU, North America, APAC export corridors | Short term (≤ 2 years) |

| Utility-intensive facility readiness gaps | -1.3% | Emerging Asia, Africa, LATAM, secondary EU sites | Long term (≥ 4 years) |

| Legacy line upgrade deferral | -1.2% | EU core, North America, mature APAC | Medium term (2-4 years) |

Challenges

Aseptic talent scarcity challenges the market because sterile manufacturing demands expertise in contamination control, microbiology, and qualification science. Global immunization initiatives aim to save more than 50 million lives by 2030, increasing demand for qualified fill-finish operations across growing numbers of facilities worldwide.

Shortages of specialized personnel slow production ramp-up and increase dependence on OEM field-service support. First-year line performance can fall 8 to 15 percentage points below design targets when teams lack aseptic experience. As a result, manufacturers invest in training academies and simulation-based qualification programs.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Isolator validation complexity | -1.3% | EU regulatory hubs, North America, Japan | Medium term (2-4 years) |

| Sterile component lead-time volatility | -1.1% | EU, North America, APAC supply corridors | Short term (≤ 2 years) |

| FAT-SAT qualification slippage | -1.0% | Global export-oriented OEM networks | Medium term (2-4 years) |

| Aseptic talent scarcity | -1.2% | North America, Western Europe, India biopharma hubs | Long term (≥ 4 years) |

| Format-change yield instability | -0.9% | Multi-format CDMO clusters globally | Medium term (2-4 years) |

| Digital integrity integration burden | -0.8% | Highly regulated global plants | Long term (≥ 4 years) |

Opportunities

Multi-format flexible micro-batches open a clear opportunity as manufacturers increasingly need low-volume, high-mix production capability. Sterile injectable supply remains vulnerable since manufacturing disruptions and quality issues continue contributing to drug shortages. Demand is rising for platforms that switch quickly between syringes, vials, and cartridges.

Robotic and isolator-integrated systems can cut format-change labor by 30% to 40%, improving operational flexibility. These platforms can also lower minimum economic batch size by approximately 50%, making small production runs commercially viable. This means manufacturers gain higher asset utilization across mixed-product facilities.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Multi-format flexible micro-batches | +2.4% | North America, EU, Japan, South Korea | Short term (≤ 2 years) |

| Regional sterile capacity localization | +2.7% | North America core, EU, India, GCC | Medium term (2-4 years) |

| Annex 1 retrofit conversion kits | +2.1% | EU regulatory hubs, UK, advanced APAC | Short term (≤ 2 years) |

| Vaccine-ready modular lines | +2.5% | Africa, South Asia, LATAM, ASEAN | Medium term (2-4 years) |

| High-potency contained filling cells | +1.9% | North America, EU, oncology hubs in APAC | Medium term (2-4 years) |

| Lifecycle consumables and digital services | +1.8% | Global installed base | Long term (≥ 4 years) |

Key Company Insights

DNP positions itself as a high-throughput specialist in aseptic PET bottle filling for beverage applications. As reported by DNP, its aseptic system achieves line speeds of up to 72,000 bottles per hour with overall line efficiency above 98%. This performance edge attracts large-scale beverage manufacturers seeking maximum production output and consistent quality.

Sidel expands its aseptic PET portfolio to meet rising beverage manufacturer demand for flexible sterile packaging. In 2025, Sidel scaled modular aseptic filling lines capable of up to 60,000 containers per hour. This scalability gives Sidel an advantage among high-volume manufacturers needing flexible multi-format production capacity.

Key Players

- DNP

- Sidel

- Syntegon

- IMA Group

- ProSys Sampling Systems Limited

Recent Developments

- 2025 – Syntegon unveiled its SynTiso liquid filling line concept at Pharmatag 2025, introducing a next-generation aseptic filling platform focused on higher efficiency, reduced contamination risk, and modular sterile processing for injectable pharmaceuticals.

- February 2026 – IMA Group announced the acquisition of a majority stake in ProSys Sampling Systems Limited, strengthening its isolator and aseptic sampling portfolio for sterile pharmaceutical fill-finish operations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.51 Billion |

| Forecast Revenue (2035) | USD 2.24 Billion |

| CAGR (2026-2035) | 4.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Machine Type (Aseptic Filling & Sealing Machines, Aseptic Packaging Machines, Isolator-Based Filling Systems, Rotary Filling Machines, Linear Filling Machines), By Automation Level (Manual / Semi-Automatic, Fully Automatic), By Container / Packaging Type (Vials, Syringes, Cartons / Tetra Pak, Pouches & Bags, Sachets, Others), By Application / End-Use Industry (Pharmaceutical & Biopharmaceutical, Food & Beverage, Nutraceuticals & Dietary Supplements, Cosmetics & Personal Care, Others), By Distribution Channel (Direct Sales, Distributors & Agents, System Integrators, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | DNP, Sidel, Syntegon, IMA Group, ProSys Sampling Systems Limited |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |