Quick Navigation

- Report Overview

- Key Takeaways

- Business Benefits of Functional Water

- By Product Analysis

- By Ingredient Analysis

- By Flavour Analysis

- By Packaging Analysis

- By End User Analysis

- By Distribution Channel Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

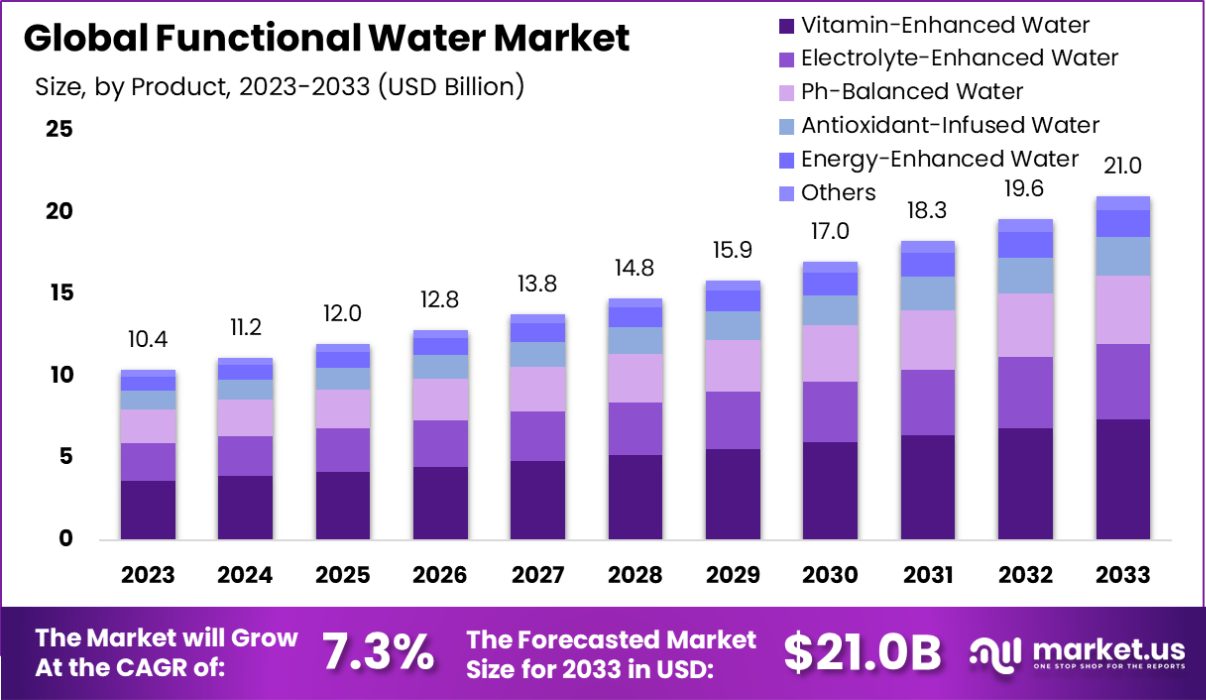

The Global Functional Water Market is expected to be worth around USD 21.0 Billion by 2033, up from USD 10.4 Billion in 2023, and grow at a CAGR of 7.3% from 2024 to 2033. Asia-Pacific Functional Water Market holds a 53.5% share, valued at USD 5.5 billion.

The functional water market is gaining traction in the global beverage industry, combining health-focused innovation with shifting consumer preferences. Functional water, enhanced with vitamins, minerals, amino acids, or antioxidants, offers a convenient hydration option with added health benefits.

The industry features a competitive landscape, with established brands and startups differentiating through natural ingredients, low sugar content, and functional attributes.

Key growth drivers include heightened health awareness and urbanization, particularly in emerging economies. According to the World Health Organization (WHO), 2.2 billion people lack safe drinking water, highlighting the need for innovative hydration solutions. The United Nations’ Sustainable Development Goal 6 also emphasizes clean water and sanitation, pushing brands toward sustainable production and eco-friendly packaging.

Trends in the segment include personalization, plant-based ingredients, and targeted functionalities like immunity-boosting and energy enhancement. Advances in ingredient absorption and recyclable packaging further align with consumer preferences for efficacy and sustainability.

Significant growth opportunities lie in regions like Asia-Pacific, which are driven by rising disposable incomes and urbanization. Strategic collaborations and investments in research will further fuel innovation and expansion, positioning functional water as a key player in the health and wellness industry.

The functional water market is poised for robust growth as it aligns with evolving consumer preferences for health-centric and sustainable hydration solutions. Functional water, enriched with vitamins, minerals, and bioactive compounds, bridges the gap between traditional hydration and wellness-driven consumption.

The industry is characterized by innovation, with established brands and startups leveraging advancements in ingredient delivery and sustainable packaging to meet consumer demands. Rising health awareness, urbanization, and a shift toward healthier lifestyles continue to fuel demand across diverse demographics.

Supporting this momentum, investments in water infrastructure underscore the critical importance of water accessibility and quality. The Environmental Protection Agency (EPA) estimates a $743 billion investment is required over the next 20 years to upgrade and maintain U.S. water infrastructure.

Programs like the Drinking Water State Revolving Fund (DWSRF), with $1.358 billion allocated in FY 2022 (a $232 million increase), and the Water Infrastructure Finance and Innovation Act (WIFIA), which issued $9 billion in loans to support $20 billion worth of projects, reflect this priority. Notably, WIFIA-financed projects serve over 31 million people and support 49,000 jobs.

These developments, coupled with consumer-driven trends like personalized health solutions and eco-conscious practices, position the functional water market as a critical segment within the broader beverage industry, with significant potential for long-term growth.

Key Takeaways

- The Global Functional Water Market is expected to be worth around USD 21.0 Billion by 2033, up from USD 10.4 Billion in 2023, and grow at a CAGR of 7.3% from 2024 to 2033.

- Vitamin-enhanced water dominates the market, accounting for 35.4% of the product segment.

- Micronutrients lead the ingredient category, representing 55.1% of the functional water market share.

- Fruit-flavoured functional water captures 43.2%, driven by consumer preference for natural and refreshing options.

- Bottles hold the majority share at 52.3%, reflecting their convenience and widespread consumer acceptance.

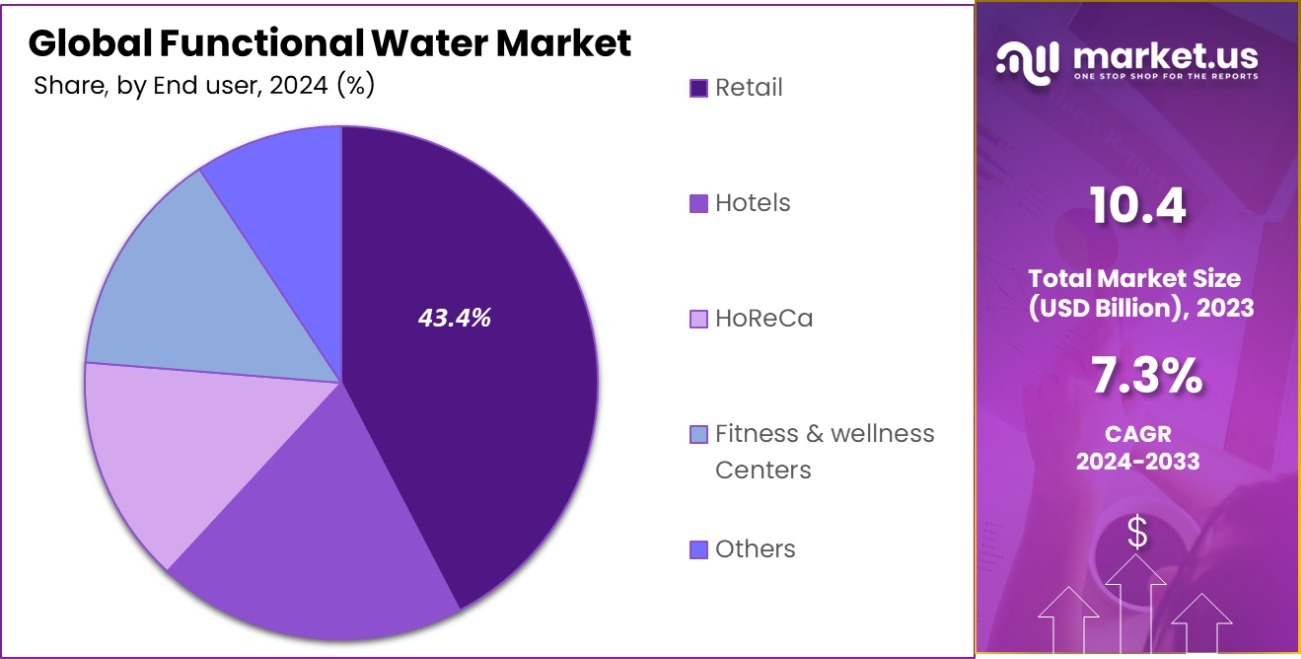

- Retail accounts for 43.4%, highlighting strong demand from individual consumers seeking health-focused hydration solutions.

- Supermarkets and hypermarkets dominate with 46.2%, offering accessibility and variety to consumers.

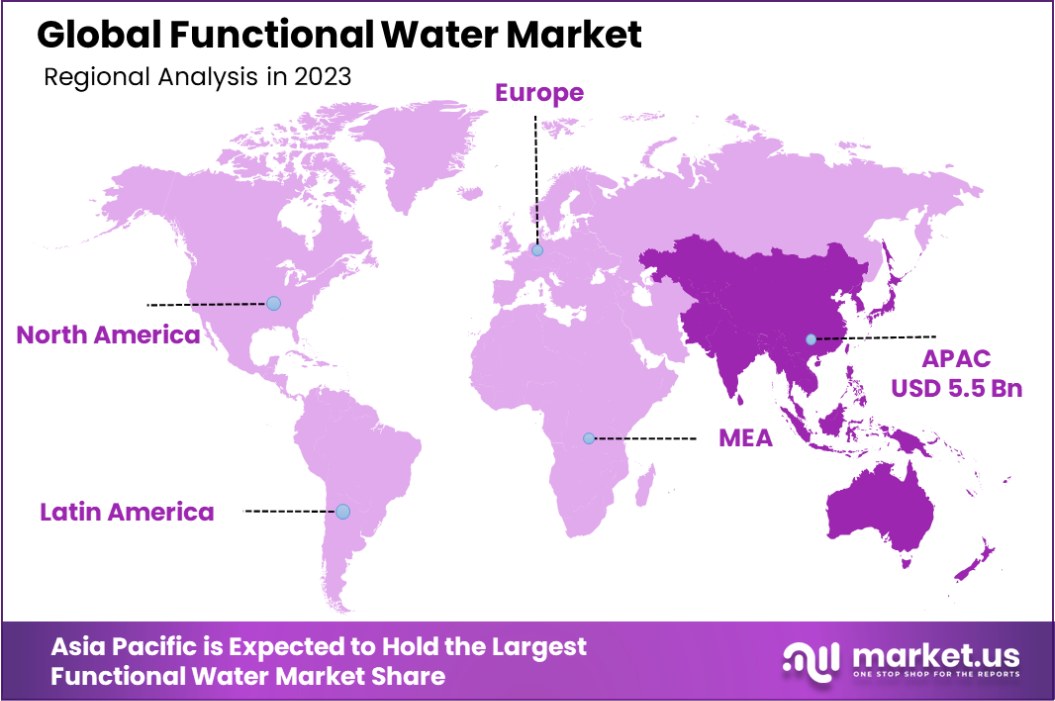

- The Asia-Pacific Functional Water Market holds a 53.5% share, valued at USD 5.5 billion.

Business Benefits of Functional Water

Functional water, enhanced with beneficial nutrients, offers significant business advantages by meeting the growing consumer demand for healthier beverage options. This demand has led to increased sales and market expansion for companies in the beverage industry.

Governments play a crucial role in supporting this sector through various initiatives. For instance, the U.S. Food and Drug Administration (FDA) regulates the labeling and health claims of functional beverages, ensuring consumer safety and product transparency. Additionally, the U.S. Department of Agriculture (USDA) provides guidelines on the inclusion of vitamins and minerals in beverages, promoting public health.

In the European Union, the European Food Safety Authority (EFSA) evaluates health claims related to functional foods and beverages, ensuring that products meet stringent safety and efficacy standards. This regulatory oversight helps maintain consumer trust and supports market growth.

Furthermore, government-funded research into nutrition and public health informs industry practices, encouraging the development of functional beverages that align with dietary guidelines and health recommendations. Such support fosters innovation and helps businesses cater to the evolving preferences of health-conscious consumers.

By Product Analysis

Vitamin-enhanced water holds 35.4% of the market, driven by growing health-conscious consumer demand worldwide.

In 2023, Vitamin-enhanced water held a dominant market position in the by-product segment of the Functional Water Market, with a 35.4% share. This segment’s robust performance can be attributed to increasing consumer awareness about health benefits such as enhanced immune function and increased energy levels.

Following closely, Electrolyte-enhanced water captured a 25.6% market share, favored for its benefits in hydration and replenishment of essential minerals post-exercise.

pH-balanced water, with a 19.8% share, appealed to consumers seeking to maintain or restore a natural pH balance in the body, aiding in preventing various health disorders. Antioxidant-infused water accounted for 10.5% of the market, popular among those aiming to combat oxidative stress and aging due to its high antioxidant content. Lastly, Energy-enhanced water held an 8.7% share, targeting consumers needing an extra energy boost, often infused with caffeine and B vitamins.

Each of these segments caters to specific consumer health concerns and preferences, driving diversification in the functional water market. This segmentation underscores the trend towards health-oriented beverages, aligning with broader wellness and lifestyle shifts among global consumers.

By Ingredient Analysis

Micronutrients dominate the functional water market with a 55.1% share, highlighting their appeal for targeted nutrition.

In 2023, Micronutrients held a dominant market position in the By Ingredient segment of the Functional Water Market, with a 55.1% share. This segment’s strong performance is primarily due to the growing consumer demand for water products enhanced with vitamins and minerals that support overall health and wellness.

Micronutrients such as zinc, selenium, and magnesium are especially sought after for their immune-boosting, anti-inflammatory, and cardiovascular health benefits.

Botanical Extracts, comprising the remaining 44.9% of the market, have also seen significant growth. These ingredients appeal to consumers interested in natural health solutions and holistic well-being.

Popular botanicals in functional waters include ginseng for energy enhancement, chamomile for relaxation, and elderberry for immune support. The botanical trend taps into the broader consumer shift towards organic and plant-based products, reflecting a preference for ingredients with traditional health associations and minimal processing.

Overall, the By Ingredient segment of the Functional Water Market reflects a clear consumer preference for products that not only hydrate but also offer specific health benefits. This trend is driving innovation and diversification in the functional beverage sector, as manufacturers strive to meet the sophisticated health and wellness needs of modern consumers.

By Flavour Analysis

Fruit-flavored functional water, capturing 43.2%, reflects consumer preference for natural, refreshing, and flavorful hydration options.

In 2023, Fruit-flavoured held a dominant market position in the By Flavour segment of the Functional Water Market, with a 43.2% share. This preference underscores consumers’ ongoing attraction to familiar, refreshing tastes such as citrus, berry, and tropical fruits which make hydration a more appealing and enjoyable experience.

These flavors not only enhance palatability but often are perceived as healthier alternatives to sugary sodas and artificial beverages.

Herb-infused water accounted for 28.9% of the market, appealing to those seeking subtle, sophisticated flavours with added health benefits. Ingredients like mint, lavender, and rosemary are popular for their calming properties and their ability to support digestion and reduce stress.

Tea-infused functional water captured 27.9% of the market share. This segment leverages the traditional benefits of tea—such as antioxidants in green tea and the calming effects of chamomile—combined with the hydrating properties of water. Consumers are drawn to these products for their health benefits, including enhanced metabolic rates and improved heart health.

Overall, the By Flavour segment shows a strong consumer preference for natural, health-promoting ingredients integrated into their daily hydration habits. This trend is likely to persist as consumers continue to seek functional beverages that offer health benefits along with great taste and convenience.

By Packaging Analysis

Bottled packaging leads the market at 52.3%, offering convenience and portability for on-the-go consumers.

In 2023, Bottles held a dominant market position in the By Packaging segment of the Functional Water Market, with a 52.3% share. This packaging type remains a top choice due to its convenience, reusability, and wide availability.

Plastic bottles, especially those made from eco-friendly and recyclable materials, are popular among consumers who prioritize portability and sustainability. Glass bottles also contribute to this segment, offering a premium alternative often associated with higher-quality or artisanal products.

Cans accounted for 20.7% of the market, favored for their lightweight nature and strong appeal among younger demographics looking for trendy, on-the-go beverage options. Tetra Packs followed with a 15.4% share, recognized for their environmental benefits such as compact design and lower carbon footprint, making them suitable for eco-conscious consumers.

Pouches made up 11.6% of the market, appealing particularly to the sports and outdoor activities sector, where flexible and lightweight packaging is highly valued. Pouches are also popular in children’s functional beverages due to their ease of use and fun designs.

Overall, the By Packaging segment highlights the varied consumer preferences in functional water, with a strong leaning towards innovative and sustainable packaging solutions that meet the needs of modern, health-conscious consumers.

By End User Analysis

Retail end-users account for 43.4%, underscoring the dominance of traditional outlets in functional water sales.

In 2023, Retail held a dominant market position in the By End User segment of the Functional Water Market, with a 43.4% share. This segment benefits from widespread consumer access through supermarkets, hypermarkets, and convenience stores, where a vast array of functional water brands and formulations are readily available.

The retail sector’s success is driven by its ability to offer variety and convenience, catering to everyday shoppers looking to integrate health-oriented beverages into their regular diet.

Hotels accounted for 21.2% of the market, leveraging functional waters as a premium amenity to health-conscious travelers and guests seeking wellness-oriented products during their stay. The integration of functional waters into minibars and during meals enhances the overall guest experience, aligning with luxury and wellness trends in hospitality.

HoReCa (Hotels, Restaurants, and Cafés) captured 18.9% of the market share. This sector incorporates functional waters into their beverage menus, providing customers with healthy hydration options that complement their meals and lifestyle.

Fitness and Wellness Centers held 16.5% of the market. These venues prioritize functional waters to support the hydration and recovery needs of fitness enthusiasts and health-focused individuals, emphasizing the performance and health benefits these products offer.

Overall, the By End User segment underscores the broad appeal and integration of functional waters across various consumer touchpoints, reflecting growing health trends and the lifestyle integration of wellness-oriented beverages.

By Distribution Channel Analysis

Supermarkets and hypermarkets represent 46.2%, making them the primary distribution channel for functional water products.

In 2023, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of the Functional Water Market, with a 46.2% share. This channel’s strength lies in its extensive reach and ability to offer a wide assortment of functional water brands and types, catering to a diverse customer base.

Supermarkets and hypermarkets are pivotal for product discovery, providing consumers with the opportunity to explore and compare different functional water options firsthand, which drives impulse purchases and brand switching.

Convenience Stores accounted for 29.1% of the market share, favored for their accessibility and the convenience they offer busy consumers seeking quick hydration solutions. These stores are strategically located in high-traffic areas, making them ideal for grab-and-go purchases.

Online Retail captured 24.7% of the market, reflecting a growing consumer preference for the ease and convenience of home delivery. The online segment has expanded rapidly, supported by robust e-commerce platforms and social media marketing that directly engage with health-conscious consumers, offering detailed product information, customer reviews, and competitive pricing.

Overall, the By Distribution Channel segment showcases the diverse shopping preferences for functional waters, with traditional retail still leading but online channels gaining significant traction due to changing consumer shopping habits.

Key Market Segments

By Product

- Vitamin-enhanced water

- Electrolyte-enhanced water

- pH-balanced water

- Antioxidant-infused water

- Energy-enhanced water

- Others

By Ingredient

- Micronutrient

- Botanical Extract

- Others

By Flavour

- Fruit-flavoured

- Herb-infused

- Tea-infused

- Others

By Packaging

- Bottles

- Cans

- Tetra Packs

- Pouches

- Others

By End user

- Retail

- Hotels

- HoReCa

- Fitness & Wellness Centers

- Others

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail

- Others

Driving Factors

Increasing Health Awareness Among Consumers

As health awareness continues to rise, more consumers are seeking beverages that offer more than just hydration. Functional waters, infused with vitamins, minerals, and other wellness-oriented additives, cater to this demand by providing health benefits like improved immunity, better hydration, and enhanced energy levels.

This shift towards health-conscious living is a significant driver for the functional water market, as individuals increasingly opt for these beneficial alternatives over traditional sodas and high-calorie drinks.

Expansion of Distribution Channels

The accessibility of functional waters has greatly improved with the expansion of distribution channels, including supermarkets, online platforms, and convenience stores. This broadened reach allows consumers to easily find and purchase these products, supporting market growth.

Particularly, the rise of e-commerce has transformed shopping habits, making it convenient for consumers to explore and buy a wide variety of functional water brands from home. The ease of access through these diverse channels enhances consumer engagement and drives sales across different regions.

Innovation in Product Offerings

Innovation is a key factor propelling the functional water market. Manufacturers are continuously introducing new flavors, formulations, and packaging designs to attract consumers. This innovation extends beyond taste to include functional benefits like mood enhancement, energy boosts, and detoxification properties.

By constantly evolving product lines to include trendy ingredients like CBD, collagen, and antioxidants, brands are able to maintain consumer interest and stand out in a competitive market. This ongoing product development is crucial for capturing and retaining consumer interest in a rapidly growing market.

Restraining Factors

High Cost of Functional Waters Compared to Regular Alternatives

The price point of functional waters can be a significant barrier to widespread adoption, particularly in price-sensitive markets. These products often carry a premium due to the cost of added nutrients and specialized manufacturing processes.

Consumers who are used to purchasing regular bottled water may find the higher cost of functional waters unjustifiable, limiting their market penetration and growth, especially among budget-conscious buyers.

Lack of Awareness and Skepticism About Health Claims

Despite growing health consciousness, there remains a considerable segment of consumers who are either unaware of or skeptical about the claimed benefits of functional waters. This skepticism is often fueled by a lack of definitive scientific support for some of the health benefits advertised by these products.

The effectiveness of added nutrients once they are processed and mixed into water can also be questioned by consumers and health experts alike, potentially restraining market growth.

Regulatory Challenges and Compliance Costs

The functional water market faces stringent regulatory challenges across different regions, which can impede growth. These regulations pertain to the health claims made by manufacturers on their packaging and in advertising.

Compliance with these varying regulations incurs additional costs and can delay product launches, especially in markets that are strict about food and beverage endorsements. Navigating these legal requirements can be a significant hurdle for new and existing players in the functional water industry, affecting overall market dynamics.

Growth Opportunity

Emerging Markets Present Expansive Growth Opportunities

Emerging markets offer a significant growth opportunity for the functional water sector due to their rising middle-class populations and increasing health awareness. Countries like China, India, and Brazil are witnessing a surge in disposable incomes, enabling more consumers to spend on health-oriented products, including functional waters.

These markets are relatively untapped compared to saturated Western markets, providing a fresh landscape for brand expansion and large-scale adoption, which could drive substantial revenue growth for companies willing to invest in localizing flavors and marketing strategies.

Integration with Fitness and Wellness Industries

Aligning functional water products with the fitness and wellness industries represents a lucrative growth opportunity. As more consumers adopt fitness regimes and seek out wellness solutions, they demand products that support their health goals, such as hydration and recovery aids.

Functional waters that cater directly to these needs, offering enhancements like electrolytes for hydration or protein for muscle recovery, can carve out a niche in this booming sector. Collaborations with gyms, health clubs, and wellness centers for exclusive product offerings could also amplify brand visibility and market penetration.

Advancements in Product Innovation and Sustainability

There is a growing opportunity to innovate product formulations and enhance sustainability in packaging within the functional water market. Consumers are increasingly attracted to products that not only promote health benefits but also are environmentally friendly.

Developing new, sustainable packaging solutions and expanding the range of health benefits (such as immune support or cognitive enhancement) can meet consumer demands more effectively. Brands that lead in innovation and sustainability are likely to gain a competitive edge, capturing the attention of environmentally conscious consumers looking for multifunctional health products.

Latest Trends

Rise of Natural and Organic Functional Water Varieties

The trend towards natural and organic products is shaping the functional water market significantly. Consumers are increasingly seeking clean-label drinks that are free from artificial additives and preservatives. This shift has prompted manufacturers to develop functional waters using organic fruit extracts, natural flavors, and plant-based compounds that offer health benefits without chemical enhancers.

Brands that can certify their products as organic or all-natural are particularly well-positioned to attract health-conscious consumers who prioritize purity and environmental sustainability in their beverage choices.

Incorporation of Novel Health Ingredients

There’s a growing trend in incorporating novel health ingredients into functional waters, such as CBD, collagen, and adaptogens like ashwagandha and Rhodiola. These ingredients are targeted at consumers looking for specific health benefits, such as stress reduction, improved skin health, and enhanced mental clarity.

As curiosity and awareness around these compounds grow, functional waters infused with these innovative ingredients are gaining popularity, allowing brands to differentiate themselves and cater to niche consumer segments seeking tailored health solutions.

Focus on Customization and Personalization

Customization and personalization are becoming key trends in the functional water market. Consumers are looking for products that can be tailored to their specific dietary needs and health goals. Brands are responding by offering customizable mix-and-match flavor packets or concentrates that can be added to water, enabling consumers to control the type and amount of functional ingredients they consume.

This trend is supported by digital platforms and apps that help users track their hydration and nutritional intake, making functional waters an integral part of personalized wellness regimes.

Regional Analysis

In 2023, the Asia-Pacific Functional Water Market dominated with a 53.5% share, valuing USD 5.5 billion.

The Functional Water Market is distinctly segmented by region, including North America, Europe, Asia Pacific, Middle East & Africa, and Latin America. Dominating these regions, Asia-Pacific stands out with a commanding 53.5% market share, valued at USD 5.5 billion.

This significant lead is fueled by rising health awareness and increasing disposable incomes, particularly in emerging economies such as China and India, where consumers are rapidly adopting healthier hydration options.

In North America, the market is driven by a strong trend towards health and wellness, with consumers showing a preference for functional beverages that offer added health benefits. This region has seen substantial growth due to innovative product launches and strong marketing strategies that emphasize the functional attributes of the water.

Europe follows closely, where there is high demand for products with natural and organic certifications. European consumers are particularly discerning about the ingredients in their beverages, which has led to the increased popularity of functional waters that are free from artificial additives.

The markets in the Middle East & Africa and Latin America are smaller but growing, driven by urbanization and changing lifestyle patterns. As awareness and availability increase, these regions are expected to exhibit higher growth rates in the coming years, although currently, they contribute less significantly to the global market landscape compared to Asia-Pacific, North America, and Europe.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the global Functional Water Market has seen significant contributions from key players, each bringing unique strategies and products to cater to health-conscious consumers worldwide. Among these, several companies stand out due to their innovative approaches and expansive market reach.

Danone S.A. remains a heavyweight in the functional water landscape, leveraging its global brand presence and extensive distribution networks to promote its health-oriented beverage lines. The company continues to focus on sustainability and health, appealing to eco-conscious consumers looking for hydration with added benefits.

The Coca-Cola Company and PepsiCo, Inc. both have expanded their portfolios to include functional waters, responding to the shift away from sugary sodas. These industry giants are utilizing their vast marketing resources to educate consumers and promote functional waters as part of an active lifestyle, which has proven effective in both retaining customers and attracting new demographics.

Nestle S.A. has capitalized on its longstanding reputation for quality by introducing a range of functional waters that address specific health concerns, such as metabolism and energy enhancement. The company’s focus on research and development has allowed it to offer scientifically-backed products that resonate well with health-aware consumers.

Emerging players like Hint Water Inc. and Karma Culture LLC are also making notable inroads into the market by focusing on niche segments, such as naturally flavored and wellness-enhancing waters. These companies are carving out significant spaces for themselves by appealing to younger demographics and fitness enthusiasts who seek products that align with their personal health philosophies and tastes.

In regions such as Asia-Pacific, local companies like Tata Group and Asahi Group Holdings, Ltd. are leveraging local consumer preferences and existing distribution networks to expand their reach in the functional water market. Their products are tailored to meet regional tastes and health trends, which enhances their appeal and market penetration in these rapidly growing markets.

Overall, the competitive landscape in 2023 shows that companies succeeding in the functional water market are those that combine health-oriented innovations with strong brand marketing and sustainable practices, aligning closely with global consumer trends toward health, wellness, and environmental consciousness.

Top Key Players in the Market

- Agua Enerviva LLC

- Asahi Group Holdings, Ltd.

- Balance Water Company LLC.

- Danone S.A.

- Fonterra Co-operative Group

- Hint Water Inc.

- Karma Culture LLC

- Keurig Dr Pepper

- Kona Deep Corporation

- Lucozade Ribena Suntory Limited

- Nestle S.A.

- New Age Beverages Corporation

- Nirvana Water Sciences

- PepsiCo, Inc.

- Pervida Inc.

- Phure Water LLC

- Superbee Network Inc.

- Talking Rain Beverage Company

- Tata Group

- The Coca-Cola Company

- Unique Foods Canada Inc.

Recent Developments

- In 2023, Agua Enerviva LLC focused on expanding its product line with new natural flavor combinations and enhanced formulations featuring electrolytes and caffeine. The company also strengthened its distribution network, targeting health-conscious consumers seeking low-sugar energy beverages.

- In 2023, Asahi Group Holdings, Ltd. advanced sustainability by joining the UN CEO Water Mandate and prioritizing responsible water use. Their 2024 Integrated Report highlights innovative functional beverages aligned with health trends and sustainable environmental practices.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 10.4 Billion |

| Forecast Revenue (2033) | USD 21.0 Billion |

| CAGR (2024-2033) | 7.3% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Vitamin-enhanced water, Electrolyte-enhanced water, pH-balanced water, Antioxidant-infused water, Energy-enhanced water, Others), By Ingredient (Micronutrient, Botanical Extract, Others), By Flavour (Fruit-flavoured, Herb-infused, Tea-infused, Others), By Packaging (Bottles, Cans, Tetra Packs, Pouches, Others), By End user (Retail, Hotels, HoReCa, Fitness and Wellness Centers, Others), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online Retail, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Agua Enerviva LLC, Asahi Group Holdings, Ltd., Balance Water Company LLC., Danone S.A., Fonterra Co-operative Group, Hint Water Inc., Karma Culture LLC, Keurig Dr Pepper, Kona Deep Corporation, Lucozade Ribena Suntory Limited, Nestle S.A., New Age Beverages Corporation, Nirvana Water Sciences, PepsiCo, Inc., Pervida Inc., Phure Water LLC, Superbee Network Inc., Talking Rain Beverage Company, Tata Group, The Coca-Cola Company, Unique Foods Canada Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |