Quick Navigation

Report Overview

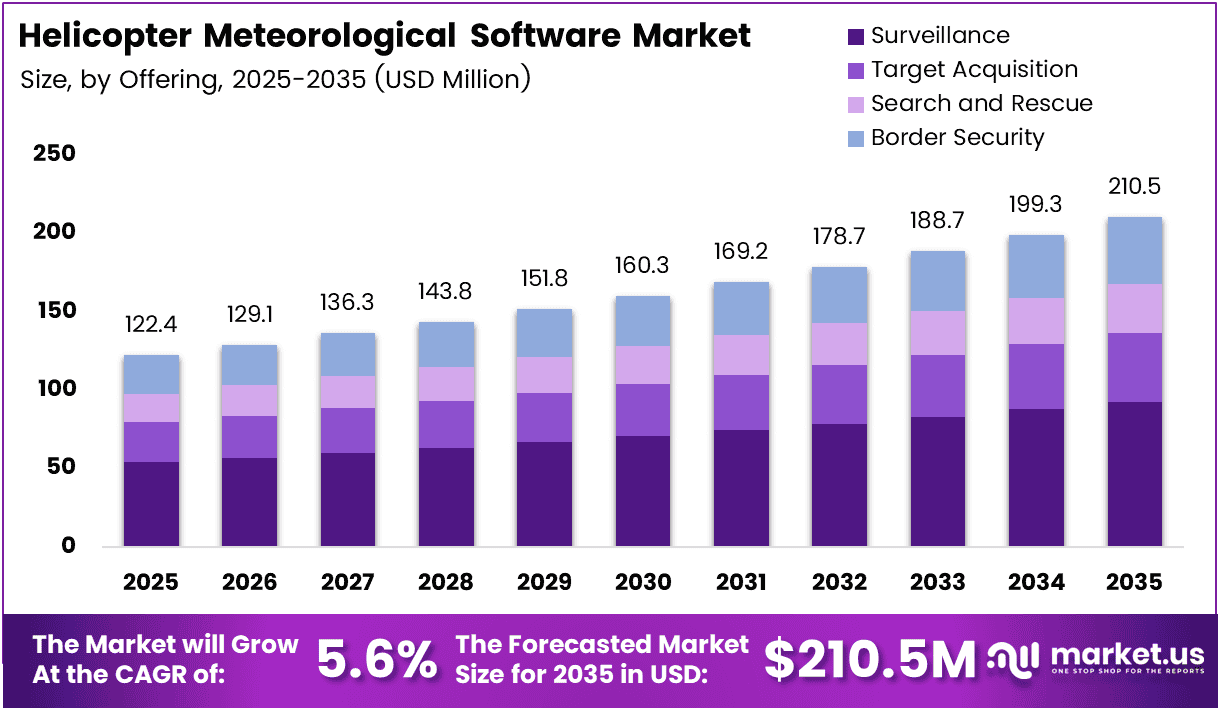

Global Helicopter Meteorological Software Market size is expected to be worth around USD 210.5 Million by 2035 from USD 122.4 Million in 2025, growing at a CAGR of 5.6% during the forecast period 2026 to 2035.

Helicopter meteorological software covers the full stack of tools pilots and operators use to access, interpret, and act on weather data during flight planning and in-cockpit operations. This includes electronic flight display systems, application-based platforms, and mobile weather tools purpose-built for low-altitude and rotary-wing missions.

The market draws its commercial foundation from three structural realities: helicopters operate at altitudes where hyperlocal weather conditions change faster than fixed-wing aircraft face, mission stakes in emergency medical and search-and-rescue contexts leave no margin for weather error, and cockpit digitization across both civil and defense fleets continues to replace paper-based preflight processes.

Defense and emergency services agencies worldwide are expanding helicopter fleet size to meet disaster response, border patrol, and offshore logistics demands. Each new airframe entering service represents a direct software procurement event — creating a compounding adoption curve that sustains market growth well beyond current forecasts.

Oil and gas operators running offshore helicopter logistics face mandatory weather compliance windows before each flight. This regulatory context converts meteorological software from a convenience tool into an operational requirement, concentrating purchasing power among a relatively small number of well-funded operators who renew contracts predictably.

Government investment in weather infrastructure directly strengthens the commercial software layer built on top of it. According to the FAA, its Alaska weather camera program produced an 85% reduction in weather-related accidents and a 69% reduction in weather-related flight interruptions between 2007 and 2014. These figures confirm that better weather data infrastructure translates into measurable safety outcomes — making the case for software investment self-funding through liability and operational cost reduction.

According to the FAA, as of March 2026, it operates 299 weather camera sites across airports, mountain passes, and coastal areas in Alaska, Hawaii, and 30 continental U.S. states — each updating every 10 minutes. This near real-time data density raises the floor for what helicopter operators now expect from their meteorological software, and vendors unable to ingest and display this data at equivalent refresh rates face a product-gap risk.

Key Takeaways

- The global Helicopter Meteorological Software Market was valued at USD 122.4 Million in 2025.

- The market is forecast to reach USD 210.5 Million by 2035, at a CAGR of 5.6% from 2026 to 2035.

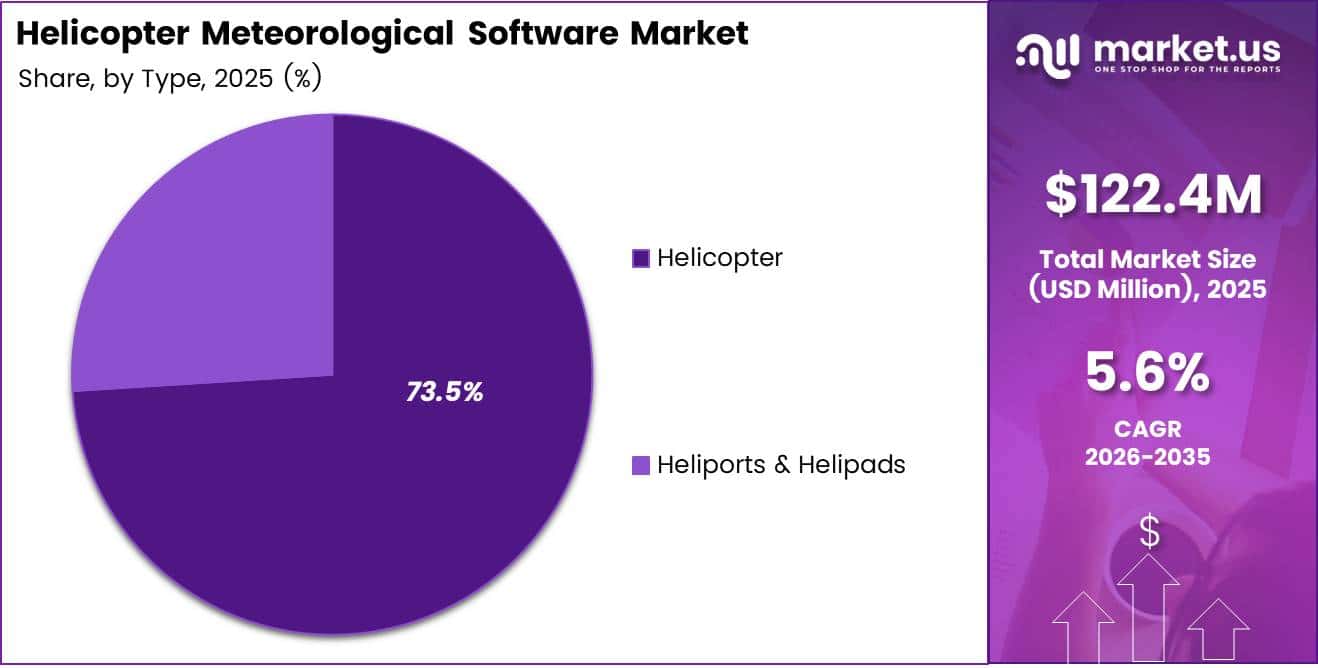

- By Type, Helicopter leads with a 73.5% share, reflecting concentrated demand from rotary-wing operators.

- By Offering, Electronic Flight Display (EFD) Software holds the largest share at 36.8%.

- By Application, Emergency Medical Services is the dominant use case with a 31.7% share.

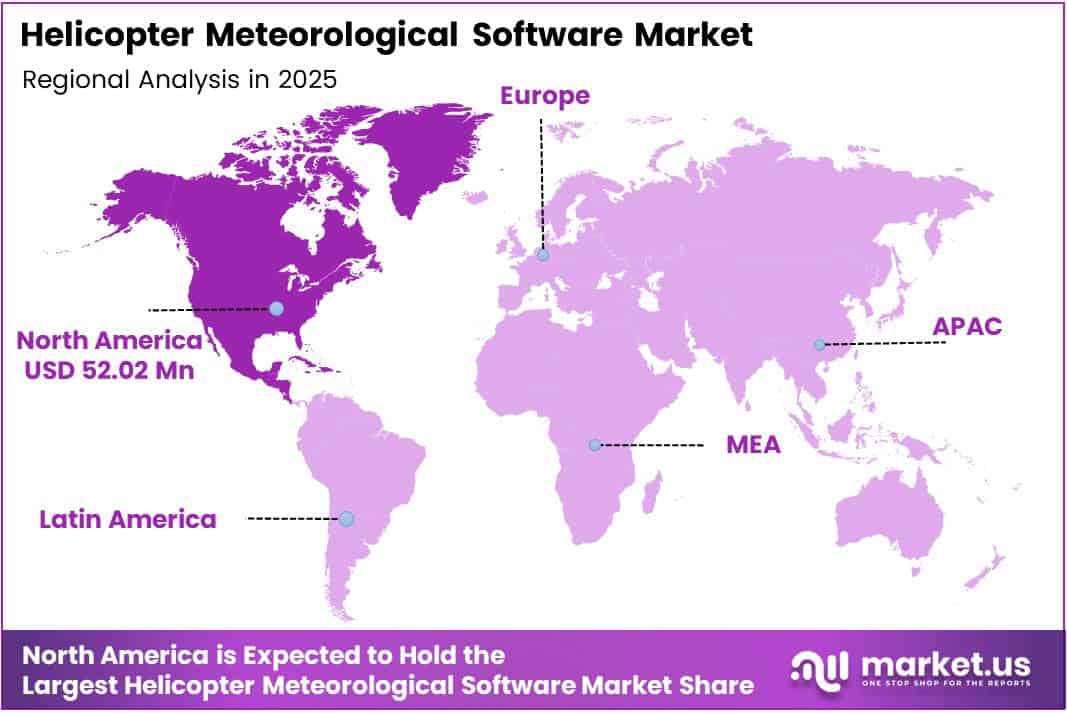

- North America leads all regions with a 42.50% share, valued at USD 52.02 Million.

Type Analysis

Helicopter dominates with 73.5% due to concentrated rotary-wing operational demand.

In 2025, Helicopter held a dominant market position in the By Type segment of the Helicopter Meteorological Software Market, with a 73.5% share. Rotary-wing aircraft require hyperlocal, low-altitude weather data that fixed-wing systems do not provide — making dedicated meteorological software a mission-critical procurement rather than an optional upgrade for helicopter operators.

Heliports and Helipads serve as the ground infrastructure layer where weather data informs clearance decisions, approach planning, and emergency response logistics. Demand from this sub-segment reflects the build-out of urban air mobility infrastructure and the expansion of offshore platform landing facilities, both of which require site-specific meteorological monitoring to support safe rotary operations.

Offering Analysis

Electronic Flight Display (EFD) Software dominates with 36.8% due to deep cockpit integration and regulatory mandates.

In 2025, Electronic Flight Display (EFD) Software held a dominant market position in the By Offering segment of the Helicopter Meteorological Software Market, with a 36.8% share. EFD platforms embed weather data directly into primary flight instruments, meaning pilots access meteorological information without breaking scan — a workflow advantage that regulators and fleet operators now treat as a baseline safety requirement.

Application-Based Software differentiates through deployment flexibility and lower upfront cost, making it the preferred entry point for smaller operators, charter services, and individual pilots. Its growth reflects a broader shift in aviation tools toward subscription-based commercial models, where operators access weather data through connected devices rather than proprietary avionics hardware.

PC and Desktop Software carries the highest adoption among dispatch centers, flight operations control rooms, and training environments where screen real estate and multi-source data overlays matter more than portability. Enterprise procurement teams in oil and gas and corporate aviation tend to standardize on desktop platforms for pre-mission planning workflows.

Mobile Software serves as the fastest-evolving sub-segment, driven by increasing smartphone and tablet penetration in cockpits and the FAA’s progressive acceptance of electronic flight bag solutions as primary weather reference tools. Vendors that deliver offline-capable, low-bandwidth mobile applications hold a structural edge in offshore and remote operation markets where connectivity is inconsistent.

Application Analysis

Emergency Medical Services dominates with 31.7% due to zero-tolerance weather risk in time-critical missions.

In 2025, Emergency Medical Services held a dominant market position in the By Application segment of the Helicopter Meteorological Software Market, with a 31.7% share. EMS operators face both regulatory and institutional pressure to use certified weather decision tools, as weather-related EMS helicopter accidents carry significant liability and patient-outcome consequences that make software procurement a compliance-driven purchase.

Corporate Services represents a structurally attractive sub-segment because corporate flight departments operate to executive-level service standards that treat weather-related delays as operational failures. This buyer profile consistently upgrades to premium meteorological software products, creating above-average revenue per seat for vendors serving this segment.

Search and Rescue operations demand meteorological software that performs under degraded communication conditions and provides predictive weather modeling rather than only current conditions. Military and coast guard operators in this segment influence procurement decisions for entire national fleets, making a single contract win disproportionately valuable for vendors with certified defense-grade products.

Oil and Gas helicopter operations run on mandatory weather compliance windows, with offshore platform operators required to document meteorological data for every flight in the logbook. This regulatory structure converts meteorological software into a recurring operating cost rather than a capital investment, providing vendors with predictable contract renewal cycles and stable revenue.

Homeland Security agencies use helicopter meteorological tools in border patrol, disaster response staging, and counter-narcotics operations where mission success depends on weather-window exploitation. Procurement in this segment follows government contract cycles, which introduces longer sales timelines but provides multi-year revenue certainty once awards are secured.

Transportation helicopter operators, including inter-island, hospital transfer, and urban shuttle services, require meteorological software that integrates with route optimization and air traffic management systems. As urban air mobility corridors develop, this sub-segment will expand to include new operator categories currently outside the traditional helicopter market.

Others within the application landscape include agricultural, film production, and utility inspection operations — niche but consistent buyers who procure meteorological tools based on operational risk rather than regulatory mandate. These operators tend to favor mobile and application-based solutions over full cockpit EFD integrations.

Key Market Segments

By Type

- Helicopter

- Heliports & Helipads

By Offering

- Electronic Flight Display (EFD) Software

- Application-Based Software

- PC & Desktop Software

- Mobile Software

By Application

- Emergency Medical Services

- Corporate Services

- Search & Rescue

- Oil & Gas

- Homeland Security

- Transportation

- Others

Drivers

Real-Time Weather Mandates and Aviation Safety Infrastructure Push Adoption of Dedicated Helicopter Meteorological Tools

Aviation safety regulators and fleet operators treat weather awareness as the primary risk variable in helicopter operations. Helicopters fly at low altitudes where terrain, fog, and wind shear create conditions that fixed-wing weather systems do not model accurately — forcing operators to invest in meteorological software purpose-built for rotary-wing flight profiles and route structures.

Defense agencies and emergency services fleets have expanded helicopter operations across disaster response, border patrol, and military logistics roles where mission abort due to weather failure carries both operational and reputational consequences. This institutional pressure converts meteorological software from an optional add-on into a mandated procurement line item within government fleet budgets, creating a durable, non-cyclical revenue base for vendors.

According to the FAA, it plans to add 64 new weather camera sites in Alaska by end of 2028 and 160 additional FAA-operated sites by 2031 under the Brand New Air Traffic Control System initiative. In February 2026, Honeywell expanded its IntuVue RDR-7000 3D weather radar technology into a ground-based weather detection application for heliports. These parallel investments signal that infrastructure and software vendors are aligning around the same data density and refresh-rate standards — raising the competitive floor across the market.

Restraints

High Integration Costs and Multi-Source Data Reliability Gaps Limit Market Penetration Among Smaller Operators

Specialized helicopter meteorological software requires deep integration with avionics hardware, flight management systems, and external weather data feeds — a technical stack that carries substantial development and certification costs. These upfront barriers favor large fleet operators and well-funded agencies while keeping independent charter operators and small rotary-wing businesses on legacy or generic tools.

The software’s operational value depends entirely on the accuracy and consistency of the underlying weather data it processes. Helicopter operators in remote regions — offshore platforms, mountain rescue zones, and Arctic routes — face environments where data feeds from satellites, ground stations, and radar networks are intermittent or conflicting, reducing the software’s reliability precisely where it matters most.

When meteorological data from multiple sources disagrees, pilots face a decision-making burden that increases cognitive load at high-stress moments. This reliability gap creates institutional hesitancy among operators who have experienced data-driven near-misses, slowing re-procurement cycles and increasing vendor scrutiny during contract renewals — a dynamic that extends average sales timelines and compresses margins for vendors competing on data quality claims.

Growth Factors

AI-Driven Predictive Weather Analytics and Offshore Expansion Open New Revenue Streams for Meteorological Software Vendors

Artificial intelligence applied to aviation weather forecasting shifts the product category from reactive display tools to predictive decision engines. Vendors that can deliver route-specific weather probability models, flight-window optimization, and auto-generated go/no-go advisories will command premium pricing from operators who currently rely on pilot judgment to interpret raw data — effectively monetizing analytical capability rather than just data access.

Offshore oil and gas helicopter operations face strict regulatory weather windows, and expanded deepwater exploration in the North Sea, Gulf of Mexico, and Southeast Asian waters creates new platform infrastructure that requires meteorological software at every landing site. According to the FAA, 60 new Visual Weather Observation System (VWOS) sites combining 360-degree pan-tilt-zoom cameras with full AWOS/ASOS sensor suites are planned by end of 2028 for remote airports and helicopter landing areas — directly expanding the addressable infrastructure that vendor software must integrate with.

Search and rescue mission growth, driven by climate-related disaster frequency and expanded coastal patrol mandates, creates a procurement segment where meteorological accuracy directly determines mission success rates. Cloud-based aviation weather platforms reduce per-seat software costs while enabling real-time data sharing across multi-agency rescue operations — making adoption viable for agencies that previously could not justify dedicated system expenditures.

Emerging Trends

Satellite Weather Integration and Mobile-First Design Redefine the Cockpit Weather Experience for Helicopter Operators

Real-time data visualization platforms now consolidate satellite imagery, radar feeds, METAR data, and pilot weather reports into a single cockpit display layer — replacing the multi-app workflow that previously forced pilots to reconcile conflicting data sources manually. Vendors delivering unified decision support interfaces gain adoption advantage as operators standardize on fewer, more capable tools per airframe.

Satellite weather data integration expands coverage to oceanic, polar, and mountainous routes where ground-based radar networks provide incomplete or delayed information. For helicopter operators in offshore energy, Arctic logistics, and high-altitude rescue, satellite-sourced meteorological feeds are not a premium feature — they are the baseline requirement for legal compliance and operational viability, making this capability a market-entry threshold rather than a differentiator.

Mobile and portable aviation weather applications have advanced to the point where tablet-based solutions now replicate desktop pre-mission planning functionality. This shift reduces hardware procurement barriers for smaller operators and accelerates onboarding timelines — but it also compresses average revenue per user as app-store pricing displaces avionics-integrated software contracts. Vendors must decide whether to compete on accessibility or defend premium positioning through deeper data integration and certification credentials.

Regional Analysis

North America Dominates the Helicopter Meteorological Software Market with a Market Share of 42.50%, Valued at USD 52.02 Million

North America leads with a 42.50% share valued at USD 52.02 Million, driven by the FAA’s extensive weather infrastructure investment, the U.S. military’s large rotary-wing fleet, and a mature offshore oil and gas sector that mandates meteorological compliance on every flight. These structural factors create a self-reinforcing procurement environment that competitors in other regions are still building toward.

Europe Helicopter Meteorological Software Market Trends

Europe holds a strong secondary position underpinned by North Sea offshore helicopter operations, NATO defense fleet modernization, and stringent EASA weather data requirements for EMS and SAR operators. Germany, the UK, and Norway concentrate the majority of demand, and the region’s focus on digital cockpit upgrades across aging helicopter fleets sustains replacement-cycle procurement activity.

Asia Pacific Helicopter Meteorological Software Market Trends

Asia Pacific presents the broadest structural expansion opportunity, as China, India, and Southeast Asian nations scale up both military helicopter fleets and civilian EMS networks in parallel. Infrastructure investment in offshore energy exploration across the South China Sea and Bay of Bengal adds a regulatory-compliance procurement layer that accelerates software adoption beyond discretionary upgrade timelines.

Middle East and Africa Helicopter Meteorological Software Market Trends

Middle East and Africa demand concentrates in GCC offshore energy logistics and South African mining operations, where helicopter weather planning tools support remote-site access under harsh environmental conditions. Gulf state sovereign wealth investment in aviation infrastructure and defense modernization sustains procurement budgets even through commodity price cycles.

Latin America Helicopter Meteorological Software Market Trends

Latin America’s meteorological software adoption centers on Brazilian offshore oil operations managed by Petrobras and its contractors, where weather compliance requirements mirror North Sea standards. Mexico’s federal security helicopter fleet and Andean search-and-rescue operations in Colombia and Peru represent additional government-funded procurement channels with multi-year contract structures.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Honeywell International Inc occupies a structurally advantaged position in this market by combining avionics hardware and meteorological software within a single product architecture. Its IntuVue RDR-7000 platform, recently extended into ground-based weather detection for heliports, means Honeywell captures revenue at both the airframe and the landing site — a dual-channel model that pure-play software vendors cannot replicate without hardware partnerships.

Vaisala Oyj competes on the strength of its proprietary weather sensor network and decades of data infrastructure investment, giving its aviation weather products a data quality credential that software-only competitors must source from third parties. In helicopter meteorological applications, this upstream data advantage translates into lower latency and higher accuracy at the hyperlocal measurement level — the exact performance dimension that EMS and SAR operators prioritize in procurement evaluations.

DTN LLC positions itself as the data integration layer for aviation weather workflows, aggregating multi-source feeds — government METAR networks, commercial satellite providers, and proprietary observational data — into a single normalized platform. This aggregation model makes DTN a natural integration partner for avionics manufacturers and EFD software vendors, giving it a B2B channel advantage that reduces direct sales dependency and accelerates market penetration across operator categories.

All Weather Inc focuses on automated weather observation systems for airports and helipad environments, establishing itself as the infrastructure vendor whose data outputs feed upstream meteorological software platforms. Its strategic positioning at the sensor layer means that software vendors building cockpit weather tools effectively depend on All Weather hardware accuracy — creating a structural upstream leverage point that the company can convert into preferred data-partnership agreements.

Key Players

- Honeywell International Inc

- Vaisala Oyj

- DTN LLC

- All Weather Inc

- Automasjon and Data AS

- Campbell Scientific Inc

- KONGSBERG Gruppen ASA

- InControl AS

- ForeFlight LLC

- HELI EFB GmbH

- EUROAVIONICS GmbH

Recent Developments

- October 2025 — Garmin introduced enhanced weather tools to its Pilot Web flight planning platform, adding future radar and storm top overlays. This update directly improves preflight weather awareness for helicopter operators, raising the standard for what pilots expect from web-based planning tools across the market.

- October 2024 — DARPA awarded Sikorsky a $6 million contract for integrating an autonomous flight system onto the Army’s UH-60M Black Hawk helicopter. The program expands AI-driven operations and autonomous weather-aware flight capabilities, signaling that defense procurement will increasingly demand software platforms capable of machine-readable meteorological data inputs.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 122.4 Million |

| Forecast Revenue (2035) | USD 210.5 Million |

| CAGR (2026-2035) | 5.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Helicopter, Heliports & Helipads), By Offering (Electronic Flight Display (EFD) Software, Application-Based Software, PC & Desktop Software, Mobile Software), By Application (Emergency Medical Services, Corporate Services, Search & Rescue, Oil & Gas, Homeland Security, Transportation, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Honeywell International Inc, Vaisala Oyj, DTN LLC, All Weather Inc, Automasjon and Data AS, Campbell Scientific Inc, KONGSBERG Gruppen ASA, InControl AS, ForeFlight LLC, HELI EFB GmbH, EUROAVIONICS GmbH |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |