Quick Navigation

Report Overview

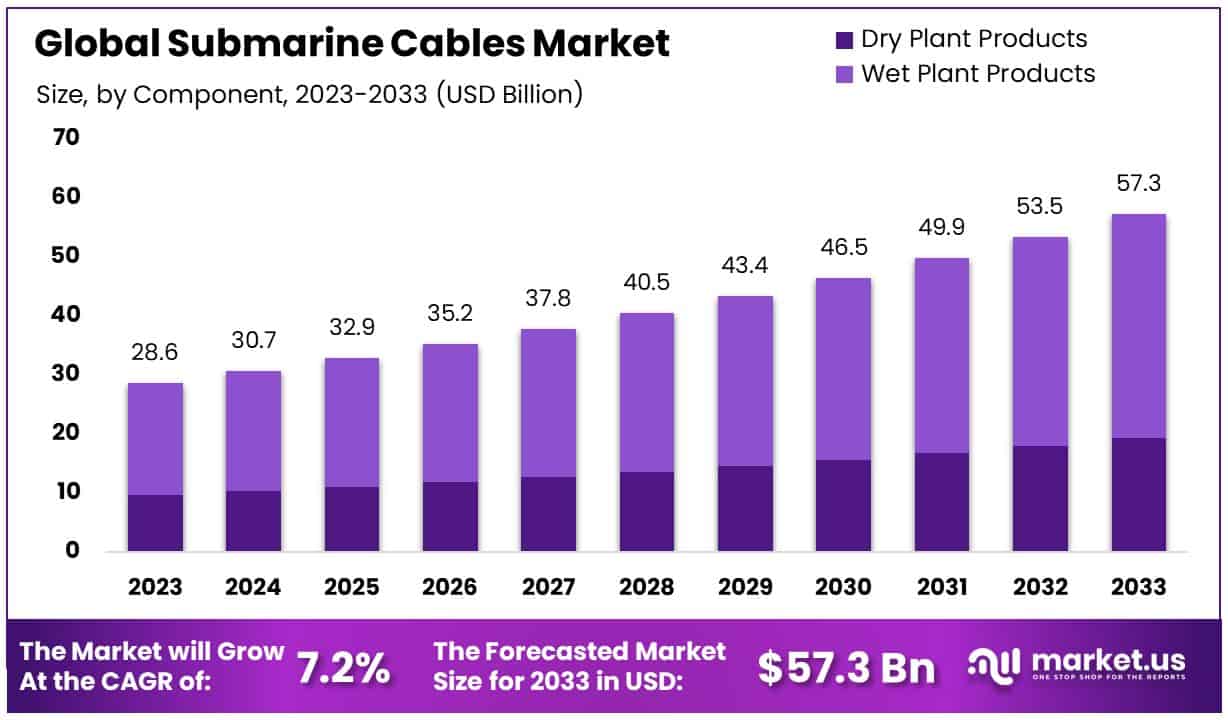

The Global Submarine Cables Market size is expected to be worth around USD 57.3 Billion by 2033, from USD 28.6 Billion in 2023, growing at a CAGR of 7.20% during the forecast period from 2024 to 2033.

The Submarine Cables Market refers to the global industry focused on the manufacturing, deployment, and maintenance of undersea cables. These cables are crucial for international communication and data transfer, connecting continents and countries beneath oceans.

Key players include telecom giants, specialized marine companies, and governments investing in digital infrastructure. With the exponential growth of digital data, cloud computing, and internet usage, the demand for submarine cables is surging, making this market a strategic focus for stakeholders aiming to enhance global connectivity and data transmission capabilities.

In the rapidly evolving landscape of global connectivity, the Submarine Cables Market stands as a cornerstone, underpinning the vast network of international communication and data exchange.

With over 550 submarine cable systems recorded as of June 2023, including 485 active systems and an additional 70 in the pipeline, the market is poised for substantial growth. This infrastructure is critical for facilitating the ever-increasing demand for high-speed internet access and the seamless transfer of vast amounts of data across continents.

The market’s expansion is intricately linked to the digital transformation sweeping across industries worldwide. The burgeoning need for robust internet connectivity, driven by the rise of cloud computing, the digital economy, and the proliferation of data centers, underscores the strategic importance of submarine cables. Moreover, the advent of offshore energy projects has expanded the scope of these cables, extending their utility to power transmission alongside data communication.

Technological advancements in the field have further catalyzed market growth, enhancing the efficiency, capacity, and reliability of submarine cable systems. These innovations not only support the increasing load of global internet traffic but also ensure the market’s resilience against physical and cyber threats.

The Submarine Cables Market is expected to witness sustained growth, fueled by the continuous digitalization of economies, the expansion of online services, and the global push towards connecting underserved regions. As a vital infrastructure component, submarine cables will continue to play a pivotal role in shaping the future of global connectivity, making it a key area of interest for investors and policymakers alike.

Key Takeaways

- Market Value Projection: The Global Submarine Cables Market is anticipated to reach USD 57.3 Billion by 2033, experiencing substantial growth from USD 28.6 Billion in 2023, with a CAGR of 7.20% during the forecast period from 2024 to 2033.

- Major Segments:

- By Component: Dry plant products hold a significant market share of 72.4%, encompassing terrestrial components essential for managing and operating submarine cable systems.

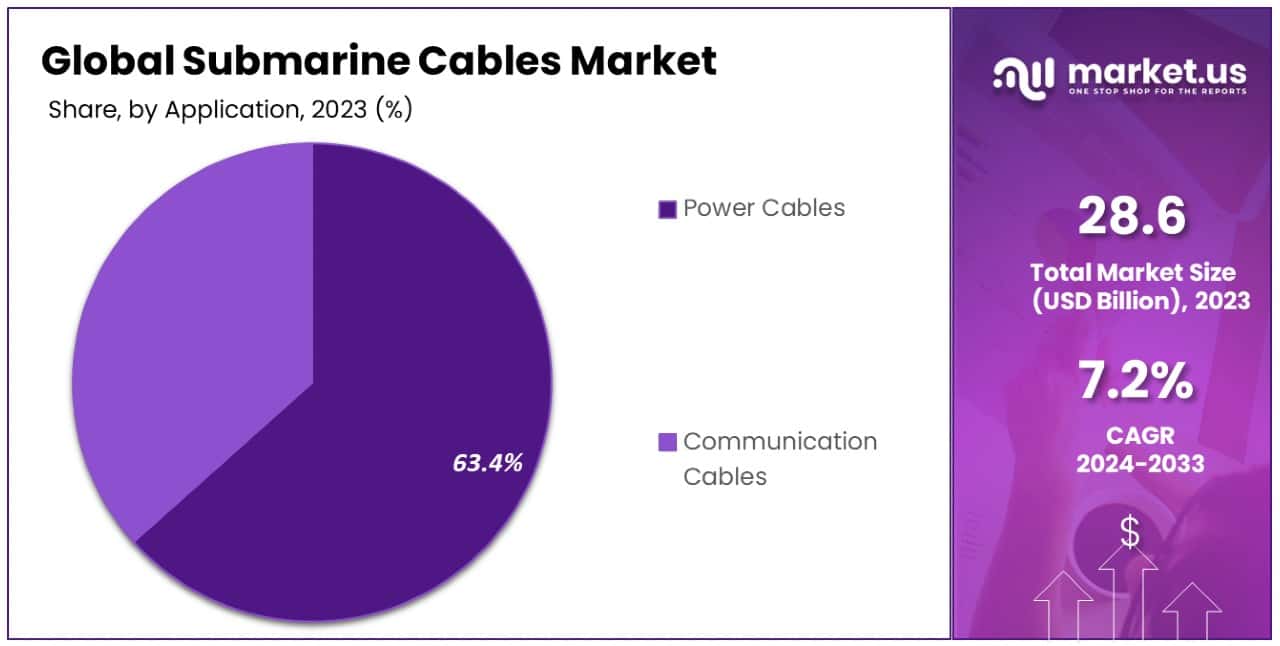

- By Application: Power cables lead the market with a 63.4% share, driven by the global transition towards renewable energy sources and the integration of offshore energy projects into mainstream energy supply.

- By Voltage: High voltage cables lead with a substantial share of 64.1%, supporting the transmission of large amounts of electricity over long distances with minimal loss, particularly in connecting offshore wind farms and facilitating inter-country power exchanges.

- By End-User: Offshore wind power generation emerges as the dominant sector, claiming 45.6% of the market, driven by the global shift towards sustainable energy sources and increasing investments in offshore wind farms.

- By Offering: Installation and commissioning hold the largest market share at 40.6%, reflecting the critical phase of laying down new submarine cable systems and integrating them into existing networks.

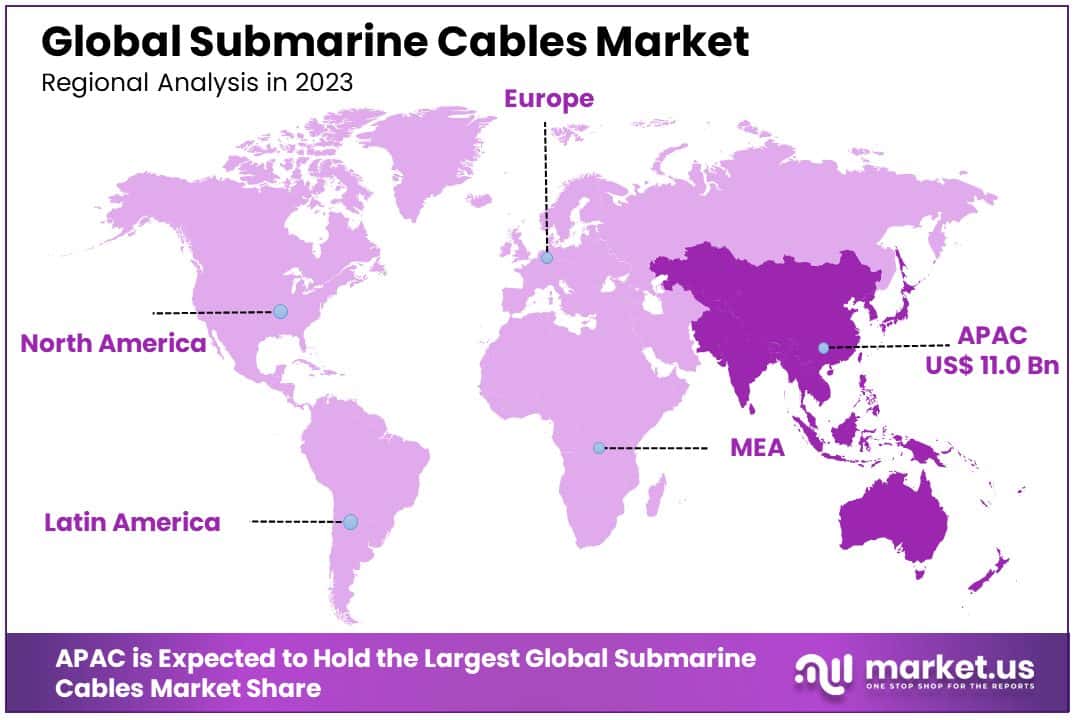

- Regional Dynamics: Asia Pacific dominates the market with a 38.5% market share, driven by increasing investments in submarine cable projects to meet the region’s growing connectivity needs.

- Analyst Viewpoint: Analysts foresee significant growth opportunities in the Submarine Cables Market, driven by the increasing demand for global connectivity, renewable energy sources, and digital transformation initiatives. Investments in infrastructure projects, upgrades, and maintenance are expected to drive market expansion further.

- Growth Opportunities: Opportunities lie in expanding submarine cable projects to meet growing connectivity demands, enhancing cable technology for improved efficiency and performance, investing in renewable energy projects to support offshore wind power generation, and providing comprehensive solutions for installation, commissioning, upgrades, and maintenance of submarine cable systems.

Driving Factors

Increasing Demand for Global Internet Connectivity Drives Market Growth

The relentless expansion of internet users and the universal shift towards digitalization have significantly propelled the need for high-speed internet and data services across the globe. This surge in demand directly correlates with the growth of the Submarine Cables Market, as these cables are foundational to enabling global communication networks.

They are pivotal in bridging continents and oceans, facilitating the seamless flow of information and data. With over 550 submarine cable systems either in operation or planned as of June 2023, the market is rapidly expanding to accommodate this demand, reflecting the critical role submarine cables play in supporting global connectivity and the digital economy.

Offshore Energy Projects Amplify Demand for Submarine Power Cables

The growth of offshore energy projects, including oil and gas exploration, and the burgeoning sector of offshore wind farms, has markedly increased the demand for submarine power cables. These cables are essential for transmitting electricity from remote offshore energy sources back to the mainland grid.

For instance, the NordLink cable, a 623 km HVDC link, exemplifies this trend by connecting the Norwegian and German power grids, showcasing how submarine cables are pivotal in integrating renewable energy sources and enhancing energy security between nations. This aspect of the market not only contributes to the expansion of submarine cable networks but also underscores the diversification of their applications beyond telecommunications, into energy transmission and sustainability efforts.

Technological Innovations Propel Market Forward

Continuous technological advancements in submarine cable systems, characterized by improved data transmission rates, enhanced bandwidth capacity, and superior durability, have significantly bolstered market growth. These innovations enable more efficient, reliable, and scalable cable systems, capable of meeting the escalating demands for internet connectivity and data services, particularly in regions with burgeoning cloud computing and data center needs.

For example, the PLCN (Pacific Light Cable Network), stretching 12,800 km and connecting the United States with Taiwan and the Philippines, underscores the impact of technological progress on the market. It facilitates high-speed internet connectivity and meets the increasing demands of the Asia-Pacific region, illustrating the dynamic interplay between technological innovation and market expansion.

Restraining Factors

Geopolitical and Regulatory Challenges Restrain Market Growth

The process of installing and operating submarine cables is often hampered by the complex geopolitical and regulatory landscapes across different jurisdictions. Securing the necessary permits and approvals involves navigating through a maze of international, regional, and local regulations, which can vary widely from one jurisdiction to another.

This complexity not only leads to significant delays in project timelines but also escalates the operational costs. The involvement of multiple countries adds layers of diplomatic negotiations, making it a time-consuming process that can hinder the swift expansion of the Submarine Cables Market. These bureaucratic hurdles act as a substantial barrier to the market’s growth, affecting the deployment of new cable systems and the upgrade of existing infrastructures.

Environmental and Natural Risks Challenge Market Expansion

Submarine cables are continually at risk from environmental and natural hazards, including seabed disturbances, marine activities, and catastrophic events like earthquakes and tsunamis. Such risks pose significant challenges to the integrity and reliability of these critical infrastructures.

For instance, the Asia-America Gateway (AAG) cable, stretching 20,000 km between Southeast Asia and the United States, has suffered multiple disruptions due to natural disasters, including the devastating 2011 Tohoku earthquake and tsunami. These incidents not only cause immediate service disruptions but also entail hefty repair costs and operational downtime, severely impacting the market.

Component Analysis

In the Submarine Cables Market, components are categorized into dry plant products and wet plant products. Dry plant products, holding a significant market share of 72.4%, emerge as the dominant sub-segment. This category includes the terrestrial components of the submarine cable systems, such as landing stations, power feed equipment, and network operations centers.

These elements are essential for the management and operation of submarine cables, converting electrical signals for power transmission or data communication from undersea to terrestrial networks.

The predominance of dry plant products is driven by the escalating demand for high-capacity and reliable communication infrastructure. As the volume of global data transfer increases, propelled by digitalization across sectors, the need for advanced dry plant technology has surged. These products ensure the efficient processing and distribution of data, maintaining the integrity of transmissions across vast distances.

Moreover, the advancement in technology within this segment, including innovations in signal processing and energy efficiency, has enhanced the performance of submarine cable systems. This, in turn, supports the ever-growing requirements for faster and more reliable global communication networks.

On the other side, wet plant products, which comprise the actual submarine cables and repeaters placed on the ocean floor, play a critical yet supportive role in the market’s growth. Despite their lower share, these components are vital for the physical transmission of data and power across continents and islands. Continuous improvements in cable design, materials, and laying techniques contribute to the efficiency and durability of submarine cables, ensuring their capacity to meet future demands.

Application Analysis

Within the application segment of the Submarine Cables Market, power cables and communication cables represent the two primary categories. Power cables lead the market with a 63.4% share, underscoring their importance in contemporary energy transmission and infrastructure projects. This dominance is attributed to the global transition towards renewable energy sources and the integration of offshore energy projects, such as wind farms and intercontinental power grids, into the mainstream energy supply.

Power cables are engineered to transmit electricity from offshore renewable energy sources back to the mainland or between countries, playing a pivotal role in enhancing energy security and enabling the transition to a more sustainable energy mix. The rise in offshore wind power generation and the push for cleaner energy solutions have significantly increased the demand for high-voltage submarine power cables.

The focus on sustainable and renewable energy sources, coupled with advancements in cable technology, has propelled the power cables segment to the forefront of the market. This shift reflects broader trends in global energy consumption and the urgent need for infrastructure capable of supporting renewable energy distribution on a large scale.

Conversely, the communication cables segment, although not the dominant sub-segment, remains crucial for global connectivity and the digital economy. This segment caters to the exponential growth in internet usage, cloud computing, and the need for robust, high-speed communication links between continents. As digital transformation initiatives continue to accelerate across industries, the demand for submarine communication cables is expected to remain strong, supporting the overall growth of the Submarine Cables Market.

Voltage Analysis

In the voltage segment of the Submarine Cables Market, classifications include medium voltage, high voltage, and extra high voltage. The high voltage segment leads with a substantial share of 64.1%. This dominance is driven by the high voltage cables’ capacity to transmit large amounts of electricity over long distances with minimal loss, making them ideal for connecting offshore wind farms and facilitating inter-country power exchanges.

High voltage submarine cables are instrumental in the global push towards renewable energy, supporting the transmission of clean power from remote offshore sources to densely populated urban centers. Their efficiency and reliability underpin the infrastructural backbone necessary for modern energy networks, reflecting the market’s adaptation to evolving energy demands and environmental considerations.

Meanwhile, medium voltage cables serve important roles in regional and shorter-distance applications, including connections between smaller islands and mainland power grids or for smaller scale offshore energy projects. Extra high voltage cables, though less prevalent, are crucial for ultra-long-distance transmission projects requiring the highest efficiency and power capacity, often used in significant international power supply networks.

End-User Analysis

The end-user segment is diverse, encompassing offshore wind power generation, inter-country & island connection, and offshore oil & gas. Offshore wind power generation emerges as the dominant sector, claiming 45.6% of the market. This segment’s growth is propelled by the global shift towards sustainable energy sources, with offshore wind farms becoming increasingly vital in many countries’ energy strategies.

The deployment of submarine cables in this sector facilitates the efficient transmission of generated power to onshore grids, overcoming geographical challenges and harnessing wind resources available at sea. The focus on reducing carbon footprints and achieving energy independence has significantly boosted investments in offshore wind, consequently driving the demand for high-capacity, reliable submarine power cables.

Inter-country & island connections and offshore oil & gas, while not leading, remain essential for energy security and operational efficiency. These segments rely on submarine cables for power supply and operational connectivity, supporting the energy and data transmission needs of remote facilities and enhancing global energy interconnectivity.

Offering Analysis

The offerings within the Submarine Cables Market are categorized into installation & commissioning, upgrade, and maintenance. Installation and commissioning hold the largest market share at 40.6%, reflecting the critical phase of laying down new submarine cable systems and integrating them into existing networks.

This segment’s prominence is attributed to the growing number of submarine cable projects worldwide, driven by the expanding need for global connectivity and renewable energy sources. The process of installing and commissioning submarine cables is complex, requiring sophisticated technology and expertise to ensure the cables are laid correctly and function optimally from the outset.

Upgrades and maintenance are crucial for the longevity and efficiency of submarine cable systems. Upgrades allow for the enhancement of existing systems to meet current demands for capacity and performance, while maintenance ensures the ongoing reliability and operational integrity of the cables, addressing issues such as repairs and fault management.

Key Market Segments

By Component

- Dry Plant Products

- Wet Plant Products

By Application

- Power Cables

- Communication Cables

By Voltage

- Medium Voltage

- High Voltage

- Extra High Voltage

By End-User

- Offshore Wind Power Generation

- Inter Country & Island Connection

- Offshore Oil & Gas

By Offerings

- Installation & Commissioning

- Upgrade

- Maintenance

Growth Opportunities

Expansion of Internet Connectivity in Underserved Regions Offers Growth Opportunity

The drive to expand internet connectivity into underserved and remote regions marks a considerable opportunity within the Submarine Cables Market. This expansion is not just a technological advancement but a bridge to economic and social development, offering communities access to global markets, education, and healthcare resources.

Initiatives by governments and international bodies to reduce the digital divide are propelling the construction of new submarine cable systems, aiming to connect these isolated areas with high-speed internet. This movement towards inclusivity not only enhances the quality of life for millions but also opens up new territories for market players to deploy infrastructure, thereby driving significant growth in the submarine cables sector.

Development of Offshore Renewable Energy Projects Offers Growth Opportunity

The surge in offshore renewable energy projects, particularly wind and tidal energy generation, presents a burgeoning opportunity for the Submarine Cables Market. As the world shifts towards cleaner energy sources, the need for submarine power cables to transport electricity from offshore generation sites to onshore grids has escalated.

This demand is fueled by the global commitment to reduce carbon emissions and the increasing viability of offshore renewable energy as a substantial power source. The development of these projects necessitates robust, high-capacity submarine cables, fostering new market opportunities for manufacturers and installers specialized in this domain. This sector’s growth is emblematic of the market’s potential to support the green energy transition, highlighting its critical role in enabling sustainable development.

Trending Factors

Adoption of New Cable Technologies Are Trending Factors

The continuous evolution and adoption of new cable technologies, such as space-division multiplexing (SDM) and hollow-core fibers, are significantly trending within the Submarine Cables Market. These innovations promise to revolutionize the industry by offering higher data transmission capacities and improved energy efficiency. SDM, for instance, allows for the transmission of data through multiple spatial channels within a single fiber, dramatically increasing the throughput.

Hollow-core fibers, on the other hand, minimize latency and signal loss, enhancing the efficiency of long-distance communication. The drive towards these advanced technologies is fueled by the increasing global demand for faster, more reliable internet connectivity, positioning them as key factors in the market’s ongoing growth and evolution.

Collaboration and Consortia for Large-Scale Projects Are Trending Factors

The formation of collaborations and consortia among key players, including telecommunications companies, internet service providers, and technology giants, is a notable trend driving the Submarine Cables Market. This approach is particularly prevalent in large-scale, high-cost projects where sharing the financial burden and risk is beneficial.

By pooling resources and expertise, these partnerships can undertake ambitious submarine cable projects that might be too costly or risky for single entities. This trend not only accelerates the deployment of new cables but also fosters innovation through shared knowledge and objectives. The increasing complexity and scale of submarine cable projects make collaboration and consortia formation essential strategies for navigating the market’s challenges and leveraging its opportunities.

Regional Analysis

Asia Pacific Dominates with 38.5% Market Share

The Asia Pacific (APAC) region holds a dominant position in the Submarine Cables Market, accounting for 38.5% of the global share. This leadership stems from several key factors, including the region’s rapid technological advancements, burgeoning internet user base, and significant investments in digital infrastructure.

The dense population centers with escalating demand for high-speed internet and data services drive the proliferation of submarine cable projects. Moreover, APAC’s strategic geographic location as a nexus for transcontinental cables further cements its pivotal role in global communications.

Market dynamics in APAC are influenced by its diverse economic landscapes, ranging from emerging markets to technological powerhouses. This diversity necessitates a broad spectrum of connectivity solutions, from enhancing international bandwidth to bolstering intra-regional links. The region’s commitment to digital transformation and the integration of remote areas into the digital economy also contribute to its high market share.

Regional Market Shares and Dynamics

North America: Holding a significant market share, North America’s focus on enhancing transatlantic connectivity and upgrading existing infrastructure supports its strong position. The region’s advanced technological ecosystem and high demand for cloud services stimulate continuous investments in submarine cables.

Europe: Europe, with its strategic initiatives to connect to both APAC and North America, plays a crucial role in the global network. The region’s emphasis on data protection and secure connectivity further accelerates the deployment of new submarine cables.

Middle East & Africa: This region is witnessing rapid growth due to the increasing need for connectivity and the development of data centers. Investments in submarine cables are seen as key to unlocking economic potential and integrating into the global digital economy.

Latin America: Latin America’s market is expanding as countries focus on improving connectivity and reducing digital divides. The region’s submarine cable projects are vital for connecting with North America and beyond, enhancing both regional and international data exchange.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

In the dynamic landscape of the Submarine Cables Market, the listed companies play pivotal roles, each contributing uniquely to the industry’s evolution and competitiveness. ALE International and ALE USA Inc., alongside SubCom, LLC, and NEC Corporation, are recognized for their technological prowess and expertise in manufacturing and deploying submarine communication cables globally. Prysmian S.p.A and Nexans stand out for their extensive experience in both power and communication cables, underpinning the market’s infrastructure needs with innovative solutions.

Tech giants such as Google LLC, Amazon.com, Inc., and Microsoft have significantly impacted the market by investing in private submarine cable projects, enhancing global connectivity for cloud services and data center operations. This diversification of market participants from traditional telecom and cable manufacturers to include major cloud service providers highlights the shifting dynamics within the industry, emphasizing the growing demand for data transmission and internet services.

NKT A/S and ZTT further contribute to the market by offering specialized cables and services that address the specific needs of offshore and renewable energy projects, showcasing the market’s expansion into new segments. The strategic positioning of these key players, leveraging advanced technologies, strategic collaborations, and direct investments, underscores their substantial influence on market trends, innovation, and growth trajectories.

Market Key Players

- ALE International

- SubCom, LLC

- NEC Corporation

- Prysmian S.p.A

- Nexans

- Google LLC

- Amazon.com, Inc.

- Microsoft

- NKT A/S

- ZTT

Recent Developments

- On March 2024, Tunisia launched a new submarine cable, marking a significant milestone in the country’s connectivity infrastructure.

- On January 2024, Intelia New Zealand announced the launch of the TE WAIPOUNAMU submarine cable project, connecting Invercargill to Sydney and Melbourne.

- On November 2023, Techpoint Digest featured discussions on various topics, including new global crypto developments and YouTube’s entry into streaming TV shows.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 28.6 Billion |

| Forecast Revenue (2033) | USD 57.3 Billion |

| CAGR (2024-2033) | 7.20% |

| Base Year for Estimation | 2023 |

| Historic Period | 2018-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Dry Plant Products, Wet Plant Products), By Application (Power Cables, Communication Cables), By Voltage (Medium Voltage, High Voltage, Extra High Voltage), By End-User (Offshore Wind Power Generation, Inter Country & Island Connection, Offshore Oil & Gas), By Offerings (Installation & Commissioning, Upgrade, Maintenance) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | ALE International, ALE USA Inc., SubCom, LLC, NEC Corporation, Prysmian S.p.A, Nexans, Google LLC, Amazon.com, Inc., Microsoft, NKT A/S, ZTT |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

The Global Submarine Cables Market is projected to be worth around USD 57.3 Billion by 2033, with a notable increase from USD 28.6 Billion in 2023.

The Submarine Cables Market includes industries involved in the manufacturing, deployment, and maintenance of undersea cables, vital for international communication and data transfer across continents.

The market is segmented by component, application, voltage, end-user, and offering, reflecting its diverse utility and applications.

Asia Pacific dominates the market with a significant market share, driven by increasing investments in submarine cable projects to meet the region's growing connectivity needs.