Quick Navigation

Report Overview

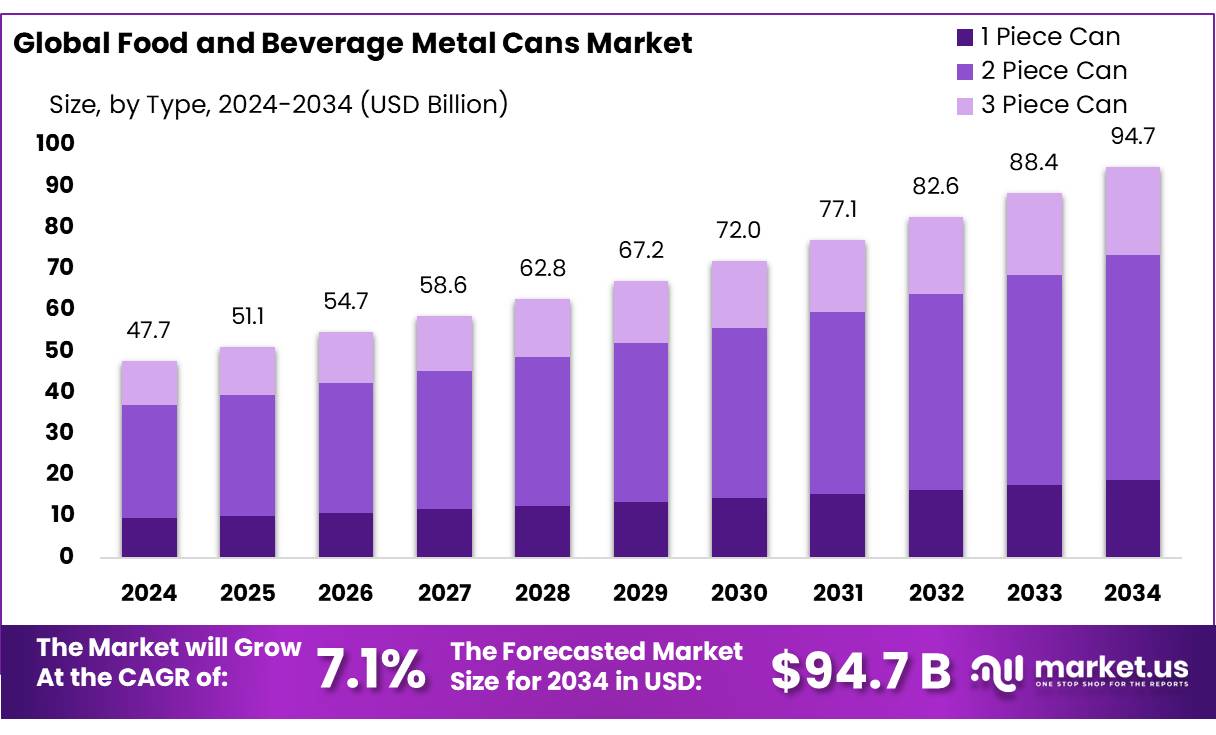

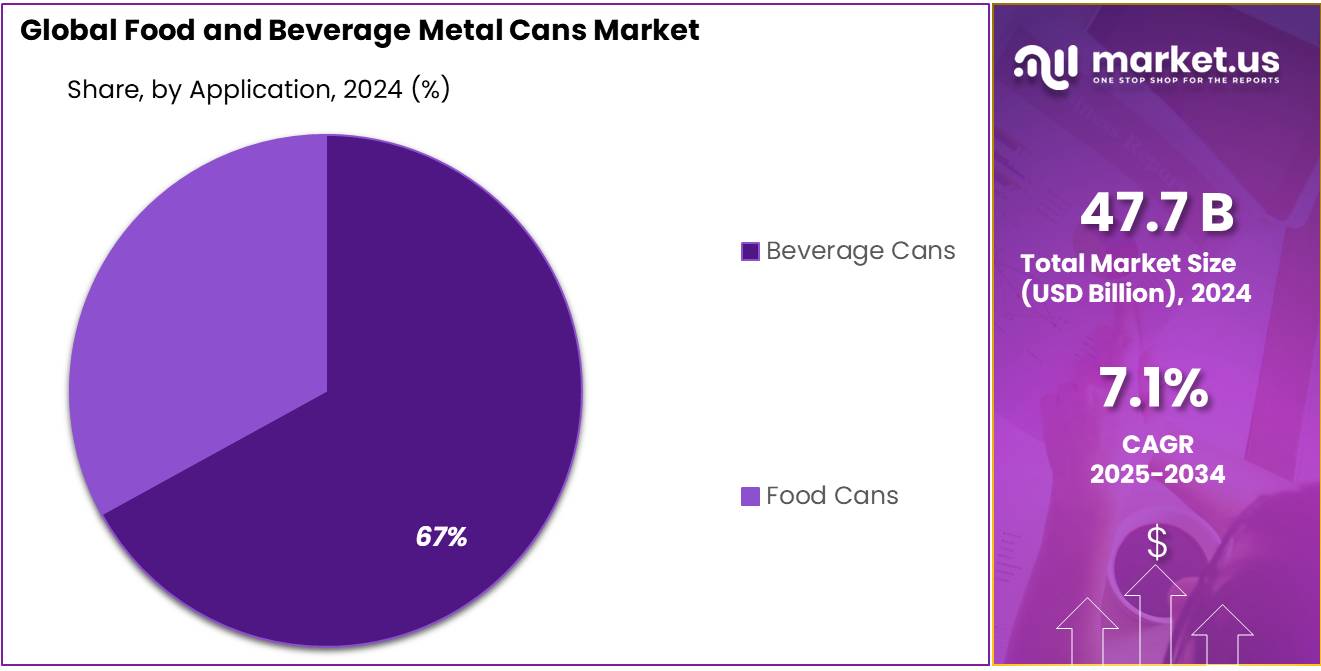

The Global Food and Beverage Metal Cans Market size is expected to be worth around USD 94.7 Billion by 2034, from USD 47.7 Billion in 2024, growing at a CAGR of 7.1% during the forecast period from 2025 to 2034.

The Food and Beverage Metal Cans industry serves as a critical segment in packaging solutions, catering to a vast range of products including carbonated drinks, alcoholic beverages, and processed foods like soups, fruits, and vegetables. These cans are favored for their durability, impermeability, and recyclability, making them an enduring choice in the global food and beverage sector. According to the U.S. Environmental Protection Agency (EPA), metal cans boast a recycling rate of about 71%, one of the highest among packaging materials, underscoring their environmental appeal.

Globally, the industry is witnessing substantial growth, driven by advancements in can technology such as lightweighting, improved barrier coatings, and aesthetic enhancements. These innovations are enabling manufacturers to extend the shelf life of food products and enhance their marketability. In the United States, according to the Department of Commerce, approximately 100 billion metal cans are produced annually, indicating robust production capabilities and the scale of consumption.

Governmental bodies worldwide are implementing initiatives to support recycling and sustainable production practices. For instance, the European Union’s Circular Economy Action Plan emphasizes enhancing recycling processes and includes specific targets for metal packaging. The plan aims to achieve a recycling rate of 80% for metal packaging by 2030, further driving the adoption of sustainable practices within the industry.

Technological innovations such as smart packaging, which includes QR codes and smart labels, offer new avenues for engaging consumers and providing product transparency. Additionally, the ongoing trend towards premiumization in food products is expected to open new markets for luxuriously designed metal cans that appeal to aesthetically driven consumers.

Key Takeaways

- Food and Beverage Metal Cans Market size is expected to be worth around USD 94.7 Billion by 2034, from USD 47.7 Billion in 2024, growing at a CAGR of 7.1%.

- 2 Piece Can segment held a commanding presence in the food and beverage metal cans market, securing more than a 57.4% share.

- Aluminium was the most widely used raw material in the food and beverage metal cans market, capturing a substantial 67.1% market share.

- Cans with a capacity ranging from 330 ml to 500 ml dominated the food and beverage metal cans market, accounting for more than 61.3% of the market share.

- Printed cans held a dominant position in the food and beverage metal cans market, capturing more than a 67.2% share.

- Pressurized cans emerged as the leading segment in the food and beverage metal cans market, securing more than a 71.9% share.

- Beverage cans held a dominant market position in the food and beverage metal cans sector, capturing more than a 67.8% share.

- Asia-Pacific (APAC) region emerged as the dominant force in the global food and beverage metal cans market, capturing a substantial 52.8% share and reaching a market value of approximately USD 25.1 billion.

Analyst Viewpoint

From an investment perspective, the Food and Beverage Metal Cans market offers both promising opportunities and certain risks that investors should consider. This growth is primarily fueled by the increasing demand for sustainable and convenient packaging solutions, particularly driven by the food industry’s shift towards ready-to-eat and premium products.

Consumer insights indicate a growing preference for metal cans due to their durability, recyclability, and the excellent protection they offer against external elements like air, light, and moisture. These attributes are especially valued in the ready-to-eat food segment, which demands packaging that can maintain the food’s freshness and nutritional value over time.

The technological front, innovations in can design and manufacturing have led to lighter, more durable cans with improved aesthetic appeal through advanced digital printing technologies. These advancements not only enhance the visual appeal but also contribute to cost reduction and environmental sustainability.

By Type

Two-Piece Cans Lead with 57.4% Market Share in Food and Beverage Packaging

In 2024, the 2 Piece Can segment held a commanding presence in the food and beverage metal cans market, securing more than a 57.4% share. This dominance is attributed to the can’s lightweight design and manufacturing efficiency, which offer significant cost advantages for producers and appeal to consumer preferences for sustainable packaging solutions.

The two-piece can design, typically fabricated from a single piece of metal with an added lid, simplifies the production process, resulting in faster production times and reduced material waste. This efficiency not only supports the industry’s push towards sustainability but also aligns with consumer demand for eco-friendly packaging, making it a preferred choice for a wide range of beverages and food products. As brands continue to prioritize durability and sustainability, the prominence of two-piece cans in the market is expected to maintain or even expand its market share.

By Raw Material

Aluminium Dominates with 67.1% in Metal Cans Market Due to Superior Properties

In 2024, aluminium was the most widely used raw material in the food and beverage metal cans market, capturing a substantial 67.1% market share. This dominance is primarily due to aluminium’s excellent corrosion resistance, lightweight nature, and complete recyclability, which align with the industry’s increasing focus on sustainability and efficiency.

Additionally, aluminium cans offer superior protection against light and oxygen, ensuring that the contents remain fresh and safe for extended periods. These advantages make aluminium the preferred choice for beverage manufacturers, particularly in the soda and beer sectors, where taste preservation is crucial. As consumers continue to prioritize environmental impact in their purchasing decisions, the preference for aluminium in metal can production is expected to remain robust, further cementing its leading position in the market.

By Capacity

330 ml – 500 ml Cans Claim 61.3% Market Share, Favored for Versatility

In 2024, cans with a capacity ranging from 330 ml to 500 ml dominated the food and beverage metal cans market, accounting for more than 61.3% of the market share. This segment’s leadership stems from the size’s perfect balance between volume and convenience, making it particularly popular among beverage manufacturers.

These cans are the preferred choice for a variety of drinks, including soft drinks, craft beers, and energy drinks, as they provide adequate quantity without being cumbersome for consumers. The size is also ideal for single servings, which aligns with growing consumer trends towards portion control and reducing waste. As the market continues to evolve, the 330 ml to 500 ml can size is poised to maintain its dominance, favored by both consumers and producers for its practicality and sustainability.

By Fabrication

Printed Cans Lead with 67.2% Share, Enhancing Brand Visibility

In 2024, printed cans held a dominant position in the food and beverage metal cans market, capturing more than a 67.2% share. This significant market share is attributed to the role of printed cans in marketing and brand differentiation, where vibrant designs and colors can attract consumer attention on crowded store shelves.

The printing technology used on these cans allows for high-quality, detailed graphics that are not only visually appealing but also resistant to fading and wear, crucial for maintaining brand integrity throughout the product’s shelf life. This capability is especially valued in sectors where competition is fierce, and branding can significantly influence consumer choices. As brands increasingly seek to stand out through unique packaging, the demand for printed metal cans is expected to remain strong, underpinning their substantial share in the market.

By Degree of Internal Pressure

Pressurized Cans Command 71.9% Market Share, Preferred for Product Integrity

In 2024, pressurized cans emerged as the leading segment in the food and beverage metal cans market, securing more than a 71.9% share. This dominant market share reflects the preference for pressurized cans in preserving and extending the shelf life of carbonated beverages such as sodas and sparkling waters, as well as certain alcoholic drinks.

The technology behind pressurized cans involves incorporating a small amount of pressure within the can to maintain the carbonation and freshness of the contents, which is crucial for taste and quality over time. This feature is particularly important for manufacturers who aim to deliver consistent, high-quality products to consumers who value taste and longevity. The significant share of pressurized cans is expected to be sustained as they continue to be the go-to choice for ensuring product integrity in the beverage sector.

By Application

Beverage Cans Dominate with 67.8% Share, Essential for Drink Packaging

In 2024, beverage cans held a dominant market position in the food and beverage metal cans sector, capturing more than a 67.8% share. This substantial market presence reflects the critical role these cans play in the packaging and distribution of a wide range of drinks, from carbonated sodas and energy drinks to beers and sparkling waters. Beverage cans are favored for their durability, light weight, and ability to preserve the flavor and carbonation of contents, which are key factors for manufacturers and consumers alike.

Additionally, their ease of recycling aligns with growing environmental concerns, making them a preferred choice in efforts to combine sustainability with convenience. This segment’s continued dominance is supported by ongoing innovations in can design and materials that enhance the consumer experience while maintaining product quality.

Key Market Segments

By Type

- 1 Piece Can

- 2 Piece Can

- 3 Piece Can

By Raw Material

- Steel

- Aluminium

By Capacity

- Below 330 ml

- 330 ml – 500 ml

- Above 500 ml

By Fabrication

- Plain

- Embossed

- Printed

- Others

By Degree of Internal Pressure

- Pressurized Cans

- Vacuum Cans

By Application

- Food Cans

- Fruits & Vegetables

- Meat & Seafood

- Pet Food

- Ready-To-Eat Food

- Others

- Beverage Cans

- Alcoholic Beverages

- Non-Alcoholic Beverages

Drivers

Increased Demand for Sustainable Packaging Drives Growth in Metal Cans Market

One of the major driving factors for the growth of the food and beverage metal cans market is the increasing consumer and manufacturer demand for sustainable packaging solutions. As awareness regarding environmental issues rises, both consumers and regulatory bodies are pushing for packaging materials that can be recycled effectively and have a minimal ecological footprint. Metal cans, predominantly made from aluminum and steel, meet these criteria as they are 100% recyclable without loss of quality.

According to the Environmental Protection Agency (EPA), recycling aluminum cans saves around 92% of the energy required to produce new cans from raw materials. This substantial energy saving has encouraged beverage manufacturers to choose metal cans over other alternatives like plastic, which is less efficient to recycle and more harmful to the environment. Moreover, the Aluminum Association has noted that nearly 75% of all aluminum ever produced is still in use today, thanks to effective recycling processes.

Government initiatives also play a crucial role in this trend. For instance, several U.S. states have implemented beverage container deposit laws, which incentivize consumers to return their metal beverage cans for recycling by offering a small cash refund. These legislative measures have not only increased recycling rates but have also promoted the use of recyclable materials like metal in beverage packaging.

Restraints

Rising Raw Material Costs Challenge Metal Cans Market Growth

A significant restraining factor for the growth of the food and beverage metal cans market is the volatility and rising costs of raw materials such as aluminum and steel. These materials are fundamental in the production of metal cans, and their prices can fluctuate widely due to changes in the global commodities market, affecting manufacturers’ operating expenses and profit margins.

For instance, the London Metal Exchange (LME) reported that aluminum prices have seen a sharp increase, influenced by factors such as trade policies, tariffs, and global economic dynamics. This rise in costs is compounded by the energy-intensive nature of metal can production, which also faces price variability in energy supplies, further straining manufacturers.

Moreover, while metal cans are highly recyclable, the initial costs associated with establishing or upgrading recycling facilities can be high. Government regulations and policies aimed at reducing waste and promoting recycling add another layer of financial burden on manufacturers. These policies, while beneficial for the environment, require significant investment in technology and processes to ensure compliance, adding to the overall cost structure of can production.

Opportunity

Expansion into Emerging Markets Presents Major Growth Opportunity for Metal Cans

One significant growth opportunity for the food and beverage metal cans market lies in expanding into emerging markets. These regions are experiencing rapid urbanization, rising income levels, and changing consumer behaviors, which are collectively driving an increased demand for packaged foods and beverages.

Countries in Asia, Africa, and Latin America, where the penetration of canned products is still relatively low compared to developed regions, represent untapped potential for metal can manufacturers. For example, the United Nations Economic and Social Commission for Asia and the Pacific (ESCAP) reports that urban populations in these areas are expected to double in the next few decades, leading to a surge in consumer demand for convenient, safe, and sustainable packaging options like metal cans.

In addition to demographic shifts, government initiatives across these regions are promoting the adoption of sustainable practices in the food and beverage industry. This includes incentives for using eco-friendly materials and support for recycling infrastructure developments, which align well with the inherent recyclability of metal cans. Such policies not only support environmental goals but also enhance the appeal of metal cans to environmentally conscious consumers.

Moreover, with the global push towards reducing plastic waste, metal cans offer a viable and environmentally friendly alternative that can meet both consumer expectations and regulatory standards. The combination of consumer preference for sustainable packaging and supportive government policies creates a conducive environment for the growth of the metal can market in these emerging regions.

Trends

Innovative Smart Packaging Technologies Revolutionize Metal Cans

A major trend shaping the future of the food and beverage metal cans market is the adoption of innovative smart packaging technologies. These advancements are not only enhancing the functionality of metal cans but are also improving consumer engagement and product safety.

Smart packaging involves the integration of technologies such as QR codes, NFC (Near Field Communication), and RFID (Radio Frequency Identification) tags into traditional packaging formats. These technologies allow consumers to interact with the packaging via their smartphones, providing access to a wealth of information including nutritional content, product origin, recycling instructions, and even augmented reality experiences. For example, a consumer could scan a QR code on a beverage can to watch promotional videos, participate in contests, or read about the beverage’s production process.

This trend is driven by the increasing consumer demand for transparency and connectivity. According to a survey by the Food Marketing Institute, over 75% of consumers are more likely to purchase a product if they have easy access to detailed information about it, such as what it contains and how it is made. By leveraging smart technologies, metal can manufacturers can meet this demand, offering a more informative and interactive experience.

Government initiatives that support food safety and consumer rights are also playing a role in promoting smart packaging. Regulations that require detailed labeling and traceability encourage manufacturers to adopt advanced technologies that can provide such information efficiently and reliably.

Regional Analysis

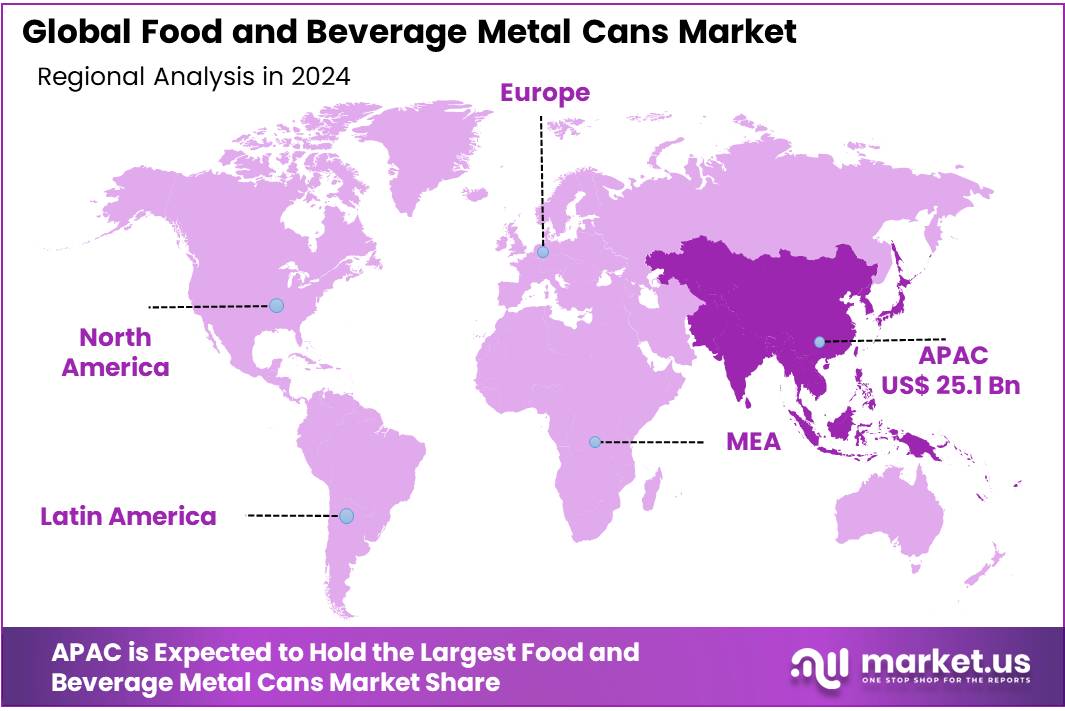

Asia-Pacific Leads Global Food & Beverage Metal Cans Market with 52.8% Share, Valued at USD 25.1 Billion

In 2024, the Asia-Pacific (APAC) region emerged as the dominant force in the global food and beverage metal cans market, capturing a substantial 52.8% share and reaching a market value of approximately USD 25.1 billion. This leadership is fueled by rapid urbanization, rising disposable incomes, and a growing demand for convenient, sustainable packaging solutions across countries like China, India, and Japan.

This growth is driven by stringent government regulations aimed at reducing plastic waste and a surge in demand for energy drinks, canned coffee, and functional beverages. The country’s rapid expansion in the beverage industry and increased investments in advanced can production further bolster this trend.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

P. Wilkinson Containers Ltd is a prominent UK-based manufacturer specializing in metal and plastic containers for the food and beverage industry. Known for their commitment to sustainability and innovation, they offer a range of bespoke packaging solutions that cater to a variety of market needs. Their focus on customer-specific designs and their ability to supply both small and large quantities make them a versatile choice for businesses looking for tailored packaging solutions.

Ardagh Group S.A. is a global leader in packaging solutions, primarily producing glass and metal products. In the food and beverage sector, their metal cans are known for their durability and recyclability, aligning with global sustainability trends. Ardagh’s significant investment in cutting-edge technology and its vast geographical footprint enable it to serve major international clients, reinforcing its position as a key player in the metal cans market.

Ball Corporation is a major player in the packaging industry, renowned for its production of aluminum cans. With a strong focus on sustainable packaging solutions, Ball Corporation continuously innovates to reduce the environmental impact of its products. Their operations span across several continents, allowing them to cater to a diverse global clientele with high efficiency and reliability in supply.

Top Key Players in the Market

- P. Wilkinson Containers Ltd

- Ardagh Group S.A.

- Ball Corporation

- Canpack S.A.

- CCL Container, Inc.

- CPMC Holdings Ltd

- Crown Holdings, Inc.

- Envases Group

- Independent Can Company

- Kian Joo Can Factory Berhad

- Masilly Holdings S.A.S.

- Mauser Packaging Solution LLC

- Muller und Bauer GmbH

- Silgan Holdings, Inc.

- Toyo Seikan Group Holding Ltd.

- Universal Can Corporation

- Visy

Recent Developments

P. Wilkinson Containers Ltd has carved a niche in the Food and Beverage Metal Cans Market as a leading manufacturer and stockist in the UK, specializing in both metal and plastic containers. The company’s expertise spans across various container sizes, ranging from small 50ml units to large 220L containers, catering to a diverse range of packaging needs.

In 2024, Canpack’s financial results reflected a positive trajectory, with net sales rising by 13% and adjusted EBITDA increasing to $590 million, up from $411 million in the previous year. These gains were largely attributed to higher sales volumes and efficient operational performance, particularly in the U.S., where energy costs were lower.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 47.7 Bn |

| Forecast Revenue (2034) | USD 94.7 Bn |

| CAGR (2025-2034) | 7.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (1 Piece Can, 2 Piece Can, 3 Piece Can), By Raw Material (Steel, Aluminium), By Capacity (Below 330 ml, 330 ml – 500 ml, Above 500 ml), By Fabrication (Plain, Embossed, Printed, Others), By Degree of Internal Pressure (Pressurized Cans, Vacuum Cans), By Application (Food Cans, Beverage Cans, Alcoholic Beverages, Non-Alcoholic Beverages) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | P. Wilkinson Containers Ltd, Ardagh Group S.A., Ball Corporation, Canpack S.A., CCL Container, Inc., CPMC Holdings Ltd, Crown Holdings, Inc., Envases Group, Independent Can Company, Kian Joo Can Factory Berhad, Masilly Holdings S.A.S., Mauser Packaging Solution LLC, Muller und Bauer GmbH, Silgan Holdings, Inc., Toyo Seikan Group Holding Ltd., Universal Can Corporation, Visy |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |