Quick Navigation

Report Overview

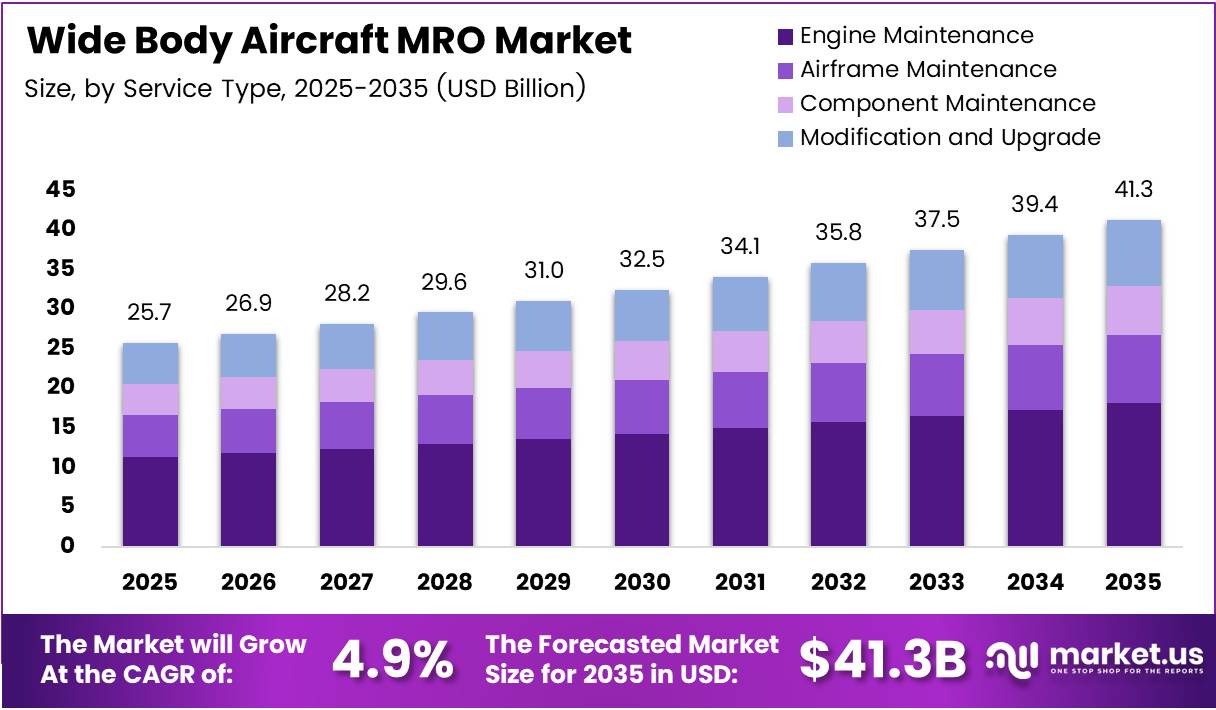

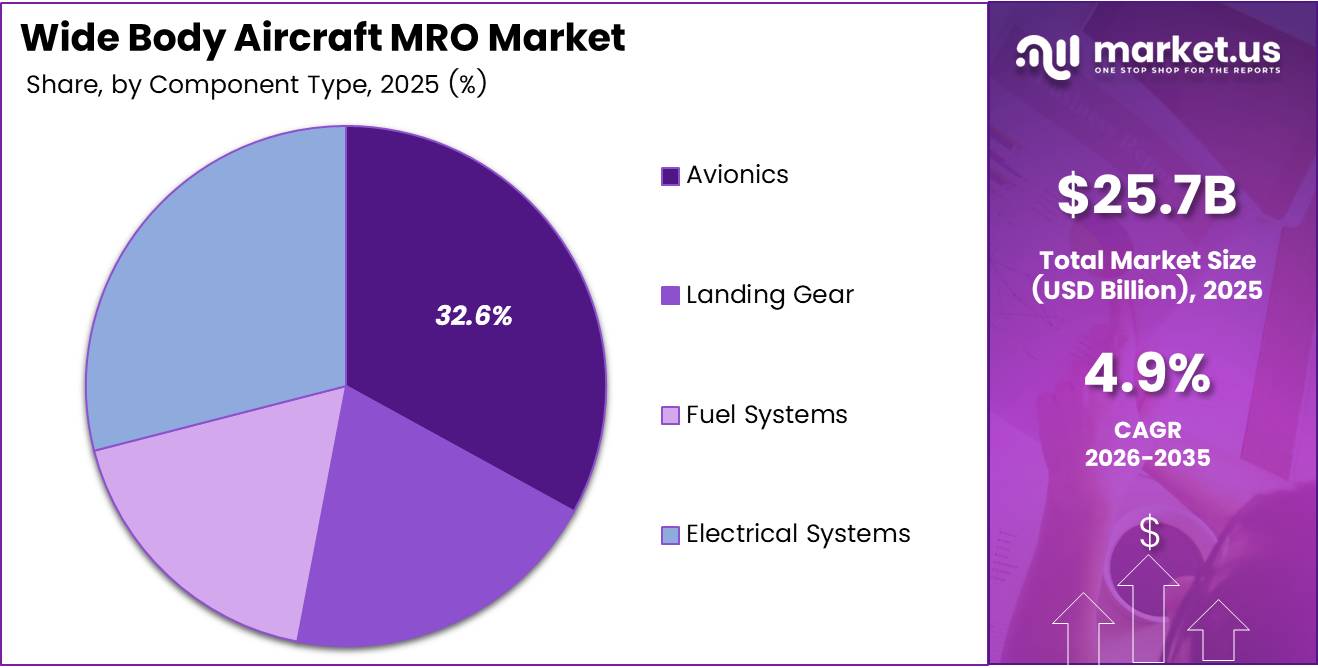

Global Wide Body Aircraft MRO Market size is expected to be worth around USD 41.3 Billion by 2035 from USD 25.7 Billion in 2025, growing at a CAGR of 4.9% during the forecast period 2026 to 2035.

Wide body aircraft maintenance, repair, and overhaul covers the full spectrum of technical services required to keep twin-aisle aircraft airworthy across commercial, cargo, and military operations. These services span engine overhaul, airframe checks, avionics upgrades, and component-level repairs. The complexity of these platforms makes MRO a non-discretionary spend for every operator.

The market operates under strict regulatory mandates from aviation authorities worldwide, including the FAA and EASA. Airlines cannot defer maintenance events beyond prescribed flight-hour or calendar-based thresholds. This regulatory structure creates a predictable, recurring revenue base for qualified MRO providers — making the sector structurally more resilient than most aviation service businesses.

Long-haul route expansion across Asia Pacific and the Middle East continues to add twin-aisle aircraft to global fleets. As newer Boeing 787 and Airbus A350 deliveries accumulate flight hours, their first heavy maintenance cycles approach — creating a measurable pipeline of scheduled MRO work that providers can plan capacity around years in advance.

Fleet aging among legacy widebody types such as the Boeing 747-400 and older 777 variants compounds base MRO volume. Older airframes require more frequent and deeper checks, and command higher labor and parts costs per event. Operators flying mixed fleets of old and new-generation widebodies face structurally higher MRO spend per available seat kilometer.

In May 2025, Supraero and Aero Equipement merged to form SuprAero Equipement, combining component distribution with MRO technical support and supply chain management. This consolidation signals that mid-market MRO suppliers recognize scale as a competitive necessity — a pattern that tends to accelerate market restructuring and compress margins for smaller independent providers.

According to Aviation Titans, wide-body D-Check costs range from USD 5 to 10 million per event, with total lifecycle maintenance averaging USD 1,500–2,500 per flight hour. These figures confirm that MRO is not a discretionary line item — it is a capital-intensive obligation that forces airlines to engage long-term contracts with qualified providers, anchoring revenue visibility across the forecast period.

According to Aviation Titans, the US MRO market exceeds USD 20 billion annually, with US facilities handling 25–30% of work from foreign airlines. This cross-border demand reflects the capacity and speed advantage of US MRO facilities, which complete D-Checks 10–15% faster than international competitors — a structural cost advantage that draws international operators and reinforces North America’s position as the market’s leading region.

Key Takeaways

- The Global Wide Body Aircraft MRO Market was valued at USD 25.7 Billion in 2025 and is forecast to reach USD 41.3 Billion by 2035.

- The market advances at a CAGR of 4.9% from 2026 to 2035.

- By Service Type, Engine Maintenance leads with a 43.4% share.

- By Component Type, Avionics holds the dominant position at 32.6% share.

- By Maintenance Type, Heavy Maintenance commands 48.1% of the segment.

- By End User, Commercial Operators account for 67.3% of market demand.

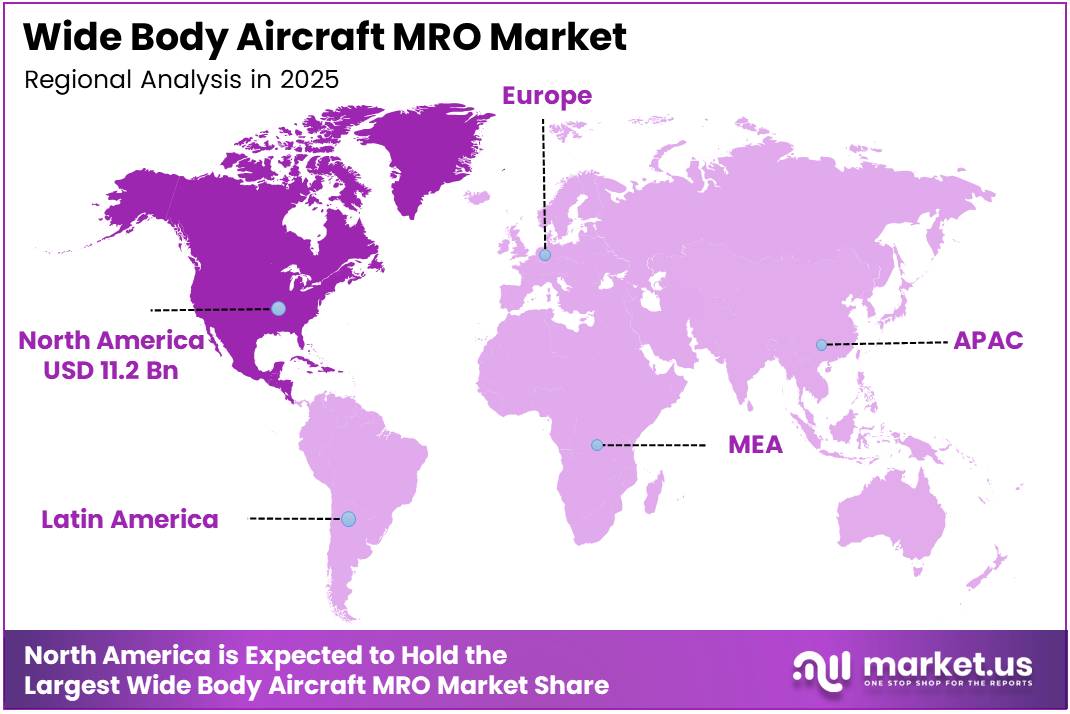

- North America dominates the regional landscape with a 43.70% share, valued at USD 11.2 Billion.

Product Analysis

Engine Maintenance dominates with 43.4% due to high overhaul cost and regulatory frequency.

In 2025, Engine Maintenance held a dominant market position in the By Service Type segment of the Wide Body Aircraft MRO Market, with a 43.4% share. Wide body engines such as the GE90, Trent 1000, and GEnx require shop visits every 5,000–8,000 flight hours. Each overhaul event costs millions of dollars, making engine work the single largest cost center in any airline’s MRO budget.

Airframe Maintenance represents the structural backbone of scheduled compliance checks for widebody fleets. C-Checks and D-Checks require extensive labor input and drive significant demand for certified hangar capacity. As aging widebody fleets accumulate calendar time, airframe checks become more frequent and more intensive, supporting sustained revenue for large-format MRO facilities.

Component Maintenance differentiates through its role in reducing aircraft-on-ground exposure for operators. Airlines increasingly exchange components on a pool basis rather than wait for individual repair turnarounds. This shift toward component pooling compresses lead times but requires MRO providers to invest in larger rotable inventories — raising barriers to entry for smaller players.

Modification and Upgrade services carry the highest revenue-per-event potential within the service type segment. Cabin reconfiguration, avionics upgrades, and fuel system retrofits are driven by airline network strategy changes and regulatory mandates. However, modification work is episodic — not recurrent — making it a high-margin but unpredictable revenue line for MRO providers.

Component Analysis

Avionics dominates with 32.6% due to mandatory upgrade cycles and digital integration requirements.

In 2025, Avionics held a dominant market position in the By Component Type segment of the Wide Body Aircraft MRO Market, with a 32.6% share. Regulatory mandates for ADS-B compliance, FANS communication systems, and ACAS upgrades force airlines to replace avionics hardware on fixed schedules. This compliance-driven cycle gives avionics MRO providers a structurally predictable workload independent of fleet age.

Landing Gear overhaul sits among the most technically demanding and infrequent component events in the widebody MRO cycle. Overhaul intervals span 10 to 12 years, but the precision engineering involved in each event — combined with strict FAA and EASA approval requirements — limits the number of qualified shops globally. This scarcity of certified capacity gives specialized landing gear MRO providers strong pricing power.

Fuel Systems maintenance links directly to aircraft fuel efficiency performance and regulatory airworthiness directives. Airlines operating widebodies on long-haul routes place premium value on fuel system integrity, where small efficiency losses translate to significant cost increases per flight. Consequently, fuel system MRO commands above-average priority in operator maintenance planning and budget allocation.

Electrical Systems maintenance has expanded in technical scope as modern widebodies such as the Boeing 787 shift to more-electric architectures. This transition increases both the volume and complexity of electrical system MRO events compared to older hydraulic-heavy platforms. For providers, this creates a capability investment requirement — but also a differentiation opportunity for those who build certified expertise early.

Maintenance Type Analysis

Heavy Maintenance dominates with 48.1% due to mandatory D-Check and C-Check compliance costs.

In 2025, Heavy Maintenance held a dominant market position in the By Maintenance Type segment of the Wide Body Aircraft MRO Market, with a 48.1% share. D-Check events requiring 200+ specialized technicians working around the clock for 45–60 days generate the largest individual revenue events in the MRO calendar. This volume concentration makes heavy maintenance both the highest-value and highest-risk segment for MRO providers managing capacity utilization.

Line Maintenance serves as the daily operational foundation that keeps widebody aircraft serviceable between scheduled major checks. Turnaround checks, pre-flight inspections, and minor defect rectification fall within this category. Because line maintenance occurs at airline hubs and outstations rather than dedicated MRO facilities, airlines often contract it to specialized ground service providers with airport-based certification approvals.

Base Maintenance occupies the middle tier between daily line checks and full heavy maintenance visits. Scheduled A-Checks and B-Checks fall within base maintenance scope and typically occur every 500–800 flight hours. Base maintenance provides MRO facilities with a steadier workflow than episodic heavy checks — making it a strategically important revenue stabilizer when heavy maintenance slots are between major events.

End-User Analysis

Commercial Operators dominate with 67.3% due to the highest widebody fleet concentration globally.

In 2025, Commercial Operators held a dominant market position in the By End User segment of the Wide Body Aircraft MRO Market, with a 67.3% share. Major network carriers operating long-haul fleets of Boeing 777, 787, and Airbus A350 aircraft generate the highest and most consistent MRO spend per operator. Their scale also gives them leverage to negotiate multi-year MRO contracts, which anchors provider revenue but compresses margins.

Cargo Operators represent a structurally distinct MRO customer driven by fleet conversion activity rather than passenger growth. Rising e-commerce volumes have extended the operational lives of freighter widebodies, including converted Boeing 747-400Fs and 767Fs. Extended utilization on these older platforms increases MRO frequency and scope, making cargo operators a disproportionately high-intensity MRO customer relative to their fleet size.

Military Operators follow procurement cycles and government defense budgets rather than commercial traffic economics. Military widebody platforms — including tankers and strategic airlifters — require highly specialized certifications that limit the pool of qualified MRO providers. This certification barrier creates a captive market structure where approved providers face limited competition and sustain premium pricing over long platform lifecycle periods.

Drivers

Aging Fleets and Rising Long-Haul Traffic Force Sustained MRO Investment Across All Operator Types

Wide body aircraft fleets worldwide are aging beyond their original design-point assumptions. Legacy platforms such as the Boeing 747-400 require D-Checks that cost USD 8–12 million per event. As these aircraft remain in service with cargo and charter operators, MRO providers absorb increasing technical complexity and parts sourcing pressure per event.

According to IATA, excess engine leasing costs reached USD 2.6 billion globally in 2025 alone, driven by engine shortages and extended turnaround times. This figure signals a structural supply-demand imbalance in engine MRO capacity — one that pushes airlines toward longer-term MRO contracts and gives established engine shops significant leverage in pricing negotiations.

Long-haul air traffic expansion adds new widebody aircraft to active fleets faster than MRO networks scale their certified capacity. Higher aircraft utilization rates compress the time between scheduled maintenance events, effectively increasing the annual volume of MRO work per aircraft. For MRO providers with certified widebody capabilities, this utilization dynamic directly translates to higher facility throughput and revenue per hangar bay.

Restraints

High Event Costs and Supply Chain Instability Constrain Operator MRO Budgets and Provider Throughput

Wide body D-Check events generate an economic impact far beyond direct maintenance spend. According to Aviation Titans, airlines lose USD 40,000–60,000 in daily revenue while an aircraft sits in the hangar, translating to USD 2.2–3.3 million in lost revenue per event. This dual burden of maintenance cost and revenue loss makes widebody operators highly sensitive to any extension in MRO turnaround time.

Aircraft spare parts availability remains a persistent operational constraint for MRO providers. Excess inventory holding costs for airlines reached USD 1.4 billion globally in 2025, reflecting the cost of stocking parts against unreliable supply timelines. When critical components are unavailable, aircraft remain grounded beyond their planned maintenance window — compounding both operator losses and MRO facility scheduling disruptions.

The concentration of qualified engine and component MRO capabilities among a small number of approved shops amplifies the impact of any supply disruption. Airlines without pre-negotiated access to spare parts pools or MRO slot priority face longer grounding events and higher emergency procurement costs. Emergency repair costs in aviation run 4.8× higher than planned maintenance — a cost differential that penalizes operators without robust MRO planning frameworks.

Growth Factors

Digital Maintenance Platforms and Fleet Conversion Demand Open New Revenue Streams for MRO Providers

In July 2024, Boeing announced a USD 4.7 billion deal to acquire Spirit AeroSystems, absorbing major structures production for the 767, 777, and 787 Dreamliner. This vertical integration move restructures the widebody supply chain in ways that directly affect MRO parts sourcing — providers who depend on independent suppliers for structural components must reassess their supply relationships ahead of this consolidation’s downstream effects.

According to SAS data, the airline issued approximately 1,000 predictive maintenance work orders since deploying its FOMAX system in early 2023, achieving an 83–86% success rate and 93–96% accuracy on positive findings. Aircraft connected to the predictive system showed 0.26% higher operational reliability versus unconnected fleet. These results demonstrate that digital maintenance investment generates measurable reliability returns, building the business case for broader platform adoption.

Wide body aircraft conversion and retrofit services create a parallel MRO revenue stream tied to network strategy shifts rather than airworthiness compliance alone. Airlines reconfiguring cabins for premium class expansion, or cargo operators converting passenger aircraft to freighters, generate retrofit contracts that require the same certified hangar capacity as heavy maintenance events. Providers who develop retrofit capabilities alongside traditional MRO services capture a wider share of total aircraft lifecycle spend.

Emerging Trends

AI-Driven Predictive Systems and Digital Twin Adoption Reshape MRO Scheduling and Cost Structures

According to IATA MRO Benchmark 2025, AI-powered predictive maintenance platforms reduce unscheduled aircraft-on-ground events by 35% within 12 months of deployment. The platforms deliver an average advance warning lead time of 21 days before component failure — giving operators sufficient runway to schedule maintenance within planned windows. This shift from reactive to anticipatory MRO fundamentally reorders the economics of widebody fleet management.

Digital twin technology replicates the physical state of an aircraft in a virtual environment, enabling engineers to simulate maintenance interventions before executing them on the actual aircraft. For widebody platforms that generate over 1 TB of sensor data per flight, digital twins provide the analytical infrastructure to translate raw data into actionable maintenance intelligence. Providers who build digital twin capabilities gain a competitive differentiator that time-based maintenance providers cannot match on cost or accuracy.

Third-party MRO service providers capture a growing share of widebody maintenance work as airlines outsource non-core technical operations to reduce fixed infrastructure costs. AI systems that achieve dispatch reliability of 99.5%+ for mature programmes — compared to the industry average of 97% — give outsourced MRO providers a performance argument that justifies premium contract pricing. This reliability gap makes outsourcing a financially compelling decision for operators evaluating internal versus external maintenance models.

Regional Analysis

North America Dominates the Wide Body Aircraft MRO Market with a Market Share of 43.70%, Valued at USD 11.2 Billion

North America commands 43.70% of the global Wide Body Aircraft MRO market, valued at USD 11.2 billion. US MRO facilities complete D-Checks 10–15% faster than international competitors and handle 25–30% of heavy maintenance work from foreign airlines. This speed and certification advantage, combined with deep OEM relationships, keeps North America structurally ahead of every other region in certified widebody MRO throughput.

Europe Wide Body Aircraft MRO Market Trends

Europe hosts some of the world’s most technically capable widebody MRO facilities, supported by EASA certification frameworks that attract operators across international routes. Germany, France, and the United Kingdom serve as the primary MRO hubs, with major engine and airframe facilities co-located near major international airports. European providers benefit from proximity to both legacy European carriers and a growing Middle Eastern operator base seeking certified heavy maintenance access.

Asia Pacific Wide Body Aircraft MRO Market Trends

Asia Pacific ranks as the fastest-expanding widebody MRO region, driven by fleet growth among Chinese, Indian, and Southeast Asian carriers adding twin-aisle aircraft to long-haul networks. In November 2025, ASI Global and Tata Projects signed an exclusive MoU to develop aircraft maintenance facilities across India, directly targeting commercial airline and MRO capacity pressures. This signals that private capital now views India’s MRO infrastructure gap as a commercially actionable opportunity.

Middle East and Africa Wide Body Aircraft MRO Market Trends

Middle Eastern carriers operate among the world’s largest and youngest widebody fleets, positioning the region as a critical MRO growth market for the next decade. Gulf airlines prefer facility investments in proximity to their hubs, supporting the development of domestic MRO capabilities in the UAE and Qatar. As fleet sizes grow and aircraft age into their first heavy maintenance cycles, MRO demand from this region will shift from line maintenance to scheduled heavy checks.

Latin America Wide Body Aircraft MRO Market Trends

Latin America’s widebody MRO market remains concentrated among a small number of large network carriers operating international routes to North America and Europe. Brazil and Mexico anchor regional MRO activity, with local providers focused on airframe and line maintenance for commercial operators. Economic volatility and currency risk complicate long-term MRO contract negotiations, pushing regional airlines toward shorter-term arrangements that limit provider revenue visibility.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Lufthansa Technik AG positions itself as one of the few truly vertically integrated independent MRO providers with full widebody capabilities across engine, airframe, and component services. Its global network of certified facilities allows the company to offer multi-year total care contracts to major international carriers. This breadth of capability makes Lufthansa Technik a structurally difficult competitor for single-service MRO specialists to displace on long-haul operator accounts.

Air France KLM Engineering and Maintenance (AFIKLME&M) operates as both an internal MRO provider for its parent group and a third-party services business competing for external airline contracts. This dual structure gives it scale advantages in parts procurement and hangar utilization while creating a potential conflict of interest with external airline clients who compete directly with Air France or KLM on certain routes. Managing this tension defines the strategic challenge at the core of its commercial MRO growth ambitions.

GE Aviation controls one of the largest installed bases of widebody commercial engines globally through its GE90, GEnx, and CF6 product families. Its MRO positioning benefits from OEM data access — allowing GE Aviation shops to perform overhauls with proprietary repair schemes that non-OEM providers legally cannot replicate. This technical exclusivity over its own engine platforms creates a captive aftermarket advantage that translates into above-market pricing power on shop visits.

Rolls-Royce PLC anchors its widebody MRO strategy around the Trent engine family, which powers the Boeing 787 and Airbus A350 — the two most commercially significant next-generation widebody platforms in service today. Its TotalCare long-term service agreements convert MRO from a transactional event into a recurring revenue stream aligned with aircraft flight hours. This power-by-the-hour model aligns provider and operator incentives around reliability, which differentiates Rolls-Royce from purely transactional MRO competitors.

Key Players

- Lufthansa Technik AG

- Air France KLM Engineering and Maintenance (AFIKLM E&M)

- GE Aviation

- Rolls-Royce PLC

- MTU Aero Engines AG

- Pratt and Whitney (RTX Group)

- Honeywell Aerospace

- ST Engineering Aerospace

- AAR CORP

- HAECO (Hong Kong Aircraft Engineering Co.)

Recent Developments

- December 2025 — Boeing completed its acquisition of Spirit AeroSystems in a USD 4.7 billion transaction (USD 8.3 billion including assumed debt), absorbing all Spirit Boeing-related commercial operations including fuselages for the 737 and major structures for the 767, 777, and 787 Dreamliner. Approximately 15,000 Spirit employees across 5 sites joined Boeing, fundamentally reshaping widebody airframe supply chain structure.

- November 2025 — Satair, an Airbus company, agreed to acquire Unical Aviation Inc. and its subsidiary ecube — a global used serviceable material provider with combined 2024 revenue of USD 298 million and operations across 7 sites in North America, Spain, and the United Kingdom. The deal, expected to close in early 2026, strengthens Airbus’s downstream parts supply position in widebody MRO aftermarkets.

- November 2025 — ASI Global and Tata Projects signed an exclusive MoU to collaborate on aircraft maintenance facility development across India, targeting capacity demands from commercial airlines, independent MRO providers, business aviation operators, and the defence sector. The agreement signals growing institutional confidence in India as a structurally viable widebody MRO hub for the Asia Pacific region.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 25.7 Billion |

| Forecast Revenue (2035) | USD 41.3 Billion |

| CAGR (2026-2035) | 4.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Service Type (Engine Maintenance, Airframe Maintenance, Component Maintenance, Modification and Upgrade), By Component Type (Avionics, Landing Gear, Fuel Systems, Electrical Systems), By Maintenance Type (Heavy Maintenance, Line Maintenance, Base Maintenance), By End User (Commercial Operators, Cargo Operators, Military Operators) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Lufthansa Technik AG, Air France KLM Engineering and Maintenance, GE Aviation, Rolls-Royce PLC, MTU Aero Engines AG, Pratt and Whitney (RTX Group), Honeywell Aerospace, ST Engineering Aerospace, AAR CORP, HAECO (Hong Kong Aircraft Engineering Co.) |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |