Quick Navigation

Report Overview

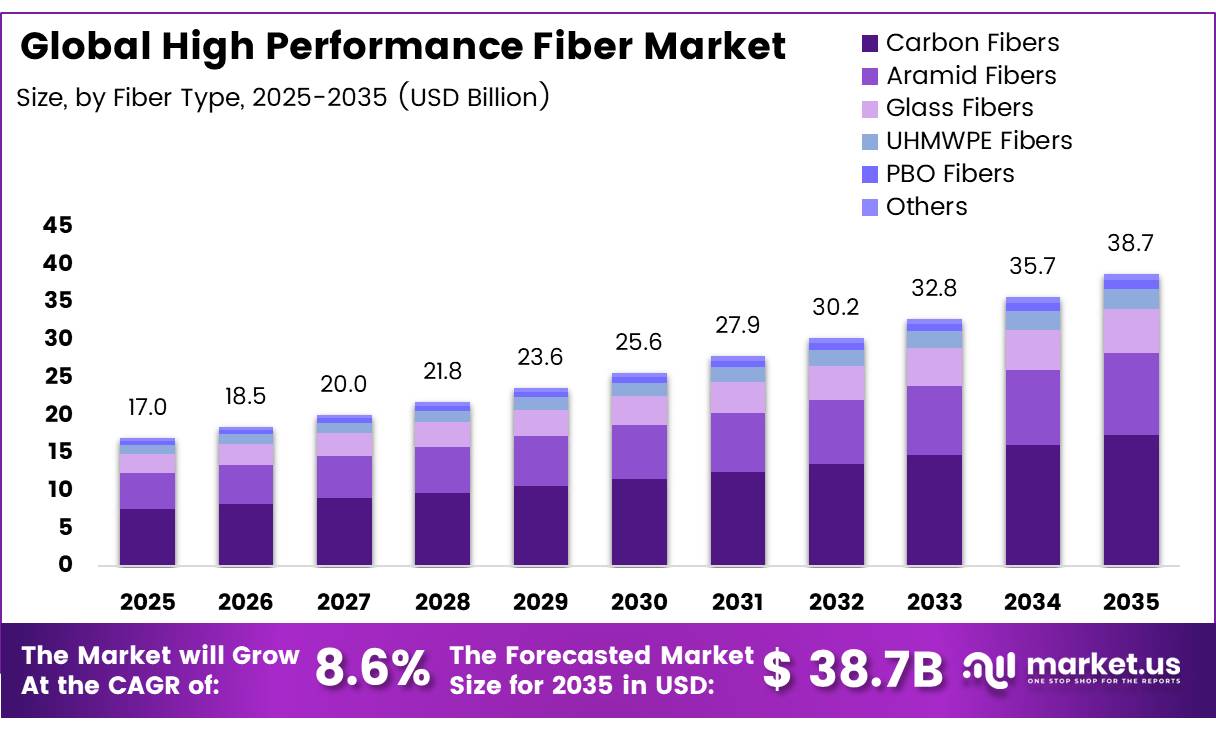

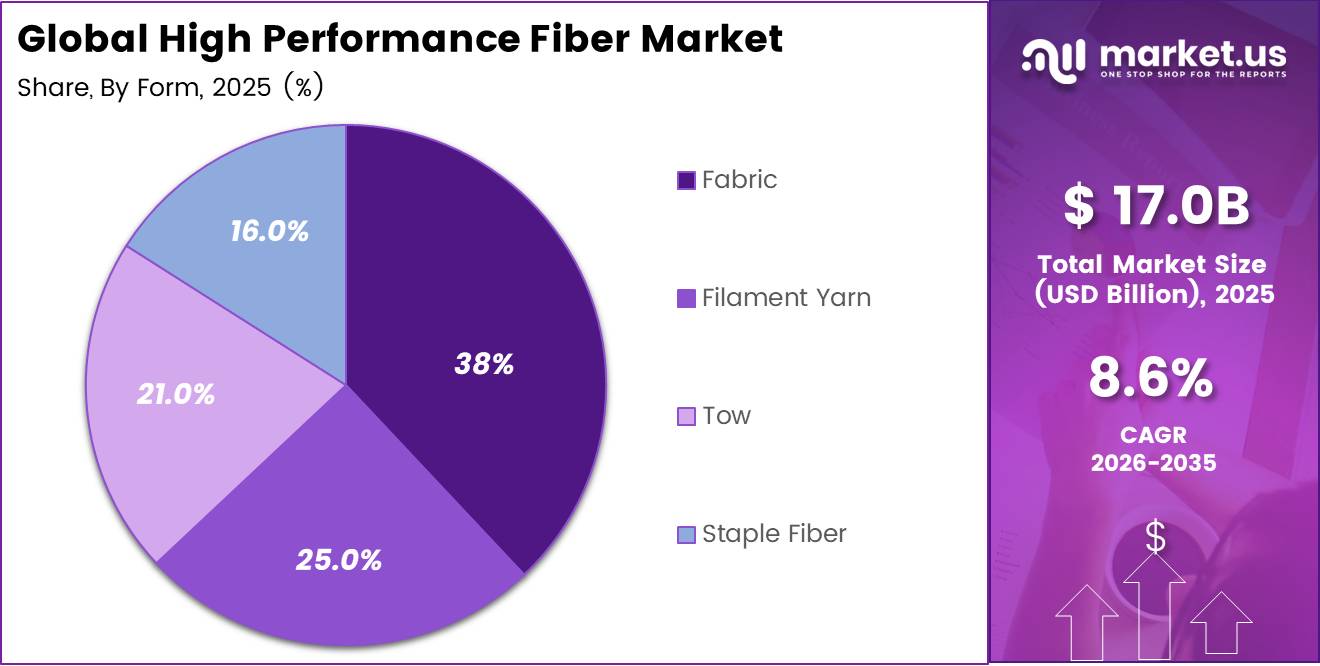

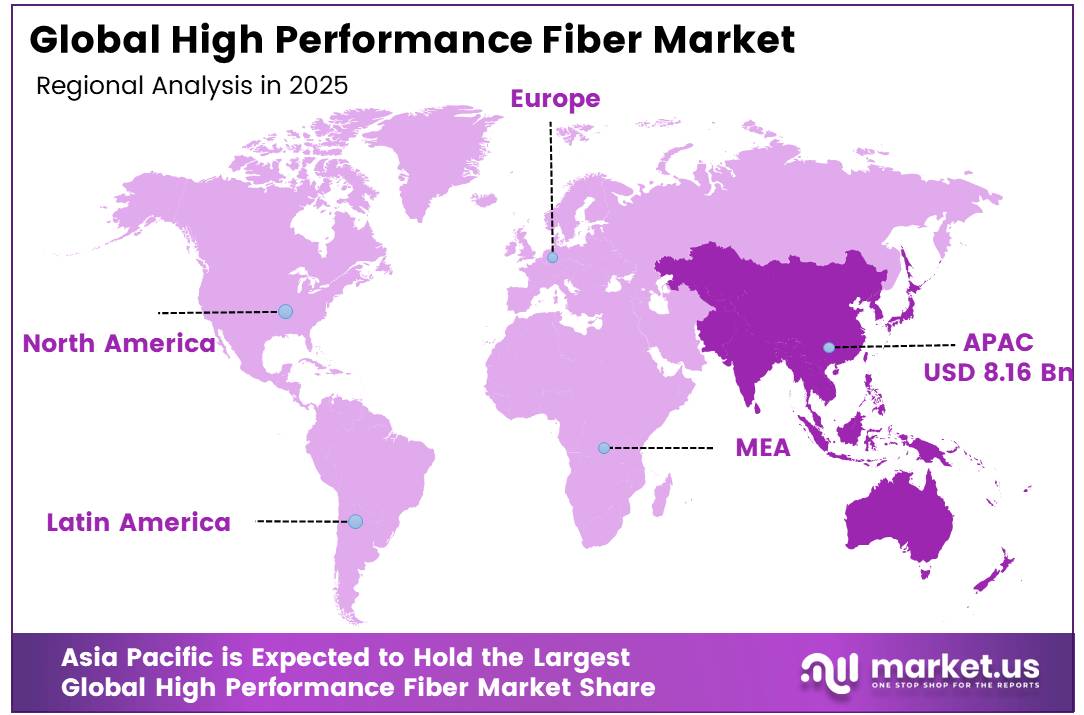

In 2025, the Global High Performance Fiber Market was valued at USD 17.0 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 8.6%, reaching about USD 38.7 billion by 2035. In 2025, Asia Pacific led the market, achieving over 48% share with a revenue of USD 8.16 Billion.

The high-performance fiber industry is advancing as aerospace, automotive, wind-energy, hydrogen-storage and protective-equipment manufacturers seek materials offering high strength, low weight, heat resistance and long service life. Carbon, aramid, ceramic and ultra-high-molecular-weight polyethylene fibers increasingly replace heavier metals in demanding structures.

- According to the U.S. Department of Energy, a 10% reduction in vehicle weight can improve fuel economy by 6%–8%, while carbon-fiber-reinforced composites can reduce certain component weights by 50%–75%.

Demand is supported by electric-vehicle efficiency, longer wind blades and composite pressure vessels. However, high precursor costs, slow production, difficult joining and limited recycling remain major industrial barriers. In September 2024, the U.S. Department of Energy awarded six recycling teams $500,000 each plus $100,000 in laboratory vouchers, totaling $3.6 million, to commercialize solutions for carbon-fiber, fiberglass and other wind-turbine materials.

Future opportunities will emerge from recycled carbon fiber, thermoplastic composites, automated fiber placement and lower-energy manufacturing. In fiscal year 2025, a U.S. Department of Energy commercialization project targeted recycled carbon-fiber composites with more than 75% lower embodied energy and cost. These developments should strengthen fiber adoption across transportation, renewable energy, defence and advanced industrial equipment globally during the coming decade.

Key Takeaways

- The global high performance fiber market was valued at USD 17.0 billion in 2025.

- The global high performance fiber market is projected to grow at a CAGR of 8.6% and is estimated to reach USD 38.7 billion by 2035.

- On the basis of fiber type, the carbon fibers dominated the global high performance fiber market, constituting 45% of the total market share in 2025.

- Based on the form, the fabric dominated the high performance fiber market, with a substantial market share of around 38% in 2025.

- Based on the distribution channel, direct sales led the global high performance fiber market, comprising 65% of the total market in 2025.

- Among the end-use industries, the aerospace and defense industry held a major share in the high performance fiber market, 37% of the market share in 2025.

- In 2025, the Asia Pacific was the most dominant region in the high performance fiber market, accounting for 48% of the total global consumption.

Fiber Type Analysis

Carbon fiber represents dominant Segment in the Market.

In 2025, carbon fibers held the leading position, capturing a 45.0% share of the high-performance fiber market. Their stiffness, fatigue resistance and low weight make them valuable in aircraft components, wind blades, pressure vessels and performance vehicles.

- A U.S. Department of Energy-supported wind project found that carbon-fiber spar caps reduced blade mass by 25% compared with fiberglass. The textile-based carbon fiber examined in the project also cost 40% less than conventional commercial material, indicating stronger potential for wider industrial adoption.

UHMWPE fibers are expected to grow fastest as demand rises for lightweight helmets, body armor, ropes and cut-resistant equipment. The U.S. Army developed a UHMWPE-based helmet prototype with a 2.5-pound shell and an estimated finished weight of 3.5 pounds. It delivered protection comparable to an existing helmet system weighing more than 5 pounds, demonstrating how the fiber can improve mobility and comfort for personnel working in demanding conditions.

End-Use Industry Analysis

Aerospace and Defense Leads in end use industry segment.

In 2025, Aerospace and Defense held the leading position, capturing a 37.0% share of the high-performance fiber market. Carbon, aramid and ceramic fibers are increasingly used in aircraft structures, engine components, radomes, spacecraft and ballistic protection because they provide high strength without adding excessive weight.

- In May 2026, the U.S. Federal Aviation Administration projected that the commercial aircraft fleet would expand from 7,387 aircraft in 2024 to 10,607 by 2045, reflecting 1.7% average annual growth. NASA’s HiCAM initiative is also developing faster and more economical production methods for composite wings and fuselages.

Automotive and Transportation is expected to grow fastest as manufacturers use lightweight fibers to offset heavy electric-vehicle batteries and improve driving efficiency. The U.S. Department of Energy states that a 10% vehicle-weight reduction can improve fuel economy by 6%–8%. Its Materials Technology program also targets a 25% reduction in light-duty vehicle body, chassis and interior weight by 2030.

Form Analysis

Fabric Are the Most Widely Used Form.

In 2025, fabric held the leading position, capturing a 38.0% share of the high-performance fiber market. Woven, braided and multiaxial fabrics distribute stress across several directions, making them practical for aircraft panels, protective structures, vehicle components and wind turbine blades. Their flexibility also allows manufacturers to shape complex parts through resin infusion, prepreg lay-up and compression moulding.

- In January 2024, the UK Defence Science and Technology Laboratory established a £42.5 million advanced-materials partnership involving 23 partners, supporting research into materials capable of surviving temperatures of 1,000°C and other extreme conditions.

Filament yarn is expected to expand fastest as continuous fibers are increasingly required for automated placement, pultrusion and filament-wound hydrogen tanks. In May 2024, the U.S. Department of Energy reported that carbon fiber represented approximately 50% of a vehicle high-pressure storage system’s cost. Government-supported filament-spinning improvements increased polymer loading by 67% and production-line speeds by 78%, improving the potential for economical, high-volume yarn manufacturing

Distribution Channel Analysis

Direct sales Held a Major Share of the Global High Performance Fiber Market.

Direct sales dominate with 65% because the technical qualification requirements governing high performance fiber procurement in aerospace and defense make transactional distributor supply impractical for the majority of high-value applications. A qualified fiber supplier for an aircraft program must demonstrate material traceability, batch consistency, and compliance with OEM-specific material specifications that require direct supplier-to-manufacturer quality management relationships.

- For instance, Solvay’s carbon fiber prepreg supply framework on the Boeing 787 Dreamliner program, where platform-level EASA and FAA certification requires unbroken material traceability from fiber producer to finished composite part, making distributor intermediation structurally ineligible regardless of logistics economics.

The distributor channel is accelerating because industrial, construction, and emerging composite manufacturing segments require regional inventory access and rapid fulfillment capability that direct OEM supply structures are not designed to serve. The expansion of AFP-XS subscription-based systems targeted at SME composite manufacturers, introduced commercially in 2025, is expanding the addressable composite production base in ways that will drive incremental distributor channel demand.

Key Market Segments

By Fiber Type

- Carbon Fibers

- Aramid Fibers

- Glass Fibers

- UHMWPE Fibers

- PBO Fibers

- Others

By End-Use Industry

- Aerospace and Defense

- Automotive and Transportation

- Industrial and Manufacturing

- Construction and Infrastructure

- Electrical and Electronics

- Protective Apparel

- Others

By Form

- Fabric

- Filament Yarn

- Tow

- Staple Fiber

By Distribution Channel

- Direct Sales

- Distributors

Driver Analysis

Wind, hydrogen, and grid decarbonization composites

The acceleration of decarbonization in power and fuels creates a multi-decade driver for high-performance fibers, especially in wind energy, where larger blade designs exceeding 100 meters in length depend on high-modulus glass and carbon fibers to balance stiffness, weight, and fatigue life, and in hydrogen and gas infrastructure, where composite pressure vessels and pipelines demand high-strength reinforcement.

Global decorative coating market sources point toward broader decarbonization trends and urban-heat initiatives, but in high-performance fibers the heavier capital goods side wind turbines, grid reinforcements, carbon capture equipment dominates the volume picture, with each multi-MW turbine incorporating hundreds of kilograms to several tons of advanced fibers, depending on blade design and tower components.

Scaling global wind capacity to meet 2030 and 2035 climate goals requires tens of thousands of new turbines and substantial repowering, while the growth of green hydrogen and compressed-natural-gas infrastructure adds demand for filament-wound tanks and pipes where weight reduction, corrosion resistance, and safety margins justify premium material choices.

For fiber suppliers, this driver encourages vertical collaboration with blade OEMs, tank manufacturers, and epoxy/polyester resin producers, often through joint development agreements that lock in specific fiber/resin combinations, and supports long-term take-or-pay contracts that stabilize revenue; given the long asset life and capex intensity of these applications, the driver’s impact is more long-term, but its magnitude is significant, warranting an estimated +1.7 percentage points of CAGR uplift concentrated in EU, China, the US, and emerging renewable corridors in India and Latin America.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aerospace production ramp and defense procurement | +2.2% | North America core, EU, East Asia | Medium term (2-4 years) |

| Automotive lightweighting and EV platformization | +1.9% | North America, EU, China, Korea | Medium term (2-4 years) |

| Wind, hydrogen, and grid decarbonization composites | +1.7% | EU, China, US, India corridors | Long term (≥ 4 years) |

| Industrial PPE and safety regulations tightening | +1.5% | Global, stronger in APAC, Middle East | Short term (≤ 2 years) |

| Advanced textiles and sports performance adoption | +1.3% | North America, EU, Japan, China | Long term (≥ 4 years) |

| Process innovation and cost-down in fiber manufacturing | +1.1% | Global, with Asia cost hubs | Medium term (2-4 years) |

Restraint Analysis

Energy‑intensive, high CAPEX production

High-performance fiber manufacturing—particularly carbon and aramid fibers remains highly capital- and energy-intensive, with industry commentary underscoring that specialized fibers require energy-heavy processes such as stabilization and carbonization, making power tariffs and capex cycles a structural restraint rather than a cyclical challenge.

A single modern carbon fiber line can demand capex in the tens to low hundreds of millions of dollars, and operating it involves high-temperature furnaces that consume significant electricity and gas, so a 10–20 percent rise in industrial power prices in Europe or parts of Asia can lift cost-per-kilogram by mid–single-digit percentages and erode margins or force price increases that constrain demand in cost-sensitive applications.

At the same time, financing conditions in 2024–2025 tightened as interest rates climbed and lenders scrutinized large industrial projects, meaning that even though multiple market estimates project the high-performance fibers market to roughly double in value over the 2026–2033 horizon, incremental capacity announcements are often phased in smaller tranches, delaying the full realization of demand.

Strategically, this capex and energy intensity restrains CAGR by limiting how fast supply can be added and by biasing investment decisions toward regions with cheaper, more stable energy rather than closer-to-customer plants in Europe or North America, effectively carving off about 2.0 percentage points from the theoretical growth path as projects are sequenced, scaled back, or deferred due to ROI and power-cost concerns.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-intensive, high CAPEX production | -2.0% | EU, North America, East Asia | Long term (≥ 4 years) |

| Volatile PAN, pitch and precursor supply | -1.6% | Asia feedstock hubs, global export lanes | Medium term (2-4 years) |

| Aerospace and defense qualification bottlenecks | -1.5% | North America core, EU, Japan | Medium term (2-4 years) |

| Automotive cost sensitivity and metal competition | -1.4% | North America, EU, China | Short term (≤ 2 years) |

| Regulatory and REACH-type compliance burdens | -1.2% | EU regulatory hubs, global majors | Long term (≥ 4 years) |

| Limited downstream conversion and fabrication capacity | -1.1% | APAC corridors, emerging markets | Medium term (2-4 years) |

Opportunity Analysis

Modular composite kits for mid-tier OEMs

This opportunity represents a pivot from selling raw high-performance fibers or generic fabrics into offering modular composite “kits” and semi-finished parts specifically designed for mid-tier OEMs that currently lack in-house composites expertise, a white space that is not baked into most baseline forecasts that assume continued dominance of large aerospace and auto primes.

By 2035, specialty and high-performance fibers demand is projected to reach millions of tonnes, but a significant portion of that volume remains concentrated in large projects; packaging fibers into standardized kits—such as pre-engineered beams, panels, or enclosure systems with defined mechanical properties—can unlock latent TAM in construction, industrial machinery, agricultural equipment, and mid-volume commercial vehicles where engineering resources and capex are limited.

If, for example, even 10 percent of incremental high-performance fiber volume between 2026 and 2035 were routed through higher-margin kits rather than commodity-like fiber sales, the addressable platform value could increase by several billion dollars, with gross margins expanded by 300–500 basis points due to embedded design, testing, and logistics services.

The business model shift involves building design libraries, certification packages, and plug-and-play documentation, lowering customer acquisition cost per OEM by reusing platforms across clients and sectors; executed over the next 2–4 years, this modular strategy could add around 1.8 percentage points of CAGR upside by enabling mid-tier OEMs in North America, Europe, China, and India to adopt high-performance materials without bearing full engineering or factory-retooling burdens.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Modular composite kits for mid-tier OEMs | +1.8% | North America, EU, China, India | Medium term (2-4 years) |

| Structural health monitoring with fiber-integrated sensing | +1.6% | EU, US, Japan, offshore APAC | Long term (≥ 4 years) |

| Circularity, recycling and secondary markets | +1.5% | EU, North America, East Asia | Long term (≥ 4 years) |

| Defense-grade protection into civilian and infrastructure | +1.4% | North America, EU, Middle East, LatAm | Medium term (2-4 years) |

| High-performance fibers in emerging mobility and logistics (eVTOL, rail, drones) | +1.3% | US, EU, China, GCC, ASEAN | Long term (≥ 4 years) |

| Specialty fiber platforms for hydrogen, CCS and new energy | +1.2% | EU, US, China, Middle East | Long term (≥ 4 years) |

Challenges Analysis

Complex, fragile global supply chains

High-performance fibers rely on globally distributed supply chains spanning PAN and specialty chemical suppliers, energy-intensive fiber plants, and downstream converters, and analyses of market dynamics and specialty fibers emphasize that demand growth to 2035 will require millions of tonnes of specialty and high-performance fibers moving through APAC logistics corridors and transoceanic routes, creating persistent exposure to transport disruptions and lead-time variability rather than outright material unavailability.

Typical lead times for precursor shipments can range from 3–5 weeks within a region to 8–12 weeks for intercontinental flows, and even modest disruptions—port congestion adding 3–5 days, container shortages lifting freight rates by double digits, or temporary export curbs from key chemical-producing countries—translate into higher safety stocks and longer cash-conversion cycles; given that the market value is around 20 billion USD in the mid-2020s, each extra week of average inventory equates to hundreds of millions of dollars tied up in working capital.

Over a 2–4 year horizon, building more resilient networks—through regionalized plants, dual sourcing, and advanced planning systems—can mitigate some friction, but these investments are capital-intensive and require organizational change, so in the meantime, supply-chain fragility continues to impose an estimated drag of about 1.3 percentage points on maximum CAGR, particularly for APAC-centric logistics corridors and globally oriented suppliers.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Composite and fiber skills gap | -1.5% | EU, UK, North America, Japan | Long term (≥ 4 years) |

| Complex, fragile global supply chains | -1.3% | APAC logistics corridors, global trade lanes | Medium term (2-4 years) |

| Product qualification and standards latency | -1.2% | North America core, EU regulatory hubs | Medium term (2-4 years) |

| Digitalization and data integration lag | -1.0% | Global majors, multi-plant networks | Medium term (2-4 years) |

| Demand cyclicality in key end-markets | -1.0% | North America, EU, China, export-driven Asia | Short term (≤ 2 years) |

| ESG reporting and taxonomy complexity | -0.9% | EU, listed multinationals globally | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Active Conflict Theatres Are Directly Reshaping Fiber Demand Structures and Procurement Behavior

The Russia-Ukraine war, now in its fourth year of full-scale operations, has produced a set of battlefield-driven material demand signals that are altering procurement planning for high performance fibers in ways that peacetime planning cycles would never generate. Ukraine’s Ministry of Defence allocated over UAH 44 billion, approximately USD 1.05 billion, specifically for FPV drone procurement in 2025, with a stated priority on fiber-optic guided models that are immune to electronic warfare jamming. This single procurement line represents a structurally new demand category for specialty optical and protective fiber materials generated entirely by active conflict conditions.

By mid-2025, more than 80 Ukrainian-designed fiber-optic drone systems had received military approval, and the Verkhovna Rada passed tax and customs incentive legislation in June 2025 specifically to accelerate domestic fiber-optic drone manufacturing. The commercial consequence is that high-tenacity fiber materials with drone frame and guidance system applications are being pulled into active defense procurement at volumes and timelines that conventional aerospace qualification cycles do not govern, creating a parallel demand channel outside the certification-gated structures that dominate aerospace and legacy defense procurement.

The broader rearmament response to the conflict is producing an equally significant structural shift in European defense procurement budgets that directly conditions fiber demand at the institutional level. According to SIPRI data published in April 2026, European NATO members increased collective defense spending by 20% in 2025, with all 29 members exceeding the 2% of GDP threshold for the first time in recorded NATO history. Germany ordered military equipment worth approximately EUR 85 billion in 2025 alone, and at the 2025 NATO Summit in The Hague, alliance members committed to a 5% of GDP defense spending target by 2035, with at least 3.5% allocated to core defense requirements. France increased its 2026 defense allocation to EUR 68.5 billion under its military programming law.

These commitments translate into multi-year procurement pipelines for armored vehicle composite panels, ballistic protection systems using aramid and UHMWPE fiber, and structural composite components for aircraft and unmanned systems that European fiber producers and their qualified supply chains are now positioned to serve at sustained elevated volumes for the foreseeable future.

Regional Analysis

Asia Pacific Held the Largest Share of the Global High Performance Fiber Market.

Asia Pacific holds 48% of the high performance fiber market because the region contains the majority of global carbon fiber and aramid precursor manufacturing capacity, a substantial and growing composites fabrication base, and national industrial policies in China, Japan, and South Korea that explicitly prioritize advanced materials production as a strategic manufacturing capability. China’s domestic carbon fiber producers, including Zhongfu Shenying and Jiangsu Hengshen, have scaled production capacity with government support while developing increasingly independent supply chains from precursor to finished composite intermediate.

North America is the fastest-growing region because federal industrial policy is directly converting domestic advanced materials manufacturing from a strategic aspiration into a capitalized investment program. The Department of Energy’s Industrial Demonstrations Program, which allocated funding toward hard-to-abate industrial processes including carbon fiber precursor manufacturing under its 2025 award cycles, is co-financing the capital-intensive carbonization and oxidation infrastructure that private producers cannot justify on commercial returns alone at current market pricing.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

High performance fiber manufacturers focus on strengthening technological differentiation, production scale efficiency, and supply chain integration to maintain competitiveness. A key priority is continuous material innovation, including the development of next-generation carbon fiber grades, ceramic-coated aramid constructions, and ultra-high-tenacity UHMWPE variants that improve structural performance, thermal stability, and ballistic protection for advanced aerospace, defense, and industrial applications.

Vertical integration with precursor polymer suppliers and composite fabricators helps secure raw material stability and improve cost control amid volatile acrylonitrile and petrochemical feedstock prices. Strategic capacity expansion, particularly across Asia Pacific and allied Western manufacturing bases, enables alignment with concentrated demand from aerospace production programs, electric vehicle lightweighting requirements, and defense procurement ecosystems.

The Major Players In The Industry

- DuPont de Nemours, Inc.

- Teijin Limited

- Toray Industries, Inc.

- Royal DSM N.V.

- Honeywell International Inc.

- Solvay S.A.

- Hexcel Corporation

- Mitsubishi Chemical Group Corporation

- Owens Corning

- JUSHI Group

- Hyosung Corporation

- Kolon Industries, Inc.

- Toyobo Co., Ltd.

- Kureha Corporation

- PBI Performance Products, Inc.

- AGY Holdings Corp.

- Zhongfu Shenying Carbon Fiber Co., Ltd.

- SGL Carbon SE

- L. Gore & Associates, Inc.

- Axiom Materials, Inc.

- Bally Ribbon Mills

- Sarla Performance Fibers Limited

- ZOLTEK Corporation

- China National Bluestar (Group) Co, Ltd.

- GuangWei Group

- Other Key Players

Key Development

- In April 2026, Arclin completed the acquisition of DuPont’s Aramids business, including the Kevlar and Nomex brands, for approximately 1.8 billion USD on April 1, 2026. The transaction transferred ownership of five manufacturing sites and approximately 1,900 employees to Arclin, a portfolio company of TJC L.P.

- In October 2025, Honeywell’s Board of Directors formally approved the spin-off of Solstice Advanced Materials on October 16, 2025, with the distribution on track for October 30, 2025, which includes Spectra UHMWPE fiber, alongside its refrigerants, semiconductor materials, and data center cooling portfolios.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$17.0 Bn |

| Forecast Revenue (2035) | US$38.7 Bn |

| CAGR (2026-2035) | 8.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Fiber Type (Carbon Fibers, Aramid Fibers, Glass Fibers, UHMWPE Fibers, PBO Fibers, and Others), By End-Use Industry (Aerospace and Defense, Automotive and Transportation, Industrial and Manufacturing, Construction and Infrastructure, Electrical and Electronics, Protective Apparel, and Others), By Form (Fabric, Filament Yarn, Tow, and Staple Fiber), By Distribution Channel (Direct Sales and Distributors) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | DuPont de Nemours, Inc. Teijin Limited Toray Industries, Inc. Royal DSM N.V. Honeywell International Inc. Solvay S.A. Hexcel Corporation Mitsubishi Chemical Group Corporation Owens Corning JUSHI Group Hyosung Corporation Kolon Industries, Inc. Toyobo Co., Ltd. Kureha Corporation PBI Performance Products, Inc. AGY Holdings Corp. Zhongfu Shenying Carbon Fiber Co., Ltd. SGL Carbon SE W. L. Gore & Associates, Inc. Axiom Materials, Inc. Bally Ribbon Mills Sarla Performance Fibers Limited ZOLTEK Corporation China National Bluestar (Group) Co, Ltd. GuangWei Group Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |