Quick Navigation

Report Overview

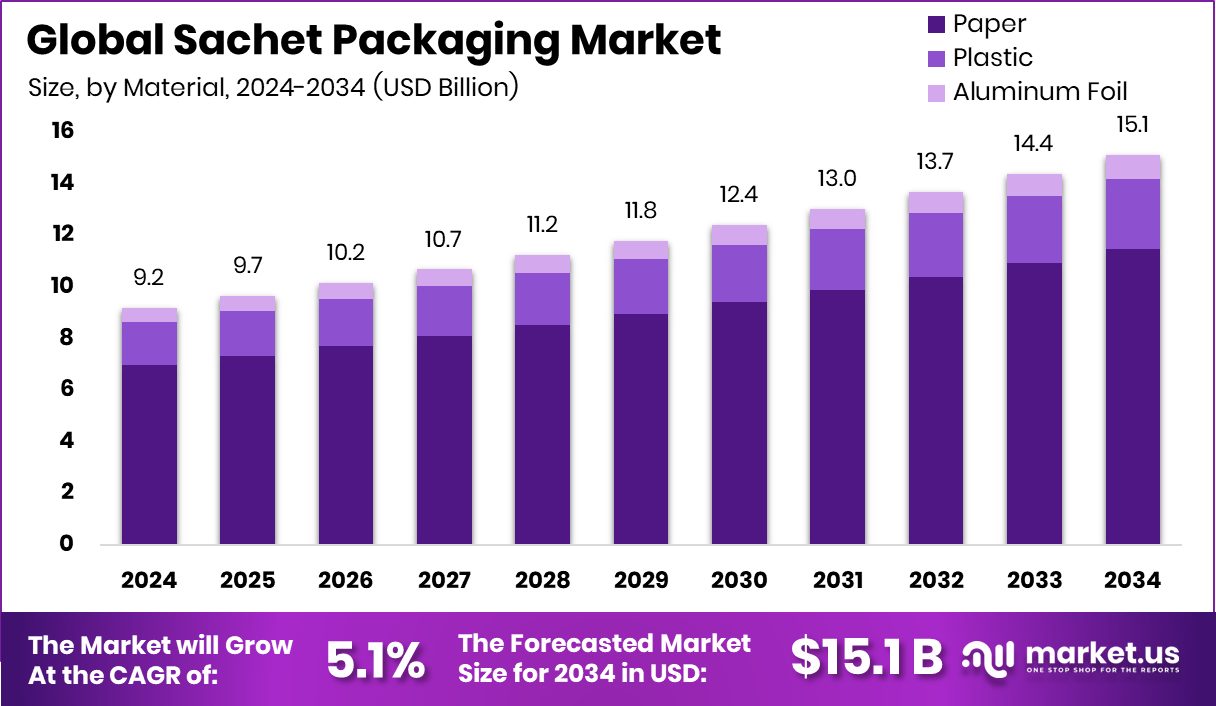

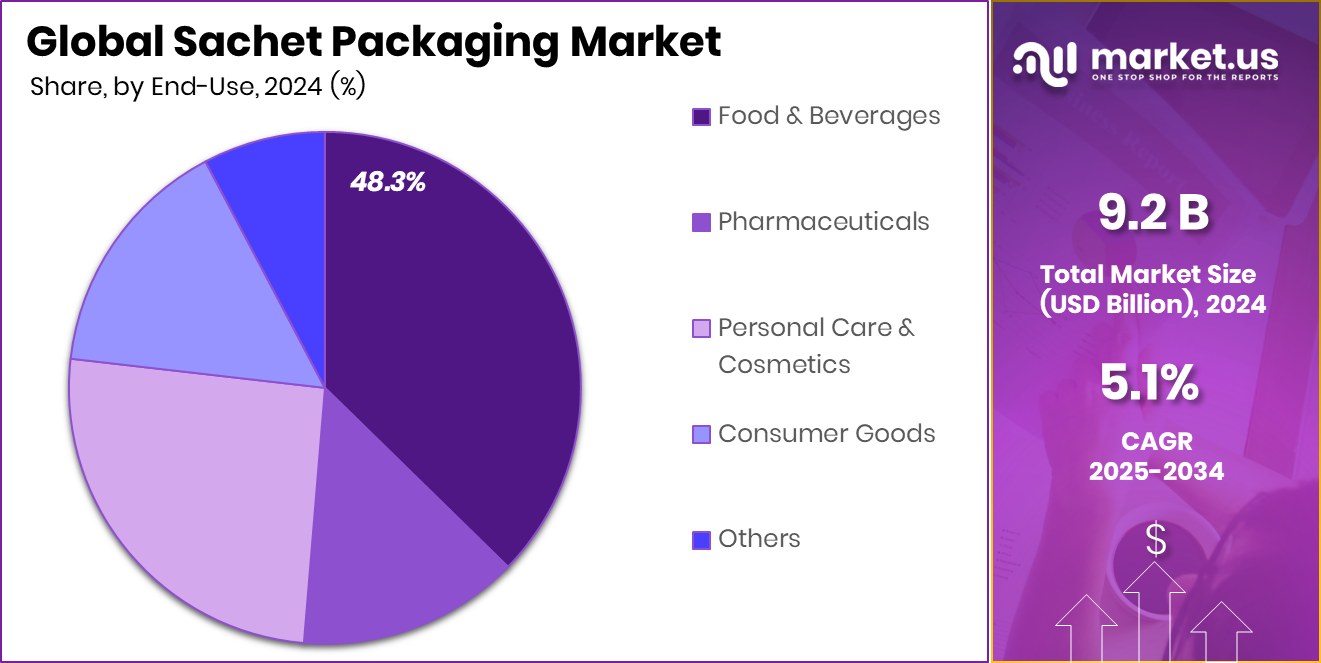

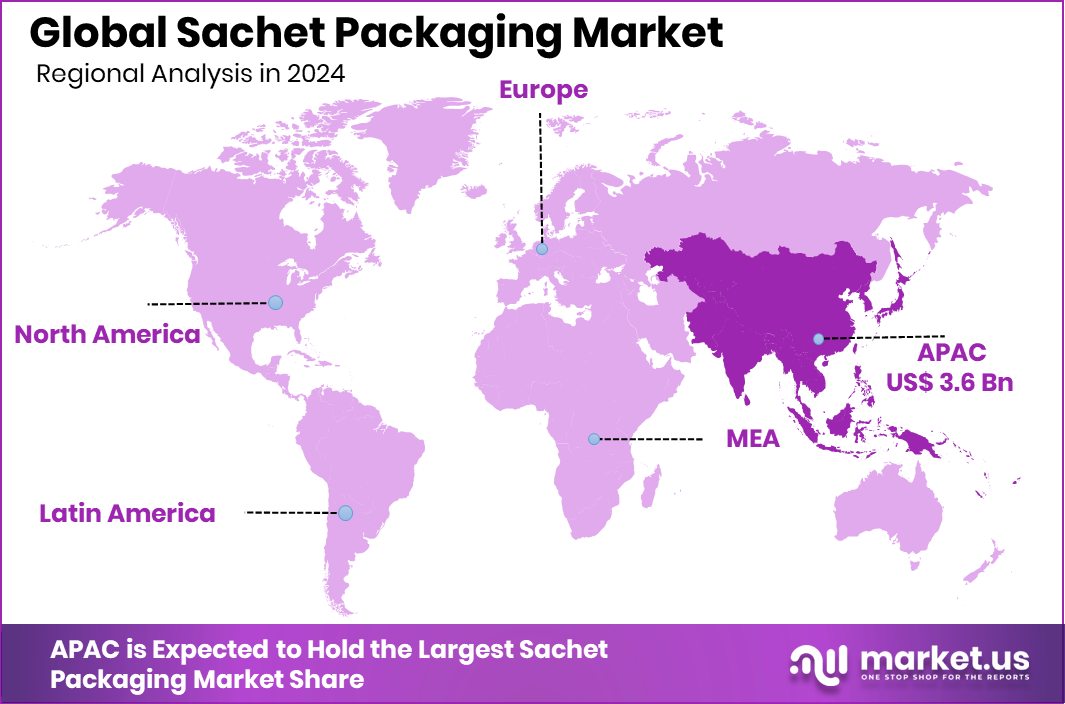

The Global Sachet Packaging Market is expected to be worth around USD 15.1 billion by 2034, up from USD 9.2 billion in 2024, and grow at a CAGR of 5.1% from 2025 to 2034. High consumption in rural regions drove Asia-Pacific sachet demand to 39.7% share.

Sachet packaging refers to small, sealed, flexible packs made from materials like plastic, paper, or foil, typically used for single-use quantities of products. These sachets are widely utilized for packaging items such as shampoo, condiments, spices, sugar, detergents, and pharmaceutical powders. Their small size, ease of transportation, and cost-effectiveness make them a popular choice in both developed and emerging markets.

The sachet packaging market has grown rapidly in recent years due to rising demand for affordable and convenient packaging formats. This format allows consumers to access branded products in small portions without committing to larger, more expensive packs. It especially caters to low-income and middle-income consumers in urban and rural areas where budget-conscious spending dominates. According to an industry report, the Minister has officially commissioned waste recycling equipment valued at $2.9 million, funded by Japan, aiming to strengthen environmental sustainability efforts.

One of the major growth factors driving this market is the increasing consumption of single-serve products across the food, personal care, and pharmaceutical industries. As urbanization accelerates, particularly in Asia and Africa, the demand for hygienic, portable, and easy-to-use packaging formats is rising sharply.

In terms of demand, sachets are widely adopted due to their low cost and ability to deliver sample-size products. Retailers and brands also prefer sachets as they boost product trial rates and widen consumer reach across remote or semi-urban locations. According to an industry report, Coca-Cola has launched a $137.7 million venture fund focused on driving innovations in sustainable packaging solutions.

Key Takeaways

- The Global Sachet Packaging Market is expected to be worth around USD 15.1 billion by 2034, up from USD 9.2 billion in 2024, and grow at a CAGR of 5.1% from 2025 to 2034.

- In the Sachet Packaging Market, paper material dominated with a 75.9% share due to eco-friendliness.

- Sachets sized between 1 ml and 10 ml led the market, accounting for 38.5% share globally.

- The food and beverage sector contributed a 48.3% share, making it the largest end-user in sachet packaging.

- The market size in Asia-Pacific reached a strong valuation of USD 3.6 billion.

By Material Analysis

Paper material dominates the sachet packaging market with a 75.9% share globally.

In 2024, Paper held a dominant market position in the By Material segment of the Sachet Packaging Market, with a 75.9% share. This strong presence is largely attributed to the growing demand for eco-friendly and recyclable packaging solutions across both developed and emerging economies. Consumers are increasingly becoming aware of the environmental impact of plastic waste, leading to a preference shift towards paper-based sachets.

Additionally, paper sachets are widely used for dry and powdered products, offering sufficient barrier protection while maintaining biodegradability. Their compatibility with water-based and natural inks further enhances their appeal among environmentally conscious brands. Governments across several regions have also implemented stricter regulations on single-use plastics, indirectly encouraging the shift to paper materials.

These factors collectively supported the dominance of paper in 2024, reflecting its growing relevance in sustainable packaging practices. The 75.9% market share held by paper indicates its clear preference over other materials within the sachet packaging landscape, reinforcing its position as the primary choice for manufacturers aiming to meet consumer expectations and regulatory standards in a cost-effective and sustainable way.

By Size Analysis

1 ml–10 ml sachet sizes account for 38.5% market share today.

In 2024, 1 ml–10 ml held a dominant market position in the By Size segment of the Sachet Packaging Market, with a 38.5% share. This size range is widely favored due to its suitability for single-use applications, especially in the personal care, food, and pharmaceutical sectors. Consumers in both urban and rural areas find 1 ml–10 ml sachets convenient for trial, travel, and on-the-go consumption.

The affordability of these small sachets has made them a preferred option among cost-sensitive consumers, particularly in developing economies. Brands also benefit by reaching a broader demographic without the need for larger packaging formats. Moreover, 1 ml–10 ml sachets are increasingly being used in promotional activities, sampling campaigns, and e-commerce product inserts, further boosting their volume consumption.

Manufacturers have responded by investing in high-speed, multi-lane filling machines tailored to produce small-volume sachets efficiently. The 38.5% market share reflects the widespread utility and consumer demand for this compact and economical format. As product accessibility and portability continue to be key purchase drivers, the dominance of 1 ml–10 ml sachets is expected to be sustained in the near term.

By End-user Analysis

Food and beverages lead end-user demand with 48.3% in the sachet packaging market.

In 2024, Food and Beverages held a dominant market position in the By End-user segment of the Sachet Packaging Market, with a 48.3% share. The dominance is driven by the widespread use of sachets for packaging sauces, ketchup, coffee, sugar, powdered drinks, and condiments in single-serve formats.

These small packs are highly preferred for their affordability, portability, and ability to preserve product freshness in small quantities. The increasing demand for portion-controlled food items, especially in quick service restaurants, cafeterias, and ready-to-eat segments, continues to fuel the adoption of sachet packaging.

Rural and semi-urban areas, particularly in developing regions, rely heavily on food sachets as a low-cost solution to access branded products without bulk purchases. In urban zones, the rise of takeaway services and delivery platforms further reinforces the need for compact, hygienic food packaging. Moreover, sachets reduce food wastage, allowing exact usage of contents in a single serving, which appeals to both consumers and food businesses.

Key Market Segments

By Material

- Paper

- Plastic

- Aluminum Foil

By Size

- 1 ml-10 ml

- 11 ml-20ml

- 21 ml-30 ml

- 30 ml and Above

By End-user

- Food and Beverages

- Pharmaceuticals

- Personal Care and Cosmetics

- Consumer Goods

- Others

Driving Factors

High Demand for Affordable Single-Use Product Packaging

One of the top driving factors in the sachet packaging market is the strong demand for affordable single-use packaging, especially in emerging economies. Many consumers prefer to buy small quantities of daily-use items like shampoo, ketchup, coffee, or sugar because it costs less and fits within their limited budgets. This packaging format helps brands reach more people, even in rural or low-income areas.

It also allows customers to try new products without spending too much. Sachets are easy to carry, store, and use, making them highly convenient for travel or on-the-go consumption. This growing preference for low-cost, disposable packs continues to push sachet packaging forward in both the food and personal care industries.

Restraining Factors

Environmental Concerns Over Single-Use Plastic Waste

One major factor holding back the sachet packaging market is the environmental concern about plastic waste. Many sachets are made using plastic or multi-layer materials that are hard to recycle.

These small packets often end up in landfills, rivers, or oceans, contributing to pollution and harming wildlife. Governments and environmental groups are pushing for stricter rules to reduce single-use plastics, which directly impacts the growth of sachet packaging.

In some countries, bans or extra taxes on such packaging are already being introduced. As awareness about sustainability rises, consumers and companies are being pushed to look for eco-friendly alternatives. This shift may slow down the demand for traditional plastic-based sachets shortly.

Growth Opportunity

Growing Demand for Eco-Friendly Sachet Packaging Solutions

A significant growth opportunity in the sachet packaging market lies in the increasing demand for eco-friendly and biodegradable packaging materials. As environmental concerns rise, consumers and governments are pushing for sustainable alternatives to traditional plastic sachets.

This shift is encouraging manufacturers to explore biodegradable options such as paper-based sachets, compostable films, and materials derived from renewable resources like starch and seaweed. These alternatives not only reduce environmental impact but also align with global sustainability goals.

The adoption of biodegradable sachets is gaining traction across various sectors, including food, personal care, and pharmaceuticals, as companies seek to meet consumer expectations and regulatory requirements. This trend presents a substantial opportunity for innovation and growth within the sachet packaging industry.

Latest Trends

Integration of Smart Features in Sachet Packaging

A notable trend in the sachet packaging market is the incorporation of smart technologies to enhance product functionality and consumer engagement. Manufacturers are embedding features such as QR codes, which allow consumers to access detailed product information, track authenticity, and receive usage instructions via their smartphones.

Additionally, advancements in smart packaging materials enable real-time monitoring of product freshness and quality, particularly beneficial for perishable goods. These innovations not only improve user experience but also help brands differentiate their products in a competitive market.

As consumer demand for transparency and convenience grows, the adoption of intelligent packaging solutions in sachets is expected to rise, offering new avenues for brand interaction and product safety assurance.

Regional Analysis

Asia-Pacific led the Sachet Packaging Market in 2024 with 39.7% regional share.

In 2024, Asia-Pacific emerged as the dominant region in the global Sachet Packaging Market, accounting for 39.7% of the total market share and reaching a value of USD 3.6 billion. This strong performance is primarily driven by high consumption of low-cost, single-use products across densely populated countries in the region. The popularity of sachets in rural and semi-urban areas, combined with growing urban demand for convenient, travel-friendly packaging, has significantly contributed to regional growth.

North America and Europe also held considerable shares in the market, supported by steady demand in the food, personal care, and pharmaceutical sectors. However, their growth remains relatively mature compared to Asia-Pacific.

Meanwhile, Latin America and the Middle East & Africa regions are witnessing the gradual adoption of sachet packaging, mainly driven by increasing urbanization and rising demand for portion-sized and trial-based products. Though these regions currently hold a smaller share, they offer potential for expansion as consumer habits shift toward convenience and affordability.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, Coveris reaffirmed its leadership in sustainable sachet packaging through its “No Waste” strategy. The company introduced recyclable and fiber-based solutions, such as the MonoFlex Fibre line, offering high shelf impact and recyclability within existing paper streams. Additionally, Coveris showcased its BarrierFresh MAP skillets, enhancing shelf life and reducing food waste.

ePac Holdings, LLC continued its trajectory as a digital-first flexible packaging provider, reporting approximately $200 million in sales. Despite industry challenges, ePac achieved a 30% increase in units produced over the previous year. The company’s strategic consolidation of U.S. operations into 11 manufacturing plants and its expansion into Canada, Europe, Asia/Pacific, and Africa demonstrate its commitment to operational efficiency and global reach. ePac’s focus on technological advancements in ERP, CRM, and digital printing positions it well for continued growth.

Glenroy, Inc. emphasized sustainability in its flexible packaging offerings, notably through its TruRenu® portfolio. This line includes recyclable pouches and film laminations with up to 53% recycled content. Glenroy’s premade STANDCAP Pouch, designed for ease of use and product freshness, exemplifies its innovative approach to reducing food waste. The company’s commitment to environmental responsibility is further evidenced by its EcoVadis Silver Medal achievement, placing it among the top 15% of companies assessed for sustainability.

Top Key Players in the Market

- Amber Packaging Industries LLC

- Amcor plc

- Budelpack

- Clondalkin Group

- Constantia Flexible Group GmbH

- Coveris

- ePac Holdings, LLC

- Glenroy, Inc.

- Graphic Packaging International, LLC

- Greendot Biopak Pvt. Ltd.

- Huhtamaki

- Mondi

- Paharpur 3p

- Polysack Flexible Packaging Ltd.

- ProAmpac

- RATTPACK

Recent Developments

- In March 2025, Constantia Flexibles successfully acquired a majority stake in Aluflexpack AG, a Swiss-based producer of custom flexible packaging for the food and pharmaceutical sectors. This acquisition aims to strengthen Constantia’s leadership in product innovation and sustainability, enhancing its ability to offer a broader range of packaging solutions.

- In October 2024, Amcor, in collaboration with Mespack, launched a recyclable 2-liter stand-up pouch using Amcor’s AmPrima® recycle-ready solutions. This innovation offers a sustainable packaging option with quality, durability, and performance suitable for brands’ filling machines, meeting the European Union’s Packaging and Packaging Waste Regulation requirements.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 9.2 Billion |

| Forecast Revenue (2034) | USD 15.1 Billion |

| CAGR (2025-2034) | 5.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material (Paper, Plastic, Aluminum Foil), By Size (1 ml-10 ml, 11 ml-20ml, 21 ml-30 ml, 30 ml and Above), By End-user (Food and Beverages, Pharmaceuticals, Personal Care and Cosmetics, Consumer Goods, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Amber Packaging Industries LLC, Amcor plc, Budelpack, Clondalkin Group, Constantia Flexible Group GmbH, Coveris, ePac Holdings, LLC, Glenroy, Inc., Graphic Packaging International, LLC, Greendot Biopak Pvt. Ltd., Huhtamaki, Mondi, Paharpur 3p, Polysack Flexible Packaging Ltd., ProAmpac, RATTPACK |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |