Quick Navigation

Report Overview

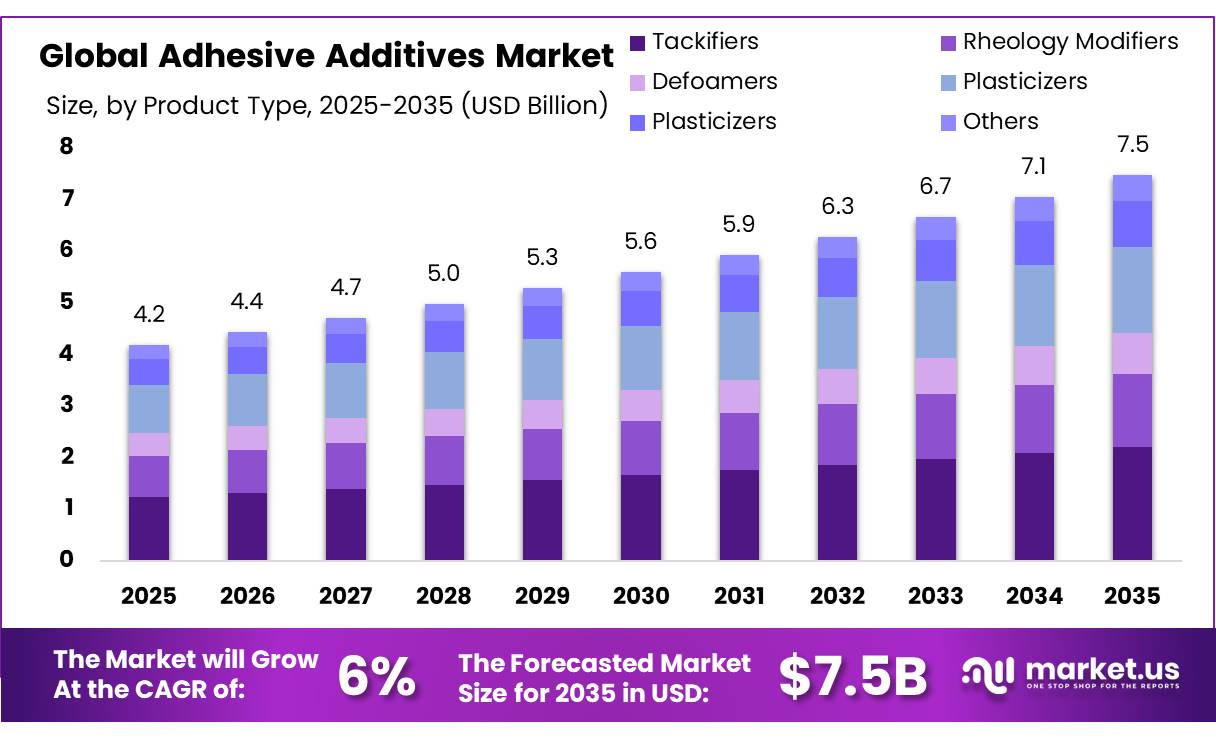

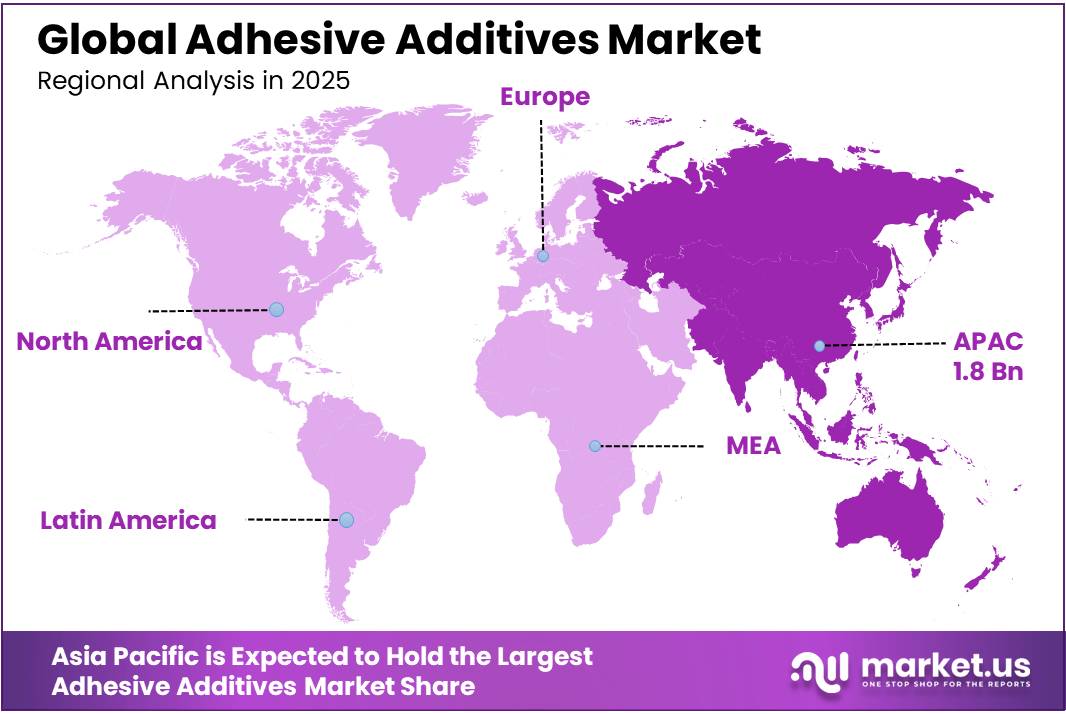

The Global Adhesive Additives Market size is expected to be worth around USD 7.5 Billion by 2035, from USD 4.2 Billion in 2025, growing at a CAGR of 6.0% during the forecast period from 2026 to 2035. In 2025, Asia-Pacific held a dominant market position, capturing more than a 43.4% share, holding USD 1.8 Billion revenue.

Key Takeaways

- The global adhesive additives market was valued at USD 4.2 billion in 2025, reflecting steady demand across packaging, construction, automotive, and industrial applications.

- The market is projected to expand at a CAGR of 6.0% during the forecast period and is expected to reach approximately USD 7.5 billion by 2035.

- By product type, tackifiers emerged as the leading segment, accounting for 29.4% of the global market share in 2025, supported by their ability to improve adhesive bonding performance and durability.

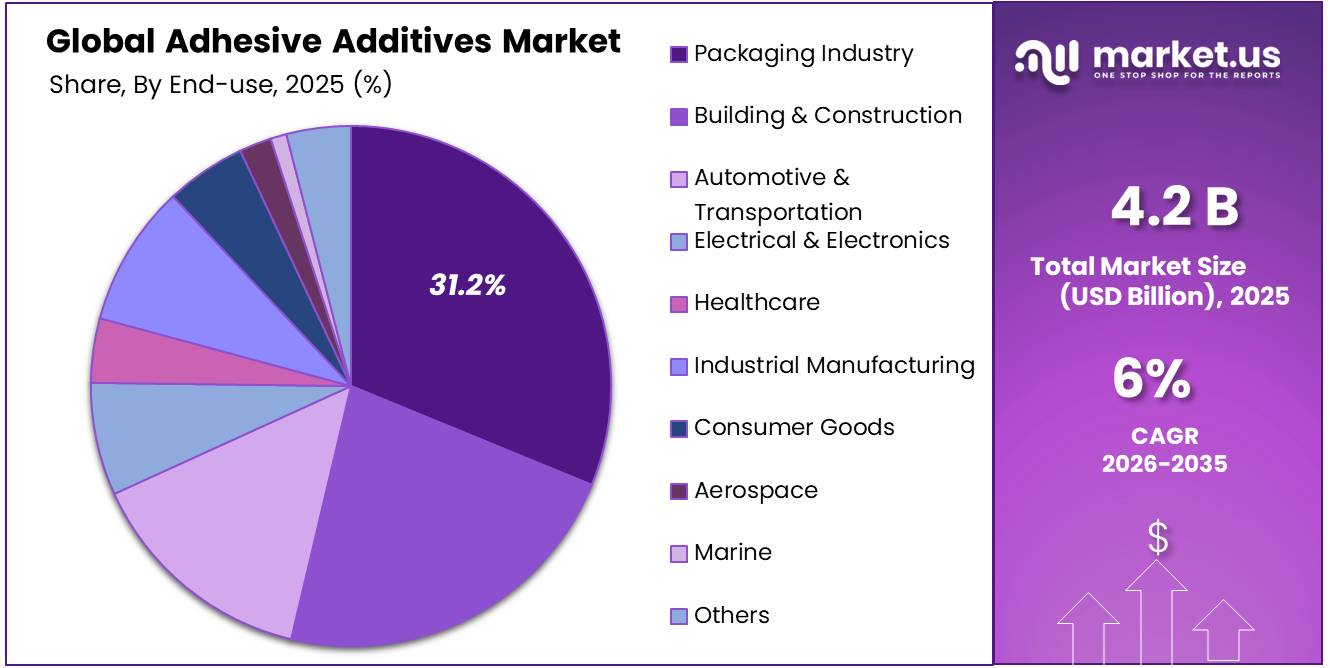

- Based on end-use industry, the packaging sector held the dominant position with a 31.2% market share, driven by increasing demand for flexible packaging, labeling, and e-commerce packaging solutions.

- Asia Pacific remained the largest regional market in 2025, representing 43.4% of global adhesive additives consumption, supported by strong manufacturing activity, rapid urbanization, and growing automotive production across major economies such as China and India.

The adhesive additives market continues to expand, supported by strong demand from the automotive, construction, and packaging industries. In 2025, global motor vehicle production reached 96.4 million units, rising 3.9% from 92.7 million units in 2024. Asia Pacific remained the largest manufacturing hub, producing approximately 59.2 million vehicles, representing more than 61% of global output. China led the region with 34.53 million units, while India achieved a record 6.49 million units. The growth in vehicle production is increasing the use of advanced adhesives for body assembly, interior components, noise reduction, and electric vehicle battery systems. These applications rely on adhesive additives such as rheology modifiers, defoamers, dispersants, and stabilizers to improve bonding strength, viscosity control, and long-term durability.

The construction sector is also creating significant demand for adhesive additives. Asia Pacific became a majority-urban region in 2019, with more than 2.3 billion people living in cities, and the urban population is projected to increase by another 1.2 billion by 2050. Rapid urbanization is driving investments in residential buildings, commercial facilities, and infrastructure projects, all of which require adhesive-based materials for flooring, insulation, wall panels, and façade systems.

In addition, China’s manufacturing industry generated US$4.66 trillion in value added in 2023, highlighting the region’s large industrial base. Supported by expanding vehicle production, urban development, and industrial growth, Asia Pacific currently accounts for 43.4% of the global adhesive additives market, which is projected to grow from US$4.2 billion in 2025 to US$7.5 billion by 2035.

Adhesive Additives Market Segmentation

Product Analysis

The product type segment was led by Tackifiers, accounting for 29.6% of the market share. Tackifiers maintained their leading position due to their essential role in pressure-sensitive adhesives (PSAs), which are extensively used in packaging, labeling, and construction applications. Their ability to improve adhesion, tack, and bonding performance makes them a key ingredient in a wide range of adhesive formulations.

Demand for tackifiers continues to be supported by the strong growth of the labeling and packaging industries. According to FINAT, the global label industry consumes approximately 74 billion square metres of labelstock annually, with the majority relying on tackifier-based PSAs. In addition, UNCTAD reported global e-commerce sales of around USD 27 trillion in 2022, while the IPC recorded a 4.4% increase in global parcel volumes in 2024. This growth has significantly increased the use of packaging tapes, labels, and other adhesive products, reinforcing the dominant position of tackifiers in the adhesive additives market.

End-Use Industry Analysis

Packaging Industry Emerged as the Dominant End-use Segment in the Adhesive Additives Market

The Packaging Industry was the leading end-use segment in the Global Adhesive Additives Market, accounting for 31.2% of the total market share. This leadership is supported by strong demand from the food packaging, consumer goods, and e-commerce sectors. According to the Food and Agriculture Organization (FAO), global primary agricultural crop production reached 9.9 billion tonnes in 2023, representing an increase of 28% compared to 2010. This growth has significantly increased the need for food packaging materials across storage, transportation, and retail supply chains.

The Flexible Packaging Association (FPA) reports that food products account for nearly 50% of all flexible packaging shipments. In addition, the U.S. flexible packaging sector represents approximately 21% of the country’s US$180.3 billion packaging industry. The rapid expansion of online retail has further strengthened packaging demand. According to UNCTAD, global business-to-business and consumer e-commerce sales reached approximately US$27 trillion in 2022, creating substantial demand for corrugated boxes, flexible laminates, and pressure-sensitive labels. The International Post Corporation (IPC) also reported that global postal parcel volumes increased by 4.4% in 2024, mainly driven by e-commerce activities.

Key Market Segments

By Product Type

- Tackifiers

- Rheology Modifiers

- Defoamers

- Plasticizers

- Wetting & Dispersing Agents

- Others

By End-use Industry

- Building & Construction

- Packaging Industry

- Automotive & Transportation

- Electrical & Electronics

- Healthcare

- Industrial Manufacturing

- Consumer Goods

- Aerospace

- Marine

- Others

Driver Analysis

Global Construction Upcycle — Rheology Modifiers & Structural Additive Demand

The ongoing global construction expansion is a major growth driver for adhesive additives in 2026, increasing demand for rheology modifiers, wetting agents, and dispersing additives used in tile adhesives, flooring, waterproofing, and structural bonding applications. The global construction adhesives market reached USD 11.3 billion in 2026 and is projected to grow to USD 16.6 billion by 2033 at a 4.3% CAGR, while the broader construction additives market is expected to reach USD 114.6 billion by 2030 at a 5.8% CAGR. Asia-Pacific accounts for nearly 40% of global construction adhesive revenue, supported by infrastructure growth.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global construction upcycle driving rheology modifier & structural adhesive additive demand | 1.80% | APAC core (China, India, SE Asia); MEA spill-over; North America secondary | Long term (≥ 4 years) |

| EV lightweighting & battery assembly accelerating silane, crosslinker, and thermal additive adoption | 1.50% | North America, EU, China EV manufacturing corridors | Medium term (2–4 years) |

| E-commerce packaging surge lifting hot-melt tackifier and dispersing agent volumes | 1.20% | APAC dominant; North America & EU secondary | Short term (≤ 2 years) |

| PFAS/VOC/REACH regulatory mandates forcing high-performance, low-emission additive reformulation | 1.00% | EU primary (Regulation 2025/40 effective Aug 2026); North America; APAC emerging | Short to Medium term (1–3 years) |

| Silane coupling agent penetration in composites, electronics, and infrastructure bonding | 0.90% | North America largest; APAC fastest growth; EU industrial corridors | Medium term (2–4 years) |

| Bio-based & sustainable additive commercialization under bioeconomy policy incentives | 0.70% | EU & North America primary; APAC expanding at 4.8%+ p.a. | Long term (≥ 4 years) |

Restraint Analysis

Petrochemical Feedstock Price Volatility

Raw material cost volatility remains a major restraint for the adhesive additives industry because feedstocks account for nearly 50% of total revenue for adhesive and sealant formulators, higher than the 35–40% typically seen in coatings. Key inputs such as butyl acrylate and 2-ethylhexyl acrylate (2-EHA) experienced price increases of up to USD 100 per metric ton across Asia-Pacific in early 2026. The global acrylate monomer market, valued at USD 4.66 billion in 2024, has historically shown 25–40% price fluctuations during feedstock disruptions. As of 2025, industry cost bases remained 15–20% above pre-pandemic levels, reducing profitability and delaying margin recovery across the value chain.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petrochemical feedstock price volatility inflating formulation input costs | -1.50% | Global; acute in EU & APAC coastal clusters (Zhanjiang, Ningbo, Rotterdam) | Short term (≤ 2 years) |

| US–China tariff escalation disrupting specialty chemical intermediate supply chains | -1.20% | North America primary; EU secondary; APAC spill-over | Short to Medium term (1–3 years) |

| REACH/PFAS/SVHC compliance costs forcing portfolio re-registration and reformulation | -1.00% | EU core; North America; APAC (China GB standards) | Medium term (2–4 years) |

| Chinese chemical overcapacity driving price deflation & margin erosion | -0.90% | Global pricing corridor; most acute in APAC & export-exposed EU | Medium term (2–4 years) |

| High production cost & feedstock scarcity constraining bio-based additive commercialization | -0.70% | EU & North America primary; APAC emerging | Long term (≥ 4 years) |

| Lengthy OEM qualification cycles delaying adoption of next-generation additive systems | -0.60% | North America, EU, APAC automotive/electronics manufacturing corridors | Medium to Long term (3–5 years) |

Opportunity Analysis

Debonding-on-Demand Additive Systems for Circular Economy Compliance

Debonding-on-demand (DoD) functional additives represent an emerging white-space opportunity in the adhesive additives industry, as commercial revenues are not yet meaningfully captured by major suppliers. The de-bondable adhesives market, valued at approximately USD 262.8 million in 2025 and projected to reach USD 512.5 million by 2033 at an 8.8% CAGR, serves as an early indicator of demand; however, the additive opportunity is expected to be larger because DoD functionality is introduced through specialized additive systems rather than complete adhesive replacement.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| AI-driven formulation intelligence platforms monetizing additive R&D as a digital service | 1.50% | Global; North America & EU early adopters; APAC fast follower | Short term (≤ 2 years) |

| Debonding-on-demand additive systems unlocking circular economy compliance TAM | 1.20% | EU primary (ESPR 2025 mandate); North America; APAC automotive corridors | Medium term (2–4 years) |

| Penetration into wearable medical device adhesive additive vertical | 0.90% | North America & EU core; APAC fastest CAGR corridor | Medium term (2–4 years) |

| India & SE Asia local manufacturing buildout to capture underpenetrated specialty additive demand | 0.80% | India, Vietnam, Indonesia, Thailand, Bangladesh | Short to Medium term (1–3 years) |

| M&A-led consolidation of fragmented CASE specialty additive suppliers | 0.70% | North America, EU; PE-driven carve-outs in APAC | Medium term (2–4 years) |

| Recyclate-compatible additive systems targeting chemical recycling value chain entry | 0.50% | EU primary; North America secondary; China emerging | Long term (≥ 4 years) |

Challenges Analysis

Specialty Workforce & Formulation Talent Deficit

Workforce shortages are becoming a growing challenge for the adhesive additives industry as experienced formulation chemists, process engineers, and regulatory specialists retire faster than new talent enters the sector. By 2026, 75% of chemical industry executives reported high concern about labor availability, especially for technical manufacturing and supply chain roles. Competition from biotechnology, pharmaceutical, and semiconductor industries, which offer 15–25% higher compensation, is increasing hiring pressure. The loss of senior formulation experts with 15–25 years of specialized knowledge can create replacement costs of USD 300,000–600,000 and extend new product development timelines by 4–8 months, reducing productivity and slowing innovation across the industry.

Challenges Impact Analysis

| Challenge | (~) % Potential CAGR | Geographic Relevance | Mitigation Horizon | |

|---|---|---|---|---|

| Petrochemical Feedstock Price Volatility | -1.40% | Global; highest in EU, APAC import corridors | Medium term (2–4 years) | |

| Escalating Regulatory Compliance Burden (VOC / PFAS / REACH) | -1.10% | EU regulatory hubs; North America (CARB, EPA); expanding APAC | Long term (≥ 4 years) | |

| Bio-Based Transition Performance Gap | -0.90% | EU sustainability corridors; North America green-build zones; nascent APAC | Long term (≥ 4 years) | |

| Specialty Workforce & Formulation Talent Deficit | -0.80% | North America manufacturing belt; EU chemical clusters; South & East APAC R&D hubs | Long term (≥ 4 years) | |

| Multi-Tier Supply Chain Disruption & Logistics Friction | -1.20% | APAC logistics corridors; Trans-Pacific routes; EU-import dependent markets | Medium term (2–4 years) | |

| Application Complexity & End-Use Diversification Pressure | -0.70% | Global; intensified in high-spec segments — EV, aerospace, medical, advanced electronics | Medium term (2–4 years) |

Geopolitical Impact Analysis

The restructured US-China trade framework has become a major cost restraint for adhesive additive manufacturers. In 2026, the effective US tariff on Chinese imports stands at nearly 33%, including MFN duties of about 3.4%, Section 301 tariffs of 7.5% to 25%, a 20% IEEPA fentanyl surcharge, and a 10% reciprocal rate under the 90-day truce extension running through August 2026. This tariff structure is increasing the landed cost of key Chinese raw materials such as TDI, acrylic monomers, and epoxy resins, which are essential for polyurethane crosslinkers, acrylic PSA systems, and reactive additive formulations.

Input cost volatility remains high. Asian toluene FOB Korea prices reached nearly USD 651/MT in early October 2025, while the US tariff spike to 145% during April-May 2025 showed the price risk linked to China-dependent sourcing. China’s rare earth export controls in April and October 2025 further added uncertainty, especially for lanthanide-catalyzed curing systems used in EV battery adhesives. Although MOFCOM Announcement No. 70 suspended some controls until November 10, 2026, reinstatement risk remains commercially important.

Logistics pressure is also affecting margins. Due to Red Sea disruption, Asia-Europe container routes have shifted around the Cape of Good Hope, adding 10-15 days per voyage since 2024. Asia-North Europe spot rates reached nearly USD 4,876/FEU at crisis levels. These delays increase working capital needs, inventory holding, and MOQ renegotiations, particularly for SMEs operating on 30-45 day stock cycles. As a result, producers with nearshore supply access in India, Southeast Asia, and the EU are gaining a stronger cost position.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Adhesive Additives Market.

In 2025, The Asia Pacific region had the largest share of the global adhesive additives market, accounting for 43.4%. This is due to increased industrialization, expansion of the packaging industry, robust manufacturing operations, and infrastructural development in nations such as China, India, Japan, and South Korea. Adhesives are in high demand in the packaging, automotive, construction, and electronics industries, which is boosting market expansion. Because of the increasing need for sophisticated and sustainable adhesive technology in the packaging, healthcare, and automotive industries, North America is one of the world’s major adhesive additives markets.

In Addition, Latin America, the Middle East, and Africa are witnessing consistent market expansion, owing to growing industrialization and building activity, as well as investments in the manufacturing and infrastructure industries. Increased awareness of the importance of sustainable adhesives has also contributed to their market expansion.

Key Regions and Countries

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- North America

- The US

- Canada

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Tier-1 leaders hold a strong position in the adhesive additives market due to vertically integrated specialty chemical operations, global production networks, broad product portfolios, and large segment-level revenues. Henkel AG remains one of the strongest adhesive-focused players. Its Adhesive Technologies business generated €10.97 billion in fiscal 2024, equal to nearly 50.8% of the group’s total €21.586 billion sales. Growth was supported by 2.4% organic expansion, mainly from Mobility and Electronics applications.

Competition is being shaped by M&A, bio-based additives, silicone-hybrid systems, and portfolio optimization. Companies such as 3M, Ashland, Croda, Lubrizol, Momentive, Solvay, and Elementis continue to defend positions in pressure-sensitive additives, rheology modifiers, silicone emulsions, and bio-derived tackifiers.

The Major Players in The Industry

- BASF

- Dow

- Evonik Industries

- Arkema

- Henkel

- 3M

- Sika

- Ashland

- Croda International

- Clariant

- Elementis

- Lubrizol

- Eastman Chemical Company

- Solvay

- Wacker Chemie

- Momentive

- Other Key Players

Recent Development

- 2026: Henkel signed a definitive agreement to acquire Switzerland-based ATP Adhesive Systems AG from Arsenal Capital Partners on January 16, 2026. ATP is a leading producer of high-performance, water-based specialty adhesive tapes for automotive, electronics, medical, construction, and graphics applications. The company employs around 700 people and was expected to generate nearly €270 million in sales in fiscal year 2025. This acquisition strengthens Henkel’s Adhesive Technologies business and expands its position in the specialty tapes segment.

- 2026: Henkel entered into an agreement to acquire the Netherlands-based Stahl Group from Wendel SE on February 4, 2026. The transaction was valued at approximately €2.1 billion, or nearly USD 2.48 billion. Stahl is a global leader in high-performance specialty coatings for flexible materials. Along with the ATP deal, Henkel committed to two major acquisitions valued at nearly €2.4 billion, making this one of the company’s largest recent expansion moves in Adhesive Technologies.

- 2026: Sika signed a binding agreement to acquire Turkey-based Akkim Sealants & Adhesives on February 12, 2026. Akkim manufactures polyurethane foams, adhesives, sealants, and coatings. The company operates 2 production facilities in Turkey and Romania, while a 3rd facility is under construction in Turkey. Akkim generated net sales of nearly CHF 220 million, or around USD 286 million, in 2025. The deal is expected to close in Q3 2026, subject to regulatory approval, and will strengthen Sika’s position in EMEA construction and industrial adhesive markets.

- 2025: Evonik started expanding production capacity for its silane-functionalized polybutadiene products under the POLYVEST® brand on June 25, 2025. These materials are used as binder and additive resins in adhesives, sealants, coatings, rubber compounds, and tires. The expansion was planned for completion by Q3 2025. This strategic multi-million-euro investment is expected to reduce lead times, improve supply reliability, and support rising demand from automotive and construction adhesive applications.

- 2026: Evonik commissioned its expanded specialty amines facility in Nanjing, China, in April 2026, following the start of construction in late 2024. The project involved a double-digit million-euro investment. The facility targets amine-based curing agents and additives used in polyurethane foams, epoxy systems, automotive adhesives, construction adhesives, and industrial adhesive formulations. The site operates on 100% green electricity and is designed to strengthen Evonik’s CASE supply chain across Asia.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$4.2 Bn |

| Forecast Revenue (2035) | US$7.5 Bn |

| CAGR (2026-2035) | 6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Rheology Modifiers, Defoamers, Tackifiers, Plasticizers, Wetting & Dispersing Agents, and Others), By End-use Industry (Building & Construction, Packaging Industry, Automotive & Transportation, Electrical & Electronics, Healthcare, Industrial Manufacturing, Consumer Goods, Aerospace, Marine, and Others), |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | BASF Company, Dow Company, Evonik Industries Company, Arkema Company, Henkel Company, 3M Company, Sika Company, Ashland Company, Croda International Company, Clariant Company, Elementis Company, Lubrizol Company, Eastman Chemical Company, Solvay Company, Wacker Chemie Company, Momentive Company, and Other Key Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |