Quick Navigation

- Report Overview

- Key Takeaways

- Purity Level Analysis

- Product Type Analysis

- Form Analysis

- Application Analysis

- End-User Industry Analysis

- Key Market Segments

- Driver Analysis

- Restraint Analysis

- Opportunity Analysis

- Challenges Analysis

- Geopolitical Impact Analysis

- Regional Analysis

- Key Players Analysis

- Key Development

- Report Scope

Report Overview

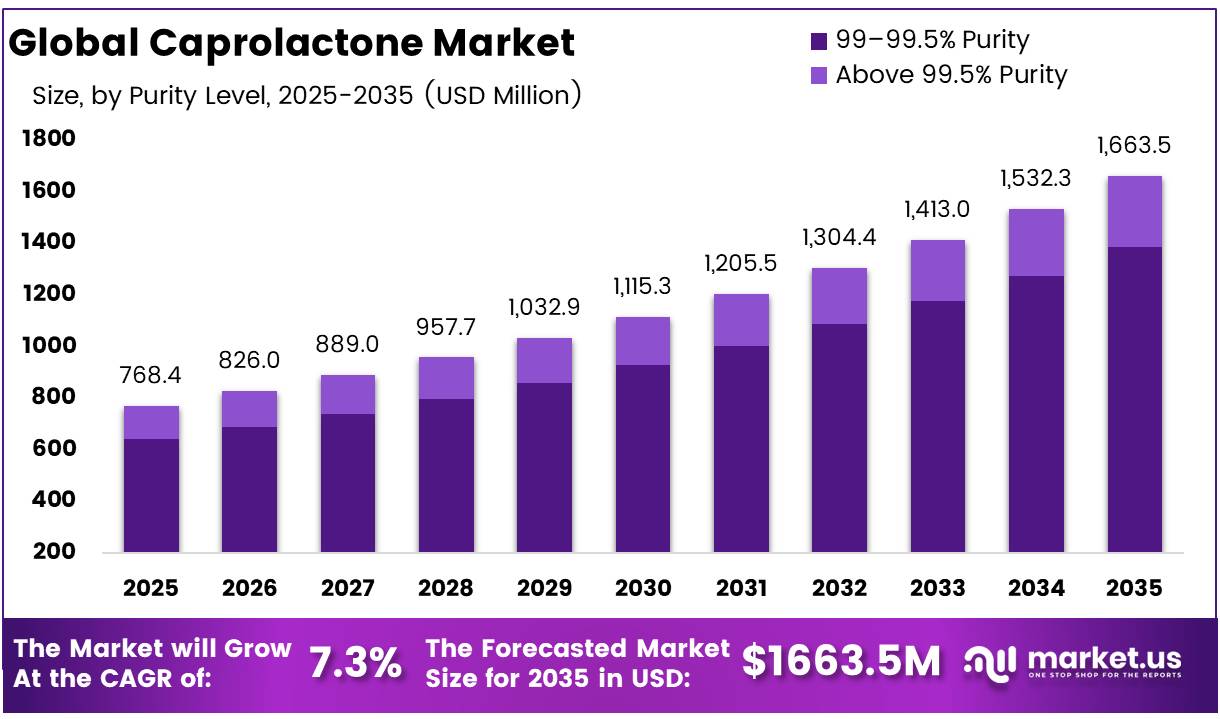

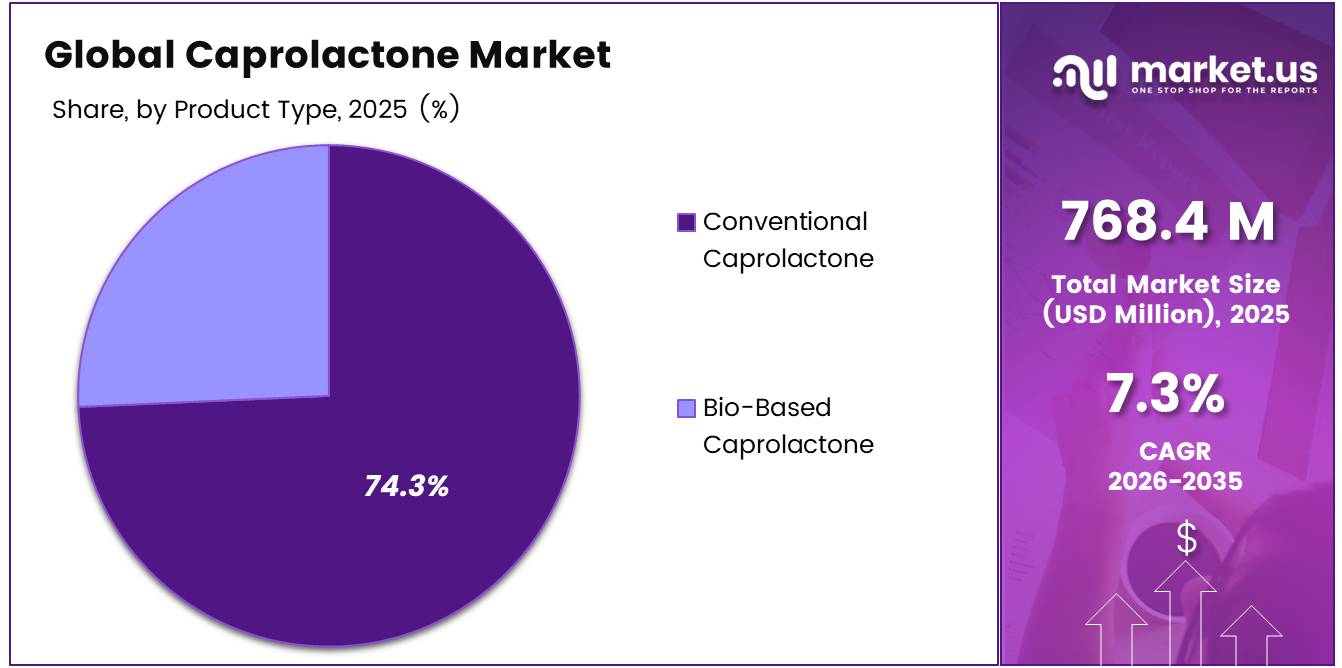

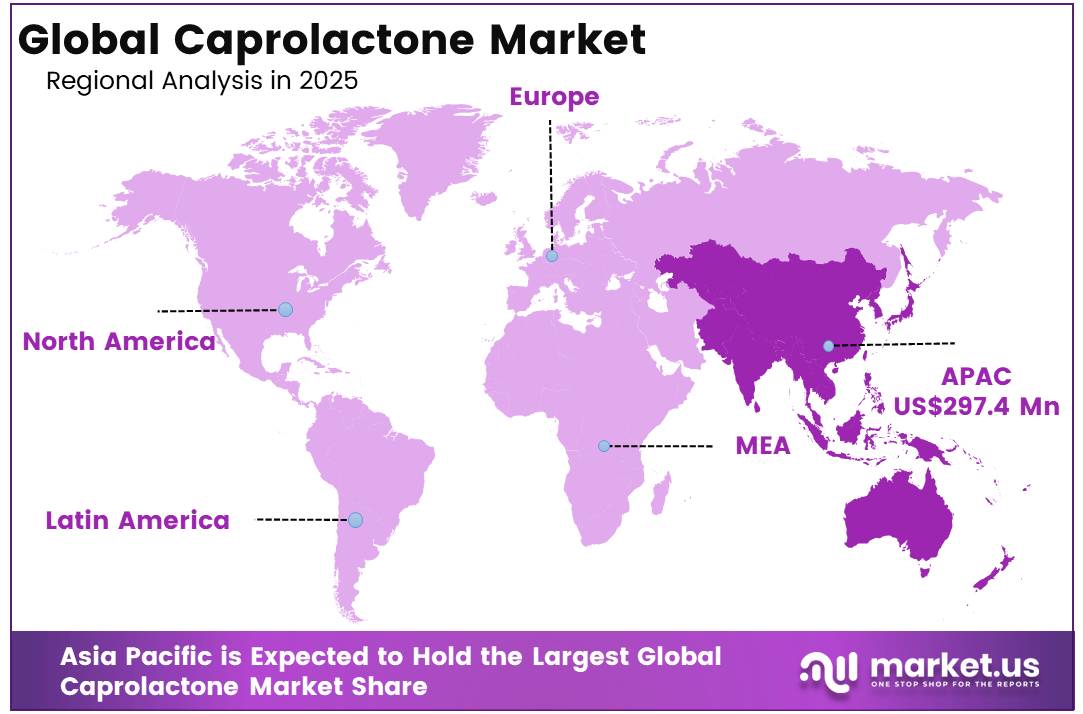

The Global Caprolactone Market was estimated to be worth approximately USD 768.4 million in 2025 and was expected to grow at a CAGR of 7.3% to achieve a valuation of USD 1,663.5 million in 2035. The Asia Pacific region was the leader in the market with a market share of above 38.7%, which accounted for revenues of USD 297.4 million.

Caprolactone is a lactone or cyclic ester having seven members and acts as an important raw material to produce polycaprolactone (PCL), polyurethane polyols, and specialized polymer intermediates used in healthcare, automotive, coating, and packaging applications. While other chemicals are mass-produced, caprolactone requires higher standards of purity as its use in polymerization processes requires stringent purity requirements.

- Growing global need for biodegradable polymers, underpinned by EU’s Single-Use Plastics Directive, forcing reforms through 27 member countries, coupled with the growing use of PCL based bio-resorbable medical products, is driving the growth of approximately USD 4.2 billion in new opportunities for biodegradable polymers by 2030, with caprolactone derived PCL emerging as one such commercial option.

Key Takeaways

- The global Caprolactone market size was USD 768.4 million in 2025.

- Global market size is estimated to grow to USD 1,663.5 million by 2035.

- Compound Annual Growth Rate (CAGR) of the market from 2026 to 2035 will be at 7.3%.

- 99–99.5% Purity stood at 83.2% of the total purity segment.

- The Conventional Caprolactone segment contributed 74.3% of the total product type segment.

- Liquid form holds the largest share at 72.1% of the total form segment.

- Polycaprolactone (PCL) Production, contributing 36.2% of the total application revenue.

- Healthcare & Medical sub-category holds a market share of 31%

- The leading regional market is Asia Pacific with a market share of 38.7% of total global revenue.

The rise in production and use of caprolactone is associated with increasing manufacture of polyurethane in Asia Pacific and clinical trials of PCL-based drug carriers. It is further associated with the transformational changes in the automotive industry globally, especially in the shift from heavy materials towards light-weight elastomer materials. Increased demand has been witnessed in Europe and North America due to increased VOC regulations, favouring waterborne PU dispersions, PCL approval in medical devices by the FDA, and OEM commitment towards sustainable polymers.

The Global Caprolactone Market is expected to expand due to increased regulations for degradable polymers, growing application in the healthcare sector as a polymer and increasing need for polyurethane elastomers in the electric vehicles industry. Consumer and manufacturer environmental sustainability commitments within consumer goods and packaging industries have created significant market interest in caprolactone derivatives such as PCL well outside of the historical chemical industrial market, particularly in North America and Europe.

Purity Level Analysis

99–99.5% Purity Grade Leads Caprolactone Market through Cost Efficiency and Industrial Compatibility

99–99.5% Purity leads with 83.2% of global Caprolactone market sales, serving as the established standard for large-scale polymer manufacturing. This grade delivers an optimal balance of technical performance and cost efficiency, enabling consistent use across PCL polymer synthesis, polyurethane intermediate preparation, and industrial coating formulations. High-capacity producers in Asia and Europe favor it for compatibility with continuous flow reactor systems, eliminating costly additional purification steps. For instance, Perstorp Holding AB supplies this grade as its primary commercial offering to polyurethane manufacturers across Europe and Asia Pacific.

The Above 99.5% Purity is the fastest growing segment, driven by demand for pharmaceutical-grade materials in drug delivery systems, biodegradable implants, and biocompatible medical products. For instance, Evonik Industries AG supplies ultra-high purity, medical-grade polycaprolactone (RESOMER® PCL) globally to orthopedic implant and drug delivery manufacturers to meet strict regulatory standards.

Product Type Analysis

Conventional Caprolactone Dominates Market through Strong Supply Chains and Industrial Reliability

Traditional Caprolactone has a strong market share of 74.3%, owing to the well-developed industrial facilities, existing petrochemical supply chain, and integrated position in global polyurethane and PCL polymer manufacturing operations. Competitive pricing, reliable sources of raw materials through cyclohexanone oxidation pathways, and favorable market conditions in Europe, the United States, and the Asia-Pacific region guarantee continued preference among industrial purchasers for conventional caprolactone in large-volume purchases in the coatings, automotive, and packaging segments.

- According to the American Chemistry Council (ACC), caprolactone polyurethane polyols are among the most flexible and reliable procurement intermediate products used in industrial polymer manufacturing.

Bio-Based Caprolactone is the fastest-growing product type, driven by EU Green Deal obligations, PPWR mandates requiring certified compostable packaging content by 2030, and green procurement commitments from major consumer goods producers. For instance, Perstorp Holding AB continues to expand its Capa™ polycaprolactone operations to meet growing global demand for biodegradable polymers and bioplastics, focusing caprolactone manufacturing and R&D at its facility in Warrington, England.

Form Analysis

Liquid Caprolactone Leads Market Due to Efficient Processing and Industrial Handling Benefits

Liquid caprolactone takes up a dominant share of 72.1% in the form category owing to its basic suitability for the continuous flow process conditions that apply in bulk chemicals manufacturing where pumping, metering, and feeding reactor operations are mandatory. Liquid caprolactone helps avoid melting procedures during the preparation of solid materials prior to use in ring-opening polymerization (ROP) reactors thereby minimizing production time and costs of utilities for mass PCL production in Europe and Asia.

Caprolactone solid at 27.9% is witnessing increasing demand in medical applications, specialty compounding, and precise laboratory synthesis, owing to benefits of precise dosing, ambient temperature stability, and minimized contamination. Its solid form enables easier long-distance shipping and extended shelf-life storage compared to liquid, making it preferred for small-batch pharmaceutical and research applications. For instance, Merck KGaA supplies solid caprolactone to research institutions and pharmaceutical compounding facilities across North America and Europe, where controlled dispensing and contamination-free handling are critical requirements.

Application Analysis

Polycaprolactone Production Dominates Applications through Rising Demand for Biodegradable Polymers

Polycaprolactone (PCL) Production makes up 36.2% of the revenue in applications and is the most strategically important end-use application in terms of volumes and value for caprolactone. Caprolactone ability to form biodegradable and biocompatible materials that possess mechanical flexibility allows it to be used in medical sutures, drug delivery matrices, three-dimensional printed scaffolds and environmentally friendly packaging films.

Medical and Drug Delivery applications are the fastest growing end uses of caprolactone. With increased clinical implementation of implantable drug release systems and resorbable surgical devices based on PCL. Adhesives & Sealants, Coatings & Paints, and Others constitute the remainder of application revenue through consistent industrial consumption in automotive refinish coatings, construction assemblies, and specialty coatings.

End-User Industry Analysis

Healthcare & Medical Sector Leads Caprolactone Demand through High-Value Biomedical Applications

Healthcare & Medical represents 31.0% of end-user’s income, thus being the most valuable consuming industry of caprolactone on a global scale. Demand from the Healthcare & Medical industry is structurally diverse with high unit-value applications in the form of biodegradable sutures, controlled release implants, scaffolds for tissue engineering, and diagnostic medical device coating solutions where PCL-grade caprolactone enjoys substantial price premium versus industrial-grade.

- Regulatory clearance via the FDA 510(k) pathway and EU MDR (2017/745) compliance significantly expands the number of addressable commercial products, driving a steady increase in global demand for medical-grade PCL in targeted drug delivery and implant applications.

Fastest-growing end-user application segment is Automotive driven by growing consumption of polyurethane elastomers in lightweight automotive parts for electric vehicles, seat foam systems, and exterior OEM coatings requiring outstanding hydrolytic resistance. (Source: International Energy Agency – IEA Global EV Outlook, 2024). Share of Packaging, Construction, Consumer Goods, Electronics, Textiles & Footwear, and Other sectors represent the remaining end-user revenue supported by stable demand of caprolactone for polyol production and PCL coatings.

Key Market Segments

By Purity Level

- 99–99.5% Purity

- Above 99.5% Purity

By Product Type

- Conventional Caprolactone

- Bio-Based Caprolactone

By Form

- Liquid

- Solid

By Application

- Polycaprolactone (PCL) Production

- Adhesives & Sealants

- Coatings & Paints

- Medical & Drug Delivery

- Others

By End-User Industry

- Healthcare & Medical

- Automotive

- Packaging

- Construction

- Consumer Goods

- Electronics

- Textile & Footwear

- Others

Driver Analysis

Medical-grade PCL adoption in resorbable devices

Caprolactone demand is being structurally lifted by medical-device programs that use polycaprolactone as a slow-resorbing biomaterial for scaffolds, drug-delivery matrices, fixation systems, and regenerative applications, because these uses convert a relatively small-volume monomer stream into premium-value downstream consumption with tighter qualification lock-in.

The regulatory pathway is demanding but commercially favorable: high-risk devices still require PMA scrutiny, while novel moderate-risk devices can use the De Novo route, and FDA’s stated De Novo review goal remains 150 review days, which supports a clearer commercialization cadence for differentiated biodegradable devices than many industrial applications can offer.

Supporting this, industry sources continue to position caprolactone-based specialty polymers for medical devices specifically, while PCL’s low processing temperature near 60 degrees Celsius and long degradation profile make it attractive where shape retention and controlled resorption matter.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Medical-grade PCL adoption in resorbable devices | +1.7% | North America core, EU, Japan, South Korea | Medium term (2-4 years) |

| 3D printing and scaffold fabrication pull | +1.3% | North America, EU, China, South Korea | Short term (≤ 2 years) |

| Biodegradable coatings, adhesives, and TPU formulations | +1.1% | EU core, North America, China, Southeast Asia | Medium term (2-4 years) |

| Packaging compliance and compostable-material substitution | +0.8% | EU core, California-led North America, developed APAC | Short term (≤ 2 years) |

| Capacity optimization and supply reliability at incumbent producers | +0.6% | Europe export hub, North America, APAC import markets | Short term (≤ 2 years) |

| Higher-value specialty mix shift from commodity chemistry | +0.9% | North America, EU, China, India | Long term (≥ 4 years) |

Restraint Analysis

Regulatory ambiguity on biodegradables

The EU Packaging and Packaging Waste Regulation, which entered into force in early 2025 and begins applying widely from mid‑2026, introduces stricter recyclability, EPR, and material‑use rules but still leaves gray zones on when biodegradable or compostable plastics are preferred, allowed only in specific applications, or discouraged, forcing brand owners to plan for multiple regulatory scenarios and often default to conventional polyolefins to avoid compliance risk.

In parallel, U.S. state‑level initiatives, including California’s EPR and labeling laws, impose different labeling and performance requirements, so a converter targeting 2027–2030 launches may need to invest in 2–3 parallel formulations and test programs to cover EU, UK, and U.S. markets, adding several hundred thousand dollars in incremental testing and tooling cost per platform and stretching development cycles by 12–24 months; this multi‑jurisdictional friction reduces the number of SKUs that actually reach commercial scale with caprolactone content and is estimated to suppress the market’s CAGR by around 0.9 percentage points versus a scenario with harmonized, pro‑biodegradable rules.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock and energy price volatility | -1.4% | EU, North America, energy-importing APAC | Short term (≤ 2 years) |

| Concentrated manufacturing base risk | -1.2% | Europe export hub, APAC and Americas importers | Medium term (2-4 years) |

| Regulatory ambiguity on biodegradables | -0.9% | EU core, UK, North America | Medium term (2-4 years) |

| Slow qualification cycles in medical and CASE | -1.1% | North America, EU, Japan, South Korea | Long term (≥ 4 years) |

| Competition from cheaper polymers and bio-routes | -1.0% | China, India, price-sensitive APAC corridors | Medium term (2-4 years) |

| Macroeconomic and capex cyclicality in end-use sectors | -0.8% | Global, with heavier drag in EU and Latin America | Short term (≤ 2 years) |

Opportunity Analysis

Med‑tech contract development and manufacturing (CDMO)

PCL is already recognized as a versatile biomaterial in implants, scaffolds, and drug‑delivery systems, but the opportunity is to move beyond raw‑material and simple compound selling into a full med‑tech CDMO model where caprolactone suppliers provide formulation, 3D‑printing support, regulatory documentation, and even finished or semi‑finished components, capturing a much larger share of value in a still‑nascent but scalable market.

Most device OEMs lack deep polymer science capabilities and face 18–36 month development and regulatory timelines with seven‑figure non‑recurring costs per platform, so a CDMO that standardizes PCL‑based device platforms could cut their time‑to‑market by 6–12 months and reduce up‑front development costs by 20–30 percent, while charging 30–50 percent higher prices per kilogram compared with bulk PCL.

Given the growth trajectory of polycaprolactone in medical applications and the rising complexity of PMA and De Novo submissions through 2030, capturing just 10–15 percent of new PCL‑based device programs into such CDMO platforms could add mid‑double‑digit millions of dollars in incremental annual revenue for a leading player by the early 2030s, corresponding to about 1.7 percentage points of CAGR upside versus a baseline where PCL suppliers remain primarily raw‑material vendors and leave med‑tech value‑chain integration to others.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Food and nutraceutical packaging & encapsulation | +1.6% | EU, North America, East Asia | Medium term (2-4 years) |

| Platform play in advanced performance intermediates | +1.8% | North America core, EU, China | Long term (≥ 4 years) |

| Biopolymer alliances for regulated packaging | +1.3% | EU core, UK, U.S. coastal states | Short term (≤ 2 years) |

| Med-tech contract development and manufacturing (CDMO) | +1.7% | North America, EU, Japan, South Korea | Long term (≥ 4 years) |

| Regionalization of capacity into APAC and India | +1.4% | China, India, ASEAN corridors | Medium term (2-4 years) |

| M&A roll-up of fragmented specialty converters | +1.5% | EU, North America, China | Medium term (2-4 years) |

Challenges Analysis

Fragile logistics and chokepoint exposure

Caprolactone’s global supply chain is structurally exposed to a small number of maritime and intermodal chokepoints connecting European production sites with high‑growth demand centers in Asia and the Americas, and while these routes remain open, episodic disruptions—such as canal blockages or port congestion—introduce 1–3 week lead‑time swings that continuously complicate inventory planning and customer service. The Ever Given incident in the Suez Canal, which blocked an estimated 9.6 billion U.S. dollars of trade per day during its six‑day grounding, remains an emblematic example of how a single event can halt a major corridor and cascade across supply chains for weeks afterward.

For caprolactone, even shorter disruptions can extend transit times from a baseline of 25–35 days door‑to‑door to 40–50 days when rerouting around chokepoints or waiting for backlogs to clear, forcing distributors and converters to carry 20–40 percent higher safety stocks to maintain service levels, raising working‑capital requirements by several million dollars at sector scale and dissuading some smaller converters from aggressively scaling PCL‑heavy product lines.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Complex multi-step production chemistry | -1.0% | EU production hubs, global downstream | Long term (≥ 4 years) |

| Volatile trade, tariffs, and compliance burden | -0.9% | North America core, EU regulatory hubs, APAC trade routes | Medium term (2-4 years) |

| Fragile logistics and chokepoint exposure | -0.8% | EU–APAC and EU–Americas corridors | Medium term (2-4 years) |

| Process engineering and biocatalysis talent gap | -0.7% | EU, U.S., Japan, emerging APAC | Long term (≥ 4 years) |

| Customer processing know-how deficit | -0.8% | China, India, Southeast Asia, Latin America | Medium term (2-4 years) |

| Measurement, LCA, and sustainability data complexity | -0.6% | EU regulatory hubs, multinational OEMs | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Energy Risks, Trade Barriers, and Industrial Policies Reshaping Caprolactone Supply Chains

The caprolactone industry is vulnerable to geopolitical risks affecting feedstock availability, economics of trade, and regulations of the end-markets. The benzene-cyclohexanone-caprolactone manufacturing process operates in a geographically focused cluster across Western Europe and North Asia, leaving it susceptible to energy price shocks, disruption at ports, and shifts in trade policies.

The European energy crisis of 2022–2023, driven by the reduced flow of gas via pipelines from Russia, resulted in higher costs of cyclohexanone production across European chemical plants, necessitating reductions in capacity utilization and caprolactone output by some producers, leading to tight supply and price increases and project delays.

The development of domestic production in China as part of its strategy on specialty chemicals outlined in the 14th Five-Year Plan will bring new competition into the APAC export market for incumbent western caprolactone producers. The European Carbon Border Adjustment Mechanism (CBAM) that will increasingly cover chemical intermediates over the period 2026–2030 will change the competitiveness of foreign caprolactone producers supplying European customers, fostering developments of more sustainable bio-based manufacturing processes.

Regional Analysis

Asia Pacific Dominates the Global Caprolactone Market Driven by Strong Manufacturing and Industrial Demand

Asia Pacific dominates in terms of the global caprolactone market revenues with a revenue share of 38.7% by 2025 to generate around USD 297.4 million. This dominance is due to strong demand from polyurethane coatings, adhesives, elastomers, biodegradable polymers, and biomedical materials across China, Japan, South Korea, and India. The region has a large manufacturing base, expanding automotive production, growing electronics output, and rising investment in healthcare materials. Increasing use of PCL-based polymers in medical, packaging, and industrial applications further supports caprolactone consumption across Asia Pacific.

Europe and North America are the second and third largest markets, respectively, due to strong regulatory support for biodegradable polymers, sophisticated medical device production facilities, and increased specifications for polyurethane from automotive OEMs. Latin America and the Middle East & Africa markets are still in their infancy stages; however, investment in the packaging and construction sectors will provide impetus for caprolactone usage.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Competitive advantage is gained in caprolactone manufacturing through technical grade differentiation, feedstock integration, and application-oriented polymer formulation for healthcare, automotive, and coatings markets. Focus on developing pharmaceutical-grade ultrahigh purity caprolactone for biodegradable medical devices, development of bio-based caprolactone using renewable feedstocks meeting the criteria for EU Green Deal, and innovation in caprolactone polyols used to formulate advanced waterborne polyurethane dispersions meeting low-VOC industrial coatings specifications are among the critical growth areas.

Vertical integration with respect to sourcing cyclohexanone feedstocks and manufacturing of PCL polymer helps maintain pricing stability irrespective of changes in petrochemical market conditions. Expansion of manufacturing capacities in Asia Pacific will allow the company to align with increasing demand for PCL and polyurethanes from healthcare, packaging, and automotive manufacturing industries. Regulatory compliance in various markets, including FDA approvals for pharmaceutical applications, REACH registrations in EU, and Chinese NMPA for medical device uses, along with long-term agreements with tier-1 automotive OEMs and pharmaceutical contract manufacturers, supports high pricing power.

The Major Key Players in the Industry

- Perstorp Holding AB

- Daicel Corporation

- BASF SE

- Merck KGaA

- Solvay S.A.

- Evonik Industries AG

- Arkema Group

- Croda International Plc

- Huntsman Corporation

- Eastman Chemical Company

- Oxea GmbH

- Ingevity Corporation

- Tokyo Chemical Industry (TCI)

- Alfa Aesar (Thermo Fisher Scientific)

- Ube Industries Ltd.

Key Development

- January 2026, Perstorp Holding AB expanded its bio-based caprolactone production line in Sweden, targeting a 20% output increase to meet rising European biodegradable polymer and sustainable packaging demand.

- February 2026, Daicel Corporation completed pharmaceutical-grade caprolactone qualification trials supplying three major Japanese medical device manufacturers producing bioresorbable orthopaedic implant and surgical fixation components.

- March 2026, BASF SE launched a caprolactone-based waterborne polyurethane dispersion product line targeting low-VOC automotive refinishing and industrial floor coating applications across European and North American markets.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 768.4 Million |

| Forecast Revenue (2035) | USD 1663.5 Million |

| CAGR (2026-2035) | 7.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Purity Level (99–99.5% Purity, Above 99.5% Purity), By Product Type (Conventional Caprolactone, Bio-Based Caprolactone), By Form (Liquid, Solid), By Application (Polycaprolactone (PCL) Production, Adhesives & Sealants, Coatings & Paints, Medical & Drug Delivery, Others), By End-User Industry (Healthcare & Medical, Automotive, Packaging, Construction, Consumer Goods, Electronics, Textile & Footwear, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC – China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America – Brazil, Mexico & Rest of Latin America; Middle East & Africa – GCC, South Africa & Rest of MEA |

| Competitive Landscape | Perstorp Holding AB, Daicel Corporation, BASF SE, Merck KGaA, Solvay S.A., Evonik Industries AG, Arkema Group, Croda International Plc, Huntsman Corporation, Eastman Chemical Company, Oxea GmbH, Ingevity Corporation, Tokyo Chemical Industry (TCI), Alfa Aesar (Thermo Fisher Scientific), and Ube Industries Ltd. |

| Customization Scope | Segment, country, and regional customization, along with company profiling, pricing trends, CAGR updates, competitive benchmarking, and additional application or technology segmentation, can be provided as per client requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate User License (Unlimited User and Printable PDF) |