Quick Navigation

Report Overview

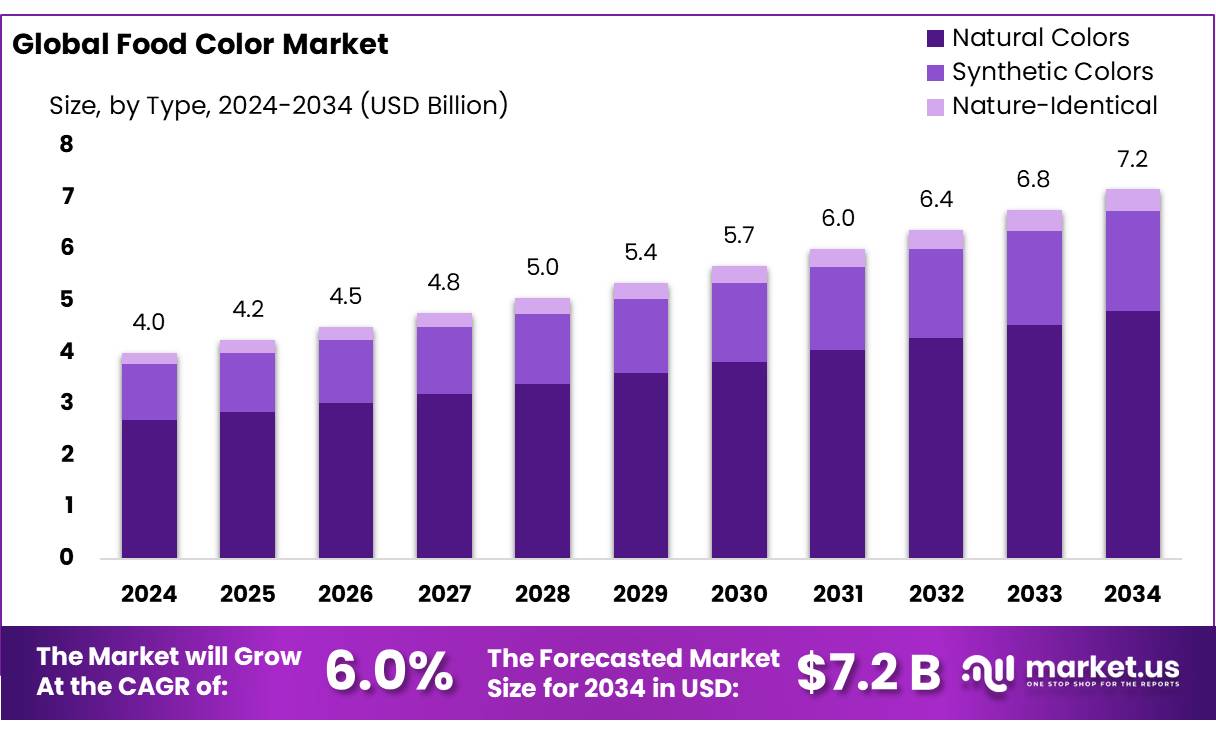

The Global Food Color Market size is expected to be worth around USD 7.2 Billion by 2034, from USD 4.0 Billion in 2024, growing at a CAGR of 6.0% during the forecast period from 2025 to 2034.

The food color industry is a dynamic sector that plays a pivotal role in enhancing the visual appeal and consumer acceptance of food products. Food colorants are categorized into synthetic, natural, and nature-identical types, each serving distinct purposes in food manufacturing.

Synthetic colors are widely used due to their stability and cost-effectiveness, while natural colorants, derived from plant, animal, or mineral sources, are gaining popularity owing to consumer preference for clean-label products. In 2024, the global market for food colorants was valued at approximately USD 2.3 billion and is expected to witness steady growth in the coming years, driven by consumer preferences for safer, plant-based options.

Government initiatives play a pivotal role in shaping the industry’s trajectory. In April 2025, the U.S. Food and Drug Administration (FDA), in collaboration with the Department of Health and Human Services (HHS), announced plans to phase out petroleum-based synthetic food dyes by the end of 2026. This initiative aims to replace artificial dyes with natural alternatives such as gardenia blue and butterfly pea flower extract, addressing health concerns associated with synthetic dyes.

Several factors are driving growth in the food color industry. The rise in consumer demand for visually appealing and innovative products, especially among the younger demographic, is a key growth driver. Additionally, the growing awareness around the harmful effects of synthetic additives and the increasing preference for natural, plant-based food colors is contributing to the industry’s expansion. Government regulations and initiatives also play a significant role. For instance, the U.S. Food and Drug Administration (FDA) has established guidelines for the safe use of food additives, ensuring the safety of food colorants used in the market.

Key Takeaways

- Food Color Market size is expected to be worth around USD 7.2 Billion by 2034, from USD 4.0 Billion in 2024, growing at a CAGR of 6.0%.

- Natural Colors held a dominant market position, capturing more than a 67.2% share in the global food color market.

- Plants & Animals held a dominant market position, capturing more than a 43.6% share in the food color market.

- Powder held a dominant market position, capturing more than a 58.4% share.

- Dyes held a dominant market position, capturing more than a 66.9% share in the food color market.

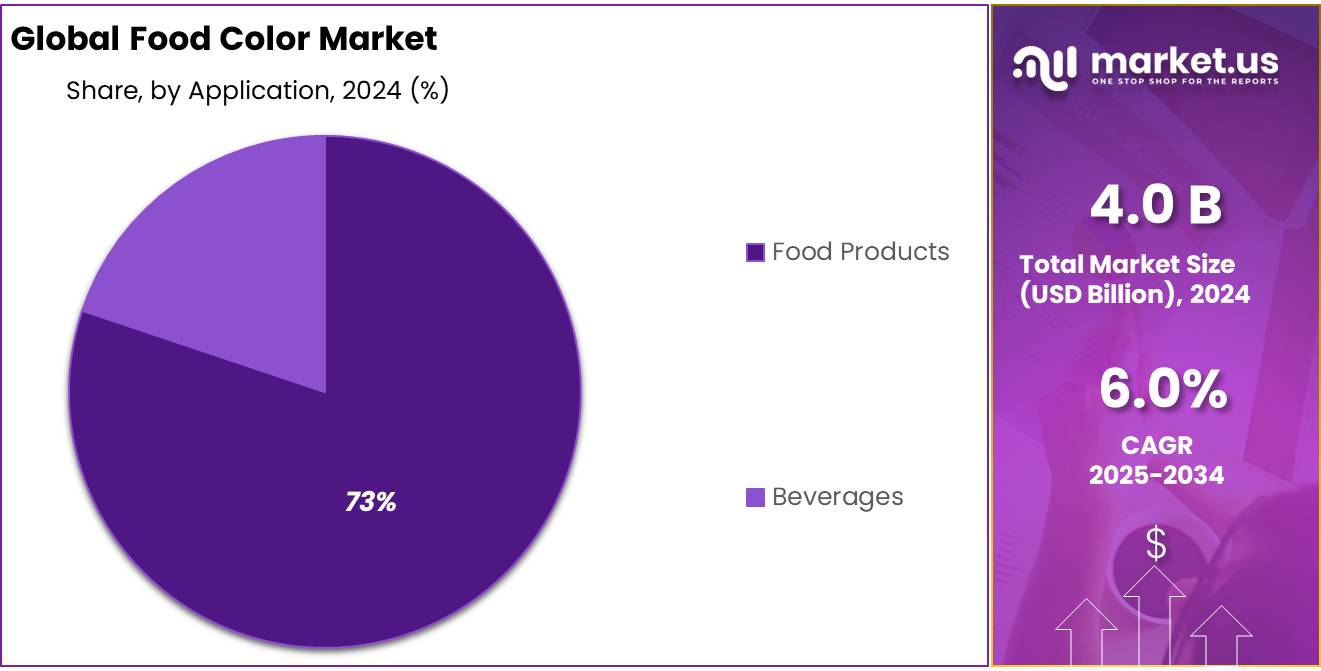

- Food Products held a dominant market position, capturing more than a 73.1% share in the global food color market.

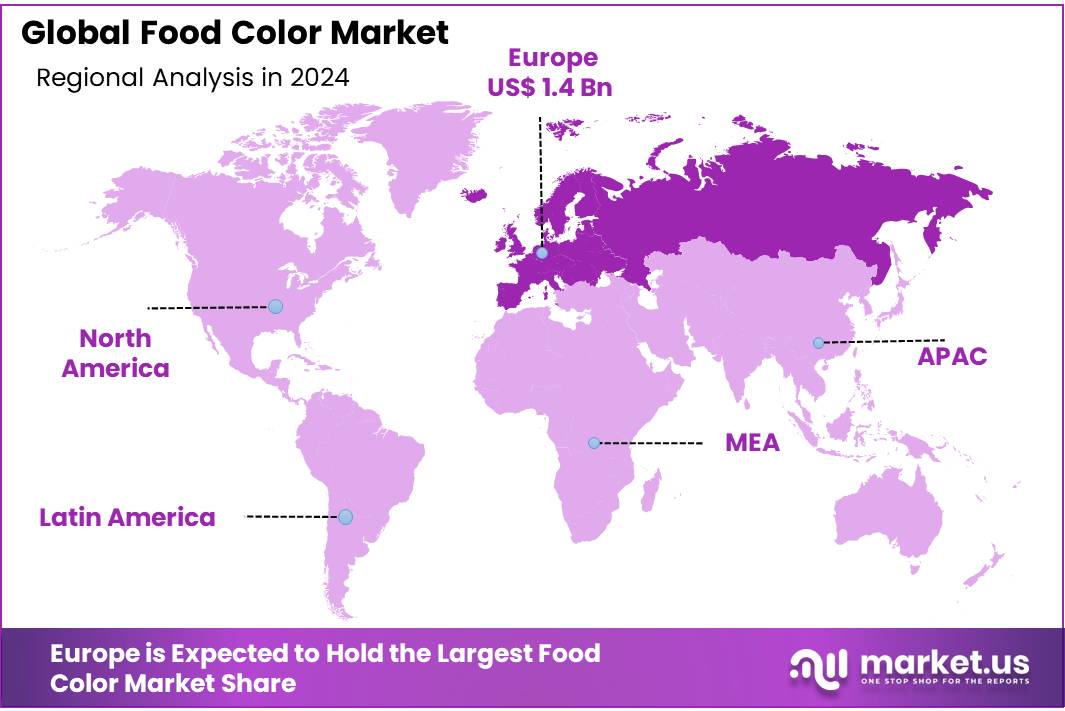

- Europe held a dominant position in the global food color market, capturing approximately 37.2% of the market share, equivalent to a valuation of around USD 1.4 billion.

By Type

Natural Colors dominate with 67.2% in 2024 due to rising clean-label food preferences.

In 2024, Natural Colors held a dominant market position, capturing more than a 67.2% share in the global food color market. This leadership is strongly linked to consumers shifting towards healthier and more transparent food choices. Natural colorants, made from sources like turmeric, beetroot, and spirulina, are now preferred over artificial dyes due to growing awareness about food safety and chemical-free ingredients.

Governments and food safety authorities around the world are also promoting the use of plant-based ingredients in food processing, further boosting the adoption of natural colors. Food companies, especially in bakery, dairy, and beverage sectors, are reformulating products to align with clean-label trends, supporting the rise in demand. With this continued focus on health, the dominance of natural colors is likely to persist and expand through 2025.

By Source

Plants & Animals lead with 43.6% in 2024 as natural sources gain industry trust.

In 2024, Plants & Animals held a dominant market position, capturing more than a 43.6% share in the food color market by source. This segment’s strength comes from the growing popularity of natural ingredients derived from safe, recognizable origins. Manufacturers are increasingly sourcing colors from beetroot, spirulina, turmeric, and cochineal insects to meet clean-label demands and reduce chemical exposure in food.

These sources not only offer rich pigmentation but also align with consumer preferences for transparency and sustainability. Food safety bodies across the world, including FSSAI and FDA, are encouraging this transition through stricter control on synthetic additives. As plant- and animal-based colorants are generally accepted in global regulations, their use is expanding in beverages, dairy, confectionery, and frozen food categories. This upward trend is likely to hold firm through 2025, supported by cleaner sourcing and ethical processing practices.

By Form

Powder form leads with 58.4% in 2024 due to longer shelf life and easy use.

In 2024, Powder held a dominant market position, capturing more than a 58.4% share in the global food color market by form. Its popularity comes from being easy to store, lightweight, and having a much longer shelf life compared to liquid or gel forms. Food manufacturers prefer powder colors because they blend well in dry mixes and processed foods like snacks, baked goods, and instant noodles.

Another key reason for their dominance is their stability under different processing conditions, such as heat and light, making them ideal for packaged products. This format also allows better control over coloring intensity during production, reducing waste and cost. Given its practicality and compatibility with large-scale food manufacturing, the powder form is expected to remain a favored choice through 2025.

By Solubility

Dyes dominate with 66.9% in 2024 due to vibrant color output and liquid solubility.

In 2024, Dyes held a dominant market position, capturing more than a 66.9% share in the food color market by solubility. Their high solubility in water and ability to produce vivid, consistent colors make them a top choice for beverages, candies, and syrups. Dyes are especially popular in products that require strong visual appeal with minimal quantity. They blend smoothly into liquid-based food and drink items without leaving residue, ensuring a uniform look.

Moreover, dyes offer better cost-efficiency and are easy to scale in industrial settings. While natural options are growing, synthetic and water-soluble dyes continue to be widely used due to their intense pigmentation and processing ease. This dominance is expected to continue in 2025, especially in regions with large-scale beverage and processed food production.

By Application

Food Products lead with 73.1% in 2024 as everyday items demand strong visual appeal.

In 2024, Food Products held a dominant market position, capturing more than a 73.1% share in the global food color market by application. This dominance comes from the high volume of processed and packaged food consumed daily, where colors play a major role in boosting product appeal. From bakery and confectionery to snacks and dairy, food manufacturers use colors to enhance presentation, align with flavor cues, and maintain consistency.

As consumer demand for attractive and colorful food items grows, manufacturers are relying more on safe coloring solutions to meet both regulatory norms and market preferences. The rise in ready-to-eat meals, frozen items, and flavored snacks has also supported this segment’s growth. With visual appearance remaining a key factor in food purchasing decisions, the food products category is expected to hold its strong market position through 2025.

Key Market Segments

By Type

- Natural Colors

- Carmine

- Anthocyanins

- Caramel

- Annatto

- Carotenoids

- Chlorophyll

- Spirulina

- Others

- Synthetic Colors

- Blue

- Red

- Yellow

- Green

- Amaranth

- Carmoisine

- Others

- Nature-Identical

By Source

- Plants & Animals

- Minerals & Chemicals

- Microorganisms

By Form

- Liquid

- Powder

By Solubility

- Dyes

- Lakes

By Application

- Food Products

- Processed Food Products

- Bakery & Confectionery Products

- Meat, Poultry, and Seafood Products

- Oils & Fats

- Dairy Products

- Others

- Beverages

- Juice & Juice Concentrates

- Functional Drinks

- Carbonated Soft Drinks

- Alcoholic Beverages

- Others

Drivers

Rising Demand for Processed Foods

The increasing demand for processed foods stands out as a significant factor propelling the growth of the food color market. As consumers seek convenience and variety, processed food products have become integral to daily diets, leading manufacturers to enhance the visual appeal of their offerings through the use of food colors.

India’s food processing sector exemplifies this trend. In 2023, the sector was valued at USD 307 billion and is projected to more than double, reaching USD 700 billion by 2030. This growth is driven by factors such as urbanization, changing consumer preferences, and supportive government policies. As processed foods become more prevalent, the demand for food colors to enhance product appearance and meet consumer expectations is expected to rise correspondingly.

Government initiatives further bolster this growth. The Production-Linked Incentive Scheme for the Food Processing Industry (PLISFPI), with a budget outlay of ₹10,900 crore, aims to support the production of ready-to-cook and ready-to-eat foods, including processed fruits and vegetables. Such initiatives not only stimulate the processed food sector but also indirectly increase the demand for food colors used in these products.

Moreover, the share of processed food exports within India’s agri-food exports has significantly increased, rising from 13.7% in 2014-15 to 23.4% in 2023-24. This expansion into international markets necessitates adherence to global standards, including the use of approved food colors to meet diverse consumer preferences and regulatory requirements.

Restraints

Strict Regulatory Standards

One significant challenge facing the food color market is the stringent regulatory environment that governs the use of food additives. Regulatory bodies like the Food Safety and Standards Authority of India (FSSAI) have established comprehensive guidelines to ensure consumer safety, which, while essential, can pose hurdles for manufacturers.

For instance, FSSAI’s regulations mandate that food products must be free from added coloring matter unless explicitly permitted. This means that any unauthorized use of colorants can lead to product recalls or legal consequences. Such strict oversight ensures that only safe and approved additives are used, but it also requires manufacturers to stay continually updated with regulatory changes and invest in compliance measures.

Moreover, the process of getting new food colors approved can be lengthy and complex. Manufacturers must provide extensive safety data and undergo rigorous testing procedures, which can delay product launches and increase costs. This is particularly challenging for small and medium-sized enterprises that may lack the resources to navigate these regulatory landscapes effectively.

In addition to national regulations, international standards can also impact the food color market. Exporting products requires compliance with the regulations of the destination country, which may differ significantly from domestic standards. This necessitates additional testing and certification, further complicating the manufacturing process.

Opportunity

Rising Demand for Natural Food Colors in Clean-Label Products

In recent years, the food industry has seen a strong shift toward clean-label ingredients, and this has opened a massive growth opportunity for natural food colors. Consumers around the world are becoming more conscious about what they eat, with a rising preference for food free from artificial additives.

According to the Food and Agriculture Organization (FAO), global demand for natural food colorants has grown by nearly 7% annually in the last five years, particularly in bakery, beverages, and dairy sectors. This shift is driven by health concerns, especially around synthetic dyes like Red 40 or Yellow 5, which have been questioned for potential health impacts in children and sensitive individuals.

In India, the Food Safety and Standards Authority of India (FSSAI) has launched initiatives such as “Eat Right India,” which promotes the use of natural ingredients and discourages synthetic colorants. This campaign has pushed domestic food producers to transition to plant-based colors like beetroot red, turmeric yellow, and spirulina blue. As a result, companies are sourcing more natural alternatives—turmeric and paprika-based colors, for example, have witnessed a usage surge of 18% between 2022 and 2024, based on figures released by the Spices Board India.

Furthermore, the European Food Safety Authority (EFSA) has re-evaluated the safety of several synthetic dyes and continues to push for safer, natural options. The European Commission has updated its food additive regulations, promoting botanical extracts over artificial chemicals. This regulatory backing is creating fertile ground for manufacturers to invest in natural color innovation, particularly in beverages and confectionery, where visual appeal is key.

Trends

Natural Colors Gain Momentum as Health-Conscious Consumers Drive Market Trends

In 2025, a significant shift is observed in the food color market, with natural colors gaining substantial traction. This trend is largely driven by consumers’ growing awareness of health and wellness, leading them to prefer products free from synthetic additives. Natural food colors, derived from sources like fruits, vegetables, and spices, are increasingly favored for their perceived safety and health benefits.

In India, the Food Safety and Standards Authority of India (FSSAI) has been instrumental in promoting the use of natural food colors. The FSSAI’s regulations encourage manufacturers to adopt natural additives, aligning with the global movement towards cleaner food labels. This regulatory support has bolstered the confidence of both producers and consumers in natural food colors.

Furthermore, technological advancements have made it feasible to extract vibrant colors from natural sources without compromising on quality or stability. Innovations in extraction techniques and formulation processes have addressed previous challenges associated with natural colors, such as limited stability and color consistency.

The preference for natural food colors is also evident in the beverage industry, where consumers are increasingly opting for drinks colored with natural ingredients. This shift is not only a response to health concerns but also a reflection of the broader trend towards sustainability and environmental consciousness.

Regional Analysis

In 2024, Europe held a dominant position in the global food color market, capturing approximately 37.2% of the market share, equivalent to a valuation of around USD 1.4 billion. This leadership is attributed to a combination of stringent regulatory frameworks, a strong preference for natural ingredients, and a mature food processing industry.

The European Food Safety Authority (EFSA) plays a pivotal role in regulating food additives, including colorants, ensuring that only thoroughly assessed and approved substances are permitted for use. This rigorous oversight has fostered consumer trust and driven manufacturers to prioritize safer, often natural, coloring options.

Consumer trends in Europe have increasingly leaned towards health-conscious choices, with a significant shift from synthetic to natural food colors. Natural colorants derived from sources like beetroot, spirulina, and turmeric are gaining popularity, aligning with the clean-label movement that emphasizes transparency and minimal processing. This shift is further supported by technological advancements that have improved the stability and vibrancy of natural colors, making them more viable for a wide range of food applications.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF is a prominent chemical company that contributes to the food color market with its naturally derived colorants, including carotenoids like beta-carotene. These colorants are used to enhance the visual appeal of food and beverages while aligning with clean-label trends. BASF’s commitment to innovation and sustainability ensures they remain a key supplier in the industry.

Cargill offers a wide range of naturally colored coatings and fillings derived from plant extracts, catering to the clean-label movement in the food industry. Their solutions provide vibrant colors without the need for artificial additives, meeting consumer preferences for natural ingredients in products like éclairs, cereal bars, and lollipops.

Top Key Players in the Market

- Archer-Daniels-Midland Co.

- BASF

- Cargill

- Dohler Group

- DSM

- Ingredion, Inc.

- Kalsec, Inc.

- Koninklijke

- Lycored Ltd.

- Naturex

- Oterra

- SAN-EI GEN F.F.I. INC

- Symrise AG

Recent Developments

In 2024, DSM-Firmenich’s Food & Beverage division reported revenues of €1.9 billion, with natural food colors contributing approximately €380 million, accounting for 20% of the division’s earnings.

In 2024, Cargill reported revenues of $160 billion, a decrease from $177 billion in 2023, reflecting challenges in the global market.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 4.0 Bn |

| Forecast Revenue (2034) | USD 7.2 Bn |

| CAGR (2025-2034) | 6.0% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Natural Colors, Synthetic Colors, Nature-Identical), By Source (Plants and Animals, Minerals and Chemicals, Microorganisms), By Form (Liquid, Powder), By Solubility (Dyes, Lakes), By Application (Food Products, Beverages) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Archer-Daniels-Midland Co., BASF, Cargill, Dohler Group, DSM, Ingredion, Inc., Kalsec, Inc., Koninklijke, Lycored Ltd., Naturex, Oterra, SAN-EI GEN F.F.I. INC, Symrise AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |