Quick Navigation

Report Overview

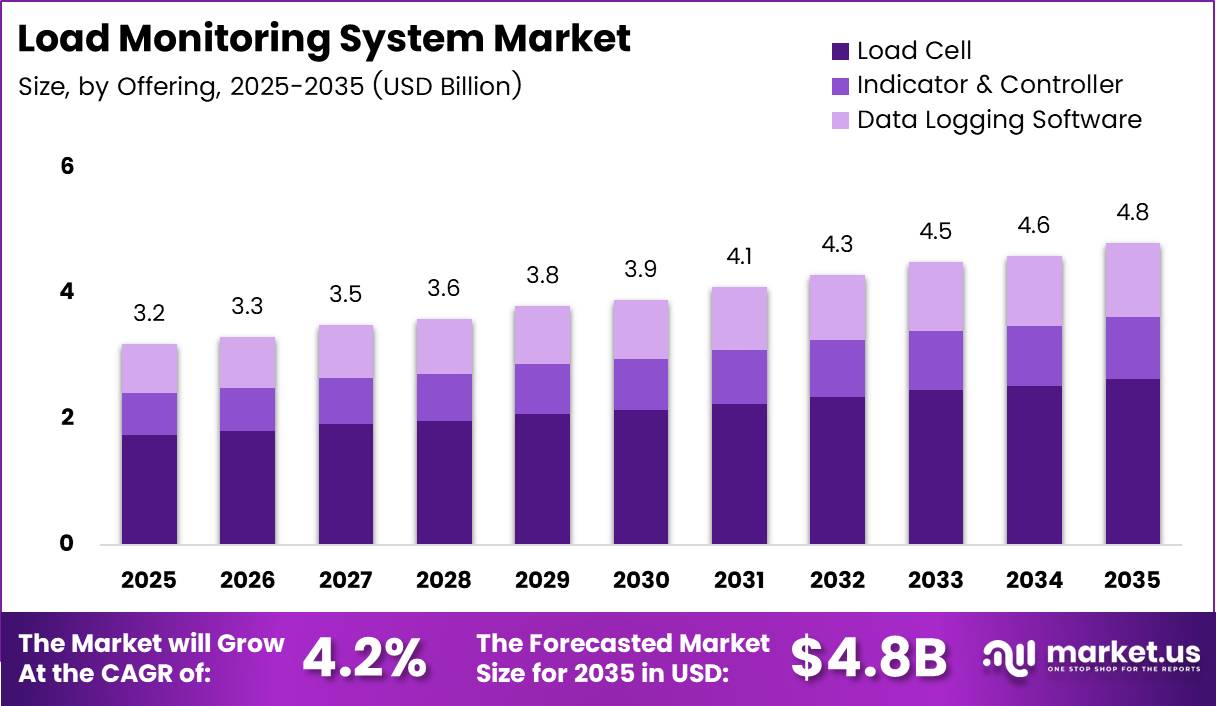

Global Load Monitoring System Market size is expected to be worth around USD 4.8 Billion by 2035 from USD 3.2 Billion in 2025, growing at a CAGR of 4.2% during the forecast period 2026 to 2035.

Load monitoring systems measure, track, and record force or weight applied to mechanical structures, lifting equipment, and industrial machinery. These systems combine load cells, indicators, controllers, and data logging software to deliver real-time visibility into operational loads. End users depend on them to prevent overloading, reduce equipment failure, and maintain compliance with safety regulations.

The market organizes around three core segment dimensions: offering type, technology type, and end-user industry. Offering spans load cells, indicators and controllers, and data logging software. Technology divides between digital and analog platforms. End users range from automotive and aerospace to construction, oil and gas, marine, and healthcare sectors.

Governments and regulators across industrial economies enforce strict equipment load compliance standards for lifting gear, transport vehicles, and structural installations. These mandates require certified load monitoring across cranes, hoists, and freight systems. Regulatory pressure converts compliance from a discretionary upgrade into a procurement requirement, which sustains baseline demand independent of capital investment cycles.

Workplace safety legislation in Europe, North America, and Asia Pacific increasingly specifies load limits for material handling operations. Non-compliance carries operational shutdowns and financial penalties. This regulatory environment creates consistent procurement cycles for calibrated load monitoring equipment across construction, logistics, and heavy industry operators.

According to Transmission Dynamics, wireless load monitoring systems now reach communication ranges of up to 3 km with battery lives extending to 20 years. This specification shift reduces infrastructure dependency in remote or complex installations. Buyers in offshore energy, mining, and large-scale construction gain monitoring capability without wired network investment, expanding the addressable market beyond fixed industrial facilities.

Data from logicbus shows that load cells specified for automated storage and retrieval systems require a minimum sampling rate of 1,000 Hz and a fatigue life exceeding 100 million load cycles. These performance thresholds reflect the precision demands of high-throughput automation environments. Vendors able to meet these specifications consistently will win preferred supplier status as warehouse and logistics automation accelerates globally.

Key Takeaways

- The global Load Monitoring System Market was valued at USD 3.2 Billion in 2025 and is forecast to reach USD 4.8 Billion by 2035.

- The market advances at a CAGR of 4.2% over the forecast period 2026 to 2035.

- By Offering, Load Cell dominates with a 54.8% share, driven by its foundational role in all load measurement architectures.

- By Technology, Digital platforms hold 67.2% market share, reflecting widespread adoption of digital signal processing across industrial deployments.

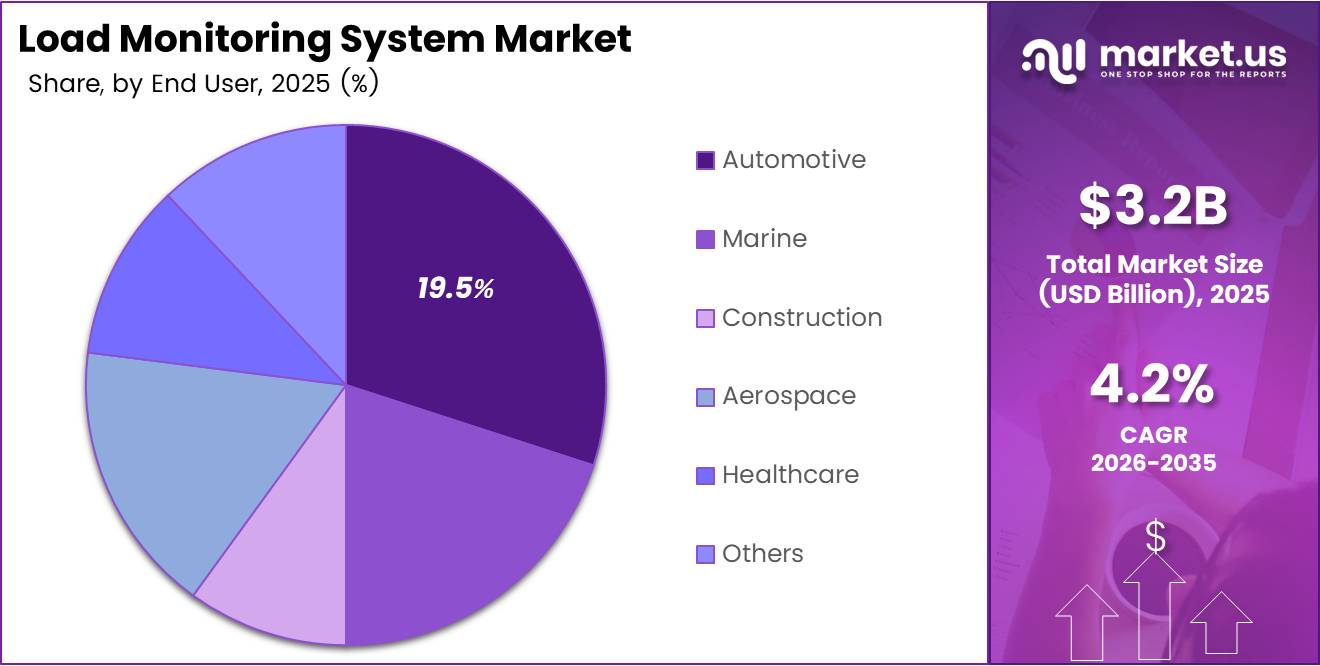

- By End User, Automotive leads with a 19.5% share, supported by stringent vehicle load compliance and onboard weighing mandates.

- Europe holds the dominant regional position with a 43.60% market share, valued at USD 1.3 Billion.

Offering Analysis

Load Cell dominates with 54.8% due to its foundational role in all load measurement architectures.

In 2025, Load Cell held a dominant market position in the By Offering segment of the Load Monitoring System Market, with a 54.8% share. Load cells serve as the primary sensing element in every monitoring configuration, making them a non-negotiable procurement item. This structural necessity protects the segment from substitution and gives load cell manufacturers pricing leverage across the full system supply chain.

Single Beam Load Cell suits low-capacity platform and bench weighing applications where compact design and cost efficiency are the primary purchase criteria. Buyers in retail, light industrial, and laboratory segments drive steady volume for this sub-type. The simplicity of single beam geometry reduces calibration complexity, which lowers total ownership cost and sustains repeat procurement across price-sensitive end users.

S-Type Load Cell handles both tension and compression measurement in a single unit, making it the preferred choice for hanging scales, hopper systems, and actuator force monitoring. Its bidirectional capability reduces the number of sensor types a plant operator must stock. This consolidation benefit drives specification preference among procurement teams managing multi-application industrial facilities.

Dual Shear Load Cell delivers high accuracy under off-center loads, which makes it the standard choice for multi-point platform weighing and tank measurement. Its tolerance of eccentric loading reduces installation sensitivity and measurement error in real-world deployments. Operators in food processing, chemical handling, and bulk material weighing specify dual shear cells where consistent accuracy across uneven load distribution is required.

Bending Beam Load Cell serves low-to-medium capacity applications including conveyor belt scales, level monitoring, and onboard vehicle weighing. In March 2025, Flintec introduced the SSB7 bending beam load cell specifically for transportation weighing systems, signaling active product development in this sub-type. Vendors investing in transport-rated bending beam designs are positioning for growing demand in fleet compliance and logistics.

Indicator and Controller units translate raw load cell signals into usable data displays and control outputs for operators and automated systems. These components add decision-layer intelligence to raw sensor data, enabling setpoint control, overload alarms, and process interlocks. Their integration role makes them recurring upgrade targets as end users migrate from analog readouts to digital display and network-connected control architectures.

Data Logging Software captures, stores, and analyzes time-series load data to support compliance documentation, predictive maintenance, and operational auditing. Software adoption rises as industrial operators shift from reactive to condition-based maintenance strategies. Vendors who bundle logging software with hardware systems create switching costs that support recurring revenue through subscriptions, updates, and analytics module expansions.

Technology Analysis

Digital dominates with 67.2% due to superior signal clarity and network integration capability.

In 2025, Digital held a dominant market position in the By Technology segment of the Load Monitoring System Market, with a 67.2% share. Digital load monitoring systems convert sensor signals directly into digital outputs, eliminating noise interference common in analog signal chains. This performance advantage drives specification preference across automated manufacturing, logistics, and infrastructure monitoring where measurement reliability directly affects safety and throughput decisions.

Analog load monitoring technology remains active in cost-constrained applications and legacy industrial environments where retrofit costs outweigh the performance gain from digital migration. Analog systems carry lower upfront hardware costs, which sustains their presence in small-scale and developing-market deployments. However, their inability to interface with modern data networks limits their adoption in new installations and positions them for gradual replacement as digital platforms reach lower price points.

End User Analysis

Automotive dominates with 19.5% due to vehicle weight compliance and onboard monitoring mandates.

In 2025, Automotive held a dominant market position in the By End User segment of the Load Monitoring System Market, with a 19.5% share. Vehicle axle load monitoring is a regulatory requirement in most major freight markets, driving consistent system procurement across commercial fleet operators. This compliance-driven demand makes automotive the most predictable revenue segment for load monitoring suppliers focused on volume and contract stability.

Marine applications require load monitoring systems that withstand saltwater exposure, vessel motion, and extreme temperature variation. Offshore crane operations, mooring line tensioning, and cargo lifting all depend on accurate real-time load data to prevent structural failure. As offshore energy infrastructure expands, marine-rated load monitoring becomes a procurement priority for both equipment manufacturers and asset operators.

Construction deployments center on crane load management, structural load tracking during building phases, and foundation monitoring for high-rise and civil infrastructure projects. Lifting equipment regulations in most construction markets mandate overload protection systems on mobile and tower cranes. This regulatory requirement converts construction site load monitoring from optional safety equipment into a compliance-driven purchase across major project categories.

Aerospace uses load monitoring systems in ground support equipment, aircraft weighing, and fatigue testing of structural components. The precision requirements in aerospace manufacturing and maintenance create demand for high-accuracy, certified load measurement equipment. Buyers in this segment prioritize traceable calibration and documentation over cost, giving premium load monitoring vendors a defensible margin position.

Oil and Gas operations deploy load monitoring across drilling equipment, pipeline tensioning, subsea lifting, and wellhead load management. Harsh operating environments and high consequence of equipment failure make certified, ruggedized monitoring systems essential rather than optional. Spending in this segment tracks capital investment cycles in upstream and subsea development, with offshore expansion driving the strongest near-term procurement activity.

Healthcare applications include patient lift systems, medical bed load monitoring, and rehabilitation equipment force measurement. Accurate load sensing in patient handling equipment reduces injury risk for both patients and clinical staff. Regulatory standards for medical device performance push healthcare procurement toward certified, high-precision load cells, creating a quality-first buying environment that supports premium pricing for compliant suppliers.

Others covers sectors including agriculture, mining, utilities, and research institutions that deploy load monitoring across specialized equipment and structural testing rigs. Demand in this group is fragmented but collectively significant, as each sub-sector applies load measurement to distinct operational safety and efficiency needs. Suppliers with broad product ranges and application engineering support capture a disproportionate share of these diverse procurement opportunities.

Key Market Segments

By Offering

- Load Cell

- Single Beam Load Cell

- S-Type Load Cell

- Dual Shear Load Cell

- Bending Beam Load Cell

- Others

- Indicator & Controller

- Data Logging Software

By Technology

- Digital

- Analog

By End User

- Automotive

- Marine

- Construction

- Aerospace

- Oil & Gas

- Healthcare

- Others

Drivers

Deep-learning load estimation achieves under 5% error in logistics trials

As reported by Sagepub, deep-learning load monitoring systems in logistics vehicle trials achieved load estimation mean absolute percentage errors under 5% compared with reference measurements. This accuracy level enables reliable overload detection without physical weighing infrastructure. Fleet operators gain a cost-effective compliance tool, and load monitoring vendors with AI-integrated offerings gain a differentiation argument over conventional sensor-only competitors.

Workplace safety regulations across industrial economies require certified load monitoring on cranes, hoists, and material handling equipment. Non-compliant operators face operational shutdowns and financial penalties. This regulatory baseline creates procurement demand that remains stable regardless of broader capital investment conditions, giving load monitoring suppliers a predictable revenue floor tied to enforcement cycles rather than discretionary spending.

Based on logicbus data, load cells specified for automated storage and retrieval systems require minimum sampling rates of 1,000 Hz and fatigue lives exceeding 100 million load cycles. High-throughput warehouse automation demands measurement reliability at this performance tier. Vendors who certify their load cells to these specifications capture preferred supplier positions in logistics automation, where procurement decisions favor proven components over lower-cost alternatives.

Restraints

Legacy equipment integration raises total cost beyond initial hardware investment

Industrial facilities operating older control systems face significant engineering effort when retrofitting digital load monitoring into existing equipment architectures. Signal protocol mismatches, power supply incompatibilities, and mechanical interface differences each require custom engineering solutions. This integration burden raises total project cost and extends deployment timelines, which causes procurement decision-makers to delay or scale back monitoring upgrades.

According to Dewesoft, remote load monitoring reduced the need for on-site manual roof inspections by more than 60% during heavy snowfall events. While this efficiency gain validates the operational case for monitoring investment, it also highlights the reliance on continuous system uptime. Calibration failures or sensor drift during critical weather events can eliminate the safety advantage, making periodic maintenance a non-negotiable operational cost that increases total ownership burden.

Data from itestsystem shows a campus structural monitoring installation instrumented with more than 40 load and strain channels logging continuously across 24 hours per day. Maintaining measurement accuracy across this channel count requires scheduled recalibration, sensor replacement, and software validation. Operators managing large-scale deployments face recurring maintenance costs that accumulate significantly over multi-year monitoring programs, constraining expansion decisions for cost-sensitive buyers.

Growth Factors

IoT freight monitoring cuts manual weighing delays by 50% per transit stop

Figures from logicbus show that IoT-based real-time load monitoring in freight transport reduced manual weighing stops by approximately 50%, cutting average trip delays from 40 to 60 minutes per stop down to under 10 minutes for exception checks only. This operational efficiency gain creates a measurable return on investment argument for fleet operators. Load monitoring vendors who quantify these time savings in sales materials accelerate procurement decisions in logistics-focused accounts.

[Source] indicates that wireless load monitoring systems achieve communication ranges of up to 3 km with battery lives extending to 20 years, based on Transmission Dynamics specifications for the LMF+ platform. These parameters remove the cabling and power infrastructure barriers that previously excluded remote and offshore sites from continuous monitoring. This capability expansion opens offshore energy, large construction sites, and remote mining operations as addressable markets for wireless load monitoring providers.

Based on topicon data, fleet axle load monitoring systems provide real-time vehicle weight data with display refresh times of approximately 1 second, reducing overload violations by double-digit percentages in field deployments. Faster feedback gives drivers actionable information before weight violations occur. Logistics operators running large fleets calculate direct cost savings from reduced fines and fewer roadside inspections, making the business case for onboard load monitoring straightforward and measurable.

Emerging Trends

AI-assisted transformer monitoring cuts overload incidents by up to 30%

According to impresa.ai, AI-assisted transformer load monitoring reduced unplanned overload incidents by 25 to 30% across monitored transformer fleets. This performance improvement translates directly into reduced outage risk and lower emergency maintenance costs for utility operators. Load monitoring vendors integrating predictive analytics into their platforms position themselves for procurement preference in the utility sector, where downtime costs far exceed monitoring system investment.

[Source] data from impresa.ai shows that equipping all distribution transformers in a pilot area with real-time load monitoring raised visibility from 0% to 100% of units continuously monitored. Full fleet visibility enables system operators to balance loads proactively rather than respond to failures reactively. This operational shift from reactive to predictive management creates recurring software and analytics revenue opportunities for monitoring platform vendors beyond the initial hardware sale.

Cloud-based load monitoring dashboards are consolidating real-time data from distributed sensor networks into centralized operational views accessible across devices and locations. This architecture shift enables remote asset management without on-site personnel. In April 2025, Flintec launched the CC PRO and CC PRO-A wireless platform with real-time monitoring and control delivered through the CC Connect application, demonstrating that leading vendors are already commercializing cloud-connected monitoring for industrial well and load operations.

Regional Analysis

Europe Dominates the Load Monitoring System Market with a Market Share of 43.60%, Valued at USD 1.3 Billion

Europe commands 43.60% of the global Load Monitoring System Market, valued at USD 1.3 Billion. The region’s lead reflects strict EU machinery safety directives that mandate certified load monitoring on lifting equipment across construction, manufacturing, and logistics operations. Germany, France, and the UK drive the largest procurement volumes, supported by dense industrial infrastructure and active enforcement of equipment compliance standards.

North America holds the second-largest regional position, supported by OSHA load compliance requirements for lifting and material handling equipment across industrial, construction, and transportation sectors. The US logistics sector’s rapid adoption of warehouse automation and fleet management technology drives consistent demand for precision load cells and digital monitoring platforms. Canadian mining and energy operations add further procurement volume in ruggedized monitoring applications.

Asia Pacific represents the highest absolute growth potential among all regions, driven by large-scale infrastructure investment in China, India, and Southeast Asia. Rapid expansion of manufacturing capacity, commercial construction, and port logistics creates broad deployment opportunities for load monitoring systems. Regulatory modernization across the region is progressively aligning local safety standards with European and North American benchmarks, expanding the compliance-driven procurement base.

Latin America shows moderate development in load monitoring adoption, concentrated in Brazil’s agricultural equipment and mining sectors and Mexico’s growing automotive manufacturing base. Infrastructure investment programs in both countries are creating crane and structural monitoring procurement opportunities. However, budget constraints in public sector projects and fragmented industrial regulation slow the pace of compliance-driven adoption relative to more mature markets.

The Middle East and Africa region is an emerging market for load monitoring, anchored by Gulf Cooperation Council investment in offshore energy infrastructure, port expansion, and large-scale construction projects. Offshore crane monitoring and structural load tracking in high-rise developments represent the primary procurement categories. South Africa’s mining sector adds industrial demand, while regulatory frameworks in most of the region remain less prescriptive, making safety-led selling the primary growth strategy for vendors entering this market.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Applied Measurements Ltd. specializes in the design and supply of load cells and force measurement instruments for UK and international industrial markets. The company’s focus on custom-engineered sensing solutions gives it an advantage in applications where standard catalog products fail to meet dimensional or performance specifications. However, a custom-first model limits volume scalability compared with manufacturers competing on standardized, high-volume product lines.

Datum Electronics Ltd. develops torque and load measurement systems targeting marine, automotive, and industrial test environments. Its dual-market presence across both torque and load sensing provides cross-selling opportunities within a single customer base. This breadth reduces revenue concentration risk. By contrast, competitors focused exclusively on load monitoring may build deeper application expertise in specific verticals, giving them a targeted advantage in high-specification procurement decisions.

Dynamic Load Monitor UK Ltd. focuses on portable and wireless load monitoring solutions designed for crane, rigging, and lifting applications across construction and offshore sectors. The portability emphasis addresses a real operational gap where fixed wired systems cannot be practically deployed. This product positioning aligns directly with the market’s shift toward wireless and remote monitoring, though the company must demonstrate long-term connectivity and durability to compete at enterprise procurement levels.

Eilersen Electric Digital AS produces digital load cells using capacitive measurement technology, which the company positions as more durable and reliable than strain gauge alternatives in harsh industrial environments. Capacitive sensing reduces vulnerability to temperature variation and mechanical fatigue over extended service periods. In 2025, VPG Force Sensors completed its rebranding to sharpen its own force measurement identity, signaling that the competitive landscape is consolidating around focused measurement specialists, which increases pressure on all dedicated load cell producers to differentiate clearly.

Key Players

- Applied Measurements Ltd.

- Datum Electronics Ltd.

- Dynamic Load Monitor UK Ltd.

- Eilersen Electric Digital AS

- Flintec Group AB

- Interface Inc.

- JCM Load Monitoring Ltd.

- Kistler Group

- LCM Systems Ltd.

- Load Monitoring Systems

Recent Developments

- September 2024 – Vishay Precision Group acquired Nokra Optische Prueftechnik & Automation GmbH to expand its precision measurement and sensing portfolio used in industrial monitoring and load measurement applications.

- April 2025 – Flintec launched the CC PRO and CC PRO-A wireless load monitoring platform, featuring real-time monitoring and control through the CC Connect application for industrial well and load-monitoring operations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.2 Billion |

| Forecast Revenue (2035) | USD 4.8 Billion |

| CAGR (2026-2035) | 4.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Offering (Load Cell: Single Beam Load Cell, S-Type Load Cell, Dual Shear Load Cell, Bending Beam Load Cell, Others; Indicator & Controller; Data Logging Software), By Technology (Digital, Analog), By End User (Automotive, Marine, Construction, Aerospace, Oil & Gas, Healthcare, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Applied Measurements Ltd., Datum Electronics Ltd., Dynamic Load Monitor UK Ltd., Eilersen Electric Digital AS, Flintec Group AB, Interface Inc., JCM Load Monitoring Ltd., Kistler Group, LCM Systems Ltd., Load Monitoring Systems |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |