Quick Navigation

Report Overview

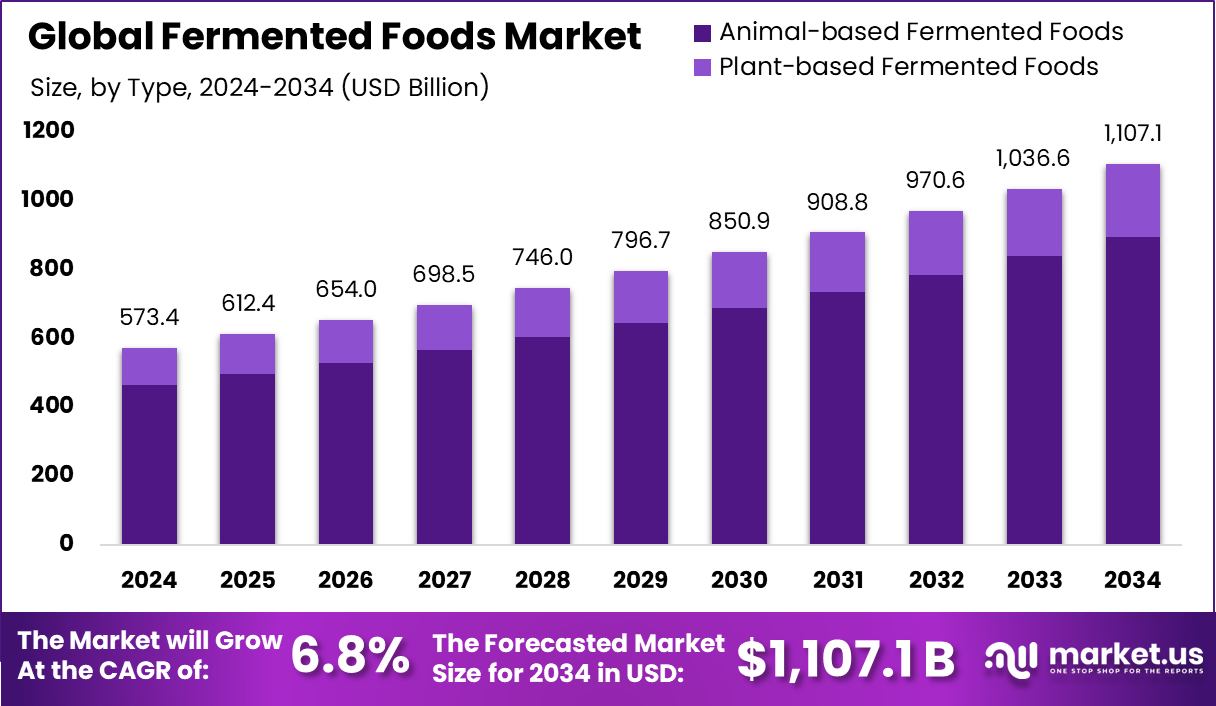

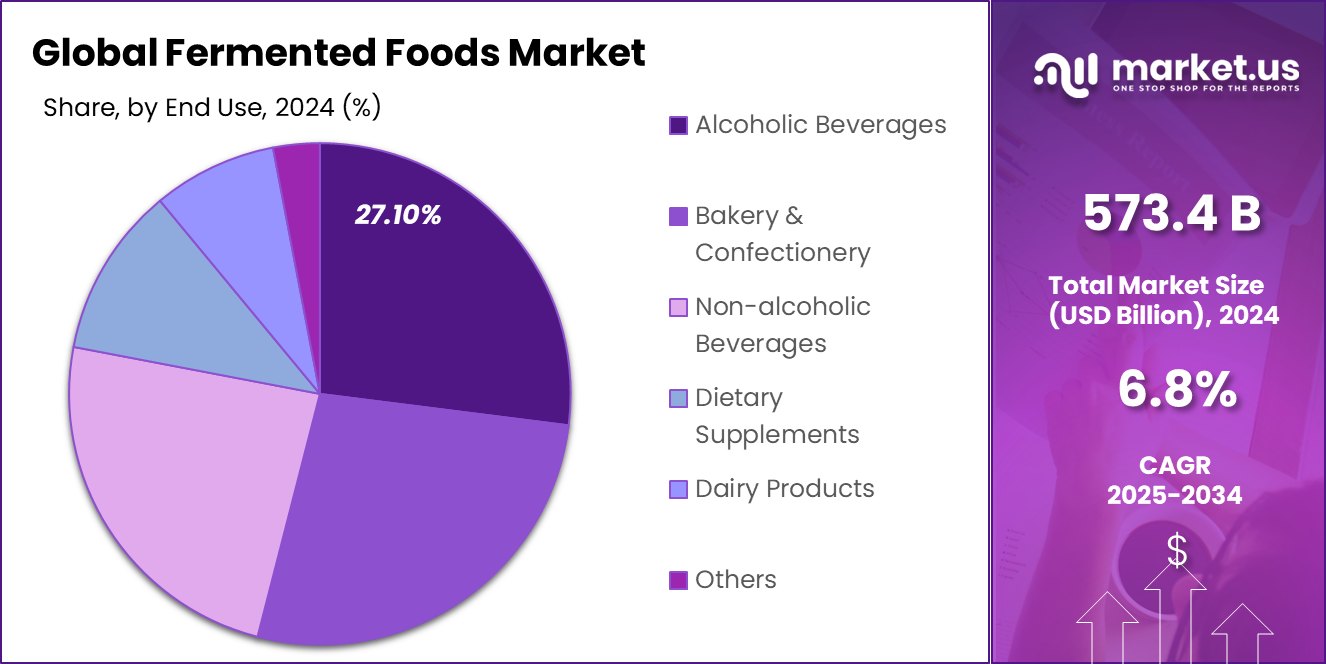

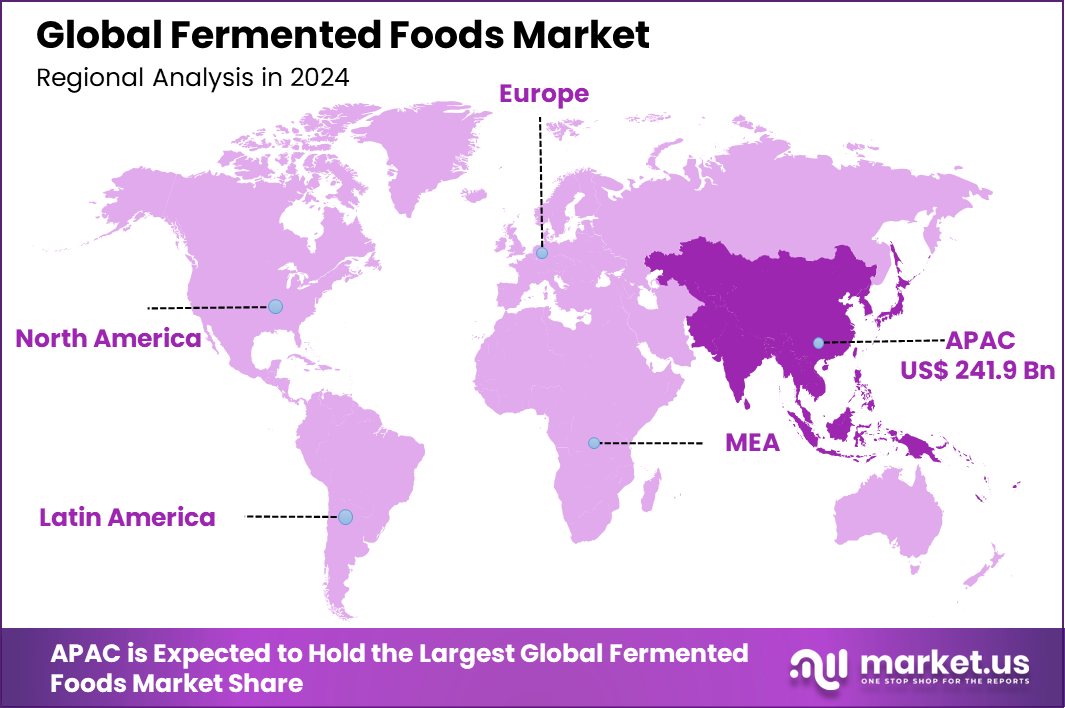

Global Fermented Foods Market is expected to be worth around USD 1,107.1 billion by 2034, up from USD 573.4 billion in 2024, and grow at a CAGR of 6.8% from 2025 to 2034. Growing awareness and demand for health-based diets boosted Asia-Pacific’s fermented foods segment to USD 241.9 billion.

Fermented Foods are foods and beverages that undergo a natural metabolic process known as fermentation, where microorganisms like bacteria, yeasts, or molds break down the sugars and starches in the food. This process not only preserves the food but also enhances its flavor and nutritional value. Examples of fermented foods include yogurt, kimchi, kefir, sauerkraut, and kombucha.

The Fermented Foods Market has been witnessing rapid growth due to rising consumer awareness about the health benefits of fermented products. The global demand is driven by an increasing preference for organic and functional foods that contribute to overall well-being. As more people seek natural and clean-label products, fermented foods have become a favored choice, especially in health-conscious consumer segments.

One of the key growth factors contributing to this market’s expansion is the growing trend of plant-based diets. As more individuals adopt vegetarian and vegan lifestyles, they are turning to plant-based fermented foods for their nutritional benefits, such as probiotics and digestive enzymes. Additionally, the increasing focus on gut health and immunity further fuels this demand.

The rising demand for fermented foods can also be attributed to the increasing availability of these products in mainstream retail stores and online platforms. With innovations in flavors and packaging, these foods have gained widespread acceptance in both developed and emerging markets.

Key Takeaways

- Global Fermented Foods Market is expected to be worth around USD 1,107.1 billion by 2034, up from USD 573.4 billion in 2024, and grow at a CAGR of 6.8% from 2025 to 2034.

- The animal-based fermented foods segment dominates the market, accounting for 81.1% of total sales.

- Anaerobic fermentation holds a significant share of 37.2% in the overall fermented foods production process.

- Alcoholic beverages represent the largest end-use category, contributing 27.1% to the global fermented foods market.

- The Asia-Pacific fermented foods market was valued at USD 241.9 billion due to high traditional consumption.

By Type Analysis

Animal-based fermented foods account for 81.1% of the fermented foods market.

In 2024, Animal-based Fermented Foods held a dominant market position in the By Type segment of the Fermented Foods Market, with an 81.1% share. This strong foothold is primarily driven by the widespread global consumption of traditional dairy-based and meat-based fermented products such as yogurt, cheese, kefir, and fermented fish. These products are deeply ingrained in dietary habits across North America, Europe, and parts of Asia, contributing significantly to their high market penetration.

The nutritional profile of animal-based fermented foods—rich in probiotics, proteins, and essential micronutrients—continues to attract health-conscious consumers. Additionally, the rise in demand for functional foods that support gut health has fueled consistent consumption in both developed and emerging markets. Established supply chains, product innovation in flavors and textures, and the rising premiumization of dairy-based fermented items have further solidified this segment’s market dominance.

Key manufacturers have also capitalized on branding, health benefit marketing, and expanding retail channels to reinforce market position. The segment benefits from a loyal customer base and high repeat purchase rates, especially in urban areas. As consumer preference continues to align with nutritional value and familiarity, animal-based fermented foods are expected to maintain their leadership in the near term within the global fermented foods market landscape.

By Fermentation Process Analysis

Anaerobic fermentation dominates the market, contributing to 37.20% of fermentation processes worldwide.

In 2024, Anaerobic Fermentation held a dominant market position in the by-fermentation-process segment of the Fermented Foods Market, with a 37.20% share. This leadership is attributed to its widespread application in producing staple fermented foods such as yogurt, kimchi, sauerkraut, and pickles. The process’s ability to preserve food naturally without oxygen while enhancing flavor and nutritional value has supported its strong adoption across both traditional and industrial food processing environments.

Anaerobic fermentation is preferred for its efficiency in maintaining product consistency, shelf stability, and probiotic integrity—factors highly valued by manufacturers and consumers alike. The method also plays a crucial role in minimizing contamination risks, making it favorable in regulated food production settings. Its compatibility with large-scale processing, especially in dairy and vegetable-based fermentation, continues to drive commercial-scale utilization.

As demand for functional foods and gut-friendly products increases, the anaerobic method remains the backbone of mass-market offerings. With well-established processing infrastructure and continued consumer preference, anaerobic fermentation is expected to maintain its top position in the fermentation process segment.

By End-Use Analysis

Alcoholic beverages represent 27.10% of the total fermented foods market segment.

In 2024, Alcoholic Beverages held a dominant market position in the by-end-use segment of the Fermented Foods Market, with a 27.10% share. This significant market presence is largely driven by the global demand for beer, wine, and spirits—products fundamentally reliant on fermentation processes. The enduring popularity of these beverages across diverse demographics and cultures has maintained steady consumption patterns in both developed and emerging economies.

An enhanced focus on flavor diversity, local sourcing, and premium ingredients has boosted demand, especially among millennials and urban populations. Additionally, alcoholic beverages benefit from strong retail visibility and robust distribution networks, further reinforcing their market leadership.

Manufacturers continue to invest in branding, packaging, and marketing strategies to target experience-seeking consumers. Moreover, fermented alcoholic products are often associated with social occasions, culinary pairing, and moderate indulgence, all of which contribute to their sustained relevance.

With established fermentation processes, regulatory frameworks, and broad consumer appeal, the alcoholic beverages segment remains a vital and profitable contributor within the fermented foods market’s end-use landscape.

Key Market Segments

By Type

- Animal-based Fermented Foods

- Dairy-Based Products

- Fermented Meats

- Others

- Plant-based Fermented Foods

- Fermented Vegetables

- Fermented Soy Products

- Others

By Fermentation Process

- Anaerobic Fermentation

- Aerobic Fermentation

- Continuous Fermentation

- Batch Fermentation

- Others

By End Use

- Alcoholic Beverages

- Bakery and Confectionery

- Non-alcoholic Beverages

- Dietary Supplements

- Dairy Products

- Animal Feed Products

- Others

Driving Factors

Rising Health Awareness Boosts Fermented Foods

One of the top drivers of the fermented foods market is growing consumer awareness around gut health and immunity. Fermented foods are rich in probiotics, which are known to support digestion, improve metabolism, and enhance overall wellness.

As people become more health-conscious—especially after the pandemic—there’s a clear shift toward foods that offer functional benefits beyond basic nutrition. Products like yogurt, kimchi, kombucha, and kefir are gaining popularity among consumers looking for natural ways to maintain good health.

This trend is strong across both developed and emerging markets. Health-focused marketing, clean labels, and the growing interest in natural food preservation methods are pushing more consumers to include fermented products in their daily diets, driving consistent market growth.

Restraining Factors

Limited Shelf Life Challenges Fermented Foods’ Growth

One key factor holding back the growth of the fermented foods market is the limited shelf life of many products. Fermented foods are often sensitive to storage conditions like temperature and humidity, which can affect their taste, texture, and safety over time.

This creates challenges in transportation, inventory management, and retail display, especially in regions with underdeveloped cold chain infrastructure. Smaller manufacturers may struggle with these logistical issues, leading to higher product losses and costs. Inconsistent product quality due to fermentation variations can also impact consumer trust.

Growth Opportunity

Plant-Based Fermented Foods Unlock New Potential

A major growth opportunity in the fermented foods market lies in the rising demand for plant-based options. With more consumers shifting toward vegan, vegetarian, and flexitarian diets, there’s a growing interest in non-dairy and meat-free fermented products.

Items like fermented soy, coconut yogurt, tempeh, kimchi, and kombucha are gaining traction for their health benefits and sustainable appeal. This trend is especially strong among younger consumers who are more eco-conscious and willing to explore new flavors.

Food companies are responding by launching innovative, plant-based fermented offerings that cater to both health and ethical concerns. As this trend grows globally, the expansion of plant-based fermented foods presents a strong opportunity for brands to tap into a fresh and fast-growing customer base.

Latest Trends

Fusion Flavors in Fermented Foods Gain Popularity

One of the latest trends in the fermented foods market is the rise of fusion flavors. Consumers today are seeking bold, unique tastes that combine traditional fermentation with global culinary influences. For example, kimchi-flavored sauces, curry-infused sauerkraut, and mango-chili kombucha are gaining popularity.

This trend is being driven by adventurous eaters, especially millennials and Gen Z, who enjoy trying new food experiences. Food brands are capitalizing on this by blending familiar fermented products with exciting flavor twists to stand out on shelves.

These innovations not only enhance taste but also attract new customers. Fusion flavors allow companies to modernize age-old fermentation methods while meeting the evolving palates of today’s global and culturally curious consumers.

Regional Analysis

Asia-Pacific dominated the Fermented Foods Market in 2024, holding a 42.20% regional market share.

In 2024, the Asia-Pacific region emerged as the dominating region in the Fermented Foods Market, accounting for a substantial 53.8% share. The regional market was valued at USD 241.9 billion, driven by the strong cultural integration of fermented foods such as kimchi, miso, tempeh, natto, and traditional pickled vegetables.

Consumer preference for naturally preserved and probiotic-rich foods significantly contributed to the region’s dominance. North America and Europe followed, supported by increasing demand for functional foods and probiotic-based dietary options. In North America, health-conscious consumers and innovation in dairy-based fermented products such as kefir and flavored yogurts supported market expansion.

Europe also maintained a steady pace due to traditional fermented products like sauerkraut, kvass, and cheese, widely consumed across various countries. Meanwhile, the Middle East & Africa, and Latin America showed moderate growth, fueled by gradually increasing awareness of digestive health and traditional fermented offerings.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, key companies such as Anheuser-Busch InBev, Archer Daniels Midland Company (ADM), and BioGaia played influential roles in shaping the global fermented foods market.

Anheuser-Busch InBev, a global leader in alcoholic beverages, continued to drive growth in the fermented alcoholic segment through its strong beer portfolio. With consumer demand shifting towards craft and premium brews, the company leveraged its global distribution network to expand its reach across North America, Europe, and emerging Asia-Pacific markets. Its investment in local breweries and flavor innovation has helped capture new age drinkers seeking authentic and diverse experiences.

Archer Daniels Midland Company (ADM) remained a prominent player through its functional ingredients and fermentation-based product offerings. ADM capitalized on the growing demand for plant-based and probiotic-enriched foods, supplying food manufacturers with high-quality fermentation cultures and enzymes. Its broad product portfolio and strong research capabilities positioned it as a key supplier supporting innovation in dairy and non-dairy fermented food categories globally.

BioGaia, a leader in probiotic solutions, focused on science-backed, gut-health-oriented fermented food products. The company’s expertise in strain development and clinical validation gave it a competitive edge in functional fermented foods, particularly in Europe and Asia. BioGaia’s strong partnerships with food and pharmaceutical companies enhanced its ability to penetrate health-conscious consumer segments.

Top Key Players in the Market

- Anheuser-Busch InBev

- Archer Daniels Midland Company

- BioGaia

- Cargill, Inc.

- Chobani Inc.

- Constellation Brands, Inc.

- Danone SA

- Dupont De Nemours and Company

- Fonterra Co-operative Group Limited

- Kraft Heinz

- Lactalis Group

- Mondelez International

- Nestlé SA

- PepsiCo, Inc.

- Unilever

- Yakult Honsha Co. Ltd

Recent Developments

- In 2024, BioGaia grew steadily with SEK 1,422.7M in sales, driven by strong probiotics demand. Pediatric and Adult Health segments rose 8% and 17% respectively, reflecting consumer trust. Operating profit reached SEK 423.4M, highlighting efficient and focused business growth.

- In 2022, Anheuser-Busch InBev inaugurated a facility with EverGrain to transform used brewing grains into protein-rich ingredients, promoting sustainability and resource efficiency.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 573.4 Billion |

| Forecast Revenue (2034) | USD 1,107.1 Billion |

| CAGR (2025-2034) | 6.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Animal-based Fermented Foods(Dairy-Based Products, Fermented Meats, Others), Plant-based Fermented Foods (Fermented Vegetables, Fermented Soy Products, Others)), By Fermentation Process (Anaerobic Fermentation, Aerobic Fermentation, Continuous Fermentation, Batch Fermentation, Others), By End Use (Alcoholic Beverages, Bakery and Confectionery, Non-alcoholic Beverages, Dietary Supplements, Dairy Products, Animal Feed Products, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Anheuser-Busch InBev, Archer Daniels Midland Company, BioGaia, Cargill, Inc., Chobani Inc., Constellation Brands, Inc., Danone SA, Dupont De Nemours and Company, Fonterra Co-operative Group Limited, Kraft Heinz, Lactalis Group, Mondelez International, Nestlé SA, PepsiCo, Inc., Unilever, Yakult Honsha Co. Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |