Quick Navigation

Report Overview

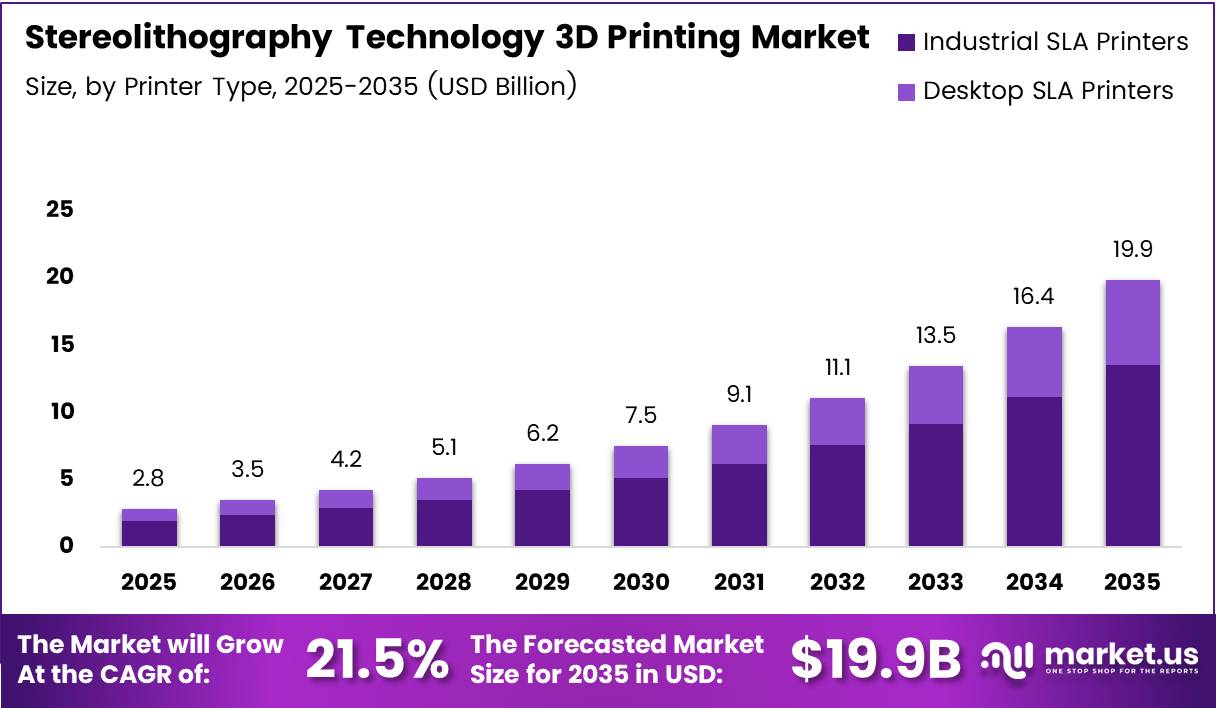

Global Stereolithography (SLA) Technology 3D Printing Market size is expected to be worth around USD 19.9 Billion by 2035 from USD 2.8 Billion in 2025, growing at a CAGR of 21.5% during the forecast period 2026 to 2035.

The stereolithography (SLA) technology 3D printing market covers hardware, photopolymer materials, and software platforms used to fabricate three-dimensional objects through ultraviolet laser curing of liquid resin. SLA produces parts with high dimensional accuracy and smooth surface finishes. These properties make it distinct from powder-bed and filament-based additive methods.

The market spans desktop printers for professional prototyping, industrial systems for end-use manufacturing, and application-specific platforms for dental and medical workflows. End-users range from independent designers and engineering firms to large aerospace, automotive, and healthcare manufacturers. This structural breadth creates multiple parallel revenue streams.

Government bodies in North America, Europe, and Asia Pacific actively support advanced manufacturing programs that fund additive technology adoption. Regulatory pathways for SLA-produced medical devices and dental components continue to expand. This regulatory progress opens procurement channels that were previously closed to photopolymer-based manufacturing.

Defense agencies and national research institutions allocate procurement budgets toward SLA-enabled tooling and precision component production. Public investment in aerospace and medical infrastructure generates sustained institutional demand. This creates a revenue floor that commercial demand alone cannot provide.

According to 3D Systems data, the SLA 825 Dual achieves feature sizes down to 0.127 mm in the XY plane. This resolution level enables detailed functional parts that previously required traditional machining. Manufacturers who adopt this specification gain a measurable quality advantage over competitors relying on older SLA platforms.

Data from 3D Systems shows the SLA 825 Dual delivers up to 25% faster build speeds than previous models through dual synchronized laser technology. Faster throughput directly reduces per-unit production cost. This performance shift moves SLA from a prototyping tool into a viable low-volume production platform, expanding the addressable market significantly.

Key Takeaways

- The global SLA Technology 3D Printing Market was valued at USD 2.8 Billion in 2025 and is forecast to reach USD 19.9 Billion by 2035.

- The market grows at a CAGR of 21.5% during the forecast period 2026 to 2035.

- Industrial SLA Printers dominate the By Printer Type segment with a 67.2% share in 2025.

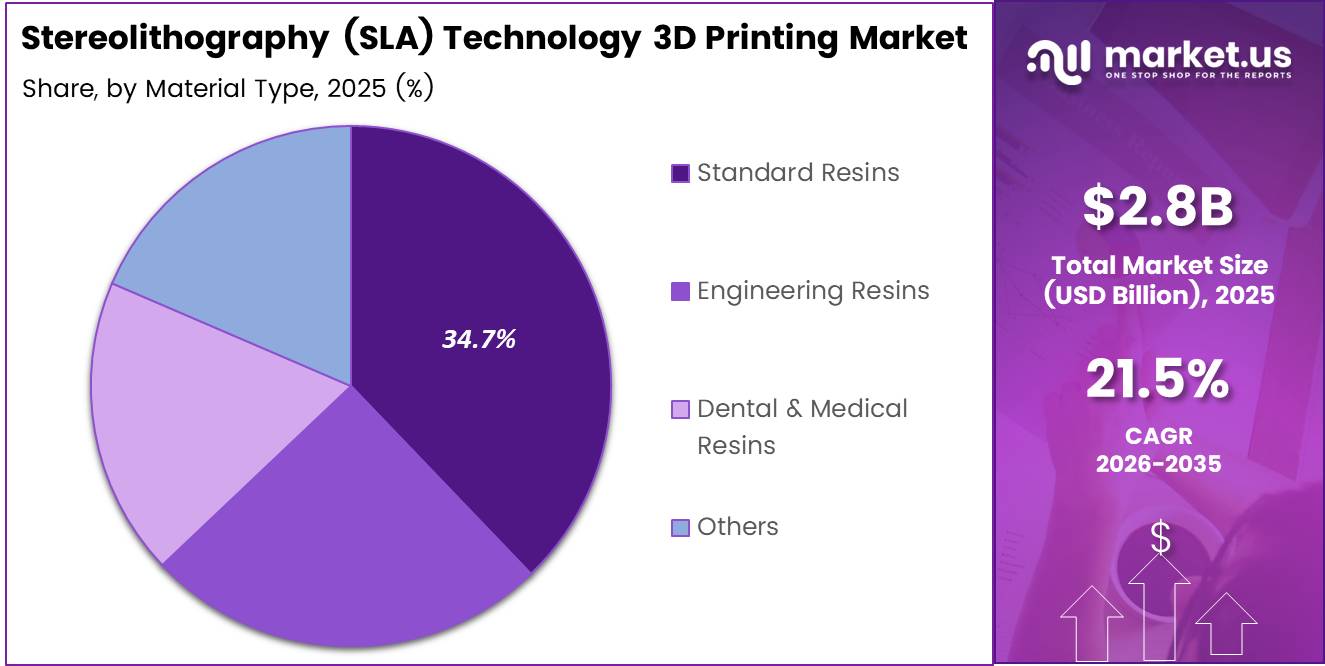

- Standard Resins hold a 34.7% share, making them the leading material type sub-segment.

- Healthcare leads the By End-Use segment with a 24.8% share in 2025.

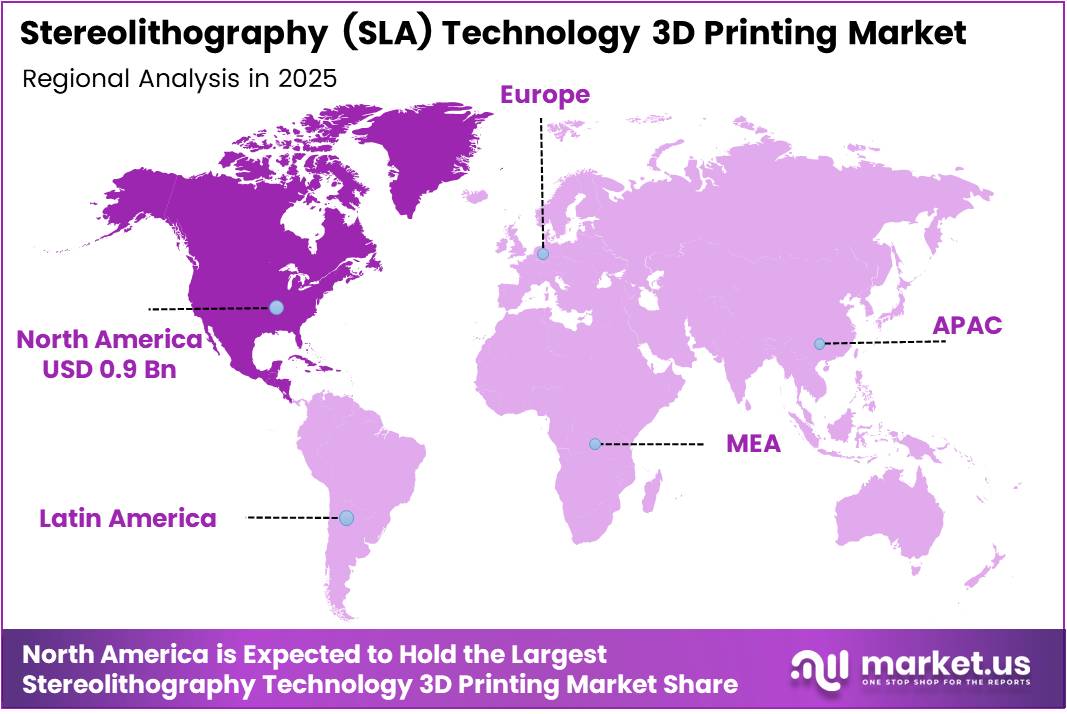

- North America is the dominant region with a 32.70% market share, valued at USD 0.9 Billion in 2025.

Market Dynamics

Drivers - Advanced SLA Platforms Bridge the Gap Between Additive Manufacturing and CNC Precision

According to 3D Systems, the SLA 825 Dual achieves feature sizes down to 0.127 mm in the XY plane. This resolution closes the gap between additive and subtractive machining for precision components. Engineering teams that previously outsourced fine-detail parts to CNC suppliers can now bring that work in-house with SLA systems, reducing cost and lead time simultaneously.

3D Systems data shows the SLA 825 Dual provides a build volume of 830 x 830 x 550 mm, enabling larger parts and higher part density per production run. Larger build envelopes reduce per-part cost by allowing more units per cycle. Manufacturers who need both scale and precision now have a single platform that delivers both, removing a key barrier to SLA adoption in production environments.

As reported by 3D Systems, the SLA 825 Dual delivers up to 25% faster build speeds through dual synchronized laser technology. Speed directly reduces machine-hour cost and improves return on capital. This performance level makes SLA commercially competitive against faster but lower-accuracy additive technologies, widening the pool of buyers who can justify the investment.

Restraints - Post-Processing Complexity and Operational Requirements Increase Total SLA Production Costs

SLA-manufactured parts require washing, curing, and support removal before use, adding labor and consumable costs not present in some competing additive methods. This post-processing burden raises the total cost per part, particularly for low-volume runs. Buyers operating in cost-sensitive segments weigh this overhead against the precision benefit and frequently select lower-resolution alternatives.

3D Systems indicates dimensional accuracy reaches plus or minus 0.051 mm for parts smaller than 34 mm, with 0.15% cumulative tolerance for larger components. While this accuracy is industry-leading, achieving it consistently requires controlled print environments, calibrated systems, and skilled operators. These operational requirements add indirect cost that smaller facilities cannot easily absorb.

Based on 3D Systems data, ArrayCast software reduces manual labor requirements by 20 times during SLA-based investment-casting tree creation. This figure confirms that without automation tools, manual post-processing workflows remain a significant cost barrier. Vendors who do not offer workflow automation alongside hardware will find their systems limited to buyers with large labor budgets, narrowing addressable market reach.

Growth Factors - High-Throughput Automated SLA Manufacturing Expands Production Efficiency and Industrial Applications

3D Systems indicates the dental version of the SLA 825 Dual prints up to 2 times faster than comparable single-laser SLA systems. Dental laboratories operate on tight daily turnaround requirements tied to patient scheduling. A 2x speed gain translates directly into higher daily case throughput without adding capital equipment, making the upgrade economically justified for high-volume dental practices.

Data from 3D Systems shows the SLA 825 Dual delivers up to 3 times the throughput of previous-generation or smaller-platform SLA printers. Higher throughput per machine reduces the number of units required to meet production targets. This drives a favorable total cost of ownership calculation that supports capital expenditure approval at the facility level, pulling forward adoption decisions.

As reported by 3D Systems, the SLA 825 Dual is designed for continuous 24/7 production and automated lights-out manufacturing. This operational model removes shift dependency and aligns SLA with standard factory automation expectations. Manufacturers who adopt lights-out SLA workflows gain a structural cost advantage that compounds over time relative to competitors using shift-dependent production methods. 3D Systems also confirms SLA can manufacture parts up to 1,500 mm in length at production-grade accuracy, opening large-component aerospace and industrial markets to additive methods.

Emerging Trends - Expanded Build Capacity, Broad Material Compatibility, and Continuous Innovation Strengthen SLA Market Competitiveness

3D Systems indicates the SLA 825 Dual delivers a 20% larger build volume than the previous generation platform. As platform build envelopes expand, manufacturers gain the ability to consolidate multi-part assemblies into single prints. This consolidation reduces assembly labor and improves structural integrity, creating a product differentiation argument that justifies SLA over competing technologies in large-component workflows.

Figures from 3D Systems show the company has released 21 SLA printer models over three decades, demonstrating a disciplined cadence of hardware advancement. This history signals continued platform investment to prospective buyers. Organizations evaluating long-term additive manufacturing strategies treat vendor development history as a proxy for future support reliability, giving established SLA vendors a procurement preference over newer market entrants.

According to 3D Systems, the company supports more than 80 SLA material formulations across its stereolithography platform. This material depth enables application coverage that single-material vendors cannot match. The SLA 825 Dual operates with layer resolutions ranging from 50 to 150 microns, giving operators precision control across applications from fine jewelry to structural industrial components. Vendors who combine broad material libraries with flexible resolution settings hold a decisive advantage in multi-vertical sales environments.

Printer Type Analysis

Industrial SLA Printers dominates with 67.2% due to high-volume manufacturing and precision requirements.

In 2025, Industrial SLA Printers held a dominant market position in the By Printer Type segment of the Stereolithography (SLA) Technology 3D Printing Market, with a 67.2% share. Industrial buyers require larger build volumes, tighter tolerances, and continuous production capability. These requirements disqualify desktop alternatives, locking institutional spend into industrial platforms and concentrating revenue with vendors offering production-grade systems.

Desktop SLA Printers serve professional designers, dental laboratories, educational institutions, and small engineering firms requiring high-resolution output at lower capital cost. Formlabs launched its Developer Platform in October 2024, opening its SLA ecosystem to third-party materials. This move broadens desktop platform utility and positions the segment to capture spend from buyers previously committed to proprietary industrial systems.

Material Type Analysis

Standard Resins dominates with 34.7% due to broad compatibility and lower per-unit material cost.

In 2025, Standard Resins held a dominant market position in the By Material Type segment of the Stereolithography (SLA) Technology 3D Printing Market, with a 34.7% share. Standard resins offer the widest printer compatibility and lowest price per litre among SLA materials. This cost and compatibility combination drives first-purchase decisions and supports high-volume prototyping workflows across industries.

Engineering Resins deliver mechanical properties such as heat resistance, stiffness, and impact strength that standard formulations cannot match. Aerospace, automotive, and electronics manufacturers specify engineering resins for functional component testing. Vendors who expand engineering resin portfolios capture a premium-priced segment with structurally higher margins.

Dental and Medical Resins serve clinical and surgical applications that demand biocompatibility certification and dimensional accuracy meeting regulatory standards. Demand for these materials ties directly to healthcare and dental industry capital spending. As regulatory approvals for SLA-produced clinical devices expand, dental and medical resin revenue grows at a faster rate than the broader materials segment.

Others in the material type segment include castable, ceramic-filled, and specialty photopolymers serving jewelry, electronics, and research applications. These niche materials command higher prices and serve buyers with highly specific performance requirements. Vendors who build specialty formulation capabilities alongside standard lines create a defensible multi-segment revenue position.

End-Use Analysis

Healthcare dominates with 24.8% due to precision requirements and device customization demand.

In 2025, Healthcare held a dominant market position in the By End-Use segment of the Stereolithography (SLA) Technology 3D Printing Market, with a 24.8% share. Clinical workflows for surgical planning, patient-specific implants, and dental prosthetics require dimensional tolerances and surface quality that SLA delivers better than most competing additive methods. This technical fit concentrates healthcare procurement into SLA platforms.

Automotive manufacturers use SLA for rapid prototype iteration, aerodynamic wind-tunnel models, and tooling inserts where surface finish and dimensional repeatability affect test validity. Stratasys launched the Neo800+ in April 2025 specifically for wind-tunnel testing and tooling, confirming active vendor commitment to this application. Automotive spend in SLA will follow platform performance gains rather than general market conditions.

Aerospace buyers specify SLA for lightweight structural prototypes, complex ducting, and flight-test components where conventional fabrication timelines are prohibitive. High tolerance requirements align with SLA’s measurable accuracy advantages. Vendors targeting aerospace must demonstrate compliance with industry qualification standards as a prerequisite for contract procurement.

Consumer Goods manufacturers use SLA for product design visualization, packaging prototypes, and pre-production appearance models. Desktop SLA systems serve this segment well, keeping entry cost low. As desktop platforms expand material compatibility, consumer goods prototyping adoption will increase among medium-sized design studios.

Manufacturing end-users apply SLA for jigs, fixtures, molds, and short-run production components where tooling lead time creates a bottleneck in conventional workflows. The ability of industrial SLA systems to operate in continuous 24/7 lights-out environments removes the shift-based constraint that previously limited additive adoption in factory settings.

Key Market Segments

By Printer Type

- Industrial SLA Printers

- Desktop SLA Printers

By Material Type

- Standard Resins

- Engineering Resins

- Dental & Medical Resins

- Others

By End-Use

- Healthcare

- Automotive

- Aerospace

- Consumer Goods

- Manufacturing

- Education

- Others

Regional Analysis

North America holds 32.70% of the global SLA Technology 3D Printing Market, valued at USD 0.9 Billion in 2025. The region benefits from concentrated aerospace, defense, and medical device manufacturing sectors that require SLA-grade precision. Strong venture and institutional capital flows into additive manufacturing startups and scale-up facilities, sustaining both demand creation and supply-side innovation simultaneously.

Europe holds a structurally important share driven by automotive and aerospace manufacturing bases in Germany, France, and the UK. Regulatory frameworks for medical device additive manufacturing are well-developed across the EU. This regulatory maturity enables faster commercialization of SLA-produced clinical components, giving European medical OEMs a compliance advantage over counterparts in markets with slower approval pathways.

Asia Pacific is the highest-growth regional market within this forecast. China, Japan, and South Korea operate large-scale electronics, automotive, and industrial manufacturing sectors that generate consistent SLA demand for tooling and prototyping. Government-funded smart manufacturing programs across the region direct capital into additive technology adoption, accelerating institutional procurement timelines beyond what private sector spending alone would achieve.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

3D Systems Inc. holds the deepest institutional position in the SLA market as the originator of stereolithography technology. The company has released 21 SLA printer models over three decades and supports more than 80 material formulations. This hardware-materials ecosystem creates switching costs that protect installed-base revenue and gives 3D Systems a formidable retention advantage over single-product competitors.

Formlabs anchors the professional and desktop SLA tier through a combination of accessible hardware pricing and a closed-loop materials ecosystem. The company acquired Micronics in July 2024 to strengthen its additive manufacturing portfolio. This acquisition signals an intent to move beyond desktop SLA into complementary polymer technologies, broadening Formlabs’ revenue base while reinforcing its position in accessible professional prototyping.

Stratasys approaches the SLA market from a position of multi-technology additive strength, giving it cross-sell leverage with industrial customers already using its FDM and PolyJet systems. The April 2025 Neo800+ launch targets aerospace, automotive, and tooling applications with up to 50% faster throughput than prior models. This positions Stratasys to compete directly for large-format industrial SLA contracts where speed and scale are primary procurement criteria.

Peopoly targets cost-sensitive buyers in the desktop and prosumer SLA tier, competing on price-to-performance ratio rather than material ecosystem breadth. A peer-reviewed study on SLA-manufactured NdFeB magnets found a coercivity of 0.923 T. This functional magnetic performance from stereolithography demonstrates the material science potential that advanced desktop SLA platforms can unlock for research and specialty manufacturing buyers.

Key Players

- 3D Systems Inc.

- Formlabs

- Stratasys

- Peopoly

- XYZ printing

- FlashForge

- Zortrax

- B9Creations

- Shining 3D

- Prusa Research a.s

- Anycubic

- Phrozen Technology

- Kudo3D

- Asiga

Recent Developments

- October 2024 – Formlabs launched the Form 4L and Form 4BL, large-format SLA 3D printers built on its Low Force Display (LFD) technology, expanding high-speed stereolithography capabilities for industrial prototyping and production applications.

- April 2025 – Stratasys launched the Neo800+, a next-generation large-format SLA 3D printer designed for tooling, wind-tunnel testing, aerospace, automotive, and high-precision industrial applications, delivering up to 50% faster throughput than previous models.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.8 Billion |

| Forecast Revenue (2035) | USD 19.9 Billion |

| CAGR (2026-2035) | 21.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Printer Type (Industrial SLA Printers, Desktop SLA Printers); By Material Type (Standard Resins, Engineering Resins, Dental & Medical Resins, Others); By End-Use (Healthcare, Automotive, Aerospace, Consumer Goods, Manufacturing, Education, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | 3D Systems Inc., Formlabs, Stratasys, Peopoly, XYZ printing, FlashForge, Zortrax, B9Creations, Shining 3D, Prusa Research a.s, Anycubic, Phrozen Technology, Kudo3D, Asiga |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Technology 3D Printing Market")