Quick Navigation

Report Overview

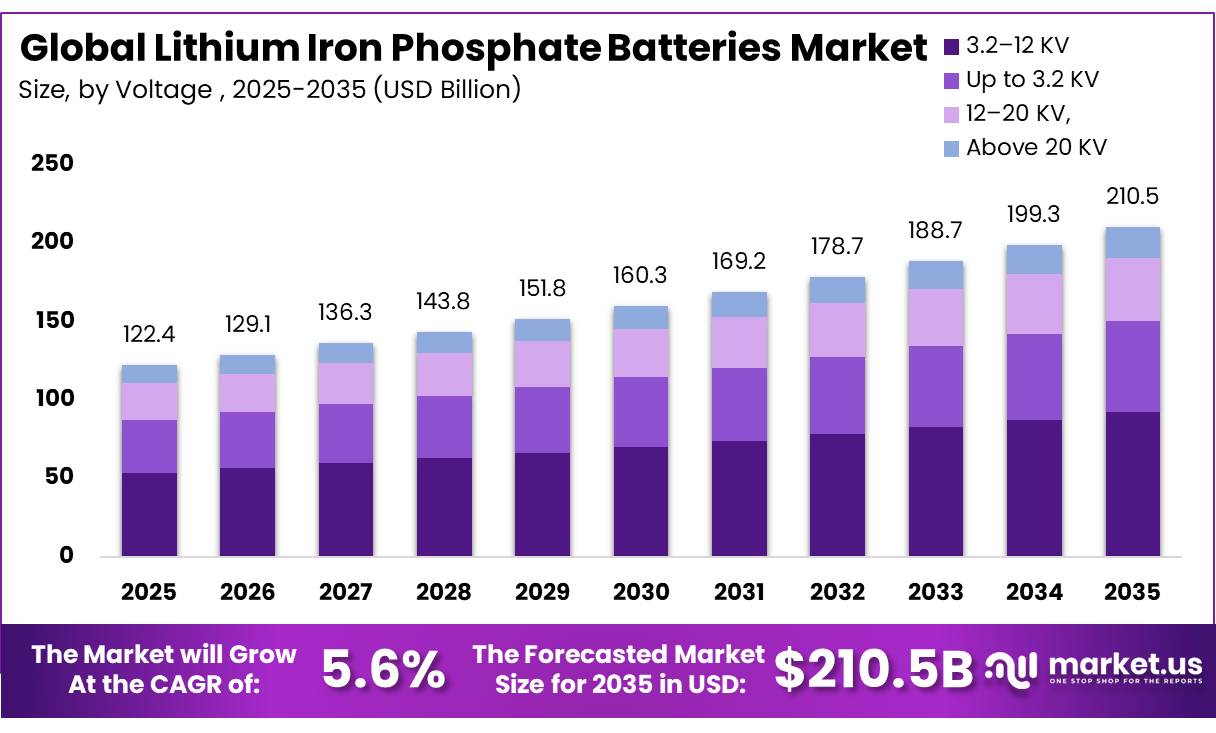

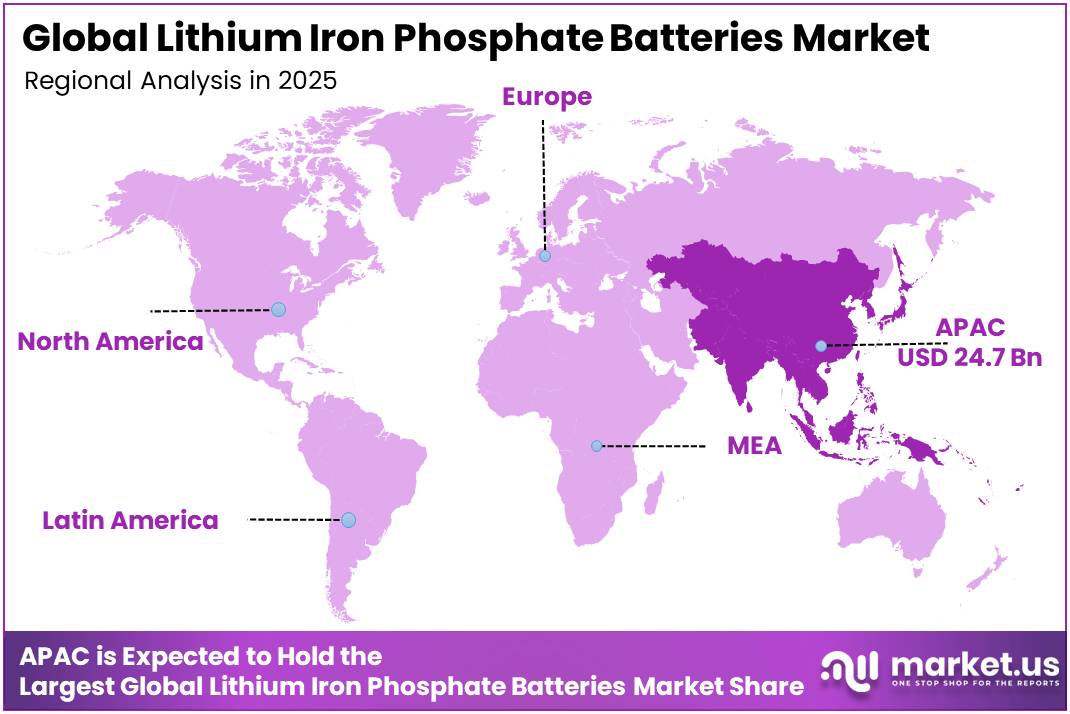

The Global Lithium Iron Phosphate Batteries Market size is expected to be worth around USD 209.7 Billion by 2035, from USD 47.8 Billion in 2025, growing at a CAGR of 16.0% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 76.0% share, holding USD 36.3 Billion revenue.

Lithium Iron Phosphate (LFP) batteries are gaining strong industrial importance because they offer lower cost, better thermal safety, long cycle life, and reduced dependence on nickel and cobalt. In 2024, LFP batteries accounted for nearly half of the global EV battery market, while in China they met almost three-fourths of domestic EV battery demand. Their share in China reached around 80% of batteries sold in November and December 2024, showing that automakers are using LFP chemistry to reduce EV prices and improve supply stability.

- In 2024, global battery demand across the energy sector reached about 1 TWh, while EV battery demand alone crossed 950 GWh, rising 25% from 2023. Electric cars accounted for more than 85% of EV battery demand, showing how strongly transport electrification is shaping LFP battery use.

Key Takeaways

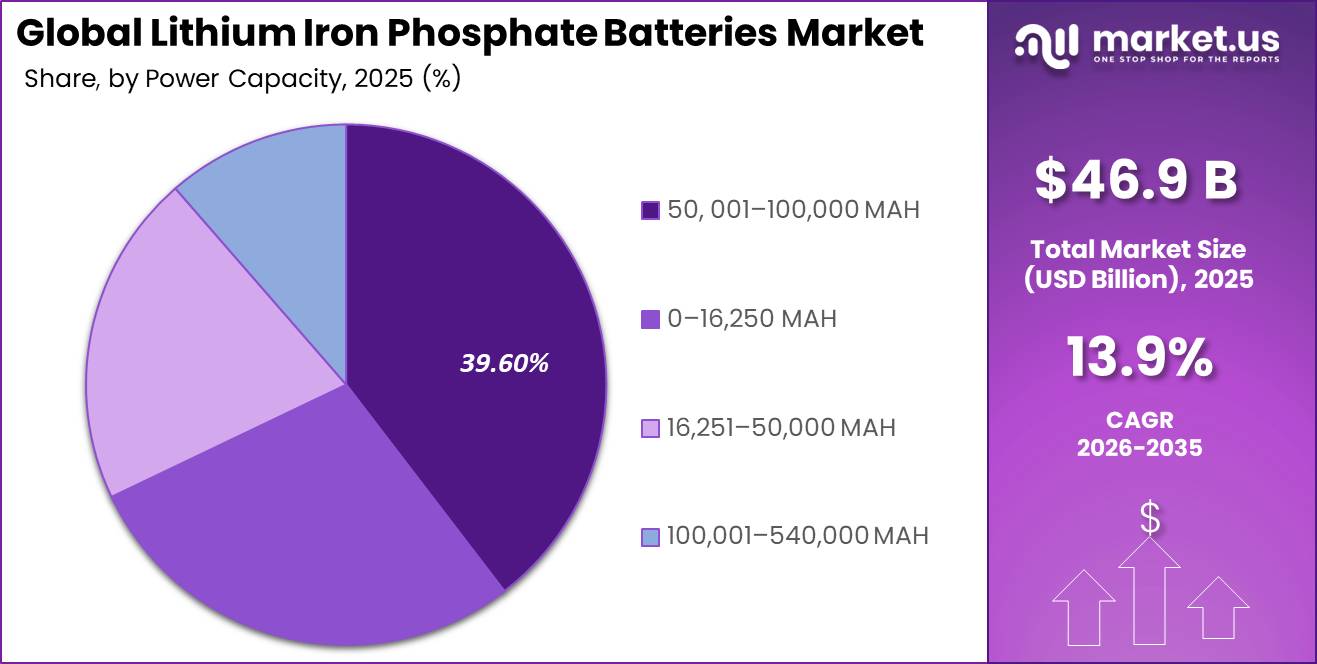

- The Lithium Iron Phosphate Battery Market was valued at USD 47.8 billion in 2025.

- The global Market is projected to grow at a CAGR of 16% and is estimated to reach USD 209.7 billion by 2035.

- On the basis of battery type, the prismatic battery segment dominated the market, constituting around 73.0% of the total market share.

- Based on voltage, the low voltage battery segment held a substantial market share of approximately 45.9%.

- Among end-users, the automotive sector dominated the battery market, accounting for nearly 56.1% of the total market share.

- In 2025, Asia Pacific emerged as the dominant region in the global battery market, accounting for around 76.0% of the total global consumption.

The fast growth in electric vehicles, stationary energy storage, and renewable power integration. LFP batteries are especially suitable for mass-market EVs, buses, commercial vehicles, and grid storage, where safety, cost, and durability matter more than maximum energy density. Government policies in the U.S., Europe, and China are also pushing local battery manufacturing and supply-chain security. The U.S. Department of Energy has highlighted LFP as a lower-cost cell chemistry that can benefit from domestic production incentives under advanced battery supply-chain programs.

The major driving factor is cost competitiveness. LFP batteries avoid high-cost nickel and cobalt, helping manufacturers manage raw-material price risk. The chemistry also supports longer service life; BYD states its Blade Battery is an LFP battery developed through 29 years of innovation and designed for more than 5,000 charging cycles, compared with around 1,000–2,000 cycles for many conventional alternatives. This makes LFP attractive for fleet operators, energy-storage developers, and consumers looking for lower lifetime ownership cost.

Government initiatives are also supporting future growth. The U.S. Department of Energy’s Battery Materials Processing Grants Program provides USD 3 billion to expand domestic battery materials processing and manufacturing capacity. In Europe, the battery value-chain IPCEI supports activities from raw material extraction to cell manufacturing, packs, recycling, and disposal, with sustainability as a central focus.

These measures are expected to increase regional LFP production, reduce import dependency, and create opportunities in cathode materials, recycling, battery packs, and stationary storage. In Europe, the Battery Regulation sets lithium recovery targets of 50% by 2027 and 80% by 2031, while the Critical Raw Materials Act targets 10% extraction, 40% processing, and 25% recycling capacity inside the EU by 2030.

CATL remains one of the strongest companies in the LFP battery ecosystem. In 2025, CATL reported lithium battery sales of 661 GWh, up 39% year-on-year, and held 39.2% of the global power battery market. Its energy storage battery shipments also represented 30.4% of the global market, supported by around 2,300 projects worldwide.

Type Analysis

Prismatic Batteries Are the Leading Segment in the Lithium Iron Phosphate Battery Market.

The prismatic battery forms the major part of the global battery market segment and holds around 73.0% market share because of its wide adoption in electric cars, energy storage, and several industrial uses. Their smaller size, increased energy density, more effective utilization of space, and improved thermal management systems make them ideal battery type to be used in the coming years for next-generation transportation and power storage purposes.

With the growing number of electric vehicles being manufactured each day and the rising installation of renewable power storage solutions, there is an increased need for prismatic batteries in the global market. Leading automotive companies have started relying on prismatic cells for their vehicles due to the efficiency in packaging, light-weight nature, and capacity to be scaled up. With rising investments in the battery gigafactory and other localized battery plants, the ecosystem for the manufacture of prismatic batteries is growing stronger.

Voltage Analysis

Low Voltage Batteries Accounted for a Significant Portion of the Lithium Iron Phosphate Battery Market.

Low voltage batteries lead in the world of Lithium Iron Phosphate battery market with a share of around 45.9% owing to wide utilization in electric vehicles, consumer electronics, industry, and portable energy storage systems. Low voltage batteries remain popular among consumers due to their efficient operation, compact size, reliable performance, and cost-effective nature, allowing users to choose them for a variety of uses. Their suitability for advanced electronic devices is an important factor influencing global demand within this segment.

The emergence of more electric vehicles and smart electronic gadgets is one of the factors that has greatly increased the use of low voltage batteries. Low voltage batteries are used to drive onboard electronics, entertainment systems, lighting systems, controllers, and other functions in automobiles, besides serving as key components apart from primary traction batteries. Portable consumer electronics such as mobile phones, laptops, and power tools have also seen increased use, accounting for billions of devices each year.

End User Analysis

The Battery Market Was Dominated by the Automotive Sector.

The automotive industry dominates the battery industry all over the world, with a market share of 56.1%, thanks to the growing popularity of electric cars. Batteries play an important role when it comes to electric vehicles because of their ability to provide constant energy, efficiency, and improved performance.

The government’s policy on using sustainable means of transportation increases the market growth for batteries. More new battery technologies are being adopted due to an increase in the use of electric vehicles because there is a need for batteries that can help drive farther and charge faster. There have been major efforts by manufacturers when it comes to battery system innovations and even building factories in their markets.

The Energy and Utilities segment was responsible for about 24.3% market share, supported by energy storage batteries for renewable sources. The Industrial category contributed 11.4% due to battery utilization in backup power supply and automation. The Consumer Electronics category had an almost 6.2% share, propelled by the use of portable electronics.

Key Market Segments

By Type

- Prismatic Battery

- Cylindrical Battery

- Pouch Battery

By Voltage

- Low Voltage

- Medium Voltage

- High Voltage

By End-User

- Automotive

- Energy and Utilities

- Industrial

- Consumer Electronics

- Others

Driver Analysis

Renewable Energy Integration and Utility-Scale BESS Mandate

Renewable energy integration and utility-scale Battery Energy Storage System (BESS) deployment continue to accelerate demand for Lithium Iron Phosphate (LFP) batteries, positioning LFP as the preferred chemistry for grid-scale energy storage due to its long cycle life and lower operating cost. In Q1 2026, LFP represented more than 97% of China’s energy storage battery shipments, reaching 209 GWh and recording 115% year-on-year growth. In the U.S., utility-scale battery storage capacity increased by 66% in 2024 with 10.4 GW added, while another 19.6 GW is planned for 2025. India further strengthened the sector through a ₹5,400 crore VGF scheme supporting 30 GWh of BESS capacity, driving rapid expansion of integrated energy storage solutions.

Drivers Impact Analysis

| Driver | (~) % CAGR Impact | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural EV Adoption & LFP Market Share Dominance | +4.5% | China core, EU, India, North America spill-over | Short term (≤ 2 years) |

| Renewable Energy Integration & Utility-Scale BESS Mandate | +3.8% | China, North America, EU, India, APAC | Short term (≤ 2 years) |

| Sustained LFP Cost Deflation to TCO Parity | +2.6% | Global — China production, all-geography deployment | Short–Medium term |

| Policy & Fiscal Incentive Architecture (IRA, EU Green Deal, India PLI) | +2.2% | North America, EU, India | Medium term (2–4 years) |

| Cell-to-Pack (CTP) & Next-Gen Manufacturing Technology Advancement | +1.8% | China, EU, North America | Medium term (2–4 years) |

| Commercial Fleet & Emerging Economy Light Mobility Expansion | +1.6% | India, Southeast Asia, Africa, Latin America | Long term (≥ 4 years) |

Restraint Analysis

Escalating U.S. and EU Tariff Regime on Chinese LFP Imports

Escalating U.S. and EU tariff measures on Chinese LFP imports have become a major restraint for global LFP battery expansion by increasing procurement costs and limiting access to low-cost supply. In the U.S., total effective tariffs on Chinese LFP battery imports reached 64.9% in 2025 and are projected to rise further in 2026, making direct imports commercially difficult for energy storage projects. The tariffs also extend to battery materials such as iron phosphate and graphite, increasing overall pack costs. As a result, ex-China LFP pricing has widened to nearly $95–165/kWh versus $50–84/kWh in China, reducing project viability and potentially lowering North American energy storage deployment pipelines by 20–30% through 2028.

Restraints Impact Analysis

| Restraint | (~) % CAGR Impact | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating U.S. & EU Tariff Regime on Chinese LFP Imports | -2.6% | North America core, EU secondary | Short term (≤ 2 years) |

| Chinese Manufacturing Overcapacity & Deflationary Price War | -1.8% | Global (ex-China manufacturers); APAC, EU | Short term (≤ 2 years) |

| Prohibitive Gigafactory CapEx Barrier (Ex-China) | -2.0% | North America, EU, India | Medium term (2–4 years) |

| China’s Export Controls on LFP Cathode Materials & Equipment | -1.5% | North America, EU, India, Southeast Asia | Medium term (2–4 years) |

| Absence of Commercial-Scale LFP Battery Recycling Infrastructure | -1.2% | EU (primary), North America, India | Medium term (2–4 years) |

| Upfront Cost Premium Over Incumbent Lead-Acid Technologies | -1.0% | India, Southeast Asia, MEA, rural APAC | Short term (≤ 2 years) |

Opportunity Analysis

Virtual Power Plant (VPP) / Grid-Services Aggregation

The World Economic Forum has explicitly identified grid-based “network-directed” battery storage as a “major untapped opportunity” capable of unlocking significant latent capacity in today’s energy infrastructure without requiring new capital investment in physical grid assets. BNEF projects annual global energy storage additions reaching 220 GW/972 GWh by 2035 at a 14.7% CAGR from 2025, and commercial battery deployments are projected to overtake residential by 2030—creating an enormous fleet of dispatchable LFP assets that will generate far greater value if operated as aggregated grid-services portfolios than as standalone backup systems.

Opportunities Impact Analysis

| Opportunity | (~) % CAGR Impact | Geographic Relevance | Execution Window |

|---|---|---|---|

| Residential VPP Aggregation Networks | +2.2% | North America (California, Texas, Northeast); EU (Germany, UK, Netherlands); Australia | Short to Medium term (1–3 years) |

| C&I Solar-Plus-Storage Leasing in Latin America | +1.9% | Brazil, Chile, Mexico, Colombia; Andean spill-over | Medium term (2–4 years) |

| Carbon-Certified LFP Supply Chain & Green Premium Monetization | +1.7% | EU primary; North America secondary; Japan and South Korea corporate procurement | Short to Medium term (≤ 3 years) |

| Lead-Acid Replacement Roll-Up in Telecom & UPS Verticals | +1.6% | South & Southeast Asia (India, Indonesia, Vietnam); Sub-Saharan Africa; Latin America | Short to Medium term (1–3 years) |

| LFP-Embedded EV Charging Infrastructure with Grid Arbitrage | +1.4% | North America primary; EU secondary; India emerging | Medium term (2–4 years) |

| China Battery Industry Consolidation M&A Play | +1.0% | China core; ASEAN re-export corridors; EU and North America OEM supply chain integration | Short term (≤ 2 years) |

Challenges Analysis

Escalating Regulatory Compliance Burden: EU Battery Regulation

The EU Battery Regulation (Regulation EU 2023/1542) entered its active enforcement phase in 2026, transforming what was previously a voluntary sustainability framework into a legally binding, market-access prerequisite that imposes significant operational and financial compliance infrastructure demands on all LFP battery producers and importers serving the European market.

As of February 18, 2026, all rechargeable industrial batteries with capacity exceeding 2 kWh require a verified carbon footprint declaration with site-specific primary data for every battery model and manufacturing plant — a requirement that forces even cost-optimized Chinese LFP producers to invest in scope 3 lifecycle assessment tooling, third-party verification audits, and real-time production monitoring infrastructure that collectively add an estimated $0.8–1.5/kWh to the compliance cost stack.

Challenges Impact Analysis

| Challenge | (~) % CAGR Impact | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| China Supply Chain Concentration & FEOC Geopolitical Exposure | -2.1% | North America, EU, India | Long term (≥ 4 years) |

| Structural Skilled Workforce Deficit | -1.6% | North America, EU, India | Long term (≥ 4 years) |

| LFP Energy Density Ceiling vs. NMC/LMFP Competition | -1.4% | Global (premium EV & aerospace segments) | Medium term (2–4 years) |

| Raw Material Price Volatility & Input Cost Regime Shift | -1.3% | Global (China-linked supply, APAC, EU) | Medium term (2–4 years) |

| Escalating Regulatory Compliance Burden (EU Battery Regulation) | -1.1% | EU core, North America secondary | Medium term (2–4 years) |

| Thermal Performance at Low Temperatures & Fast-Charge Limitations | -0.9% | Northern EU, North America, Northern China, India cold regions | Short term (≤ 2 years) |

Geopolitical Impact Analysis

Persistent geopolitical tensions and supply chain disruptions affecting the Lithium Iron Phosphate battery market.

Geopolitical conflicts, trade tensions, and disruption in supply chain logistics play a huge role in impacting the global market for lithium iron phosphate (LFP) batteries. Conflicts such as the Russia-Ukraine war, increased U.S.-China trade tension, and unstable mineral supply sources affect production strategies, material procurement, and global investment dynamics within the LFP battery industry.

Firstly, the Russia-Ukraine conflict has led to an increase in investment in the use of renewable energy and energy storage systems for energy generation, which is mainly seen across European countries. This move is having a positive impact on the demand for lithium iron phosphate batteries within this industry space.

Secondly, increased tensions between the U.S. and China have led to uncertainty along the supply chain since China dominates the process of lithium processing, LFP cathode manufacture, and lithium-ion batteries. Export restrictions and other related factors have led to an increased interest from both North America and Europe towards investing in their battery industry.

Regional Analysis

The Asia Pacific Region Dominated the Global Lithium Iron Phosphate Battery Market.

Asia Pacific is expected to be the dominant player in the global lithium iron phosphate (LFP) battery market by 2025 since it is estimated to account for about 76.0% of the entire global market share valued at approximately USD 36.3 billion because of its well-developed battery manufacturing industry, efficient electric vehicles manufacturing capability, and deployment of renewable energy storage systems.

North America is poised to become one of the key growth zones within the lithium iron phosphate battery industry, attributed mainly to growing investment in local battery manufacturing, as well as in electric vehicles and energy storage facilities. Various government policies, including the Inflation Reduction Act, are helping fast-track localization of battery supply chains by making huge investments in gigafactories, lithium mining and processing units, and electric vehicles factories.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Lithium Iron Phosphate (LFP) Batteries market shows a highly oligopolistic market structure, where a small group of large manufacturers controls a major share of global supply while several regional players compete in selected applications and geographies. The market is not monopolistic because no single company dominates completely, and it is not fully fragmented due to the strong scale advantages in battery chemistry, raw material sourcing, manufacturing capacity, and long-term OEM supply contracts.

Global competition is led by major Chinese battery companies, with CATL and BYD Company Ltd. holding the strongest positions. During 2025, CATL maintained around 39.2% share of the global EV battery market, while BYD accounted for nearly 17–18%, meaning the two companies together controlled more than half of global battery installations.

Top Key Players Outlook

- CATL

- BYD Company Limited

- LG Energy Solution Ltd.

- Samsung SDI Co., Ltd.

- Panasonic Corporation

- Gotion High-tech Co., Ltd

- CALB Co., Ltd.

- EVE Energy Co., Ltd.

- Lithium Werks B.V.

- A123 Systems LLC

- Saft Groupe S.A.

- Leclanché S.A.

- Clarios

- Exide Industries Limited

- Tesla Inc.

- Others

Recent Developments

In 2025, BYD reported about USD 116 billion in annual sales and sold 2.26 million EVs, up 28%, showing strong battery-backed vehicle demand. For new product development, BYD introduced its second-generation Blade Battery in 2026, supporting up to 777 km range and charging from 20% to 97% in under 12 minutes at -20°C. For investment and expansion, the company planned to build 20,000 Flash Charging stations by end-2026, including 2,000 highway stations. BYD also expanded battery production in Brazil through a wider USD 1.08 billion investment plan and considered up to USD 100 million in BESS-related investment.

In 2025, CATL sold 661 GWh of lithium batteries, up 39% YoY, and held 39.2% of the global power battery market, while its energy storage battery share reached 30.4%. For partnerships and agreements, CATL and Stellantis moved ahead with a €4.1 billion joint venture for a large-scale LFP battery plant in Spain, supporting local EV battery supply in Europe. For new product development, CATL launched Shenxing Pro LFP in 2025, offering 76% pack volume efficiency, 25% higher pack stiffness, and double durability.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 47.8 Bn |

| Forecast Revenue (2035) | USD 209.7 Bn |

| CAGR (2026-2035) | 16.0 % |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Prismatic Battery, Cylindrical Battery, Pouch Battery), By Voltage (Low Voltage, Medium Voltage, High Voltage), By End-User (Automotive, Energy and Utilities, Industrial, Consumer Electronics, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Contemporary Amperex Technology Co. Limited (CATL), BYD Company Limited, LG Energy Solution Ltd., Samsung SDI Co., Ltd., Panasonic Corporation, Gotion High-tech Co., Ltd, CALB Co., Ltd, EVE Energy Co., Ltd., Lithium Werks B.V., A123 Systems LLC, Saft Groupe S.A., Leclanché S.A., Clarios, Exide Industries Limited, Tesla Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |