Quick Navigation

Report Overview

The Global Wires and Cables Market size is expected to be worth around USD 356.1 Bn by 2033, from USD 214.5 Bn in 2023, growing at a CAGR of 5.2% during the forecast period from 2024 to 2033.

Wires and cables are essential components used for the transmission of electrical power and signals across various industries. Wires refer to single strands of conductive material, typically made from copper or aluminum, that carry electricity or data signals.

Cables, on the other hand, are made up of multiple wires, which are insulated and often bundled together for added protection and to enhance functionality. These products are widely used in electrical power distribution, telecommunications, electronics, and numerous other sectors.

Governments worldwide are supporting the growth of the wires and cables market through regulations and initiatives aimed at modernizing infrastructure and advancing clean energy. For example, in 2023, the European Union announced an investment of EUR 13 billion in the Green Deal to upgrade infrastructure and enhance power grids, directly benefiting the demand for high-quality cables.

Similarly, the U.S. government allocated over USD 7 billion in 2023 to modernize electrical grids, including funding for high-voltage transmission lines and smart cables. In the electric vehicle (EV) sector, the U.S. and China are two of the largest consumers of high-voltage cables used in EV charging infrastructure. The U.S. alone plans to invest USD 5 billion in EV charging networks over the next five years, leading to significant growth in cable requirements.

The wires and cables market is also shaped by import-export trends. China is the largest exporter of wires and cables, accounting for approximately 35% of global cable exports, valued at USD 50 billion in 2023. On the import side, the United States is a key importer, with USD 30 billion worth of wires and cables imported annually, primarily from China, Germany, and Japan.

Private investments are playing a major role in expanding the wires and cables market. Companies like Prysmian Group, Nexans, and Southwire are focusing on acquisitions, partnerships, and technological innovation to strengthen their positions.

For instance, in 2024, Prysmian Group acquired General Cable for USD 3 billion to expand its manufacturing capabilities in North America and Europe. Nexans has partnered with Schneider Electric to develop advanced smart cables integrated with sensors to monitor energy efficiency in real-time.

Key Takeaways

- Wires and Cables Market size is expected to be worth around USD 356.1 Bn by 2033, from USD 214.5 Bn in 2023, growing at a CAGR of 5.2%.

- Low Voltage (up to 1,000 volts) held a dominant market position, capturing more than a 54.2% share.

- Overhead cables held a dominant market position, capturing more than a 64.2% share.

- Polyvinyl Chloride (PVC) held a dominant market position, capturing more than a 38.3% share.

- Copper held a dominant market position, capturing more than a 66.8% share.

- Energy & Power held a dominant market position, capturing more than a 38.3% share.

- Asia Pacific (APAC) dominates the market, accounting for 43.3% of the total share, valued at USD 92.9 billion in 2023.

Strategic Business Review

The global wires and cables industry is integral to modern infrastructure, encompassing sectors such as telecommunications, energy transmission, and data communication. In 2022, the global fiber optic cable market was valued at approximately $15 billion, with the Asia-Pacific region accounting for $5.49 billion of this total.

In the United States, the communication and energy wire and cable manufacturing industry has shown consistent revenue figures. In 2017, the industry generated around $6.3 billion, with projections indicating a steady performance through 2024.

Technological advancements have significantly influenced the industry, particularly the shift from copper to fiber optic cables. Fiber optics offer higher bandwidth and faster data transmission, making them essential for high-speed internet and telecommunications. This transition is crucial for supporting the increasing demand for data and the expansion of services like 5G and IoT.

Environmental and health considerations are also shaping the industry. There is a growing emphasis on developing cables that minimize environmental impact and adhere to health and safety regulations. This trend is particularly prominent in regions like Europe, the U.S., and Japan, where stringent standards are in place.

By Voltage

In 2023, Low Voltage (up to 1,000 volts) held a dominant market position, capturing more than a 54.2% share. This segment’s growth is largely driven by its widespread use in residential, commercial, and industrial applications. Low voltage cables are essential for powering homes, offices, and small-scale machinery, making them a primary choice for everyday electrical systems.

Medium Voltage cables (1 kV to 36 kV) followed with a steady market share. These cables are primarily used in urban and industrial infrastructure, including power distribution networks and factories. The increasing demand for reliable energy in growing urban areas is pushing the adoption of medium voltage cables.

High Voltage cables (36 kV to 230 kV) are gaining traction due to their role in long-distance transmission lines and heavy industries. The global push for energy efficiency and the need to support large-scale power grids is driving demand in this segment. The market for high voltage cables is expected to grow at a faster pace as renewable energy projects expand.

Extra High Voltage cables (above 230 kV) represent the smallest segment but are crucial for long-distance power transmission, especially in large-scale projects like offshore wind farms and cross-border energy grids. With governments investing in high-capacity, high-efficiency transmission systems, this segment is witnessing gradual growth.

By Installation

In 2023, Overhead cables held a dominant market position, capturing more than a 64.2% share. Overhead installations are commonly used due to their cost-effectiveness and ease of maintenance. They are widely seen in power distribution networks, especially in rural and semi-urban areas. The relatively low installation costs and quicker setup times contribute to the continued popularity of overhead cables.

Underground cables, on the other hand, are growing steadily. Although they represent a smaller portion of the market, their demand is rising, particularly in urban areas and regions with extreme weather conditions. Underground cables offer better protection against environmental factors like storms, which is driving their adoption. As cities expand and the need for reliable power infrastructure increases, underground installations are expected to gain market share.

By Insulation Material

In 2023, Polyvinyl Chloride (PVC) held a dominant market position, capturing more than a 38.3% share. PVC is favored for its affordability, ease of use, and strong resistance to chemicals and moisture. It is commonly used in low to medium voltage cables for residential, commercial, and industrial applications. The widespread availability and cost-effectiveness of PVC make it the preferred choice in many markets.

Cross-linked Polyethylene (XLPE) followed as a key insulation material with significant demand, particularly in high voltage and medium voltage cables. XLPE is known for its excellent thermal resistance, electrical properties, and durability, making it ideal for more demanding applications. Its growth is driven by the increasing need for efficient, high-performance cables in power transmission and distribution systems.

Ethylene Propylene Rubber (EPR) holds a smaller but growing share of the market. Known for its flexibility, weather resistance, and high insulation properties, EPR is used in both low and high voltage cables, especially in harsh environments. The material’s resilience in extreme temperatures and its suitability for offshore and industrial applications are contributing to its increasing adoption.

Polyurethane (PUR) cables are becoming popular in specific industrial applications due to their flexibility, abrasion resistance, and ability to withstand harsh chemicals. PUR cables are mainly used in robotics, mining, and other heavy-duty sectors, where durability is critical.

Polyethylene (PE) is commonly used for both insulated and uninsulated cables. PE offers excellent electrical properties, especially for low voltage cables, and is gaining ground in the market due to its high strength and low cost. It’s primarily used in applications where high insulation performance and environmental protection are essential.

By Conductor Material

In 2023, Copper held a dominant market position, capturing more than a 66.8% share. Copper is widely used due to its excellent conductivity, durability, and long-term reliability. It remains the preferred choice for high-performance and high-quality cables, especially in power transmission and data cables. Its high cost is offset by its superior efficiency and lower energy loss, making it ideal for both residential and industrial applications.

Aluminum, while representing a smaller share than copper, continues to gain traction. Aluminum cables are lighter, cost-effective, and more suitable for long-distance power transmission. They are increasingly used in medium to high voltage transmission lines and offer a more affordable alternative to copper without compromising too much on performance. As infrastructure projects expand globally, aluminum’s role is expected to grow.

Steel, primarily used for armoring and strengthening cables, holds a niche but important market segment. Steel cables provide added durability, particularly in environments with high mechanical stress or external damage risks. These cables are commonly used in applications such as power transmission lines and subsea cables where protection from physical damage is critical.

Optical Fiber, although representing a smaller share in the overall market, is experiencing growth due to the increasing demand for high-speed internet and data transmission. Optical fibers offer high bandwidth, low signal loss, and are essential for telecommunications, internet services, and data centers. The ongoing digitalization and global demand for better connectivity are driving the adoption of optical fiber cables.

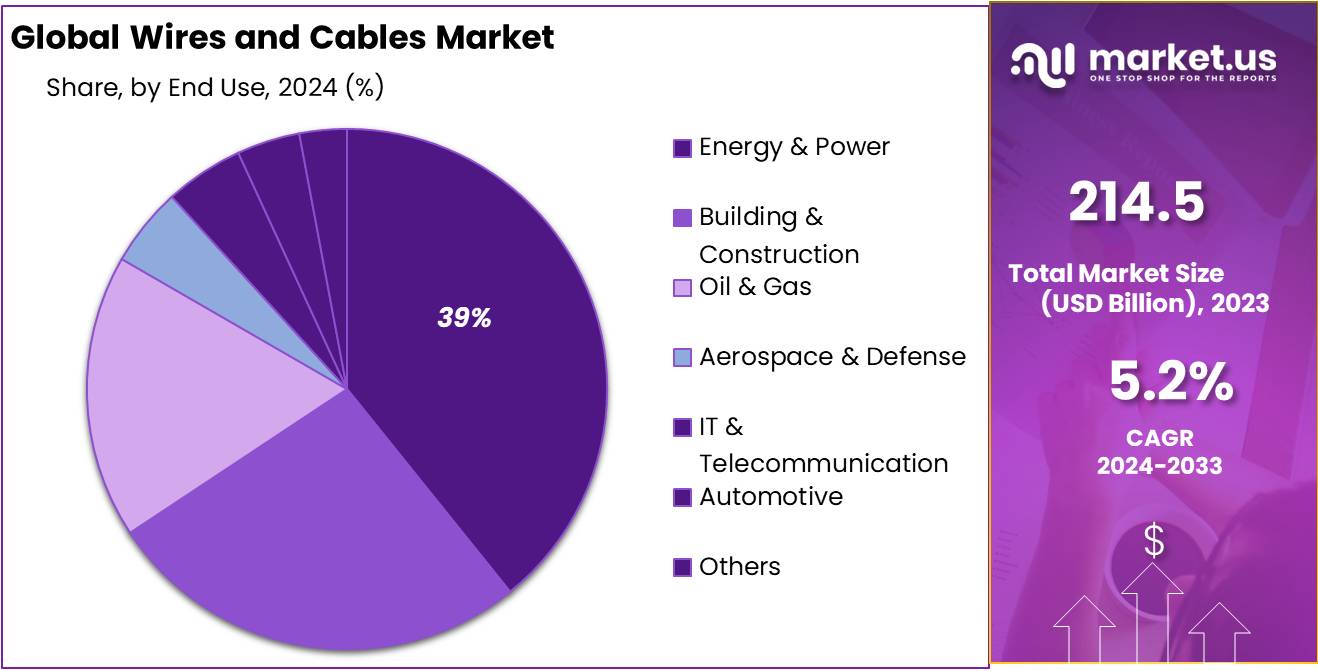

By End-use

In 2023, Energy & Power held a dominant market position, capturing more than a 38.3% share. This segment is driven by the increasing demand for electricity and the need for robust power generation, transmission, and distribution infrastructure. Wires and cables are essential for connecting power plants, substations, and consumers, supporting the growth of renewable energy and smart grids. As global energy consumption rises, the Energy & Power sector is expected to continue its dominant role in the market.

The Building & Construction sector follows closely, with a significant share of the market. The growing demand for residential, commercial, and industrial construction projects has fueled the need for reliable wiring solutions. Wires and cables are integral to electrical installations, lighting systems, and other essential infrastructure in new buildings. This sector benefits from ongoing urbanization and infrastructure development worldwide.

The Automotive industry is another key contributor to the wires and cables market. As electric vehicles (EVs) gain popularity, the demand for specialized wiring solutions is growing. Wires and cables are crucial for vehicle power systems, infotainment, and safety features. The transition to electric vehicles and the rise of autonomous vehicles are expected to further boost the market for automotive wiring solutions.

The Oil & Gas sector also plays a vital role, though it represents a smaller portion of the market. Cables used in this industry must withstand extreme conditions, including high temperatures, pressure, and exposure to chemicals. Wires and cables are used in offshore platforms, refineries, and pipelines, making them crucial for maintaining operations and ensuring safety.

IT & Telecommunication is a rapidly growing segment, driven by the demand for high-speed data transmission and networking. The expansion of 5G networks, data centers, and the overall digital transformation is increasing the need for specialized wires and cables that can handle high bandwidth and connectivity.

Key Market Segments

By Voltage

- Low Voltage

- Medium Voltage

- High Voltage

- Extra High Voltage

By Installation

- Overhead

- Underground

By Insulation Material

- Polyvinyl Chloride (PVC)

- Cross-linked Polyethylene (XLPE)

- Ethylene Propylene Rubber (EPR)

- Polyurethane (PUR)

- Polyethylene (PE)

By Conductor Material

- Copper

- Aluminum

- Steel

- Optical Fiber

By End-use

- Aerospace & Defense

- Building & Construction

- Oil & Gas

- Energy & Power

- IT & Telecommunication

- Automotive

- Others

Drivers

Expansion of Renewable Energy Infrastructure

According to the International Energy Agency (IEA), renewable energy sources accounted for almost 90% of new power capacity globally in 2020. This surge in renewable energy production means that more power needs to be transmitted over long distances, driving the demand for high-quality wires and cables. For example, the IEA reports that the share of renewable electricity generation is expected to grow from 29% in 2020 to 40% by 2040.

To meet this growing demand, countries are investing heavily in new power grids and upgrading existing ones to accommodate renewable energy sources. In the United States, for instance, the Department of Energy (DOE) has committed to investing billions into modernizing the national grid.

The DOE’s Grid Modernization Initiative focuses on improving the resilience and efficiency of the power grid to handle the increasing share of renewable energy. This modernization involves the widespread use of cables and wires that can transmit electricity with minimal loss, making it a key area of growth for the market.

Government Policies and Initiatives

Governments worldwide are playing a pivotal role in driving the growth of the renewable energy sector. These efforts include subsidies, tax incentives, and funding for renewable energy projects, all of which contribute to the increased demand for wires and cables.

The European Union’s Green Deal, for instance, sets ambitious goals for reducing carbon emissions and increasing renewable energy generation. Under this agreement, the EU aims to achieve carbon neutrality by 2050, which will require significant investments in clean energy infrastructure, including power grids and cables.

Similarly, in India, the government has set an ambitious target of achieving 500 GW of non-fossil fuel energy capacity by 2030. The country has already invested heavily in solar and wind energy projects, leading to a rapid increase in the demand for cables that can transport the energy generated.

The Indian government’s policies, including the National Smart Grid Mission, aim to create a more reliable and efficient power grid to support the integration of renewable energy sources. These initiatives are expected to continue driving the demand for wires and cables in the coming years.

Technological Advancements in Cable Manufacturing

Technological advancements in the materials and design of wires and cables are helping to meet the growing demand for renewable energy infrastructure. In particular, innovations in high-voltage direct current (HVDC) transmission and smart cables have improved the efficiency of power transmission.

According to the World Bank, HVDC lines can transmit electricity over much longer distances compared to traditional alternating current (AC) lines, making them ideal for transporting power generated from remote renewable sources like wind farms and solar plants. This shift in technology is expected to increase the use of specialized wires and cables designed for long-distance, high-efficiency power transmission.

For instance, manufacturers are increasingly using cross-linked polyethylene (XLPE) insulation for cables, which offers superior heat resistance and higher voltage capacity compared to traditional materials like PVC.

XLPE cables are particularly important for renewable energy applications because they can withstand the high temperatures and electrical loads generated by large-scale solar and wind energy farms. These advancements in cable technology are helping to reduce energy loss during transmission, improving overall efficiency, and making it easier to integrate renewable energy into existing grids.

Growing Electrification of Transportation and Industry

The electrification of various sectors, particularly transportation and industry, is another major factor driving the demand for wires and cables. The global shift toward electric vehicles (EVs) has led to a surge in demand for high-performance wiring for battery systems, charging stations, and electrical infrastructure.

According to the International Energy Agency (IEA), the number of electric cars on the road is expected to reach 145 million by 2030, up from 10 million in 2020. This electrification trend is also seen in the transportation of goods, with electric buses, trucks, and rail systems requiring advanced wiring solutions.

Restraints

Increasing Copper Prices and Its Impact on Cable Manufacturing

According to data from the World Bank, the price of copper surged by more than 80% from 2020 to 2021, reaching highs of over $10,000 per ton. In 2023, the average price of copper was approximately $8,500 per ton. This sharp increase in copper prices is primarily driven by supply chain disruptions, rising demand from emerging economies, and challenges in mining and production.

As copper is the primary raw material in the wires and cables market, these price hikes directly impact manufacturers’ production costs. Higher raw material costs result in increased pricing for finished cables, which can deter investments, particularly in price-sensitive sectors. Additionally, the increased cost burden can reduce profit margins for companies, which may also impact the affordability of cables for consumers.

Supply Chain Disruptions and Their Effect on Material Availability

In addition to rising raw material costs, supply chain disruptions have further exacerbated the issue. The COVID-19 pandemic and geopolitical tensions have led to delays and interruptions in the supply of essential materials. For example, in 2022, supply chain disruptions in major copper-producing countries like Chile and Peru led to a decrease in copper output, further driving up prices.

According to the International Copper Study Group (ICSG), global copper production decreased by 2.5% in 2022, adding pressure to the already strained supply chain. These disruptions have made it harder for manufacturers to secure a steady supply of copper, increasing lead times and prices for wires and cables.

This volatility in supply and prices forces companies to either absorb the higher costs, reduce production, or pass on the price increases to customers, potentially leading to a reduction in demand for cables in certain markets.

Impact of Rising Costs on End-Use Industries

The rising cost of wires and cables due to higher raw material prices has a direct impact on industries that rely on these products for infrastructure and manufacturing. In sectors such as construction, automotive, and renewable energy, the increased costs of cables can lead to higher project costs, which in turn can delay or reduce the scale of investments.

According to the U.S. Energy Information Administration (EIA), the cost of building utility-scale solar power plants increased by 15-20% in 2022, partially due to the rising costs of copper and other raw materials. Similarly, in the automotive industry, which is increasingly adopting electric vehicles (EVs), the cost of wiring and cables has become a crucial factor in determining overall vehicle costs.

Opportunity

Growing Electric Vehicle Sales and Charging Infrastructure Demand

According to the International Energy Agency (IEA), global electric car sales reached 10 million units in 2022, a 55% increase compared to the previous year. The IEA projects that by 2030, there will be 145 million electric cars on the road, representing about 30% of global car sales. As a result, the need for high-quality electrical wiring and robust charging infrastructure is expanding, driving demand for specialized wires and cables in the automotive sector.

This growth is further fueled by government policies and initiatives aimed at reducing emissions. For instance, the European Union has set ambitious targets for EV adoption, aiming for 30 million electric cars on the road by 2030, with a goal to achieve net-zero emissions by 2050.

In the United States, the Biden administration’s $7.5 billion initiative to build a national network of EV chargers will also significantly boost demand for cables that can support high-voltage, fast-charging systems.

High-Performance Cables for EV Batteries and Charging Stations

As electric vehicles rely on advanced battery systems, manufacturers need to develop specialized cables that can efficiently manage high current loads, ensuring fast charging times and the safety of electrical systems.

The wiring for EVs is also required to be lighter and more flexible, offering manufacturers new opportunities to innovate in material and cable design. The rising demand for high-performance cables for EV batteries, motors, and charging stations is expected to continue over the coming years.

A report by the U.S. Department of Energy’s Vehicle Technologies Office indicated that the average number of charging stations in the U.S. grew by more than 30% from 2020 to 2021.

In addition, the office projected that the market for EV charging equipment would exceed $25 billion by 2025, further driving demand for wires and cables. In particular, cables capable of handling high-voltage charging (e.g., 350 kW and beyond) are expected to see strong growth as part of the global push toward faster charging infrastructure.

The Role of Government Initiatives and Regulations

Governments worldwide are playing a pivotal role in boosting the EV market and, consequently, the demand for wires and cables. Incentives, tax rebates, and regulatory measures such as stricter emissions standards are driving the adoption of electric vehicles.

For example, the European Union has committed to reducing CO2 emissions from cars and vans by 55% by 2030, with plans to phase out sales of new petrol and diesel vehicles by 2035. These regulatory frameworks are creating a favorable environment for the EV industry, leading to increased demand for the wiring solutions that support both the vehicles and their charging infrastructure.

Trends

Use of Eco-friendly and Recyclable Materials

XLPE is more durable, resistant to heat, and can be recycled more efficiently. According to a report by the European Union’s REACH initiative, the demand for low-carbon and recyclable cable materials is increasing across Europe, driven by tighter environmental regulations. In fact, the EU’s Circular Economy Action Plan aims to boost the recycling rate of materials in products like cables, with the goal of making all plastic packaging recyclable by 2030.

According to the International Telecommunication Union (ITU), about 40% of electrical and electronic waste (e-waste) globally comes from cables, which has sparked a push for recyclable and less harmful materials. As the global push for sustainability intensifies, cables with reduced environmental footprints are expected to become the new standard.

Government Regulations Supporting Sustainable Practices

Governments worldwide are tightening regulations around environmental sustainability, which is further accelerating the shift toward eco-friendly cables. For instance, in the European Union, the Waste Electrical and Electronic Equipment (WEEE) Directive mandates that electronic waste, including cables, be recycled, and restricts the use of harmful materials like lead and mercury.

The EU has also set ambitious targets for reducing carbon emissions, with a goal to cut greenhouse gas emissions by 55% by 2030 compared to 1990 levels. Such regulations are influencing manufacturers to adopt greener production methods and materials.

In the United States, the Environmental Protection Agency (EPA) has been pushing for the reduction of hazardous substances in cables and wires. This includes promoting alternatives to PVC insulation, which is considered harmful to the environment.

As governments implement stricter regulations, the demand for wires and cables made from recyclable and non-toxic materials continues to grow, providing a significant opportunity for manufacturers to innovate and stay ahead of regulatory requirements.

Growth of the Renewable Energy Sector Driving Demand for Green Cables

The expansion of renewable energy sources like wind, solar, and hydroelectric power is another key driver of the trend towards sustainable cables. Renewable energy installations require a robust network of wires and cables that can withstand harsh environments and high energy loads. At the same time, the cables used in renewable energy projects must meet high sustainability standards.

For instance, the International Renewable Energy Agency (IRENA) projects that global renewable energy capacity will grow by 60% from 2020 to 2030. This surge in renewable energy capacity translates to an increased need for eco-friendly cables that support energy-efficient systems.

According to the World Bank, the global solar power market alone is expected to expand by 20% annually, requiring extensive new installations of cables made from sustainable materials. Similarly, as offshore wind energy projects expand, there is a growing demand for cables that can withstand extreme environmental conditions while being environmentally responsible.

The need for green cables in renewable energy projects is creating a lucrative growth opportunity in the market, especially for manufacturers who can meet the high environmental standards required by these sectors.

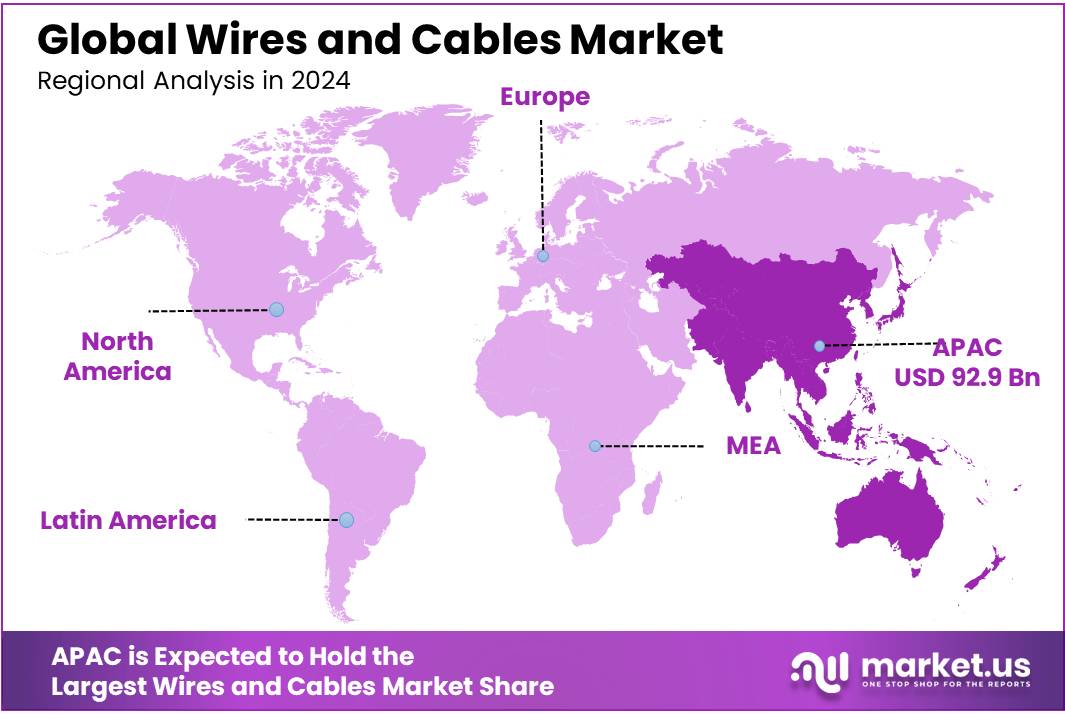

Regional Analysis

The global wires and cables market is seeing substantial regional growth, driven by diverse industrial demands and infrastructure development. Asia Pacific (APAC) dominates the market, accounting for 43.3% of the total share, valued at USD 92.9 billion in 2023.

This dominance is primarily due to the rapid industrialization, urbanization, and increasing investments in renewable energy across key economies such as China and India. APAC’s demand is further supported by the growing automotive and consumer electronics sectors, which require advanced wiring solutions. China’s ambitious plans to expand its energy grid and India’s push for electric vehicle (EV) infrastructure are key growth drivers in this region.

In North America, the market is also seeing steady growth, with the region holding a significant share due to extensive investments in energy infrastructure and a shift towards electric vehicles. The United States, in particular, is a major player in the wires and cables market, contributing heavily to the demand for high-quality cables in the energy and IT sectors. The market size in North America is projected to continue growing due to government initiatives aimed at modernizing the grid and supporting green energy.

Europe is another key market, supported by strong industrial sectors and government-driven initiatives to improve energy efficiency. The European Union’s Green Deal and focus on sustainability are driving demand for more energy-efficient cables, particularly in the renewable energy and electric vehicle charging infrastructure sectors.

Latin America and Middle East & Africa are smaller markets, but they are experiencing growth due to infrastructure development and increasing demand for energy-efficient systems, with investments being made in the power, automotive, and telecommunications sectors.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The wires and cables market is highly competitive, with numerous established players driving innovation and market growth. Prysmian S.p.A, a global leader in the cables industry, is one of the key players, renowned for its advanced solutions in energy and telecommunications.

Similarly, Nexans and Southwire Company LLC are major players offering a wide range of high-performance cables across various sectors, including energy, construction, and industrial applications. LS Cable & System Ltd., Sumitomo Corporation, and Fujikura Limited also hold prominent positions in the market, with a strong presence in the power transmission and automotive segments. These companies are actively involved in expanding their product portfolios to cater to growing industries like renewable energy, electric vehicles, and infrastructure development.

Other notable players include Amphenol Corporation, Belden Inc., and Corning Incorporated, which focus heavily on high-quality, specialized cables for communications, industrial, and IT sectors. Companies such as Finolex Cables, KEI Industries Limited, and TE Connectivity offer a diverse range of products, including both power and data cables, which are increasingly in demand due to the ongoing digitization of industries.

Regional players like British Cables Company (Wilms Group) and Waskonig & Walter also play important roles in their respective markets, meeting specific local requirements and contributing to the market’s fragmented landscape.

Top Key Players in the Market

- American Wire Group

- Amphenol Corporation

- Belden Inc.

- British Cables Company (Wilms Group)

- Cable & System Limited

- CommScope Holding Company, Inc.

- Corning Incorporated

- Encore Wire Corporation

- Finolex Cables.

- Fujikura Limited

- Furukawa Electric Co., Ltd.

- Hengton Optic-Electric

- KEI Industries Limited.

- Leoni AG

- LS Cable & System Ltd.

- Nexans

- NKT A/S

- Prysmian S.p.A

- Shanghai Shenghua Group

- Southwire Company LLC

- Sumitomo Corporation

- TE Connectivity

- TELE-FONIKA Kable S.A.

- Waskonig & Walter

Recent Developments

American Wire Group expects further growth, with projected revenues for 2024 reaching USD 270 million, marking a 8% year-on-year growth.

Amphenol is expected to continue its growth, with a projected revenue of USD 14.6 billion in 2024, marking a 9% year-on-year increase, driven by strong demand for high-speed data transmission cables and electric vehicle wiring systems.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 214.5 Bn |

| Forecast Revenue (2033) | USD 356.1 Bn |

| CAGR (2024-2033) | 5.2% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Voltage (Low Voltage, Medium Voltage, High Voltage, Extra High Voltage), By Installation (Overhead, Underground), By Insulation Material (Polyvinyl Chloride (PVC), Cross-linked Polyethylene (XLPE), Ethylene Propylene Rubber (EPR), Polyurethane (PUR), Polyethylene (PE)), By Conductor Material (Copper, Aluminum, Steel, Optical Fiber), By End-use (Aerospace and Defense, Building and Construction, Oil and Gas, Energy and Power, IT and Telecommunication, Automotive, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | American Wire Group, Amphenol Corporation, Belden Inc., British Cables Company (Wilms Group), Cable & System Limited, CommScope Holding Company, Inc., Corning Incorporated, Encore Wire Corporation, Finolex Cables., Fujikura Limited, Furukawa Electric Co., Ltd., Hengton Optic-Electric, KEI Industries Limited., Leoni AG, LS Cable & System Ltd., Nexans, NKT A/S, Prysmian S.p.A, Shanghai Shenghua Group, Southwire Company LLC, Sumitomo Corporation, TE Connectivity, TELE-FONIKA Kable S.A., Waskonig & Walter |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |