Quick Navigation

- Report Overview

- Key Takeaways

- By Type Analysis

- By Technology Analysis

- By Station Analysis

- By Voltage Analysis

- By Current Analysis

- By Installation Analysis

- By End-use Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

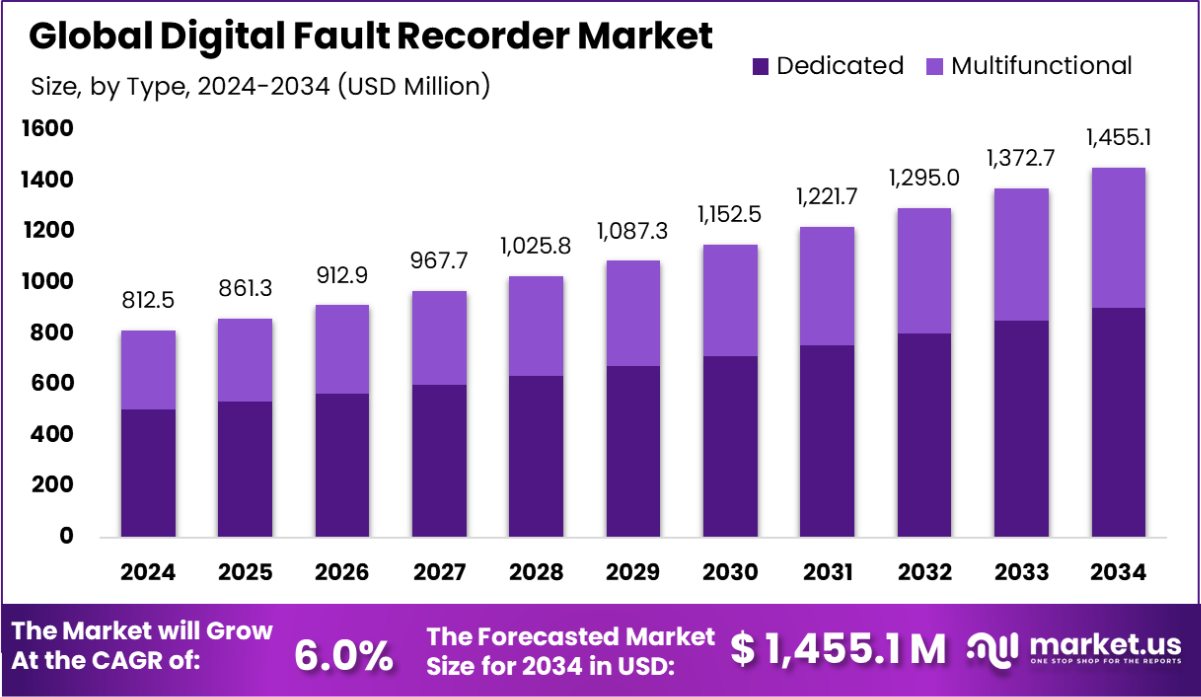

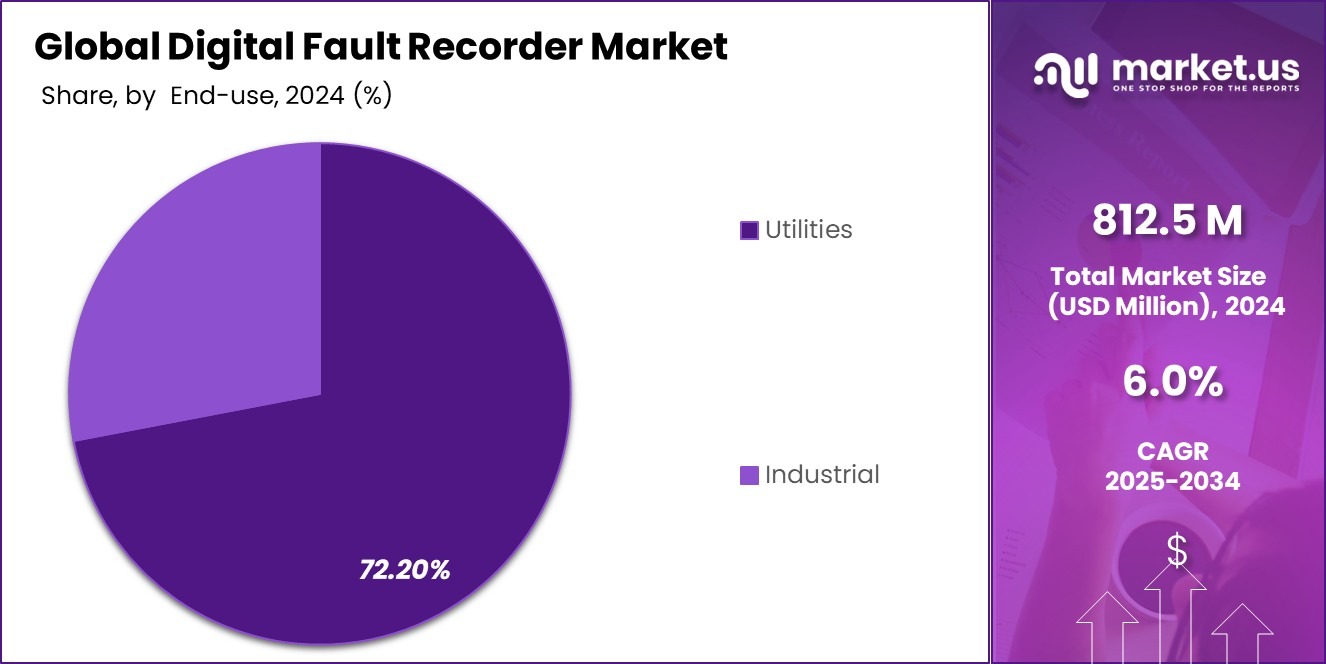

Global Digital Fault Recorder Market is expected to be worth around USD 1,455.1 Million by 2034, up from USD 812.5 Million in 2024, and grow at a CAGR of 6.0% from 2025 to 2034. Rising infrastructure upgrades in Asia-Pacific drove Digital Fault Recorder installations worth USD 351.2 million in 2024.

A Digital Fault Recorder (DFR) is a critical device used in the power distribution sector, designed to monitor and record information about electrical disturbances. It captures the data related to these disturbances, which can include voltage, current, frequency, and waveform anomalies within the power system. This information is vital for analyzing and diagnosing faults in electrical grids, helping to prevent future failures and improve reliability.

The Digital Fault Recorder market is expanding due to several factors. Increased investments in grid modernization initiatives across various countries are driving the demand for advanced monitoring equipment like DFRs. As power networks become more complex and the cost of downtime grows, the need for precise fault recording devices that can help in the quick restoration and maintenance of power systems is becoming essential.

One significant growth factor in the DFR market is the rising emphasis on renewable energy sources. The integration of renewable energy sources requires robust grid management and fault detection systems to handle variable power outputs and maintain stability. DFRs play a crucial role in this context, ensuring smooth operations and minimizing outages.

Moreover, the demand for DFRs is bolstered by the global push for more resilient power infrastructures. As regions experience extreme weather conditions and increased load demands, the role of DFRs in enhancing the resilience and efficiency of power distribution networks becomes more pronounced.

Opportunities in the Digital Fault Recorder market are vast, especially with the advent of smart grid technologies. Smart grids employ digital communications and IoT technology, which are compatible with DFRs, to enhance the automation and communication within the grid.

Key Takeaways

- Global Digital Fault Recorder Market is expected to be worth around USD 1,455.1 Million by 2034, up from USD 812.5 Million in 2024, and grow at a CAGR of 6.0% from 2025 to 2034.

- The dedicated type holds a 62.20% share, dominating the digital fault recorder market with robust installations worldwide.

- High-speed disturbance recording technology captures 53.20% market share, enabling fast and precise fault analysis globally.

- Non-automated stations contribute 67.10% to the market, reflecting the demand for simplified and cost-effective systems.

- The voltage range of 66 kV to 220 kV accounts for 47.20% of market demand.

- Digital fault recorders with 100 A to 150 A capacity represent 45.20% of installations.

- Transmission installations capture a 43.10% share, showcasing widespread deployment across regional grid networks.

- Utilities lead the market with a 72.20% share, prioritizing grid reliability and power quality improvements.

- The market in Asia-Pacific was valued at USD 351.2 million, indicating strong regional demand growth.

By Type Analysis

Dedicated type dominates the Digital Fault Recorder Market with a 62.20% global share.

In 2024, Dedicated held a dominant market position in the By Type segment of the Digital Fault Recorder Market, with a 62.20% share. This significant lead highlights the strong preference among utilities and industrial users for dedicated systems that offer high reliability, continuous monitoring, and enhanced fault analysis capabilities.

Dedicated digital fault recorders are typically installed in substations and are designed for long-term service with minimal maintenance, making them ideal for high-voltage transmission networks.

The prevalence of Dedicated systems can be attributed to their robust architecture, real-time event capturing, and integration ease with SCADA and protection systems. These systems have gained traction, especially in regions experiencing grid modernization, including North America and Europe, where aging infrastructure demands precise and uninterrupted fault detection.

By Technology Analysis

High-speed disturbance recording holds 53.20% of the Digital Fault Recorder Market segmentation.

In 2024, High-speed Disturbance Recording held a dominant market position in the By Technology segment of the Digital Fault Recorder Market, with a 53.20% share. This leading share is attributed to its capability to capture transient events and disturbances with high accuracy and speed, making it a critical tool for power system monitoring and protection. Utility operators and grid managers have increasingly preferred high-speed systems to ensure minimal downtime, enhance fault analysis, and support grid resilience.

The growing complexity of modern power systems, coupled with the integration of renewable energy sources, has amplified the need for precise and real-time fault diagnostics. High-speed Disturbance Recorders address these requirements effectively by delivering superior sampling rates and faster data processing, which has driven their adoption across substations and transmission networks. Their compatibility with modern grid infrastructure further reinforces their market penetration.

Additionally, regulatory mandates focusing on grid reliability and the prevention of cascading failures have supported the accelerated deployment of these systems globally. With key market players investing in high-performance, AI-integrated solutions, the high-speed Disturbance Recording segment is expected to maintain its leadership position in the coming years. This trend reflects a strategic shift towards proactive fault management and smarter grid operations.

By Station Analysis

Non-automated stations lead the Digital Fault Recorder Market with a 67.10% adoption rate.

In 2024, Non-Automated held a dominant market position in the By Station segment of the Digital Fault Recorder Market, with a 67.10% share. This significant share reflects the continued reliance on conventional substations across various developing regions where modernization is progressing gradually. Non-automated stations remain prevalent due to their lower installation and maintenance costs, along with the established infrastructure that supports legacy systems.

Many utility companies have not fully transitioned to automated substations, particularly in regions with constrained budgets and less regulatory pressure for automation. As a result, digital fault recorders tailored for non-automated environments continue to witness strong demand. These systems are essential for event recording and fault diagnosis, even in traditional station setups, offering utilities an effective way to monitor grid performance without major upgrades.

The dominance of this segment also indicates a phased approach by many utilities, opting for incremental technology adoption rather than full-scale substation automation. In such settings, digital fault recorders function as critical standalone tools, ensuring grid stability and operational continuity. Despite the gradual rise of automated substations, the Non-Automated segment is expected to sustain its stronghold in the near term, supported by ongoing usage in aging power infrastructure and cost-sensitive markets.

By Voltage Analysis

66 kV to 220 kV range covers 47.20% Digital Fault Recorder Market.

In 2024, 66 kV to 220 kV held a dominant market position in the By Voltage segment of the Digital Fault Recorder Market, with a 47.20% share. This voltage range is widely used in transmission and sub-transmission networks, making it a critical part of power infrastructure in both developed and emerging economies. The strong presence of utilities operating within this voltage class has driven consistent demand for digital fault recorders, ensuring rapid fault detection and event analysis.

Substations and grid infrastructure within this voltage category serve as vital links between generation and distribution networks. As such, monitoring equipment like digital fault recorders is essential to ensure reliability and prevent outages. Utilities prioritize fault recorders for these voltage levels due to their role in improving operational efficiency and system restoration after disturbances.

The 66 kV to 220 kV segment also benefits from grid expansion projects, especially in countries focusing on strengthening mid-range transmission capabilities. These projects often include upgrades that integrate digital fault recorders to enhance grid observability. The segment’s dominant share indicates its alignment with the ongoing need for efficient monitoring of medium-voltage networks.

By Current Analysis

The current range of 100 A to 150 A contributes 45.20% market share.

In 2024, 100 A to 150 A held a dominant market position in the By Current segment of the Digital Fault Recorder Market, with a 45.20% share. This range is widely suitable for medium-voltage transmission and distribution systems, where accurate current measurement and event detection are essential for operational reliability. Utilities and grid operators frequently deploy digital fault recorders in this current range to monitor critical nodes and prevent prolonged outages.

The 100 A to 150 A segment benefits from its adaptability across a broad spectrum of substation applications, particularly where moderate current levels are standard. These systems offer a balance between performance and cost, making them a preferred choice for utilities focused on upgrading legacy infrastructure with minimal capital expenditure. Their widespread compatibility with existing setups further boosts their adoption in grid modernization efforts.

The segment’s strong market presence also reflects a trend toward optimized monitoring in mid-load networks, where fault detection and transient recording are essential to maintain grid stability. As the global power infrastructure continues evolving, digital fault recorders within this current range remain critical for accurate diagnostics and system restoration.

By Installation Analysis

Transmission installations account for 43.10% of the Digital Fault Recorder Market.

In 2024, Transmission held a dominant market position in the By Installation segment of the Digital Fault Recorder Market, with a 43.10% share. This leading position reflects the critical role of transmission networks in maintaining grid stability across long-distance power transfers. As transmission lines are more vulnerable to faults due to environmental exposure and higher voltage loads, the demand for digital fault recorders in this segment remains strong.

Digital fault recorders installed in transmission networks help utilities identify, locate, and analyze faults swiftly, minimizing outage durations and preventing system-wide disruptions. The 43.10% share highlights the increasing prioritization of grid reliability and real-time event detection in transmission infrastructure. These systems provide time-synchronized data crucial for understanding complex disturbances and for post-event analysis.

Utilities and grid operators continue investing in transmission system upgrades, particularly in regions expanding their inter-regional power exchanges. The deployment of high-voltage lines to support renewable energy integration and cross-border energy trade has further driven the need for advanced monitoring tools like digital fault recorders.

By End-use Analysis

Utilities drive the Digital Fault Recorder Market, capturing a dominant 72.20% share.

In 2024, Utilities held a dominant market position in the By End-use segment of the Digital Fault Recorder Market, with a 72.20% share. This significant market share reflects the central role utilities play in operating, maintaining, and modernizing power transmission and distribution networks. Digital fault recorders are essential tools for utilities to monitor system stability, detect faults, and perform real-time diagnostics, ensuring uninterrupted power delivery.

The high share indicates widespread adoption of digital fault recorders across substations managed by public and private utilities. These systems enable detailed fault analysis and post-event reviews, helping utilities improve grid reliability and reduce restoration time. With increasing demand for stable electricity supply and aging infrastructure, utilities are investing in advanced monitoring systems to enhance fault detection and response capabilities.

Key Market Segments

By Type

- Dedicated

- Multifunctional

By Technology

- High-speed Disturbance Recording

- Low-speed Disturbance Recording

- Steady-state Recording

By Station

- Non-Automated

- Automated

By Voltage

- Up 66 kV

- 66 kV to 220 kV

- Above 220 kV

By Current

- Upto 100 A

- 100 A to 150 A

- Above 150 A

By Installation

- Generation

- Transmission

- Distribution

By End-use

- Utilities

- Industrial

- Renewable Energy

- Transportation

- Others

Driving Factors

Growing Focus on Grid Reliability and Stability

One of the top driving factors for the Digital Fault Recorder (DFR) Market in 2024 is the increasing focus on improving grid reliability and stability. Power grids around the world are getting more complex due to rising electricity demand, integration of renewable energy, and aging infrastructure. Utilities and grid operators need to monitor and respond to faults quickly to avoid large-scale blackouts and equipment damage.

Digital fault recorders help detect faults, analyze disturbances, and improve system performance. With many countries upgrading their transmission and distribution networks, DFRs have become essential tools. Their ability to provide real-time data and event analysis supports faster recovery and better system planning, making them a key technology in modern grid management.

Restraining Factors

High Installation and Maintenance Costs Limit Adoption

A major restraining factor for the Digital Fault Recorder (DFR) Market is the high cost of installation and maintenance. Many utilities, especially in developing regions, operate with limited budgets and may hesitate to invest in advanced monitoring systems. Installing DFRs requires not only purchasing the equipment but also upgrading existing infrastructure, integrating with communication systems, and training personnel.

Ongoing maintenance adds to the total cost of ownership. These expenses can be a significant barrier for smaller power companies or rural networks. While DFRs offer long-term benefits in fault detection and grid stability, the upfront financial burden slows down adoption, particularly in regions where immediate returns on investment are difficult to achieve.

Growth Opportunity

Smart Grid Expansion Creates Strong Market Opportunity

A key growth opportunity for the Digital Fault Recorder (DFR) Market lies in the global expansion of smart grids. As countries modernize their power systems, they are increasingly adopting smart grid technologies to improve efficiency, reliability, and automation. Digital fault recorders play a vital role in this transition by offering real-time fault detection, accurate event recording, and system analysis.

Their integration with smart grid systems enables faster response to faults and better decision-making. Governments and utilities are investing heavily in smart infrastructure to support renewable energy and manage demand. This shift opens up strong opportunities for DFR manufacturers, especially those offering intelligent, scalable, and communication-enabled solutions tailored for advanced grid networks in both developed and emerging markets.

Latest Trends

Integration of AI for Smarter Fault Analysis

One of the latest trends in the Digital Fault Recorder (DFR) Market is the integration of Artificial Intelligence (AI) for smarter and faster fault analysis. Traditional DFRs record data during faults, but analyzing this data manually can take time.

With AI, utilities can automatically identify patterns, locate faults, and even predict future failures based on historical data. This not only speeds up decision-making but also improves grid reliability.

AI-powered DFRs help reduce downtime, enhance system protection, and optimize maintenance schedules. As power grids become more complex with renewable energy and distributed generation, the need for intelligent, automated solutions is rising. This trend is pushing manufacturers to design DFRs that are smarter, more efficient, and future-ready.

Regional Analysis

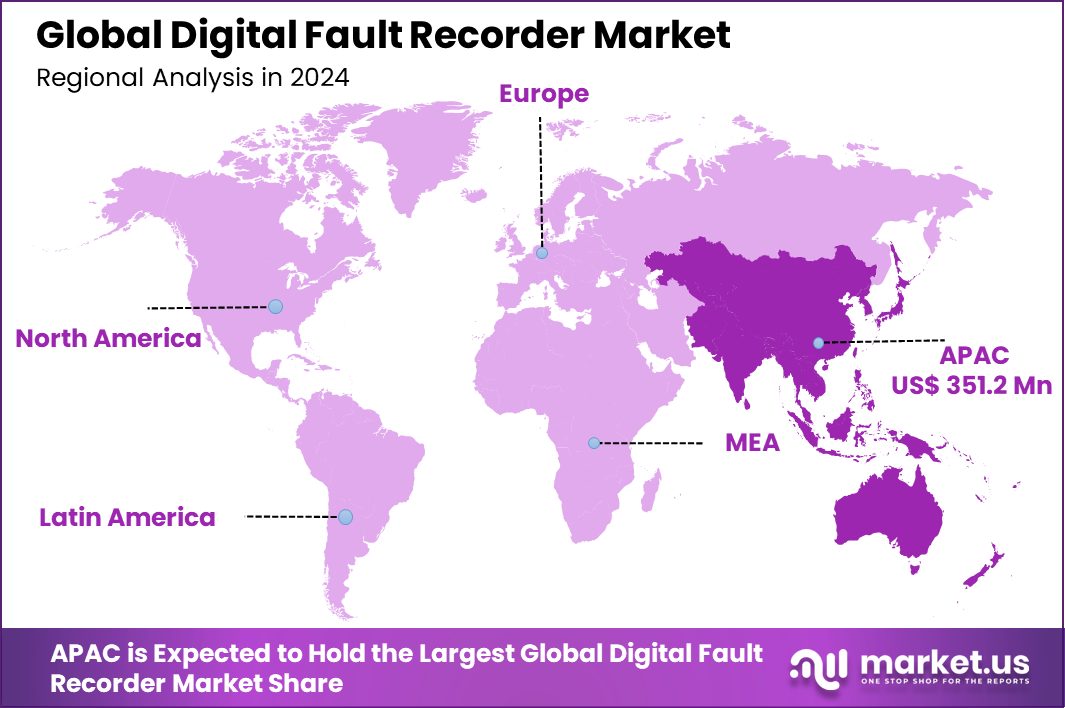

In 2024, Asia-Pacific led the Digital Fault Recorder Market with a 43.20% share regionally.

The Asia-Pacific region dominated the global Digital Fault Recorder market, capturing a significant share of 43.20%, valued at USD 351.2 million. This leadership position is primarily attributed to the rapid expansion of power infrastructure and growing grid modernization initiatives across major economies like China, India, and Japan. The region’s strong industrial base and rising demand for uninterrupted power supply further drive the adoption of digital fault recorders.

In North America, steady growth is observed due to ongoing investments in smart grid technologies and aging transmission infrastructure upgrades, particularly in the United States and Canada.

Europe follows closely, with countries like Germany, France, and the UK prioritizing renewable integration and grid reliability, encouraging the deployment of advanced monitoring systems. The Middle East & Africa region is gradually advancing, supported by increasing electricity demand and grid resilience projects in the Gulf countries and South Africa.

Latin America showcases a growing focus on power transmission efficiency, with Brazil and Mexico being key contributors. Despite regional differences in technological maturity and investment pace, each geography continues to recognize the value of digital fault recorders in improving grid stability and incident analysis.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

ABB remains a market leader, leveraging its robust product portfolio and global service network. In 2024, ABB strengthened its position by expanding its digital substation offerings, integrating its DFRs with broader grid automation solutions. With the rise of smart grids and renewable energy sources, ABB’s ability to offer scalable, real-time fault detection systems has made it a preferred partner for utilities and transmission operators, especially in Asia-Pacific and Europe.

Ametek, known for its high-precision electronic instruments, continued to demonstrate steady performance in the DFR market. The company has strategically focused on enhancing the capabilities of its digital fault recording devices through advanced analytics, event reporting, and data logging features. In 2024, Ametek’s fault recorders found increasing demand in North America and the Middle East, particularly in utility modernization projects and critical infrastructure applications.

Ducati Energia maintained its relevance with its specialized fault recording systems tailored for medium-voltage networks and industrial applications. In 2024, the company emphasized compact, high-reliability solutions with remote diagnostics, appealing to customers in emerging markets like Latin America and Southeast Asia. Ducati Energia’s strength lies in its customization and European manufacturing quality, allowing it to secure niche segments despite intense competition.

Top Key Players in the Market

- ABB

- Ametek

- Ducati Energia

- Elspec

- ERLPhase Power

- GE Grid Solutions, LLC

- Kinkei System Corporation

- Kocos

- Logiclab

- Qualitrol Company

- Siemens

- DUCATI Energia Spa,

- E-Max Instruments

Recent Developments

- In 2024, Siemens expanded its digital fault recorder line with the SIPROTEC 7KE85, supporting grid reliability. With €75.9B in revenue and €9.0B net income, Siemens focused on smarter power monitoring across high-voltage systems and energy infrastructure worldwide.

- In 2024, E-MAX introduced new AC Current Relays, enhancing their product lineup to meet evolving industry needs.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 812.5 Million |

| Forecast Revenue (2034) | USD 1,455.1 Million |

| CAGR (2025-2034) | 6.0% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Dedicated, Multifunctional), By Technology (High-speed Disturbance Recording, Low-speed Disturbance Recording, Steady-state Recording), By Station (Non-Automated, Automated), By Voltage (Up 66 kV, 66 kV to 220 kV, Above 220 kV), By Current (Upto 100 A, 100 A to 150 A, Above 150 A), By Installation (Generation, Transmission, Distribution), By End-use (Utilities, Industrial (Renewable Energy, Transportation, Others)) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | ABB, Ametek, Ducati Energia, Elspec, ERLPhase Power, GE Grid Solutions, LLC, Kinkei System Corporation, Kocos, Logiclab, Qualitrol Company, Siemens, DUCATI Energia Spa, E-Max Instruments |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |