Quick Navigation

Report Overview

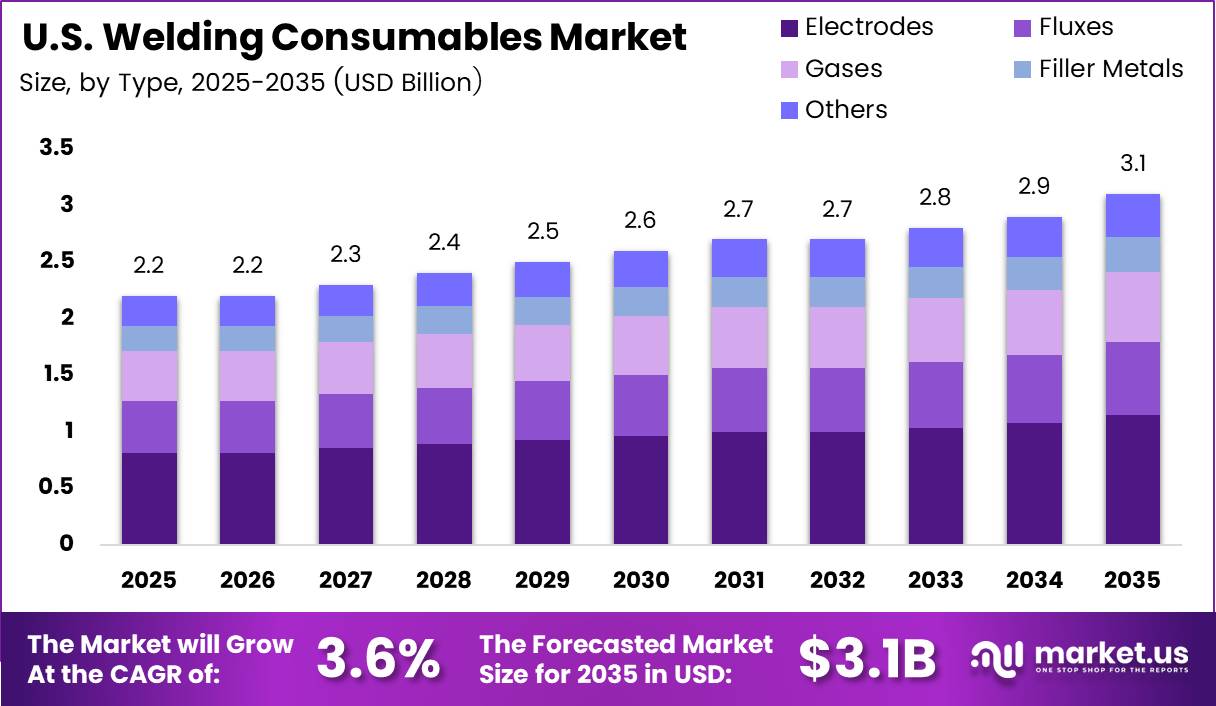

U.S. Welding Consumables Market size is expected to be worth around USD 3.1 Billion by 2035 from USD 2.2 Billion in 2025, growing at a CAGR of 3.6% during the forecast period 2026 to 2035.

The U.S. welding consumables market covers electrodes, filler metals, fluxes, and shielding gases consumed during arc, gas, and resistance welding operations across domestic industrial facilities. These materials are required inputs for every structural and pressure-containing weld joint produced in the country. Their demand ties directly to the volume and complexity of fabrication activity across construction, energy, defense, and manufacturing sectors.

The market structure spans multiple product categories that serve distinct welding processes. Shielded metal arc, gas metal arc, submerged arc, and flux-cored arc welding each require different consumable chemistries and formats. This process diversity creates parallel demand streams within the domestic market that move at different rates depending on sector investment levels and automation adoption in each end-use industry.

Federal and state governments direct capital into infrastructure programs that generate direct welding consumable demand across bridge construction, pipeline installation, utility grid upgrades, and port modernization projects. Buy American provisions embedded in infrastructure legislation require domestically produced materials on qualifying projects. This requirement creates a structural preference for U.S.-produced welding consumables that insulates qualifying vendors from import price competition on federally funded contracts.

Regulatory frameworks from the Occupational Safety and Health Administration and the American Welding Society govern fume exposure limits, weld procedure qualification, and consumable certification requirements across industrial applications. Compliance with these standards restricts substitution of uncertified consumable products on qualified weld procedures. This compliance layer protects average selling prices for certified consumable lines and raises the cost of entry for suppliers attempting to displace incumbent vendors without matching documentation.

According to weldingwire.net data, metal-cored welding wires achieve deposition efficiencies of 92% to 98%, enabling a high percentage of the consumable to become deposited weld metal. This efficiency level directly lowers material cost per completed joint. Fabricators who switch to metal-cored formats on high-volume weld stations recover the premium product cost through waste reduction, making the upgrade financially self-justifying across most production volume thresholds.

Data from weldingwire.net shows flux-cored and metal-cored wires using 1.2 mm diameter achieve deposition rates of 5.4 to 6.4 kg per hour in production welding. This throughput substantially exceeds solid wire outputs at equivalent diameters. U.S. fabricators facing rising labor costs gain a compounding cost advantage by adopting advanced wire formats, as the productivity gap between wire types amplifies per-hour labor savings across every production shift.

Key Takeaways

- The U.S. Welding Consumables Market was valued at USD 2.2 Billion in 2025 and is forecast to reach USD 3.1 Billion by 2035.

- The market grows at a CAGR of 3.6% during the forecast period 2026 to 2035.

- Electrodes dominate the By Type segment with a 35.8% share in 2025.

- Mild Steel leads the By Material Type segment with a 46.9% share in 2025.

- Construction leads the By End Use segment with a 25.8% share in 2025.

Market Dynamics

Drivers - High-Efficiency Flux-Cored and Metal-Cored Consumables Reduce Welding Costs and Improve Productivity

Data from weldingwire.net shows metal-cored welding wires achieve deposition efficiencies of 92% to 98%, converting nearly all consumable weight into deposited weld metal. This efficiency directly lowers material cost per completed joint across U.S. production facilities. Fabricators running high joint-volume lines gain a measurable cost-per-weld advantage over competitors still relying on lower-efficiency solid wire or stick electrode formats on the same weld operations.

weldingwire.net indicates flux-cored welding wires achieve deposition efficiencies of 84% to 89% depending on wire diameter and slag volume. While below metal-cored performance levels, this efficiency still outperforms most manual electrode processes used across U.S. construction and maintenance applications. Fabricators who transition from stick electrodes to flux-cored wire capture both throughput and efficiency gains simultaneously, reducing per-joint cost across two measurable variables with a single process change decision.

In January 2024, Lincoln Electric launched the Mechanized Pipeliner AutoShield, a self-shielded flux-cored system for mechanized pipeline fill and cap passes without shielding gas. Eliminating shielding gas requirements reduces equipment complexity and field logistics cost on pipeline construction projects. This product launch confirms active vendor investment in consumable systems that lower the total operating cost of pipeline welding, a high-volume demand driver tied directly to U.S. energy infrastructure expansion programs.

Restraints - Low-Productivity Welding Processes and Skilled Workforce Requirements Limit Technology Transition

The American Welding Society reports that commonly used 1/8-inch E7018 SMAW electrodes typically provide deposition rates of 3 lb per hour or less. This throughput ceiling restricts productivity in U.S. facilities that rely on manual stick welding for structural joint production. As labor cost per welding hour rises in the domestic market, the output limitation of stick electrode processes becomes a direct margin pressure rather than a process preference question.

weldingwire.net data shows comparable 1.2 mm solid MIG wire typically achieves deposition rates of 3.6 to 4.5 kg per hour at standard production parameters. This throughput ceiling limits productivity gains available to U.S. facilities that have adopted solid wire but not yet transitioned to metal-cored or flux-cored alternatives. Vendors who cannot demonstrate a clear cost justification for wire format upgrades face prolonged solid wire retention among mid-tier fabricators who lack the production volume to trigger economic switchover thresholds.

Based on Lincoln Electric data, the Innershield NR-305 weld deposits provide typical elongation of 25%. Achieving these mechanical properties consistently requires controlled welding parameters and qualified operator technique across every production run. U.S. facilities that lack adequate welder training programs or process monitoring equipment risk weld quality variance that triggers costly rework and procedure re-qualification, effectively penalizing end-users operating below the skill and process control threshold required to realize stated consumable performance specifications.

Growth Factors - Rising Adoption of High-Productivity FCAW Solutions Expands Infrastructure and Structural Welding Opportunities

The American Welding Society states that self-shielded flux-cored wire provides 2 to 3 times the production rate of 1/8-inch E7018 electrodes in comparable applications. This productivity multiplier directly reduces labor cost per meter of completed weld on U.S. construction sites. Contractors who qualify flux-cored procedures on structural steel joints gain a competitive bidding advantage through lower labor cost per joint, which compounds across the large weld volumes generated by infrastructure and commercial building projects.

According to the American Welding Society, switching from stick electrodes to flux-cored wire improves deposition efficiency by 10% or more in field applications. This efficiency gain reduces material consumption per joint beyond the throughput benefit alone. U.S. fabricators and contractors who adopt flux-cored wire across their highest-volume weld operations capture efficiency savings that accumulate into significant annual consumable cost reductions on large-scale structural programs where total weld metal deposited per project is measured in metric tons.

Lincoln Electric data shows the Innershield NR-305 achieves typical Charpy V-notch impact toughness of 40 J at minus 29 degrees Celsius. This low-temperature toughness qualifies the consumable for cold-climate infrastructure and seismic structural applications across northern U.S. states and federal construction programs requiring AWS D1.8 seismic weld qualification. Consumable vendors who hold multiple concurrent weld procedure qualifications reduce the procurement workload for U.S. fabricators, creating a strong preference argument during project-level supplier selection decisions.

Emerging Trends - High-Strength Flux-Cored Consumables and Aluminum Welding Solutions Transform Industrial Fabrication

Lincoln Electric data indicates the Innershield NR-305 weld deposits exhibit a typical tensile strength of 550 MPa and a yield strength of 470 MPa. These mechanical property values support consumable qualification on high-strength structural steel joints requiring defined minimum tensile and yield performance. U.S. fabricators working with higher-grade structural base materials benefit from flux-cored consumables that match steel specifications without requiring supplementary post-weld heat treatment steps that add time and cost to production workflows.

As reported by arsawelding.com, the ESAB Pipeweld 111T-1 gas-shielded flux-cored wire achieves deposition rates ranging from 2.1 to 7.5 kg per hour using 1.2 mm wire at 150 to 350 amperes. This operating range spans from positional root-pass work to high-deposition fill and cap applications on U.S. pipeline and pressure vessel projects. Consumable vendors who offer products qualified across the full deposition rate spectrum reduce the number of separate wire qualifications a fabricator must maintain across a pipeline project’s different welding positions and pass sequences.

In early 2026, Lincoln Electric introduced the AlumaFab Aluminum MIG Welding System for high-volume aluminum welding, targeting U.S. automotive and industrial fabrication. This system-level product launch reflects growing domestic aluminum welding consumable demand tied to electric vehicle battery enclosure production and lightweight structural component manufacturing. Vendors who pair aluminum-specific consumable portfolios with dedicated wire feeding and process control systems capture a more integrated share of the customer’s aluminum welding program spend.

Type Analysis

Electrodes dominates with 35.8% due to broad applicability across manual and field welding operations.

In 2025, Electrodes held a dominant market position in the By Type segment of the U.S. Welding Consumables Market, with a 35.8% share. Electrodes serve the widest range of U.S. field construction, maintenance, and fabrication operations where portability and minimal equipment requirements define the working constraint. Their compatibility with low-capital equipment sustains demand across small fabricators, contractors, and repair operations that constitute a large portion of total domestic welding activity.

Fluxes serve submerged arc and oxy-fuel welding processes that dominate thick-plate fabrication across U.S. shipbuilding, pressure vessel, and pipeline construction facilities. Flux consumption scales directly with weld volume and bead size, making large-structure fabrication programs the primary demand driver within this sub-segment. Buyers on long-term construction contracts establish qualified flux suppliers early in the project lifecycle, locking in vendor relationships that persist for the duration of multi-year fabrication programs.

Material Type Analysis

Mild Steel dominates with 46.9% due to its universal use across U.S. construction, fabrication, and infrastructure sectors.

In 2025, Mild Steel held a dominant market position in the By Material Type segment of the U.S. Welding Consumables Market, with a 46.9% share. Mild steel is the most widely fabricated structural material in the U.S. economy. Its use across construction, shipbuilding, energy infrastructure, and general manufacturing ensures that mild steel welding consumables generate the highest aggregate domestic volume demand across all geographies and end-use sectors simultaneously.

Stainless Steel consumables serve U.S. food processing, pharmaceutical, chemical processing, and offshore industries where corrosion resistance is a structural specification rather than an aesthetic preference. Stainless welding requires tighter shielding gas control and more precise heat input management than mild steel, supporting premium pricing for qualified stainless consumable products. Vendors with established stainless alloy expertise and concurrent AWS or ASME qualification documentation hold a preferred-vendor advantage in regulated U.S. industries where supplier approval processes are extended and costly.

Aluminum welding consumables serve U.S. automotive lightweighting programs, aerospace structural fabrication, and marine construction where weight reduction directly affects operational performance or fuel economy outcomes. Aluminum welding requires specialized wire feeding systems and inert shielding gas chemistry, creating system-level equipment dependencies that tie consumable purchases to specific platform configurations. In early 2026, Lincoln Electric introduced the AlumaFab Aluminum MIG Welding System for high-volume aluminum welding, confirming that domestic demand for aluminum welding solutions is sufficient to justify dedicated system investment from major U.S. vendors.

End Use Analysis

Construction dominates with 25.8% due to sustained federal infrastructure investment and structural steel fabrication demand.

In 2025, Construction held a dominant market position in the By End Use segment of the U.S. Welding Consumables Market, with a 25.8% share. Federal infrastructure legislation allocates capital toward bridge rehabilitation, highway construction, port modernization, and utility grid upgrades that require structural steel fabrication at scale. This public investment program generates multi-year welding consumable procurement demand that extends beyond normal commercial construction cycles and provides revenue visibility that private-sector project pipelines alone cannot sustain.

Automobile manufacturing uses welding consumables across body-in-white assembly, chassis fabrication, battery enclosure production, and exhaust system manufacturing on U.S. production lines. Automotive welding operates under strict process parameter controls and dedicated wire-feeding equipment configurations that demand consistent consumable chemistry across every production batch. Vendors who achieve Tier 1 automotive supplier qualification gain access to multi-year supply agreements tied to vehicle production schedules rather than annual competitive rebid cycles.

Energy sector buyers consume welding consumables across U.S. oil and gas pipeline construction, refinery turnaround maintenance, nuclear plant component repair, and offshore platform fabrication. Each sub-sector carries distinct consumable qualification requirements tied to pressure class, operating temperature, and corrosion service conditions. Consumable vendors who hold multiple concurrent energy sector certifications simultaneously reduce the number of separate supplier approval processes a fabricator must manage, increasing their share of wallet across integrated energy facility procurement programs.

Key Market Segments

By Type

- Electrodes

- Shielded Metal Arc Welding Electrodes

- Gas Metal Arc Welding Electrodes

- Others

- Fluxes

- Submerged Arc Welding Flux

- Oxy-Fuel Welding Flux

- Others

- Gases

- Shielding Gases

- Backing Gases

- Others

- Filler Metals

- Solid Wire

- Flux-Cored Wire

- Metal-Cored Wire

- Welding Rods

- Others

- Others

By Material Type

- Mild Steel

- Stainless Steel

- Aluminum

- Nickel Alloys

- Copper Alloys

- Others

By End Use

- Construction

- Automobile

- Energy

- Shipbuilding

- Aerospace

- Heavy Engineering

- Others

Key Company Insights

Lincoln Electric Holdings Inc. holds the leading strategic position in the U.S. market through its combination of welding equipment, consumables, and automation systems serving domestic industrial buyers. In July 2024, the company acquired Vanair Manufacturing, a U.S.-based provider of mobile power solutions including welders, broadening its service truck and maintenance repair market coverage. This acquisition extends Lincoln Electric’s consumable pull-through opportunity into the maintenance and repair segment, where field welding consumable repurchase rates are high and brand loyalty is strong.

ESAB Corporation competes across the U.S. consumables market with a broad product portfolio spanning electrodes, flux-cored wires, and specialty alloy filler metals for industrial and construction buyers. ESAB states that flux-cored welding can be up to 3 times more productive than stick welding in fabrication applications, a productivity claim that supports its sales position in U.S. fabrication markets where labor cost drives consumable format decisions. ESAB’s pending acquisition of EWM GmbH adds heavy industrial automation capability that strengthens its integrated solutions argument with large U.S. industrial accounts.

Harris Products Group occupies a strong position in U.S. gas welding, brazing, and soldering consumables, serving HVAC, plumbing, and specialty industrial markets that require non-arc joining materials. Its product focus on gas-based and brazing consumable categories insulates it from direct competition with arc wire and electrode specialists in the market’s largest volume segments. This differentiated category position allows Harris to compete on application expertise and distribution reach rather than engaging in price competition against larger arc welding consumable vendors.

Illinois Tool Works Inc. (Hobart Brothers) leverages its position within ITW’s diversified industrial portfolio to support Hobart’s consumables business with cross-segment manufacturing scale and U.S. distribution infrastructure. Hobart Brothers serves structural steel fabrication, shipbuilding, and general manufacturing customers across the domestic market with flux-cored and metal-cored wire product lines. The parent company’s operational scale provides procurement and logistics advantages that allow Hobart to compete on delivery reliability and supply consistency, factors that fabricators on tight production schedules weight heavily in supplier selection decisions.

Key Players

- Lincoln Electric Holdings Inc.

- ESAB Corporation

- Harris Products Group

- Weldcote Metals

- Eutectic Castolin

- Illinois Tool Works Inc. (Hobart Brothers)

- voestalpine Bohler Welding USA

- Kobe Steel Ltd. (Kobelco Welding of America)

- Air Liquide Welding

- Washington Alloy Co.

- Sandvik Materials Technology (Exaton)

- Messer Group

- Wire Wizard Welding Products

Recent Developments

- August 2025 – Lincoln Electric acquired the remaining interest in Alloy Steel Australia, completing full ownership and enhancing its wear-plate and engineered maintenance solutions relevant to U.S. operations.

- June 2025 – ESAB Corporation signed a definitive agreement to acquire EWM GmbH (Germany) for approximately €275 million (USD 317 million), targeting completion in H2 2025, to strengthen its heavy industrial welding equipment and automation capabilities.

- 2025 – ESAB completed the acquisition of Bavaria Schweisstechnik, a European consumables business, expanding its international consumables portfolio with relevance to U.S. multi-national customer supply chains.

- February 2026 – Miller Electric launched the Venture 150 T battery-powered TIG welder, expanding its portable battery-powered lineup for field and maintenance welding applications across the U.S. market.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.2 Billion |

| Forecast Revenue (2035) | USD 3.1 Billion |

| CAGR (2026-2035) | 3.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Electrodes: Shielded Metal Arc Welding Electrodes, Gas Metal Arc Welding Electrodes, Others; Fluxes: Submerged Arc Welding Flux, Oxy-Fuel Welding Flux, Others; Gases: Shielding Gases, Backing Gases, Others; Filler Metals: Solid Wire, Flux-Cored Wire, Metal-Cored Wire, Welding Rods, Others; Others); By Material Type (Mild Steel, Stainless Steel, Aluminum, Nickel Alloys, Copper Alloys, Others); By End Use (Construction, Automobile, Energy, Shipbuilding, Aerospace, Heavy Engineering, Others) |

| Competitive Landscape | Lincoln Electric Holdings Inc., ESAB Corporation, Harris Products Group, Weldcote Metals, Eutectic Castolin, Illinois Tool Works Inc. (Hobart Brothers), voestalpine Bohler Welding USA, Kobe Steel Ltd. (Kobelco Welding of America), Air Liquide Welding, Washington Alloy Co., Sandvik Materials Technology (Exaton), Messer Group, Wire Wizard Welding Products |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |