Quick Navigation

Report Overview

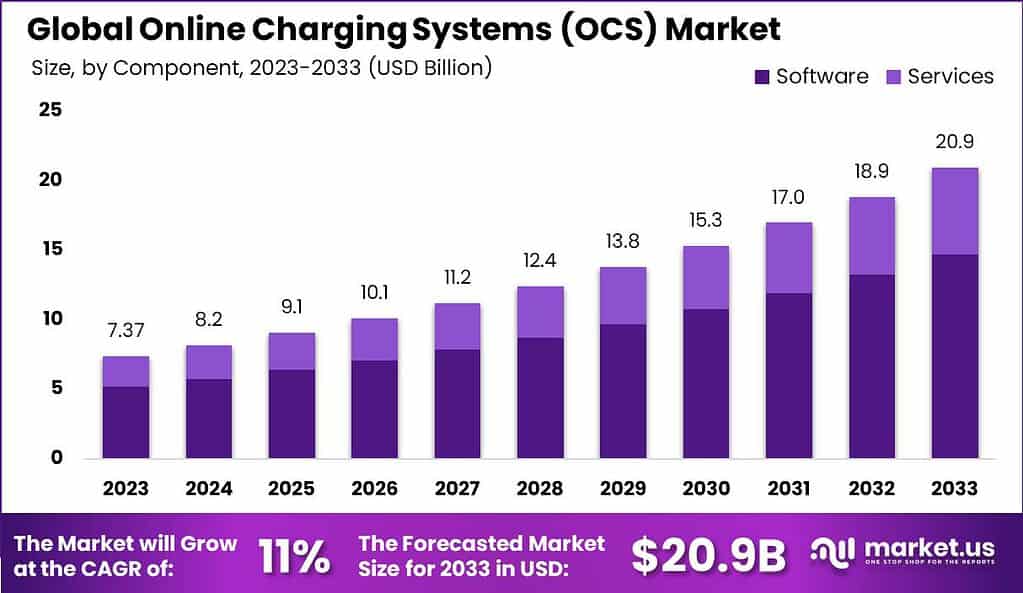

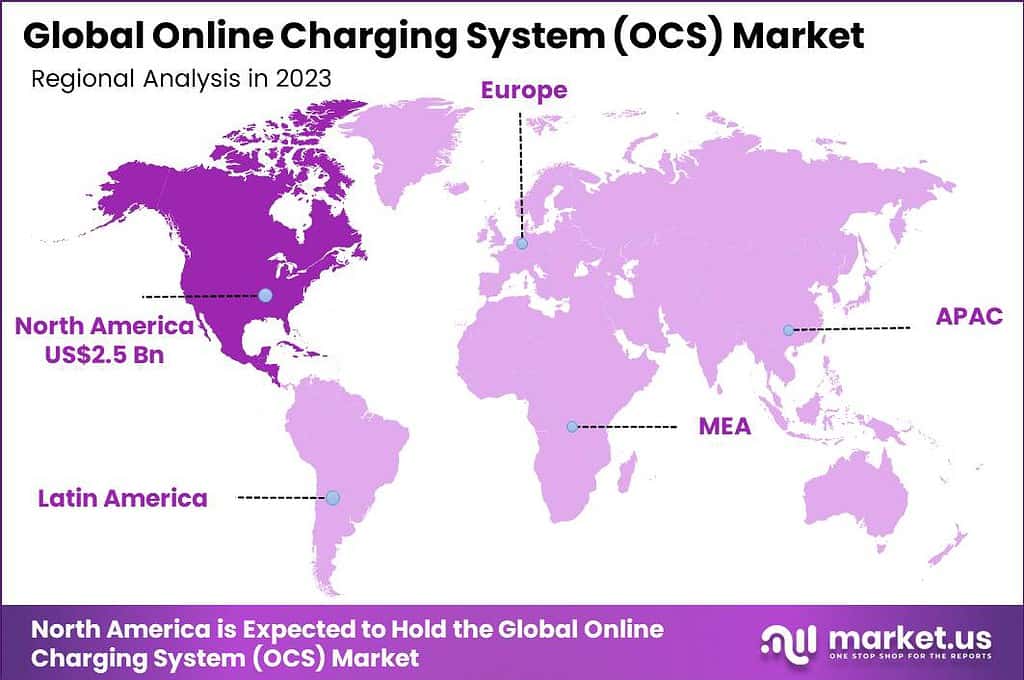

The Global Online Charging System (OCS) Market size is expected to be worth around USD 20.9 Billion By 2033, from USD 7.37 Billion in 2023, growing at a CAGR of 11% during the forecast period from 2024 to 2033. In 2023, North America emerged as the leader in the Online Charging System (OCS) market, holding a significant market share of over 35.1% with market share showcasing impressive revenue figures, approximately at USD 2.5 Billion.

An Online Charging System (OCS) is a telecommunications industry solution designed to facilitate real-time charging and billing processes. This system is crucial for service providers as it allows for immediate charging of services such as voice calls, data usage, and SMS directly from the user’s account balance. OCS ensures that customers are billed accurately based on their service usage, enabling service providers to manage credits in real-time and prevent revenue loss.

The Online Charging System market is experiencing significant growth due to the increasing demand for real-time billing solutions and the expansion of telecommunication services worldwide. This market includes a variety of stakeholders, from mobile network operators to software solution providers, all contributing to the development and implementation of advanced OCS platforms.

The primary growth drivers for the Online Charging System market include the widespread adoption of mobile devices and the surge in data consumption. As more consumers use data-intensive applications, the need for effective real-time charging systems becomes crucial. Additionally, the shift towards 5G networks is prompting telecom operators to upgrade their charging systems to handle more complex billing arrangements.

A key trend in the OCS market is the integration of AI and machine learning technologies, which enhance the efficiency and accuracy of billing operations. These technologies help in predicting customer usage patterns and adjusting billing cycles accordingly. Furthermore, there’s a growing preference for cloud-based OCS solutions, as they offer scalability and flexibility while reducing operational costs.

The demand for Online Charging Systems is primarily driven by the ongoing expansion of telecommunication networks and services across emerging markets. These systems are essential for managing the billing of millions of transactions daily, ensuring customer satisfaction and operational efficiency.

The continuous evolution of mobile technology and the introduction of new telecommunication standards present numerous opportunities for the growth of the OCS market. There is also significant potential in developing regions where mobile connectivity is rapidly expanding, necessitating robust and scalable charging solutions. Additionally, the advent of IoT and its integration with mobile networks opens new avenues for the application of OCS in various industries, including automotive and smart home technology.

Key Takeaways

- The Global Online Charging System (OCS) Market is projected to grow from USD 7.37 Billion in 2023 to around USD 20.9 Billion by 2033, at a Compound Annual Growth Rate (CAGR) of 11% during the forecast period from 2024 to 2033.

- In 2023, the Software segment of the OCS market held the largest share, accounting for over 70.2% of the market.

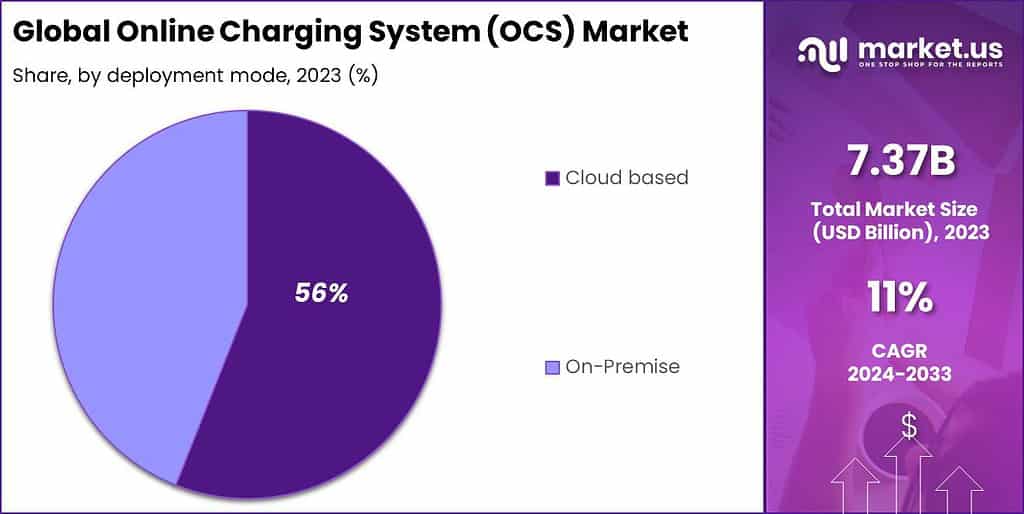

- The Cloud segment also took a leading position in the market, capturing more than 56% of the market share in 2023.

- The Mobile Network segment led the market with a significant share, capturing over 75% in 2023.

- Large Enterprises held a dominant position in the market, securing over 65% of the market share in 2023.

- The Telecom and Communication segment was dominant in the OCS market, holding more than 60% of the market share in 2023.

- North America led the OCS market in 2023, with a market share of over 35.1%, translating to revenue of approximately USD 2.5 billion.

Component Analysis

In 2023, the Software segment of the Online Charging System (OCS) market held a dominant position, capturing more than a 70.2% share. This significant market share is largely attributed to the critical role that software plays in the functionality and efficiency of OCS.

The software component is the backbone of OCS, providing the necessary algorithms and databases for real-time billing and customer management. It ensures accurate billing, fraud detection, and supports flexible tariff settings, which are essential for telecom operators to adapt to rapidly changing market demands.

The leadership of the Software segment is also bolstered by continuous advancements in technology. As telecom networks evolve towards more complex systems like 5G, the demand for sophisticated OCS software that can handle increased data throughput and more intricate charging models grows.

Furthermore, the increasing customization needs of telecom operators drive the growth of the Software segment. Operators seek tailored solutions that can integrate seamlessly with their existing operations as new technologies and service models emerge. OCS software providers are focusing on developing modular and scalable software solutions that can be customized to meet these diverse requirements, ensuring their dominance in the market.

Deployment Mode Analysis

In 2023, the Cloud segment of the Online Charging System (OCS) market held a dominant position, capturing more than a 56% share. This significant market share is primarily due to the scalable and flexible nature of cloud-based solutions, which are increasingly favored by telecommunications companies and service providers.

Cloud-based OCS solutions offer several advantages that make them appealing. They reduce the need for substantial upfront capital expenditures on hardware and infrastructure, which is a critical consideration for companies aiming to cut costs while expanding their service offerings.

The leadership of the cloud segment in the OCS market is also bolstered by its inherent capacity for innovation. Cloud platforms facilitate easier integration with other digital systems and advanced technologies like AI and machine learning, enabling more sophisticated billing models and enhanced customer service capabilities.

Network Type Analysis

In 2023, the Mobile Network segment of the Online Charging System (OCS) market held a dominant market position, capturing more than a 75% share. This leadership is primarily driven by the global surge in mobile device usage and increasing mobile data consumption as consumers and businesses increasingly rely on mobile connections for both personal and professional tasks.

The preference for mobile networks in the OCS market is also fueled by the widespread adoption of smartphones and the rollout of advanced mobile technologies such as 5G. These advancements necessitate more dynamic and flexible charging systems that can manage new billing models and data services offered by mobile operators.

Additionally, the mobile network segment benefits from the ongoing trends toward IoT and machine-to-machine communications, where mobile networks often provide the backbone for connectivity. As these technologies scale, the complexity of billing and service delivery increases, making sophisticated OCS solutions more critical.

Organization Size Analysis

In 2023, the Large Enterprises segment held a dominant market position in the Online Charging System (OCS) market, capturing more than a 65% share. This substantial market share is largely attributed to the high capital investment capabilities of large enterprises, which enable them to adopt advanced OCS solutions.

These organizations often handle massive volumes of customer data and transactions, necessitating robust, scalable systems to manage billing operations efficiently. The demand for OCS in large enterprises is driven by the need for real-time charging and complex billing solutions that can support a vast array of services and customer bases.

Large enterprises are increasingly focusing on enhancing customer experiences and streamlining billing operations, which further drives the adoption of sophisticated OCS solutions. The integration of OCS allows these organizations to offer more personalized and flexible service packages, adapting quickly to market changes and customer needs. This adaptability is crucial in sectors such as telecommunications and media, where service offerings are highly diversified and require dynamic pricing models.

Vertical Analysis

In 2023, the Telecom and Communication segment held a dominant market position in the Online Charging System (OCS) market, capturing more than a 60% share. This leadership is primarily driven by the critical need within the telecom sector to manage vast volumes of data and complex billing cycles efficiently.

As telecommunications companies expand their service offerings from voice and data to streaming and IoT services they require robust systems capable of real-time charging and billing to enhance customer satisfaction and streamline revenue management.The rapid evolution of mobile technology and the proliferation of connected devices have compelled telecom operators to upgrade their existing billing systems to OCS.

The growth of the Telecom and Communication segment is also bolstered by regulatory pressures. Many regions require telecom providers to ensure transparency in billing and to support consumer rights by preventing billing errors and enabling customer self-service. Online Charging Systems play a crucial role in fulfilling these regulatory requirements by providing precise, real-time billing information that helps protect consumer interests.

Key Market Segments

By Component

- Services

- Software

By Deployment Mode

- Cloud

- On-Premise

By Network Type

- Mobile Network

- Fixed Network

By Organization Size

- Large Enterprises

- Small And Medium-Sized Enterprises

By Vertical

- Telecom and Communication

- BFSI

- Media and Entertainment

- Healthcare

- Other Industries

Driver

Increasing Demand for Real-Time Billing Solutions in Telecom

The Online Charging System (OCS) market is primarily driven by the escalating need for real-time billing solutions within the telecom sector. As data consumption surges, propelled by the expansion of 4G and 5G networks, telecom operators are increasingly seeking effective ways to manage network usage and customer charges in real-time.

This trend is underscored by the growing customer demand for clear and controlled data expenditure. OCS enables operators to offer flexible pricing models and enhance customer satisfaction by providing immediate updates on usage and costs, thereby building trust and fostering loyalty.

Restraint

Integration Complexities with Legacy Systems

Integrating modern OCS platforms with existing legacy systems poses a significant challenge, hindering market growth. Many telecom operators operate on outdated billing systems, and transitioning to advanced OCS requires considerable time, financial investment, and technical expertise.

This complex integration can lead to service disruptions and costly errors, deterring operators, especially in smaller or developing markets, from adopting new technologies. The financial burden and the operational upheaval of training staff and modifying workflows further exacerbate the reluctance towards OCS adoption.

Opportunity

Expansion of 5G Networks

The rollout of 5G networks worldwide presents a substantial opportunity for the OCS market. The intricate billing requirements of 5G services, which encompass various charges like data, speed, and latency, demand sophisticated OCS solutions.

As 5G heralds a range of new applications and services, from enhanced mobile broadband to IoT connectivity, telecom operators require OCS that can support dynamic and diverse billing arrangements. This adaptability allows for the customization of plans based on user consumption and application use, potentially opening up new revenue avenues systems.

The rise of 5G also opens the door to new revenue streams for telecom companies, such as edge computing, private networks, and IoT applications, all of which will require real-time charging and billing solutions. As telecom operators look to capitalize on the 5G opportunity, investing in OCS technology will be a critical component of their strategy.

Challenge

Ensuring Scalability and Performance

As telecom networks expand and diversify, particularly with the advent of 5G and IoT, a significant challenge for OCS providers is ensuring scalability and high performance. The increasing number of connected devices and users requires OCS platforms to manage larger volumes of data interactions efficiently.

Scalability issues can lead to billing inaccuracies and customer dissatisfaction, impacting operator revenues. To address this, OCS solutions must be robust enough to handle peak demands without degradation in service, necessitating ongoing investments in infrastructure and technological upgrades to maintain performance standards.

Emerging Trends

The Online Charging System (OCS) market is witnessing significant changes driven by advancements in telecommunications. One key trend is the integration of OCS with real-time data processing and policy control solutions. This convergence allows for more dynamic billing strategies that can adapt to user behavior and network conditions instantaneously, ensuring a more personalized customer experience.

Another important development is the rising adoption of cloud-based OCS solutions. These offer scalability and flexibility, reducing the infrastructural cost for telecom operators and enabling quicker deployment of services. Operators can rapidly deploy their charging systems to meet the dynamic demands of the market by leveraging cloud computing. This approach eliminates the need for significant upfront investments in hardware and infrastructure.

The proliferation of 5G technology is particularly transformative for OCS. It demands more sophisticated billing solutions that can accommodate the high data throughput and diverse service offerings characteristic of 5G networks. There is also an increasing shift towards convergent billing platforms that can handle multiple service types and payment methods seamlessly.

Business Benefits

Implementing an advanced OCS offers numerous business advantages for telecom operators. Firstly, it enhances revenue generation capabilities by supporting innovative billing models that can be tailored to individual customer needs and market demands. For example, dynamic pricing models enable operators to adjust prices based on real-time factors such as network congestion or user activity levels, maximizing profitability.

Additionally, OCS significantly improves customer satisfaction by providing transparency in billing and real-time account management. Customers gain access to up-to-the-minute updates on their usage and spending, which helps prevent bill shock and builds trust. OCS also automates many aspects of the billing process, reducing manual errors and operational costs. It also supports the rapid introduction of new services, which is crucial in the fast-evolving telecom industry.

The flexibility and agility provided by modern OCS solutions are critical in a landscape increasingly dominated by data-driven services and the Internet of Things (IoT). As telecom operators expand their offerings to include a wider array of connected devices and tailored service packages, OCS platforms that can efficiently manage these complexities will become indispensable.

Regional Analysis

In 2023, North America held a dominant market position, capturing more than 35.1% market share, with revenue reaching around USD 2.5 billion in the Online Charging System (OCS) market. This leadership can be attributed to the high penetration of 4G and 5G networks and the advanced telecommunication infrastructure in the region.

Leading operators in the U.S. and Canada, such as AT&T, Verizon, and T-Mobile, have been rapidly investing in OCS solutions to improve their billing systems, enhance customer experience, and support real-time data usage tracking. The strong presence of tech giants in the software and telecom industries also contributes to North America’s dominance in the OCS market.

One of the critical reasons for North America’s leadership is its early adoption of digital transformation initiatives, particularly in the telecom sector. The region’s growing demand for real-time service delivery, especially in industries like entertainment, e-commerce, and streaming services, has pushed telecom operators to implement more robust OCS solutions. Also, the regulatory environment in the U.S. and Canada encourages innovations and investment in digital billing systems.

In addition to infrastructure and technology adoption, consumer behavior plays a significant role in market dominance. North American consumers are highly engaged with on-demand services and mobile data consumption, which require efficient online charging and billing systems.

As a result, telecom operators in the region continue to upgrade their OCS systems to offer seamless and flexible billing options, driving further market growth. With the projected expansion of 5G services across the continent, the demand for advanced OCS platforms is expected to remain high in the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

The Online Charging System (OCS) is a crucial component in telecommunications and other sectors that require real-time billing and charging capabilities. Key players in this market include major telecommunications companies, specialized software providers, and cloud service platforms and compete to offer solutions that enable real-time charging.

Ericsson stands as a leading innovator in the Online Charging System (OCS) market. Their technology allows telecommunications operators to handle charging for services in real-time, enhancing customer satisfaction through transparent and flexible billing solutions. Ericsson’s OCS solutions are designed to support the rapid deployment of new services, which is crucial in the dynamically evolving telecom sector.

Huawei Technologies Co., Ltd. is another dominant force in the OCS market, known for its robust infrastructure and pioneering software solutions.Their OCS platform integrates seamlessly with existing mobile network architectures, providing operators with powerful tools to monetize their networks. Huawei’s solutions are particularly user-friendly interfaces with the ability to support a multitude of billing scenarios, from prepaid to postpaid systems.

Nokia Corporation’s OCS solutions are at the forefront of enabling real-time transparency for billing and charging processes. Their platform is built to accommodate the vast data demands of modern networks, supporting everything from traditional voice services to the latest IoT applications.

Top Key Players in the Market

- Ericsson

- Huawei Technologies Co., Ltd.

- Nokia Corporation

- Amdocs

- ZTE Corporation

- Oracle Corporation

- Comviva (A Tech Mahindra Company)

- CSG International

- SAP SE

- Salesforce Inc.

- Other Key Players

Recent Developments

- Ericsson: In 2023, Ericsson continued to enhance its OCS solutions with a focus on enabling 5G monetization. Ericsson’s convergent charging system supports real-time charging capabilities and is designed to handle the increased data usage and demands brought by 5G networks. This solution offers telecom providers greater flexibility and the ability to introduce innovative pricing models for services like cloud gaming and IoT.

- Huawei Technologies: Huawei’s OCS solutions are built to optimize 5G network monetization by supporting real-time charging for both prepaid and postpaid services. In 2023, Huawei launched updates to its OCS platform, emphasizing scalability and integration with AI for personalized service offerings.

- Nokia Corporation: Nokia introduced its Nokia Converged Charging (NCC) solution in 2023, which plays a pivotal role in enabling 5G monetization for telecom operators. It supports real-time rating and charging and integrates no-code functionalities to simplify service creation. This helps operators introduce new 5G services quickly, ensuring flexible and innovative charging models.

- Amdocs: In 2023, Amdocs strengthened its RevenueONE platform, which includes comprehensive OCS functionalities for 5G services. The company’s acquisition of Openet has bolstered its policy control and real-time charging capabilities, which are critical for supporting advanced 5G scenarios like network slicing and IoT.

- Oracle Corporation: Oracle’s Cloud Scale Charging solution, introduced in 2023, focuses on supporting 5G networks with low-latency and high-transaction capabilities. The solution integrates real-time charging functionalities and supports the dynamic requirements of telecom operators as they transition to 5G.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 7.37 Bn |

| Forecast Revenue (2033) | USD 20.9 Bn |

| CAGR (2024-2033) | 11% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Services, Software), By Deployment Mode (Cloud, On-Premise), By Network Type (Mobile Network, Fixed Network), By Organization Size (Large Enterprises, Small And Medium-Sized Enterprises), By Vertical (Telecom and Communication, BFSI, Media and Entertainment,Healthcare, Other Industries) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Ericsson, Huawei Technologies Co., Ltd., Nokia Corporation, Amdocs, ZTE Corporation, Oracle Corporation, Comviva (A Tech Mahindra Company), CSG International, SAP SE, Salesforce Inc., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Market")