Quick Navigation

Report Overview

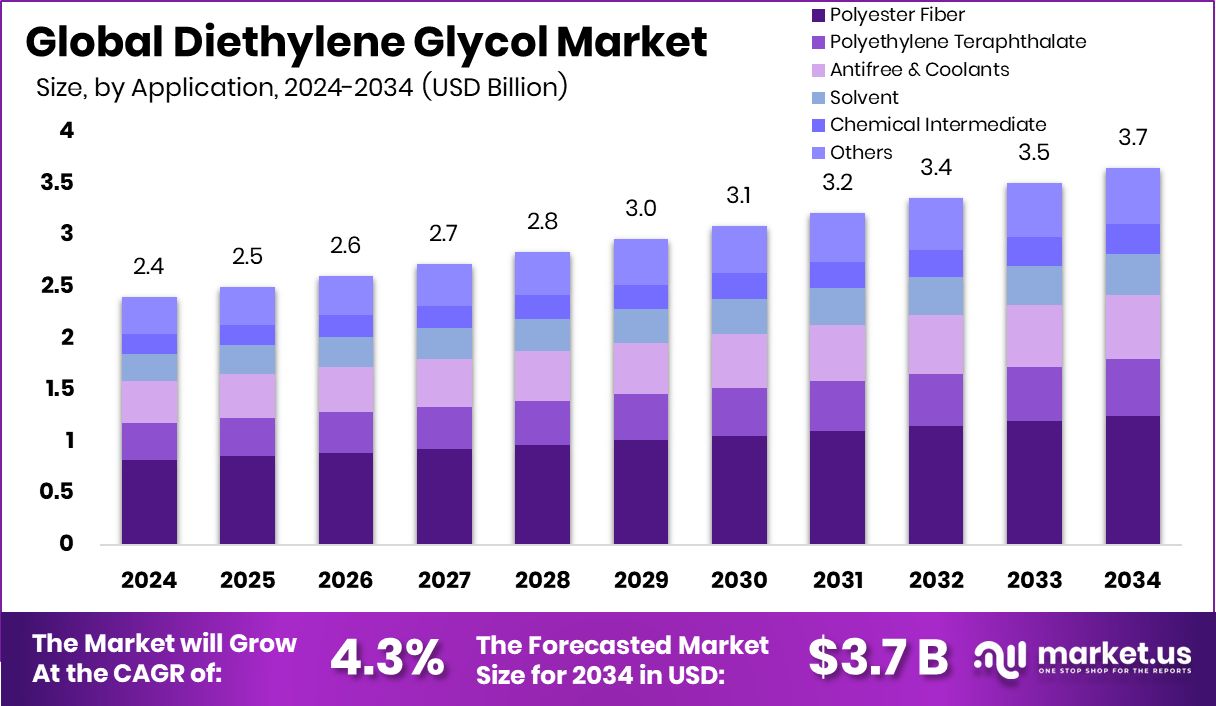

Global Diethylene Glycol Market is expected to be worth around USD 3.7 billion by 2034, up from USD 2.4 billion in 2024, and grow at a CAGR of 4.3% from 2025 to 2034. Diethylene Glycol Market in Asia-Pacific held 48.2% share, dominating global consumption trends.

Diethylene Glycol (DEG) is a colorless, odorless, and hygroscopic organic compound with the chemical formula C₄H₁₀O₃. It is commonly used as a solvent, humectant, plasticizer, and intermediate in the production of resins, polyurethanes, and antifreeze formulations. DEG is miscible with water, alcohols, and many organic solvents, making it a versatile ingredient in industrial and commercial applications.

The Diethylene Glycol market is driven by its wide applicability across industries such as paints and coatings, automotive antifreeze, plastic manufacturing, and textiles. Its demand is primarily fueled by the growing chemical and polymer industries, especially in developing economies. DEG is also used in the production of unsaturated polyester resins, which are essential for reinforced plastics in construction and the marine sectors.

Growth factors include expanding demand from the global textile sector, where DEG serves as a key chemical in fiber production. Additionally, the increase in the manufacture of plasticizers and coolants is significantly contributing to volume growth. Rising industrialization in Asia and steady consumption from the automotive sectors further support long-term expansion.

Demand is also increasing due to the steady use of DEG in industrial brake fluids and lubricants. As manufacturing activities pick up post-pandemic, this base chemical continues to find strong use in processing environments needing stable, reliable intermediates.

Key Takeaways

- Global Diethylene Glycol Market is expected to be worth around USD 3.7 billion by 2034, up from USD 2.4 billion in 2024, and grow at a CAGR of 4.3% from 2025 to 2034.

- In 2024, Polyester Fiber accounted for a 34.2% share in the Diethylene Glycol Market applications.

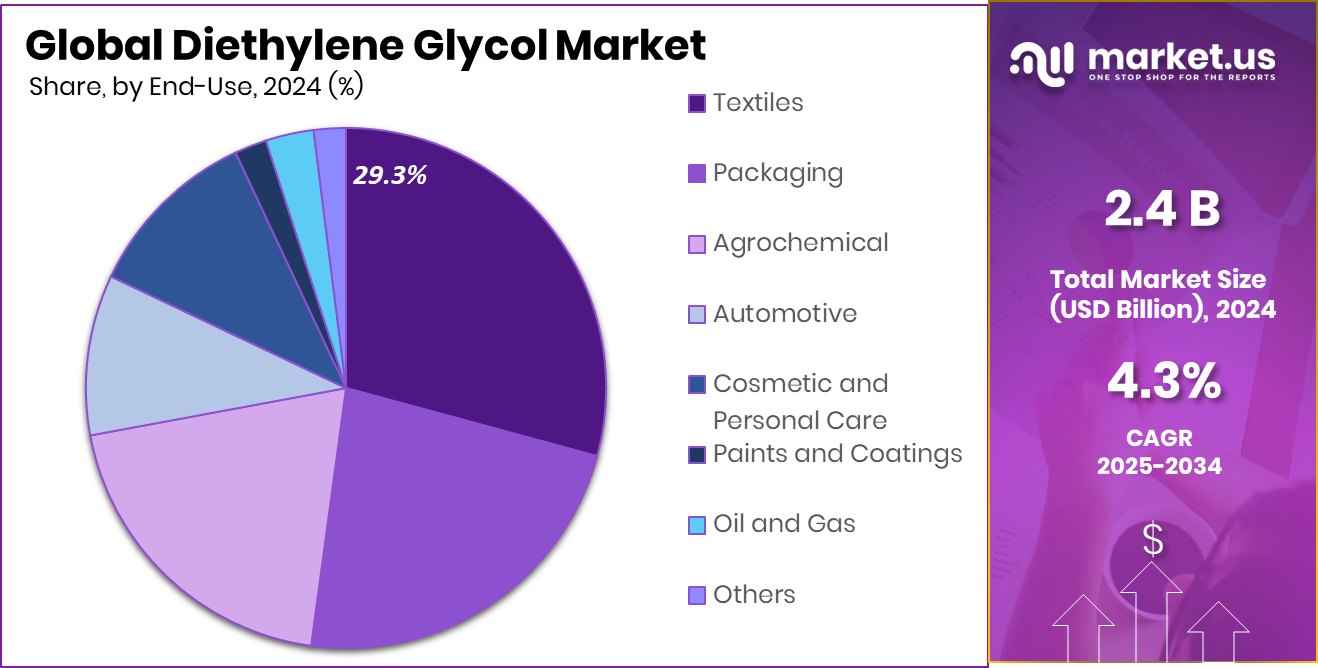

- In 2024, Textiles represented a 29.3% share in the Diethylene Glycol Market by end-use segment.

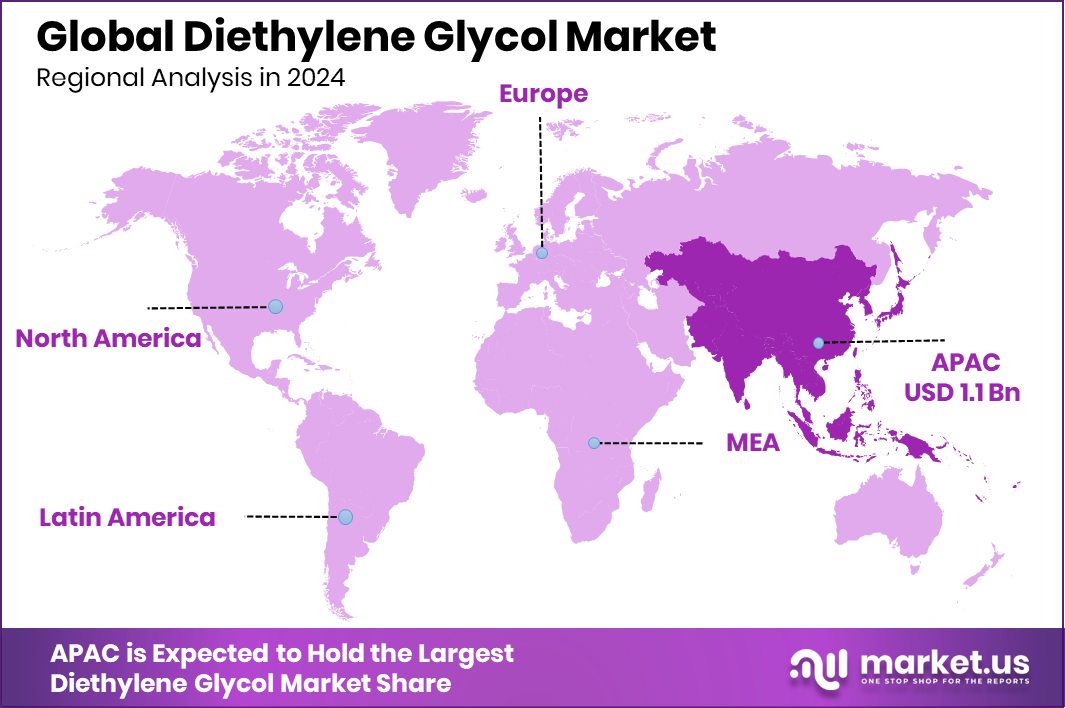

- Rapid industrialization in Asia-Pacific pushed Diethylene Glycol demand to USD 1.1 billion.

By Application Analysis

In 2024, Polyester Fiber accounted for 34.2% of Diethylene Glycol Market applications.

In 2024, Polyester Fiber held a dominant market position in the By Application segment of the Diethylene Glycol Market, with a 34.2% share. This leading share highlights the significant role of Diethylene Glycol (DEG) as a raw material in the production of polyester fibers, which are widely used across the textiles and packaging industries.

The demand for polyester fiber continues to be fueled by its durability, affordability, and versatility, driving consistent consumption of DEG. The rising need for synthetic fibers in developing economies, especially in Asia-Pacific, further supported the strong market position of polyester applications during the year.

Manufacturers prioritized DEG for its excellent properties, such as hygroscopicity and low volatility, which are crucial for producing high-quality polyester fibers. Additionally, the growing fashion industry and expanding middle-class population worldwide boosted textile consumption, indirectly increasing the use of DEG. With sustainability trends pushing for recyclable and synthetic materials, polyester fiber maintained its momentum, thereby cementing DEG’s market demand.

By End-use Analysis

The Textiles sector led end-use demand, holding 29.3% share of the market.

In 2024, Textiles held a dominant market position in the By End-use segment of the Diethylene Glycol Market, with a 29.3% share. This significant share highlights the critical importance of Diethylene Glycol (DEG) in textile manufacturing processes, particularly in the production of polyester-based fabrics.

The growing demand for synthetic textiles, which offer affordability, strength, and wrinkle resistance, contributed heavily to the increased consumption of DEG within this sector. Textile manufacturers relied on DEG for its role in producing fibers that meet modern consumer expectations for both functionality and sustainability.

The textile industry’s expansion across emerging economies, especially in Asia-Pacific and Latin America, further accelerated DEG demand. Rising disposable incomes, urbanization, and changing fashion trends led to higher consumption of ready-to-wear garments, home furnishings, and industrial fabrics, indirectly boosting the need for polyester fibers made using DEG.

Key Market Segments

By Application

- Polyester Fiber

- Polyethylene Teraphthalate

- Antifree and Coolants

- Solvent

- Chemical Intermediate

- Others

By End-use

- Textiles

- Packaging

- Agrochemical

- Automotive

- Cosmetic and Personal Care

- Paints and Coatings

- Oil and Gas

- Others

Driving Factors

Rising Demand for Unsaturated Polyester Resins Globally

One of the biggest driving factors for the Diethylene Glycol (DEG) market is the rising demand for unsaturated polyester resins. These resins are widely used in industries like construction, automotive, and marine for making fiberglass-reinforced plastics. As more buildings, vehicles, and boats are being made around the world, the need for unsaturated polyester resins is growing fast.

Since Diethylene Glycol is a key raw material to produce these resins, its demand is also increasing steadily. Especially in developing countries like India and China, huge investments in construction and infrastructure projects are pushing the market further.

Restraining Factors

Health and Safety Concerns Limit Market Growth

A major restraining factor for the Diethylene Glycol (DEG) market is growing health and safety concerns. DEG is a toxic chemical that can cause serious health issues if swallowed, inhaled, or absorbed through the skin.

In the past, accidental use of DEG in medicines and toothpaste caused major tragedies, leading to strict government rules and safety regulations. Because of these risks, manufacturers must handle and transport DEG very carefully, increasing their overall costs.

Also, many industries are now looking for safer alternative chemicals to avoid legal troubles and health hazards. These safety issues and regulatory pressures are expected to slow down the growth of the Diethylene Glycol market, especially in sensitive industries like food, pharmaceuticals, and cosmetics.

Growth Opportunity

Expanding Use of Diethylene Glycol in Paints

A big growth opportunity for the Diethylene Glycol (DEG) market is its expanding use in paints and coatings. DEG works as a solvent in water-based paints, helping them dry evenly and smoothly.

With the construction industry booming worldwide, the demand for paints and coatings is rising fast for houses, offices, and large buildings. Also, customers are preferring high-quality finishes and durable paints, where DEG plays an important role.

Environmental rules are also encouraging the shift toward water-based, low-odor paints, which need DEG. As both developing and developed countries focus more on construction and renovation, the need for paints is growing, which will naturally boost the demand for Diethylene Glycol in the coming years.

Latest Trends

Shift Towards Eco-Friendly Diethylene Glycol Alternatives

A key trend in the Diethylene Glycol (DEG) market is the growing shift towards eco-friendly alternatives. Industries are increasingly seeking sustainable and less toxic options due to environmental concerns and stricter regulations.

This trend is particularly evident in sectors like paints, coatings, and personal care, where consumers demand safer, greener products. As a result, manufacturers are investing in research and development to create bio-based and biodegradable substitutes for DEG.

This movement not only addresses environmental issues but also opens new market opportunities for innovative, sustainable solutions. Companies that adapt to this trend by offering eco-friendly alternatives are likely to gain a competitive edge and meet the evolving preferences of environmentally conscious consumers.

Regional Analysis

Asia-Pacific led Diethylene Glycol Market in 2024 with a 48.2% share, worth USD 1.1 billion.

In 2024, the Asia-Pacific region held a dominant position in the global Diethylene Glycol market, accounting for 48.2% of the total market share, valued at USD 1.1 billion. The region’s strong presence is mainly driven by rapid industrialization, expanding construction activities, and a robust textile and plastic manufacturing base across major economies like China and India.

Demand for unsaturated polyester resins and flexible packaging is also contributing to this growth. In contrast, North America and Europe represent mature markets with moderate growth, supported by demand from the paints, coatings, and automotive industries. The Middle East & Africa region is witnessing steady progress due to expanding construction sectors and infrastructural development.

Latin America shows emerging potential, especially in consumer goods and industrial applications, but remains smaller in comparison. The dominance of Asia-Pacific highlights its central role in global DEG production and consumption, with increasing capacity additions and raw material availability supporting its lead.

Other regions are likely to see gradual growth, but the Asia-Pacific region is expected to remain the key revenue-generating hub for Diethylene Glycol over the coming years due to favorable economic activity and ongoing industrial investments.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, INEOS remained a pivotal player in the global Diethylene Glycol (DEG) market, leveraging its strong presence in petrochemicals and consistent backward integration. With its extensive manufacturing infrastructure across Europe and North America, the company effectively sustained stable DEG output to meet regional demand spikes.

INEOS’s commitment to operational efficiency and vertical integration allowed it to mitigate raw material price fluctuations, offering competitive pricing in key downstream markets like polyester resins and antifreeze products.

Orlen S.A., a major Central European refining and petrochemical group, actively contributed to DEG supply through its robust glycol production lines. In 2024, Orlen capitalized on increased DEG consumption in Eastern Europe’s polyester fiber and construction chemical industries. The company’s strategic refining capacity expansions in Poland enhanced DEG output while minimizing feedstock dependency, positioning Orlen as a reliable regional supplier.

BASF SE, one of the world’s leading chemical producers, retained a strong DEG portfolio supported by its global value chain. In 2024, the company emphasized supply stability across its integrated Verbund production sites, particularly in Ludwigshafen and Antwerp.

BASF’s DEG production was closely tied to its ethylene oxide capacities, allowing precise control over output volumes amid varying demand. The company also invested in digitalization across logistics and process optimization, streamlining DEG delivery to sectors such as flexible packaging and automotive coolants.

Top Key Players in the Market

- INEOS

- Orlen S.A.

- BASF SE

- Shell plc

- SABIC

- Mitsubishi Chemical Corporation

- MEGlobal

- LyondellBasell Industries Holdings B.V.

- EQUATE

- KİMPUR

- Reliance Industries Limited

- INEOS

- PTT Global Chemical Public Company Limited

- Nan Ya Plastics Corporation

- Hengli Group Co., Ltd.

- Other Key Players

Recent Developments

- In March 2025, LyondellBasell announced an investment to expand propylene production capacity at its Channelview Complex near Houston. The new unit will have an annual capacity of approximately 400,000 metric tons. Propylene is a building block for various chemicals, and this expansion may influence the production of related derivatives, potentially impacting Diethylene Glycol markets.

- In January 2025, Mitsubishi Chemical partnered with Mitsui Chemicals to initiate a joint study aimed at ensuring a stable supply of phenol-related products. This collaboration focuses on products like phenol, acetone, and bisphenol A, which are essential in various industries.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 2.4 Billion |

| Forecast Revenue (2034) | USD 3.7 Billion |

| CAGR (2025-2034) | 4.3% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Application (Polyester Fiber, Polyethylene Teraphthalate, Antifree and Coolants, Solvent, Chemical Intermediate, Others), By End-use (Textiles, Packaging, Agrochemical, Automotive, Cosmetic and Personal Care, Paints and Coatings, Oil and Gas, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | INEOS, Orlen S.A., BASF SE, Shell plc, SABIC, Mitsubishi Chemical Corporation, MEGlobal, LyondellBasell Industries Holdings B.V., EQUATE, KİMPUR, Reliance Industries Limited, INEOS, PTT Global Chemical Public Company Limited, Nan Ya Plastics Corporation, Hengli Group Co., Ltd., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |