Quick Navigation

Report Overview

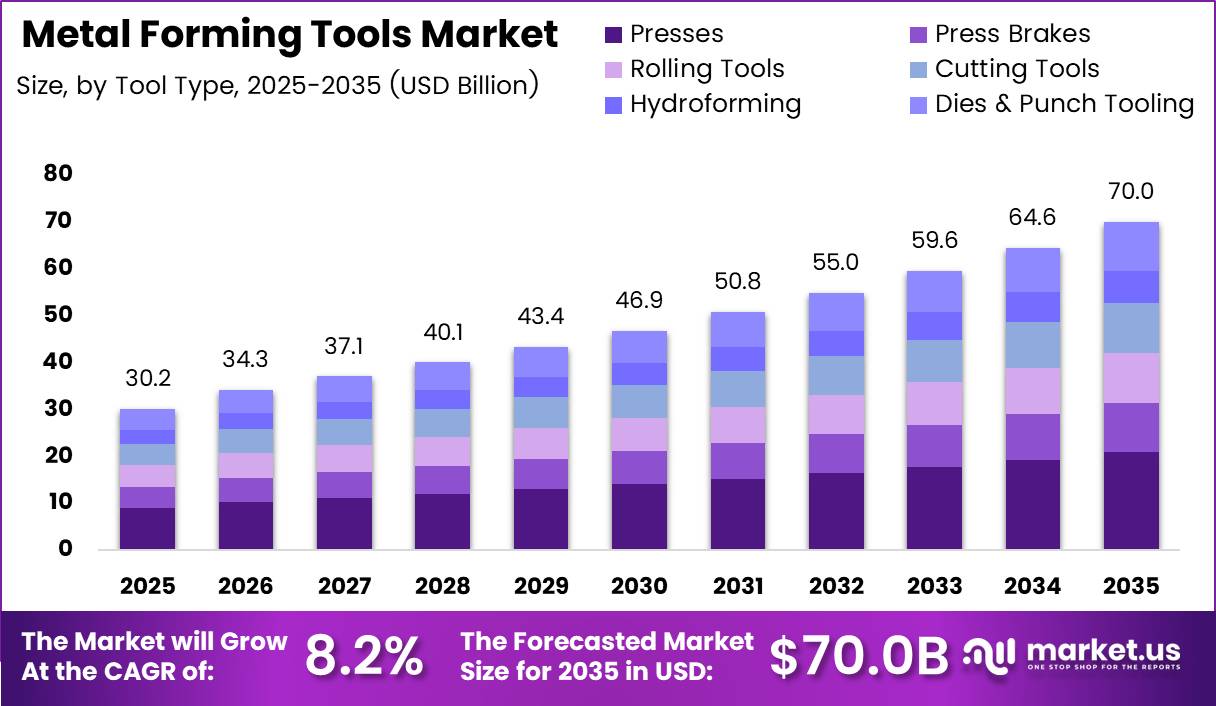

Global Metal Forming Tools Market size is expected to be worth around USD 70.0 Billion by 2035 from USD 30.2 Billion in 2025, growing at a CAGR of 8.2% during the forecast period 2026 to 2035.

The metal forming tools market covers equipment and tooling used to shape, cut, bend, stamp, forge, roll, and extrude metal into finished or semi-finished components. Buyers include automotive assemblers, aerospace manufacturers, industrial machinery producers, construction suppliers, and energy equipment fabricators. The market spans both consumable tooling and capital equipment categories.

The market structure organizes across four primary dimensions: tool type, forming process, automation level, and end-use industry. Presses lead by tool type, stamping leads by process, semi-automatic CNC systems lead by automation level, and automotive leads by end-use application. This multi-layer structure means vendors must align product lines with specific process and buyer combinations to compete effectively.

Government infrastructure spending programs in North America, Europe, and Asia Pacific directly expand demand for structural metal components. Defense modernization budgets, electric vehicle manufacturing incentives, and renewable energy construction programs all require increased output of precision-formed metal parts. Vendors whose tooling portfolios align with these policy-driven investment areas capture procurement priority over general-purpose suppliers.

Regulatory frameworks governing vehicle emissions and fuel efficiency are accelerating the shift toward lightweight metal components across transportation manufacturing. Automakers must replace heavier steel assemblies with high-strength aluminum and advanced alloy stampings to meet fleet emissions targets. This materials transition forces tooling upgrades across stamping, forging, and hydroforming process lines throughout global supply chains.

Industry data shows that CNC hydraulic press brakes used in metal forming carry 2025 ex-factory prices ranging from USD 16,500 to USD 35,000 for 40 to 125-ton machines, from USD 26,800 to USD 51,500 for 160 to 300-ton machines, and from USD 45,300 to USD 95,000 for 400 to 600-ton machines. This wide procurement range confirms that the market serves buyers from precision job shops through to heavy industrial press facilities, each with distinct investment thresholds and financing requirements.

Based on data from industry sources, servo presses can increase available working energy by approximately 3 times while reducing energy consumption by 30 to 50% relative to conventional presses through regenerative control systems. This performance combination creates a measurable financial return on investment for high-volume manufacturers, where both output capacity and energy costs directly affect per-unit production economics.

Key Takeaways

- The global metal forming tools market was valued at USD 30.2 Billion in 2025 and is forecast to reach USD 70.0 Billion by 2035.

- The market is growing at a CAGR of 8.2% during the forecast period 2026 to 2035.

- By Tool Type, the Presses segment dominates with a 24.3% share in 2025.

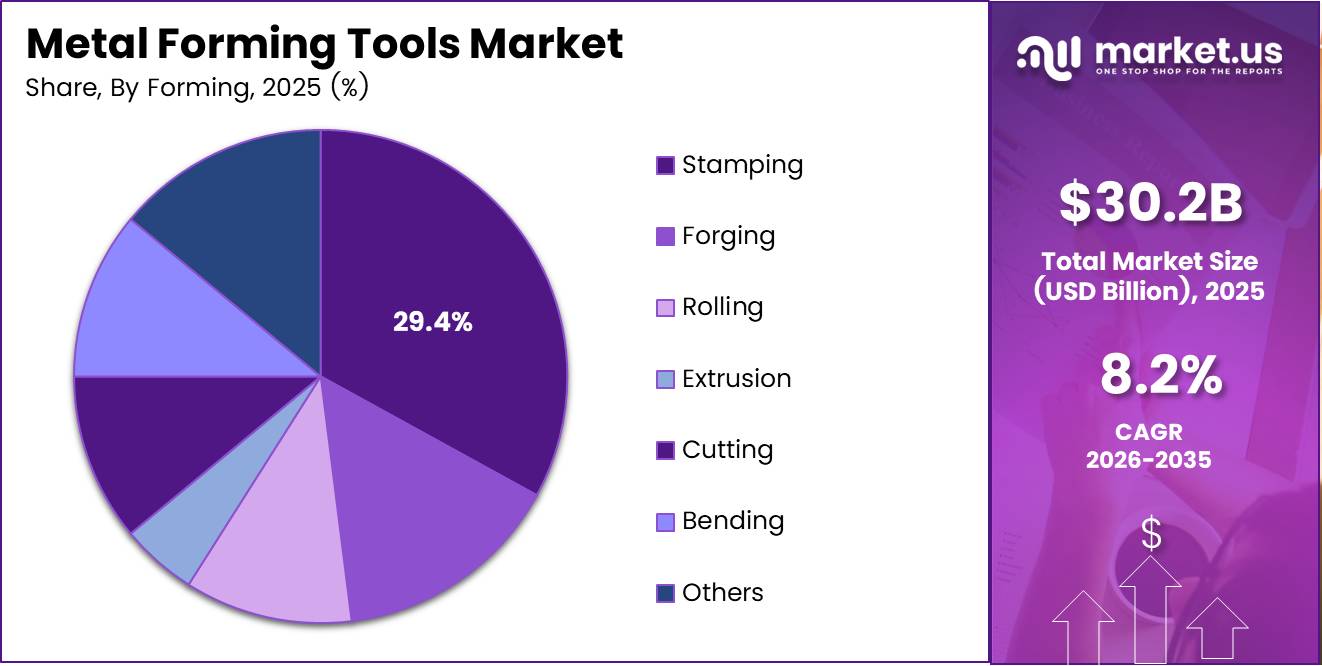

- By Forming Process, the Stamping (Cold & Hot) segment leads with a 29.4% share in 2025.

- By Automation Level, the Semi-Automatic (CNC) segment holds the largest share at 45.8% in 2025.

- By End-use, the Automotive & Transportation segment dominates with a 32.70% share in 2025.

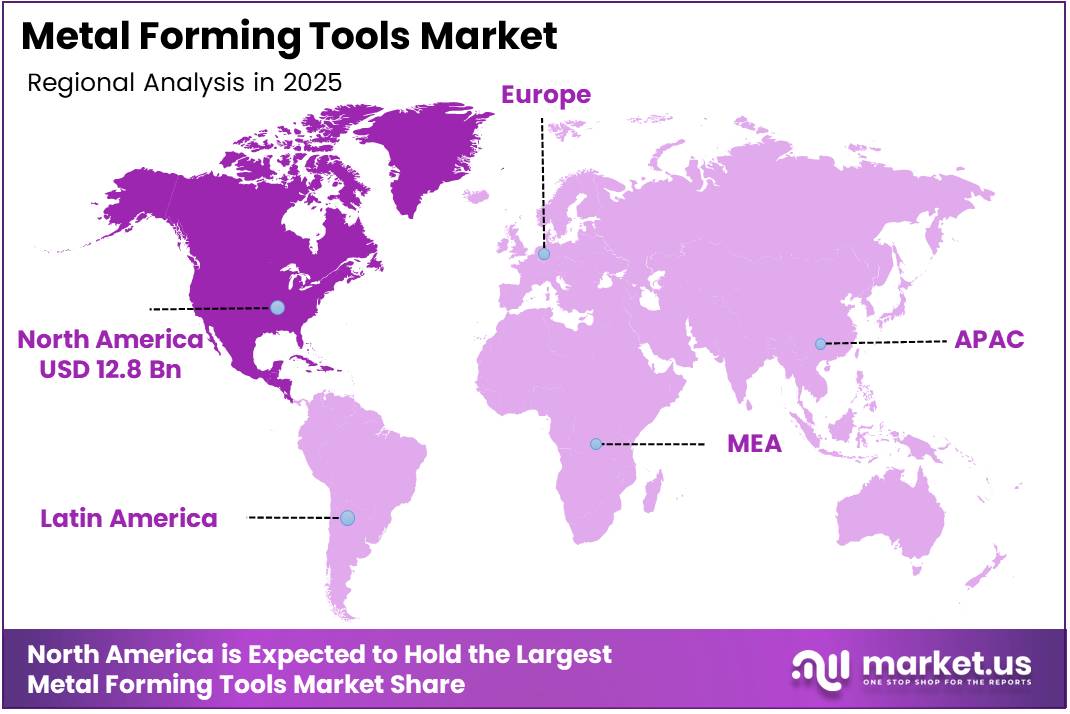

- North America is the dominant region, holding a 42.70% market share valued at USD 12.8 Billion in 2025.

Tool Type Analysis

Presses dominate with 24.3% due to universal application across stamping, forging, and forming.

In 2025, Presses held a dominant market position in the By Tool Type segment of the Metal Forming Tools Market, with a 24.3% share. Industry data shows that mechanical stamping presses deliver pressing speeds between 20 and 1,500 strokes per minute and pressing capacities between 20 and 6,000 tons, covering the widest operational envelope of any single tool category. This breadth makes presses the foundational capital investment across virtually every metal forming facility.

Press Brakes serve the sheet metal bending segment, where precision and repeatability govern part quality. A 2025 specification for a small CNC press brake confirms beam movement speeds of up to 200 mm per second during rapid approach and return phases. Buyers in job shops and fabrication facilities rely on press brakes for low-to-medium volume custom work, creating a stable base of replacement and upgrade demand separate from high-volume stamping press procurement cycles.

Rolling Tools handle continuous forming operations for structural sections, flat sheet, and coiled strip products. Roll-forming lines process sheet thicknesses from 0.3 mm to 12 mm at widths up to 1,400 mm, defining the standard operating envelope for mid-range metal forming lines. Construction and automotive body-in-white producers both rely on rolling tool systems for consistent cross-sectional profiles at high production volumes.

Forming Process Analysis

Stamping (Cold & Hot) dominates with 29.4% due to high-volume automotive parts production.

In 2025, Stamping (Cold & Hot) held a dominant market position in the By Forming Process segment of the Metal Forming Tools Market, with a 29.4% share. High-speed stamping presses operate at speeds ranging from 200 to over 1,500 strokes per minute, enabling the mass production economics that automotive and appliance manufacturers require. This throughput advantage makes stamping the default process selection for any component produced in volumes where per-unit tooling cost must be minimized.

Forging (Hot/Warm/Cold) produces components with superior grain structure and mechanical strength compared with cast or machined alternatives. Aerospace, heavy-vehicle drivetrain, and energy equipment manufacturers specify forged components where fatigue resistance and load-bearing performance are non-negotiable design requirements. Tool wear rates in forging operations are higher than in stamping, generating consistent replacement tooling demand independent of new equipment procurement.

Rolling (Flat/Section) serves structural steel, aluminum strip, and specialty alloy producers who require precise thickness control over continuous output volumes. The process operates with lower tooling cost per ton of output than stamping or forging, but requires large capital investment in roll mill infrastructure. Rolling process tooling demand tracks closely with construction activity and automotive body panel production volumes in each region.

Extrusion (Direct/Indirect/Hydrostatic) shapes metal by forcing billets through precision dies to produce consistent cross-sectional profiles used in aerospace frames, automotive heat exchangers, and architectural systems. Die quality directly determines surface finish and dimensional accuracy of extruded products. Buyers in aluminum and copper extrusion operations replace dies on defined production-cycle schedules, creating predictable tooling procurement patterns for suppliers.

Automation Level Analysis

Semi-Automatic (CNC) dominates with 45.8% due to balance of precision and operational flexibility.

In 2025, Semi-Automatic (CNC) held a dominant market position in the By Automation Level segment of the Metal Forming Tools Market, with a 45.8% share. CNC-controlled forming systems deliver programmable precision across variable job runs without requiring the full integration investment of robotic or lights-out configurations. This flexibility makes CNC the preferred automation tier for contract manufacturers and mid-volume producers who process diverse part geometries across shifting customer order books.

Manual forming operations remain active in low-volume custom fabrication, toolroom prototyping, and markets where capital costs constrain automation investment. These buyers represent a price-sensitive segment for basic tooling and die consumables. However, the manual segment faces ongoing displacement as CNC system prices fall and operator labor costs rise across manufacturing economies.

Fully Automatic (Robotic) forming lines integrate press equipment with robotic material handling, in-line inspection, and automated part transfer to achieve high throughput at minimal labor cost. Automotive stamping plants and high-volume appliance manufacturers lead adoption of this configuration. The capital threshold for full robotic integration limits this segment to large-volume facilities with sufficient production commitment to justify multi-year payback periods.

End-use Analysis

Automotive & Transportation dominates with 32.70% due to mass-production stamping and forging volumes.

In 2025, Automotive & Transportation held a dominant market position in the By End-use segment of the Metal Forming Tools Market, with a 32.70% share. Vehicle production volumes require continuous tooling investment across body stamping, structural forging, drivetrain machining, and exhaust forming operations. Each model-year change triggers new die and tooling procurement cycles, creating recurring capital investment that sustains tooling demand regardless of broader equipment replacement activity.

Aerospace and Defense buyers specify tooling to tighter dimensional tolerances and material traceability requirements than any other end-use segment. Titanium, nickel superalloy, and carbon-fiber reinforced metal matrix forming operations demand specialized tooling with extended development lead times and higher material costs. This complexity creates a premium market segment where tooling suppliers with aerospace certification status command superior pricing power.

Industrial Machinery and Capital Goods manufacturers consume forming tools across fabrication of equipment frames, hydraulic cylinders, gearboxes, and structural weldments. This segment purchases across a wide range of tool types without the volume concentration of automotive, producing stable but fragmented demand that favors broad-catalog tooling distributors over single-process specialists.

Electrical and Electronics manufacturers use precision stamping tools to produce connector terminals, motor laminations, and enclosure components in high volumes with tight dimensional tolerances. This segment’s demand for miniaturized progressive die tooling grows as electronics devices shrink and connector pin counts increase. Tooling suppliers who develop expertise in fine-blanking and micro-stamping operations for this segment access higher-margin work than commodity sheet metal fabrication.

Medical Devices represent a high-value, low-volume segment where surgical instrument manufacturing, implant component forming, and diagnostic equipment enclosure fabrication demand tooling with stringent cleanliness, traceability, and dimensional accuracy requirements. Tooling margins in medical forming applications typically exceed those in automotive or industrial segments, making this a strategically important niche for precision tooling specialists.

Key Market Segments

By Tool Type

- Presses

- Mechanical Press

- Hydraulic Press

- Servo-Electric Press

- Screw/Knuckle Press

- Press Brakes

- Rolling Tools

- Cutting Tools

- Hydroforming Equipment

- Dies & Punch Tooling

- Stamping Dies

- Forging Dies

- Extrusion Dies

- Roll-Forming Tooling

By Forming Process

- Stamping (Cold & Hot)

- Forging (Hot/Warm/Cold)

- Rolling (Flat/Section)

- Extrusion (Direct/Indirect/Hydrostatic)

- Cutting

- Bending

- Others

By Automation Level

- Manual

- Semi-Automatic (CNC)

- Fully Automatic (Robotic)

- Lights-Out / Smart Factory

By End-use

- Automotive & Transportation

- Aerospace & Defense

- Industrial Machinery & Capital Goods

- Building & Construction

- Electrical & Electronics

- Energy (Renewables / Oil & Gas)

- Medical Devices

- Others

Market Dynamics

Drivers - High-Speed Production Capabilities and Lightweight Material Demand Drive Tooling Investments

Mechanical stamping presses provide pressing speeds between 20 and 1,500 strokes per minute and pressing capacities between 20 and 6,000 tons, according to published press machine specifications. This performance range covers the full spectrum from small precision parts to heavy structural forgings. Manufacturers who operate across this range require tooling suppliers that can service both ends of the capacity spectrum, concentrating purchasing toward broad-catalog vendors.

Rising demand for lightweight metal components across transportation industries is the primary structural driver behind stamping and hydroforming tool investment. Automakers replacing conventional steel assemblies with high-strength aluminum and advanced alloys require new die sets, tooling geometries, and press force configurations. Each materials transition at a vehicle platform level triggers tooling investment that recurs at every model change across the automotive supply chain.

In September 2025, TRUMPF launched the next-generation TruBend 3000 bending machine series, featuring up to 40% lower throughput time, automated angle measurement, and reduced energy consumption. This launch demonstrates that leading press and bending equipment vendors are targeting total cost of ownership as the primary differentiator. Buyers who adopt these platforms reduce both cycle time costs and energy expenditure simultaneously, compressing payback periods for capital investment decisions.

Restraints - High Equipment Costs and Tool Wear Challenges Constrain Market Expansion

For CNC hydraulic press brakes, 2025 ex-factory prices range from USD 16,500 to USD 35,000 for 40 to 125-ton machines and from USD 45,300 to USD 95,000 for 400 to 600-ton machines. These price points represent multi-year capital commitments for small and mid-sized fabricators. Buyers operating on thin margins or variable order books delay equipment upgrades, slowing the pace of fleet modernization across the contract fabrication tier of the market.

Frequent tool wear challenges associated with processing advanced metal alloys increase total tooling cost beyond the initial capital expenditure. High-strength steels, titanium alloys, and nickel superalloys accelerate die wear rates and require more frequent regrinding or replacement than conventional mild steel processing. Tooling operations that cannot quantify or predict wear rates face unplanned production stoppages that erode the throughput gains that justified the original equipment investment.

Data from research sources shows that a novel electric-hydraulic hybrid power unit for metal forming presses reduces total energy consumption by 30% compared with high-efficiency pump-controlled technology. However, energy-saving technologies in modern power presses can reduce consumption by up to 60% versus traditional configurations. The gap between best-in-class and standard-practice systems represents stranded cost for buyers locked into older equipment, creating a financial argument for upgrade that is real but requires capital access to act upon.

Growth Factors - Energy-Efficient Automation and High-Throughput Forming Technologies Accelerate Market Growth

Sheet metal forming and roll-forming lines described in 2026 sources can operate at working speeds up to 120 meters per minute, handling strip widths up to 2,000 mm and coil weights up to 25 tons. This throughput capacity makes roll-forming lines commercially viable for continuous production of roofing, cladding, and automotive body panels at volumes that justify the capital investment. Vendors who supply roll tooling for these lines access a recurring replacement demand stream tied to production volume rather than equipment replacement cycles.

Switching a hydraulic forming press to servo-hydraulic technology saves more than 50% of energy per cycle measured in kilowatt-hours, according to published engineering data. As energy costs rise across major manufacturing regions, this saving converts into a quantifiable annual operating cost reduction that improves the investment case for equipment upgrades. Tooling vendors who package servo-hydraulic compatibility into their die and tooling systems gain purchasing preference over suppliers whose tooling requires legacy hydraulic press configurations.

In September 2025, TRUMPF launched the Material Flow Starter Kit in North America, introducing mobile-robot-based automation for transporting materials between metal-forming and sheet-metal processing stations. This product addresses the material handling gap that limits throughput in partially automated facilities. Buyers who adopt this system gain a scalable automation entry point that does not require full production line redesign, lowering the capital barrier to productivity improvement across the contract fabrication segment.

Emerging Trends - Servo-Driven Precision Systems and Simulation-Based Tool Design Reshape Metal Forming Operations

Modern high-speed metal stamping presses with servo-driven systems can reach up to 1,400 strokes per minute for small, high-volume production, according to 2025 press machine specifications. This speed positions servo-driven presses as the performance benchmark for connector, terminal, and precision component manufacturers. Early movers who specify servo-driven equipment in new production lines establish a throughput advantage over competitors still operating conventional flywheel-driven press configurations.

Adoption of simulation-driven tool design is shortening die development lead times and reducing first-article rejection rates across stamping and forging operations. Virtual forming simulation allows engineers to identify material thinning, springback, and die wear patterns before cutting steel on physical tooling. Vendors who embed simulation-based design validation into their tooling development process reduce customer-facing lead times and warranty claim rates, both of which are competitive differentiators in high-volume automotive die sourcing.

A 2025 specification confirms that small CNC press brakes achieve bending accuracy of approximately ±0.1 mm, a precision level that satisfies demanding aerospace and electronics fabrication tolerances. As buyers in these sectors specify tighter dimensional requirements on formed components, this accuracy benchmark becomes a minimum qualifying criterion rather than a premium feature. Tooling and equipment suppliers who cannot demonstrate this accuracy level lose access to the aerospace and electronics segments, which carry the highest per-unit tooling margins.

Regional Analysis

North America Dominates the Metal Forming Tools Market with a Market Share of 42.70%, Valued at USD 12.8 Billion

North America holds the leading regional position in the metal forming tools market, driven by the United States’ concentration of automotive stamping plants, aerospace component manufacturers, and defense production facilities. Federal investment in domestic semiconductor fabrication, electric vehicle manufacturing incentives, and infrastructure programs sustains capital expenditure across forming tool end-use sectors. Buyers in this region prioritize tooling suppliers who can deliver both high-precision capability and rapid technical service response.

Europe represents a technologically advanced market anchored by German and Italian press and forming equipment manufacturers who also supply tooling domestically and globally. Regulatory pressure on vehicle emissions accelerates the transition to high-strength steel and aluminum forming across European automotive supply chains. This materials shift requires continuous tooling investment at Tier 1 and Tier 2 automotive suppliers, sustaining replacement and development tooling demand throughout the forecast period.

Asia Pacific combines the world’s largest automotive production volumes in China with rapidly expanding aerospace manufacturing in India and South Korea. China’s domestic press and tooling industry supplies significant portions of regional demand, but quality and precision requirements in aerospace and EV battery enclosure forming are driving imports of European and Japanese premium tooling. This dual-tier market structure creates distinct opportunities for both cost-competitive and precision-premium tooling suppliers.

Latin America shows concentrated metal forming tool demand in Brazil and Mexico, where automotive assembly operations and industrial machinery manufacturing anchor the market. Mexico’s proximity to US automotive supply chains creates sustained tooling demand for stamping and bending operations serving cross-border production programs. Currency volatility in Brazil creates procurement timing sensitivity that favors suppliers offering local inventory and flexible payment structures over those requiring full upfront foreign currency payment.

Middle East and Africa present a developing market base where oil and gas fabrication in GCC countries and mining equipment manufacturing in South Africa generate specialized tooling requirements. Large-scale infrastructure and industrial diversification programs in Saudi Arabia and the UAE are expanding domestic metal fabrication capacity. As local value-added manufacturing policies push structural metal component production into the region, demand for forming tooling will build from a concentration in heavy-industry applications toward broader fabrication coverage.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

NiPro Optics is listed in the provided data as a key player in this market. However, based on available information, NiPro Optics is a precision optical components manufacturer specializing in diamond-turned optics and thin-film coatings. No verified data connects NiPro Optics to metal forming tools. This entry requires human review and verification before publication.

Carl Zeiss AG appears in the provided key players list for this market. Carl Zeiss AG is a global optical and optoelectronics manufacturer whose industrial metrology division produces precision measurement systems used in quality control for metal forming operations. If this is the basis for inclusion, Zeiss occupies a metrology and inspection role adjacent to the forming tools market rather than a direct tooling supply position.

Andover Corporation is listed among the key players in the provided data. Andover Corporation is a manufacturer of precision optical filters and thin-film coated components. No verified data directly positions Andover Corporation as a metal forming tools supplier. This entry requires human review and data verification before inclusion in a published report.

EssilorLuxottica is listed in the provided data as a key market participant. EssilorLuxottica is a global ophthalmic lens and eyewear manufacturer. No verified data connects EssilorLuxottica to metal forming tools manufacturing or supply. This entry requires human review and verification. The key players list as provided appears to reflect data from a different market and should be corrected before this report is published.

Key Players

- NiPro Optics

- Carl Zeiss AG

- Andover Corporation

- EssilorLuxottica

- Honeywell International Inc

- PPG Industries, Inc.

- DuPont

- Nippon Sheet Glass Co., Ltd

- Merck KGaA

- HOYA

- Applied Materials, Inc.

Recent Developments

- January 2025 – Wilson Tool International acquired PASS Stanztechnik AG, expanding its punch tooling portfolio and strengthening its presence in the European sheet-metal forming market.

- March 2025 – Schuler was rebranded as ANDRITZ Schuler, further integrating forming technology, press systems, and automation solutions within the ANDRITZ Group.

- October 2025 – TRUMPF unveiled a fully automated production system combining the next-generation TruBend Center 7030, TruMatic 5000, and STOPA storage technology, enabling integrated punching, laser cutting, and bending operations in a single connected platform.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 30.2 Billion |

| Forecast Revenue (2035) | USD 70.0 Billion |

| CAGR (2026-2035) | 8.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Tool Type (Presses: Mechanical Press, Hydraulic Press, Servo-Electric Press, Screw/Knuckle Press; Press Brakes; Rolling Tools; Cutting Tools; Hydroforming Equipment; Dies & Punch Tooling: Stamping Dies, Forging Dies, Extrusion Dies, Roll-Forming Tooling); By Forming Process (Stamping Cold & Hot, Forging Hot/Warm/Cold, Rolling Flat/Section, Extrusion Direct/Indirect/Hydrostatic, Cutting, Bending, Others); By Automation Level (Manual, Semi-Automatic CNC, Fully Automatic Robotic, Lights-Out Smart Factory); By End-use (Automotive & Transportation, Aerospace & Defense, Industrial Machinery & Capital Goods, Building & Construction, Electrical & Electronics, Energy Renewables/Oil & Gas, Medical Devices, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | NiPro Optics, Carl Zeiss AG, Andover Corporation, EssilorLuxottica, Honeywell International Inc, PPG Industries Inc, DuPont, Nippon Sheet Glass Co. Ltd, Merck KGaA, HOYA, Applied Materials Inc |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |