Quick Navigation

Report Overview

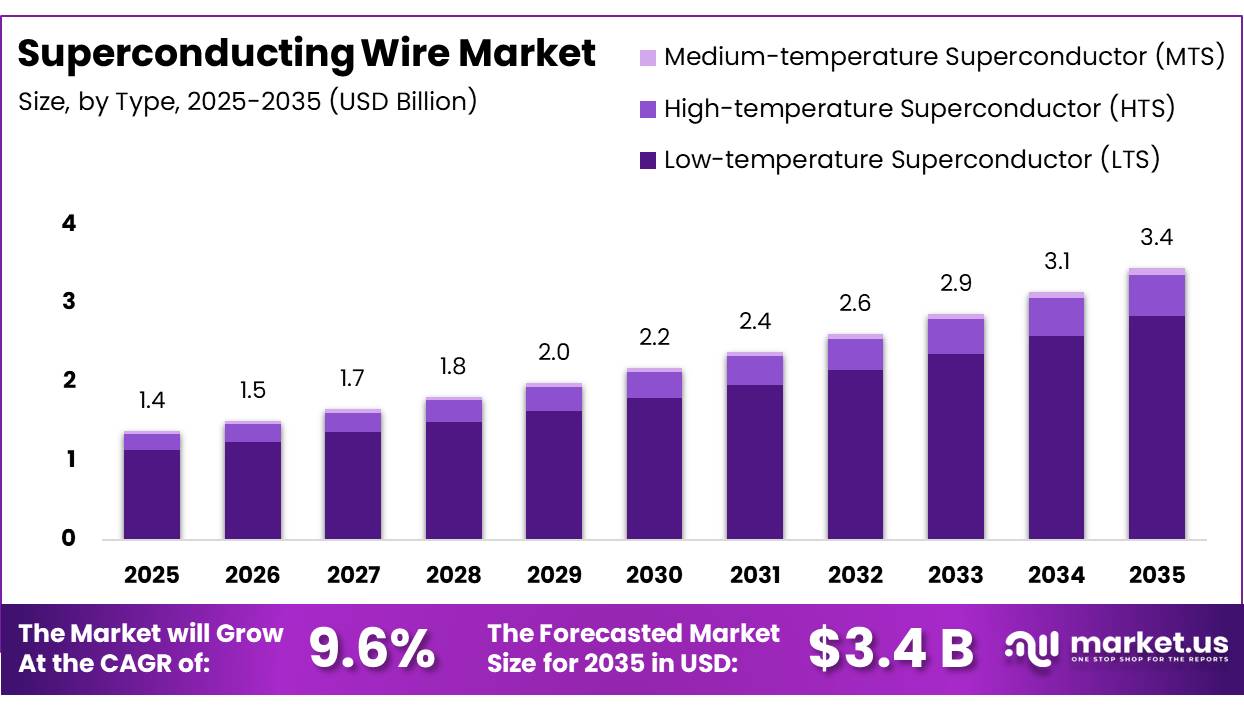

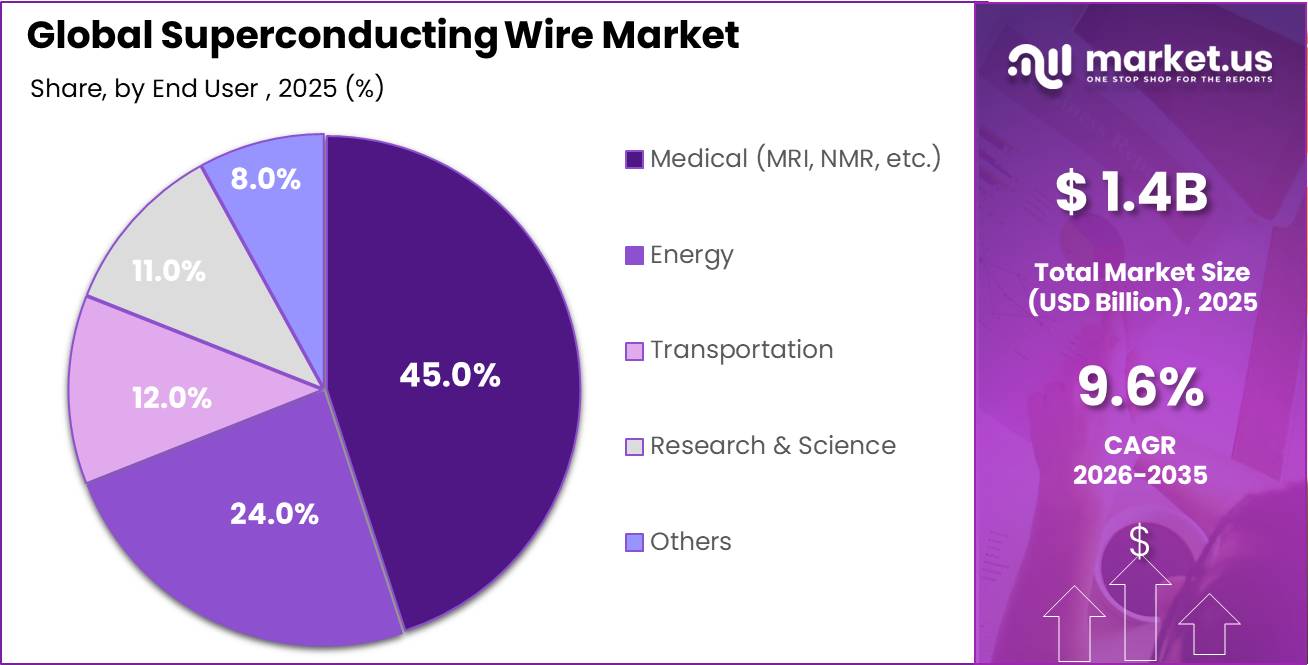

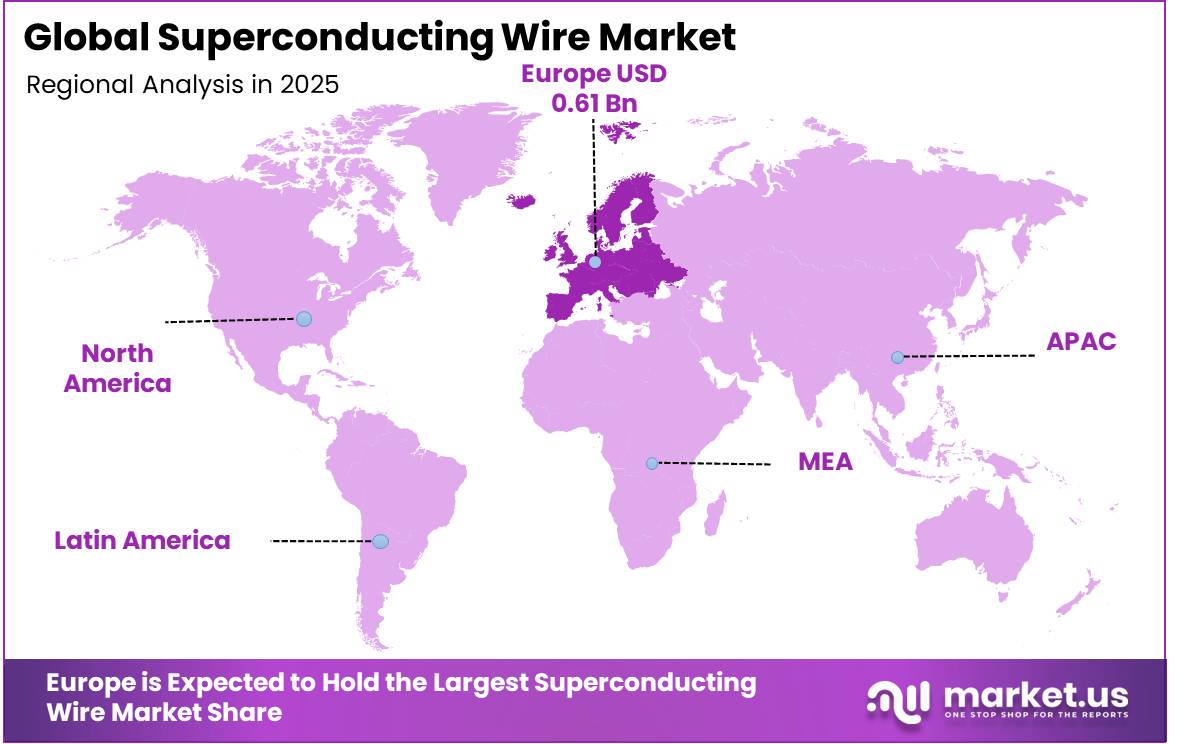

In 2025, the Global Superconducting Wire Market was valued at US$1.4 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 9.6%, reaching about US$3.4 billion by 2035. Europe held a dominant market position, capturing more than a 43.9% share, holding USD 0.61 billion in revenue.

Superconducting wire market is an advanced energy-materials industry built around low-temperature and high-temperature conductors used in MRI magnets, research systems, power equipment, fusion magnets, transport, and grid technologies. The U.S. Department of Energy explains that superconducting materials can conduct direct current without energy loss when cooled below a critical temperature, while superconducting wires support very high currents and enable powerful wound coils. This makes the product important for high-field magnets, efficient power systems, and compact electrical equipment.

- The industrial scenario is supported by strong demand from medical imaging and large scientific infrastructure. OECD Health at a Glance 2025 stated that MRI availability has increased rapidly in most OECD countries, while MRI examinations more than doubled in Korea and Latvia and increased by around 70% in France between 2013 and 2023.

- In fusion, ITER uses the largest integrated superconducting magnet system ever built, with 10,000 tonnes of magnets and 51 GJ of stored magnetic energy. Its Nb3Sn strand procurement exceeded 500 metric tonnes and more than 100,000 km, supplied by 9 producers.

Key Takeaways

- The global superconducting wire market was valued at USD 1.4 billion in 2025.

- The global superconducting wire market is projected to grow at a CAGR of 9.6% and is estimated to reach USD 3.4 billion by 2035.

- On the basis of type, the Low-temperature Superconductor (LTS) dominated the market, constituting 82.4% of the total market share.

- Based on the end user, the Medical segment (MRI, NMR, etc.) dominated the superconducting wire market, with a substantial market share of around 45.0%.

- Based on the application, Magnetic Resonance Imaging (MRI) led the market, comprising 38.0% of the total market.

- Among the sales channels, the Direct sales channel held a major share in the superconducting wire market, accounting for 68.0% of the market share.

- In 2025, Europe was the most dominant region in the superconducting wire market, accounting for 43.9% of the total global consumption.

Growth is driven by grid modernization, clean-energy integration, and higher investment in advanced conductors. IEA’s Electricity 2026 report noted that more than 2,500 GW of renewable, storage, and large-load projects were stalled in grid queues worldwide, while annual grid investment must rise by about 50% from today’s USD 400 billion by 2030. This creates future opportunities for superconducting cables, fault current limiters, compact motors, and high-efficiency transmission systems. The U.S. DOE’s ARPA-E also announced USD 10 million for 3 projects to develop and domestically manufacture high-performance superconducting tapes, supporting fusion, electric grids, motors, and aviation applications.

Type Analysis

Low-temperature Superconductor (LTS) dominates due to its proven use in high-field magnet systems.

In 2025, Low-temperature Superconductor (LTS) held a dominant market position, capturing more than a 82.4% share in the superconducting wire market by type. In June 2025, this segment led because LTS wires were widely used in established applications such as MRI, NMR, research magnets, and other high-performance magnet systems. Their stable performance, proven reliability, and long commercial use made them the preferred choice for industries that require strong magnetic fields and consistent operating safety.

High-temperature Superconductor (HTS) emerged as the growing segment in 2025, supported by rising interest in energy systems, compact power equipment, advanced grid applications, and next-generation superconducting technologies.

End User Analysis

Medical applications dominate due to strong use in MRI and NMR systems.

In 2025,Medical (MRI, NMR, etc.) held a dominant market position, capturing more than a 45.00% share in the superconducting wire market by end user. In June 2025, this segment led because superconducting wires remained essential in MRI and NMR systems, where powerful and stable magnetic fields are required. Hospitals, diagnostic centers, research laboratories, and healthcare equipment makers continued to depend on superconducting wires for reliable imaging and scientific testing performance.

Energy emerged as the growing segment in 2025, driven by increasing interest in superconducting cables, power grid infrastructure, fault current limiters, and high-efficiency electrical systems.

Application Analysis

Magnetic Resonance Imaging (MRI) dominates due to its strong need for superconducting magnet systems.

In 2025, Magnetic Resonance Imaging (MRI) held a dominant market position, capturing more than a 38.0% share in the superconducting wire market by application. In June 2025, this segment led because MRI systems depend heavily on superconducting wires to generate stable magnetic fields for medical imaging. The segment remained supported by steady demand from hospitals, diagnostic imaging centers, and medical technology providers that require reliable magnet performance and long operating life.

Power Grid Infrastructure emerged as the growing segment in 2025, supported by rising focus on efficient electricity transmission, grid modernization, and advanced superconducting power technologies.

Sales Channel Analysis

Direct dominates with 68.0% due to strong buyer preference for customized supply and technical support.

In 2025, Direct held a dominant market position, capturing more than a 68.0% share in the superconducting wire market by sales channel. In June 2025, this segment led because superconducting wire is a highly technical product that often requires direct coordination between producers and end users. Medical equipment makers, energy companies, research labs, and advanced technology buyers preferred direct purchasing for better product specifications, quality checks, pricing discussions, and after-sales support. Direct sales also helped suppliers manage long-term contracts and application-specific requirements more effectively.

Indirect emerged as the growing segment in 2025, supported by rising demand from smaller buyers, regional distributors, and specialized suppliers serving research, medical, and industrial users.

Key Market Segments

By Type

- Low-temperature Superconductor (LTS)

- High-temperature Superconductor (HTS)

- Medium-temperature Superconductor (MTS)

By End User

- Medical (MRI, NMR, etc.)

- Energy

- Transportation

- Research & Science

- Others

By Application

- Magnetic Resonance Imaging (MRI)

- Power Grid Infrastructure

- Superconducting Fault Current Limiters (SFCL)

- Maglev Transportation

- Others

By Sales Channel

- Direct

- Indirect

Driver Analysis

Fusion magnet build-out lifting REBCO tape pull-through

Fusion is the single strongest structural accelerator for high-temperature superconducting wire because it converts superconducting tape from a specialty component into a critical-path material for compact, high-field magnet architectures. Commonwealth Fusion Systems disclosed in 2024 that its PIT VIPER cable can carry 50 kiloamps, tolerate 300 megapascals of pressure, and withstand 1,000 kilonewtons of force per meter, which materially validates the mechanical and electrical loading case for REBCO-based fusion magnets rather than only lab-scale demonstrations.

By late 2025, Tokamak Energy reported a complete HTS magnet system reaching 11.8 tesla at -243 degrees Celsius under fusion-relevant conditions, reinforcing that commercial fusion programs are moving from concept funding toward hardware qualification and procurement discipline. This matters commercially because fusion developers buy not only tape but also engineered cable stacks, quench monitoring, insulation systems, and cryogenic integration, lifting revenue per installed kiloamp-meter and improving supplier pricing power. The CAGR effect is strongest in North America and the UK because private fusion capital formation remains concentrated there, but Japan, South Korea, China, and EU research ecosystems also support a widening procurement base for REBCO conductors and ancillary magnet components.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fusion magnet build-out lifting REBCO tape pull-through | +2.6% | North America core, UK, EU labs, Japan, South Korea, China | Medium term (2-4 years) |

| Grid densification and HTS cable economics in constrained corridors | +2.1% | North America urban nodes, EU, Japan, South Korea, offshore links | Medium term (2-4 years) |

| Public funding for domestic HTS tape manufacturing scale-up | +1.7% | US core, EU selective, Japan, China | Short term (≤ 2 years) |

| Data-center power intensity creating niche HTS distribution use cases | +1.4% | US core, Nordic hubs, Ireland, Japan, Singapore spill-over | Short term (≤ 2 years) |

| MRI and high-field scientific magnet refresh sustaining base demand | +1.2% | North America, EU, Japan, China | Medium term (2-4 years) |

| Capacity expansion and reliability gains reducing adoption friction | +1.9% | US, Japan, EU, China supply chain | Short term (≤ 2 years) |

Restraint Analysis

High tape cost

Superconducting wire remains structurally expensive because the product is not a simple commodity conductor but a precision-engineered layered material with tight process control, low defect tolerance, and expensive precursor chemistry, and the market still depends heavily on specialty HTS formats where scale is insufficient to force costs down quickly. Industry evidence indicates that advanced REBCO development efforts have explicitly targeted a 10x wire-price reduction to around $33 per kiloamp-meter, while other recent literature still frames near-term commercial viability as requiring further reduction toward roughly $50 per kiloamp-meter, which shows how far the cost curve remains from broad utility economics.

That cost structure compresses gross margins for downstream integrators because project economics must absorb not only conductor price but also cryostat design, cryogenic plant, cabling, and installation risk, so many utility and industrial buyers defer CapEx until a clearer ROI threshold emerges. In practical terms, the restraint is most acute in North America, the EU, and Japan, where buyers are sophisticated but cost disciplined, making the near-term CAGR hit large even when technical demand is real.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High tape cost | -2.4% | North America core, EU, Japan | Short term (≤ 2 years) |

| Thin testing base | -1.8% | Global, APAC corridors | Short term (≤ 2 years) |

| Long qualification cycles | -1.6% | North America, EU, Japan, Korea | Medium term (2-4 years) |

| Limited capacity | -2.1% | US, Japan, EU supply chain | Short term (≤ 2 years) |

| Cryogenic Opex burden | -1.5% | Urban grids, data centers, Europe, Japan | Medium term (2-4 years) |

| Tariff and policy risk | -1.3% | US, EU, China-linked trade lanes | Medium term (2-4 years) |

Opportunity Analysis

Aviation electrification (MgB2 HTS)

Electrified aircraft propulsion is a genuine white-space opportunity because current baselines for superconducting wire largely discount aviation demand as speculative, yet NASA’s work with fine-filament magnesium diboride (MgB2) conductors for future electrified aircraft demonstrates a credible path to high-current-density, lower-weight systems in the 2030s.

If even 5% to 10% of projected narrow-body and regional aircraft deliveries in the 2030–2035 window adopt partial superconducting propulsion or power distribution subsystems, and each airframe embeds tens of kiloamp-meters of MgB2 or related superconducting wire, the cumulative TAM could reach multiple billions of dollars of incremental conductor value, with EBIT margins 300–500 basis points higher than grid conductors due to certification intensity and performance criticality.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Aviation electrification (MgB2 HTS) | +2.3% | North America core, EU, Japan | Medium term (2-4 years) |

| AI / HPC campus HTS microgrids | +2.0% | US core, EU, APAC data hubs | Short term (≤ 2 years) |

| Outcome-based grid availability contracts | +1.7% | North America, EU, Japan | Medium term (2-4 years) |

| HTS manufacturing platform licensing | +1.8% | US, Japan, EU, China | Medium term (2-4 years) |

| Superconducting urban rail and maglev retrofits | +1.5% | China core, EU, Japan, Korea | Long term (≥ 4 years) |

| Consolidation of niche LTS/HTS suppliers via M&A roll-ups | +1.9% | Global, North America and Asia-Pacific | Short term (≤ 2 years) |

Challenges Analysis

Complex multi-step processing

Complex multi-step processing remains a systemic challenge because modern REBCO and other HTS conductors require precise multilayer deposition, substrate preparation, and post-processing over hundreds of meters, and each step adds time, defect risk, and engineering overhead that hold back throughput and cost-down curves, even though sales continue. Scientific and industry analyses highlight utilization rates of REBCO targets below 50% and mention long delivery times for implementing new process recipes, implying that a large portion of capital equipment sits underutilized while process engineers iterate on reactor designs, film thickness (e.g., around 5 µm), and dopant distributions such as 10x barium zirconate density.

This friction increases per-meter conversion cost, stretches lead times by several months when new product variants or higher-field specifications are introduced, and forces manufacturers to maintain higher working capital buffers to accommodate process tuning, collectively shaving roughly 1–1.5 percentage points off the maximum achievable CAGR until next-generation reactors and integrated lines can be widely deployed.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Complex multi-step processing | -1.4% | US, EU, Japan, China | Medium term (2-4 years) |

| Yield volatility and QA burden | -1.2% | North America, Asia-Pacific lines | Medium term (2-4 years) |

| Cryogenic skills shortage | -1.0% | EU labs, US fusion, APAC hubs | Long term (≥ 4 years) |

| Application selection uncertainty | -0.9% | Global, EU regulatory hubs | Medium term (2-4 years) |

| Long integration and testing cycles | -1.1% | North America, EU, Japan | Long term (≥ 4 years) |

| CapEx intensity and financing complexity | -1.3% | Global, APAC logistics corridors | Medium term (2-4 years) |

Geopolitical Impact Analysis

Geopolitical Realignment and Strategic Metal Security Reshaping Superconducting Wire Manufacturing.

Current geopolitical tensions are reshaping the superconducting wire market through strategic metal access, tariff exposure, technology-security policies, and regional sourcing pressure. Superconducting wires require highly specialized inputs such as tin, titanium, copper, silver, yttrium, and advanced substrates. As these materials are also linked to defence, electronics, power infrastructure, and advanced manufacturing, buyers are becoming more cautious about supplier concentration, cross-border controls, and long qualification cycles.

- In 2026, tin and titanium supply remained important risk areas for superconducting wire producers. The U.S. Geological Survey estimated global tin mine production at 290,000 metric tons in 2025, with China producing 71,000 metric tons and Indonesia 61,000 metric tons. Tin remains important for Nb3Sn-based superconducting wires. For titanium sponge, USGS estimated global production at 370,000 metric tons in 2025, with Japan at 53,000 metric tons, Russia at 25,000 metric tons, and Kazakhstan at 16,000 metric tons. These concentrated supply points can affect input planning for NbTi-related wire systems.

Trade policy is also adding cost pressure. In August 2025, the U.S. Federal Register confirmed a 50% tariff on semi-finished copper products and intensive copper derivative products, effective from August 1, 2025. Since copper is widely used as a stabilizer and conductive support in superconducting wire systems, tariff-led cost changes can influence procurement and regional manufacturing strategies.

In April 2026, the European Commission also identified superconducting materials as part of advanced materials, linking them with autonomy, safety, sustainability, and industrial competitiveness. This is pushing more attention toward secure local supply chains, advanced material standards, and regional technology capability.

Regional Analysis

Europe dominates with 43.9% due to strong medical, research, and energy technology demand.

In 2025, Europe held a dominant market position in the superconducting wire market, capturing more than a 43.9% share, valued at USD 0.61 Bn. In June 2025, the region led due to its strong base in medical imaging, high-field research magnets, clean-energy infrastructure, and advanced electrical systems. European demand was supported by large scientific programs using superconducting magnet technology

CERN reported in February 2026 that High-Luminosity LHC work included niobium-tin superconducting magnets for advanced accelerator applications. Europe’s power-grid investment needs also supported future demand, as Reuters reported in September 2025 that the EU requires €477 billion for transmission and €730 billion for distribution networks by 2040.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global superconducting wire market is highly specialised and competitive, where staying ahead means constantly improving technology, scaling up production, and building reliable supply chains. Leading manufacturers focus heavily on material innovation developing advanced REBCO-coated conductors, improved niobium-titanium and niobium-tin wire configurations, and next-generation HTS tape designs that deliver better current-carrying capacity, stronger thermal stability, and superior mechanical performance for the most demanding medical, energy, and research applications.

Companies American Superconductor Corporation (AMSC), Bruker Corporation, Furukawa Electric Co., Sumitomo Electric Industries, and SuperPower Inc. are also investing heavily in expanding their HTS wire manufacturing capabilities, as higher-temperature superconducting solutions provide significant operational cost advantages over conventional LTS systems and are increasingly preferred by power utilities, fusion energy projects, and transportation authorities.

Market Key Players

- Fujikura Ltd.

- Sumitomo Electric Industries, Ltd.

- Furukawa Electric Co., Ltd.

- Bruker Corporation

- Luvata (Mitsubishi Materials Group)

- Superconductor Technologies Inc. (STI)

- Western Superconducting Technologies Co., Ltd.

- SuperPower Inc. (Furukawa)

- SHSC (Shanghai Superconductor Technology Co., Ltd.)

- LS Cable & System Ltd.

- Nexans S.A.

- SuNam Co., Ltd.

- American Superconductor Corporation (AMSC)

- THEVA Dünnschichttechnik GmbH

- ASG Superconductors S.p.A.

- Others

Key Development

- In July 2025, Bruker Corporation announced a strategic collaboration with a leading global technology company to expand its superconducting wire product portfolio into quantum computing applications, a significant step toward diversifying its revenue base beyond traditional medical and scientific research segments and establishing the company at the forefront of the emerging quantum technology supply chain.

- In August 2025, American Superconductor Corporation (AMSC) formed a strategic partnership with a leading renewable energy company to develop and supply superconducting wire solutions specifically designed for offshore wind and grid-scale energy storage applications, demonstrating the company’s commitment to meeting rising demand from the global clean energy transition.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.4 Bn |

| Forecast Revenue (2035) | USD 3.4 Bn |

| CAGR (2026-2035) | 9.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Low-temperature Superconductor (LTS), High-temperature Superconductor (HTS), and Medium-temperature Superconductor (MTS)), By End User (Medical (MRI, NMR, etc.), Energy, Transportation, Research & Science, and Others), By Application (Magnetic Resonance Imaging (MRI), Power Grid Infrastructure, Superconducting Fault Current Limiters (SFCL), Maglev Transportation, and Others), By Sales Channel (Direct and Indirect) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Fujikura Ltd., Sumitomo Electric Industries Ltd., Furukawa Electric Co. Ltd., Bruker Corporation, Luvata (Mitsubishi Materials Group), Superconductor Technologies Inc. (STI), Western Superconducting Technologies Co. Ltd., SuperPower Inc. (Furukawa), SHSC (Shanghai Superconductor Technology Co. Ltd.), LS Cable & System Ltd., Nexans S.A., SuNam Co. Ltd., American Superconductor Corporation (AMSC), THEVA Dünnschichttechnik GmbH, ASG Superconductors S.p.A., and several other. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |